Following reports over the weekend, the Treasurer has confirmed that the Productivity Commission will examine competition in Australia’s financial system. This includes a consideration of vertical and horizontal integration and access to banking services for small business.

The Government is committed to ensuring that Australia’s financial system is competitive and innovative.

That is why I have tasked the Productivity Commission to hold an inquiry into competition in Australia’s financial system. Competition is central to the Government’s plans to support innovation and economic growth, and deliver better outcomes for consumers and small businesses.

This delivers on the Turnbull Government’s commitment to task the Productivity Commission to review the state of competition in the financial system, made as part of the Government’s response to the Financial System Inquiry.

The Productivity Commission will look at how to improve consumer outcomes, the productivity and international competitiveness of the financial system and economy more broadly, and support financial system innovation, while balancing financial stability objectives.

In doing so it will consider the level of contestability and concentration in key segments of the financial system, including the degree of vertical and horizontal integration. It will also examine competition in the provision of personal deposit accounts and mortgages and services and finance to small and medium businesses.

The Government encourages all parties with an interest in competition in the financial system to consider making a submission to the Commission.

The Inquiry will commence on 1 July 2017 and is due to report to the Government by 1 July 2018.

Further information and the terms of reference will be available on the Commission’s website.

The customer owned banking sector welcomes today’s announcement by the Treasurer of a Productivity Commission (PC) inquiry into the state of competition in the financial system.

“The enduring solution to concerns about the banking market is action to promote sustainable competition so that poor conduct is swiftly punished by loss of market share,” said COBA CEO Mark Degotardi.

“Customer owned banking institutions – mutual banks, credit unions and building societies – are eager to build on their 4-million strong customer base, but we need a fairer regulatory framework.

“Fast-tracking this PC inquiry was our top policy priority for the 2017-18 Budget so we are delighted it has been unveiled a day early.

“Consumers stand to gain from a more competitive banking market where all competitors have a fair go.

“Currently, major banks benefit from unfair regulatory capital settings and a free subsidy from taxpayers in the form of an implicit guarantee that significantly lowers their cost of funding.

“These problems can be addressed by the PC as well as measures to empower consumers to more easily find the best deal for them on a savings account, credit card or home loan.

“This PC inquiry was recommended by the Financial System Inquiry because the current regulatory framework suffers from ‘complacency’ about competition.

“COBA believes one way to tackle this problem is to give the powerful banking regulator APRA an explicit ‘secondary competition mandate’ and an obligation to report annually against this mandate.

“We look forward to engaging with the PC inquiry, particularly on removing barriers to innovation and competition.”

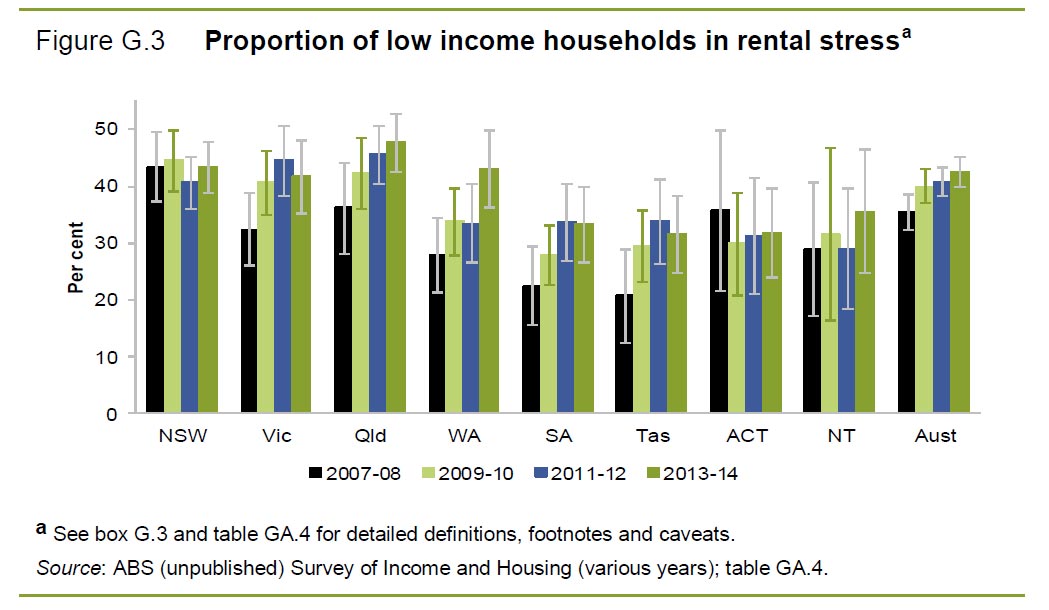

The latest report from the Productivity Commission “Report on Government Services 2017, Volume G: Housing and homelessness” shows rental stress is on the rise. Nationally, the proportion of low income renter households in rental stress increased from 35.4 per cent in 2007-08 to 42.5 per cent in 2013-14.

In addition, the report included data on Commonwealth Rent Assistance (CRA) showing a rise in payment to reduce rental stress, of $4.4 billion in 2015-16. A further hidden impact of high housing costs.

CRA helps eligible people meet the cost of rental housing in the private market, aiming to reduce the incidence of rental stress. It is an Australian Government non-taxable income supplement, paid to recipients of income support payment, ABSTUDY, Family Tax Benefit Part A, or a Veteran’s service pension or income support supplement.

Australian Government expenditure on CRA was $4.4 billion in 2015-16, increasing in real terms from $3.6 billion in 2011-12. The average government CRA expenditure per eligible income unit was $3251 in 2015-16.

Nationally in June 2016, there were 1 345 983 income units receiving CRA . Of these, 79.4 per cent paid enough rent to be eligible to receive the maximum rate of CRA (an increase from 75.0 per cent in 2012).

The median CRA payment at June 2016 was $130 per fortnight, with median rent being $437 per fortnight.

CRA and rental stress

Rental stress is defined as more than 30 per cent of household income being spent on rent, and is a separate sector-wide indicator. CRA is indexed to the Consumer Price Index (CPI) but rental costs have increased at a faster rate than the CPI since 2008 (ABS 2016), so the real value of CRA payments has decreased for individuals in that time.

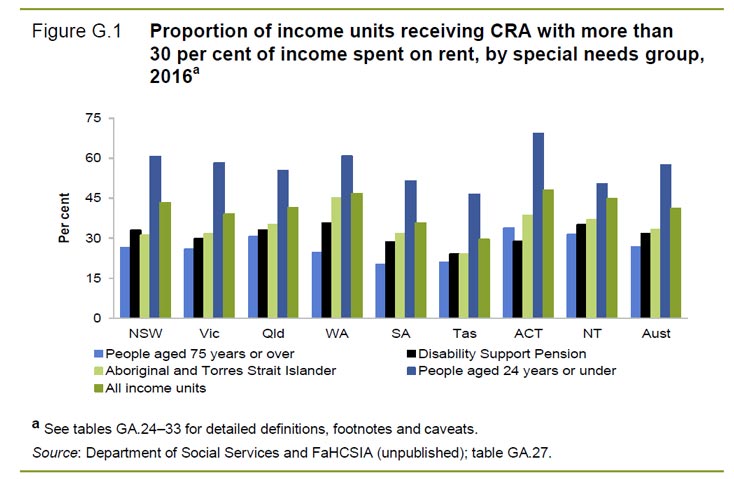

Nationally in June 2016, 68.2 per cent of CRA income units would have paid more than 30 per cent of their gross income on rent if CRA were not provided — with CRA this proportion was 41.2 per cent.

The table below presents a range of CRA data, including Australian Government expenditure and information on CRA income units — including Aboriginal and Torres Strait Islander recipients, those with special needs — and those in rural and remote areas.

They conclude that copyright protection in Australia suffers from a number of shortcomings. It is overly broad, applying equally to: commercial and non-commercial works; works with very low levels of creative input; works that are no longer being supplied to the market; and works where ownership can no longer be identified. Further, copyright does not target those works where ‘freeriding’ by users would undermine incentives to create new works. As such, Australia’s copyright arrangements are skewed too far in favour of copyright owners to the detriment of consumers and intermediate users.

Copyright protects literary, musical, dramatic and artistic works for the duration of the creator’s life plus 70 years, sound recordings and films for 70 years, television and sound broadcasts for 50 years, and published editions for 25 years. To provide a concrete example, a new work produced in 2016 by a 35 year old author who lives until 85 years of age will be protected until 2136. Evidence (and logic) suggests copyright protection lasts far longer than is needed.

The Australian Government should make clear that it is not an infringement of Australia’s copyright system for consumers to circumvent geoblocking technology and should avoid international obligations that would preclude such practices.

The scope from August 2015 was “The Australian Government wishes to ensure that the intellectual property system provides appropriate incentives for innovation, investment and the production of creative works while ensuring it does not unreasonably impede further innovation, competition, investment and access to goods and services”.

Here are the main findings.

Australia’s intellectual property (IP) arrangements fall short in many ways and improvement is needed across the spectrum of IP rights.

• IP arrangements need to ensure that creators and inventors are rewarded for their efforts, but in doing so they must:

− foster creative endeavour and investment in IP that would not otherwise occur

− only provide the incentive needed to induce that additional investment or endeavour

− resist impeding follow–on innovation, competition and access to goods and services.

• Australia’s patent system grants exclusivity too readily, allowing a proliferation of low-quality patents, frustrating follow–on innovators and stymieing competition.

− To raise patent quality, the Australian Government should increase the degree of invention required to receive a patent, abolish the failed innovation patent, reconfigure costly extensions of term for pharmaceutical patents, and better structure patent fees.

• Copyright is broader in scope and longer in duration than needed — innovative firms, universities and schools, and consumers bear the cost.

− Introducing a system of user rights, including the (well-established) principles–based fair use exception, would go some way to redress this imbalance.

• Timely and cost effective access to copyright content is the best way to reduce infringement. The Australian Government should make it easier for users to access legitimate content by:

− clarifying the law on geoblocking

− repealing parallel import restrictions on books. New analysis reveals that Australian readers still pay more than those in the UK for a significant share of books.

• Commercial transactions involving IP rights should be subject to competition law. The current exemption under the Competition and Consumer Act is based on outdated views and should be repealed.

• While Australia’s enforcement system works relatively well, reform is needed to improve access, especially for small– and medium–sized enterprises.

− Introducing (and resourcing) a specialist IP list within the Federal Circuit Court (akin to the UK model) would provide a timely and low cost option for resolving IP disputes.

• The absence of an overarching objective, policy framework and reform champion has contributed to Australia losing its way on IP policy.

− Better governance arrangements are needed for a more coherent and balanced approach to IP policy development and implementation.

• International commitments substantially constrain Australia’s IP policy flexibility.

− The Australian Government should focus its international IP engagement on reducing transaction costs for parties using IP rights in multiple jurisdictions and encouraging more balanced policy arrangements for patents and copyright.

− An overdue review of TRIPS by the WTO would be a helpful first step.

• Reform efforts have more often than not succumbed to misinformation and scare campaigns. Steely resolve will be needed to pursue better balanced IP arrangements.

The transition from the mining investment boom to broader-based growth is underway. This transition is occurring at the same time as our economy is reconciling the impacts of globalization, technological and environmental change.

By its nature, the geography of our economic transition will not be consistent across the country.

The combination of forces driving the transition of our economy will unavoidably create friction points in specific regional areas and localities across the country, while being the source of considerable growth and prosperity in others.

The different impacts across the geographic regions of the Australian economy occur because of variable factors such as endowments of natural resources and demographics. Some regions may also have limited capacity to respond to changes in economic conditions; for example, due to different policy or institutional settings.

Scope of the research study

The purpose of this study is to examine the regional geography of Australia’s economic transition, since the mining investment boom, to identify those regions and localities that face significant challenges in successfully transitioning to a more sustainable economic base and the factors which will influence their capacity to adapt to changes in economic circumstances.

The study should also draw on analyses of previous transitions that have occurred in the Australian economy and policy responses as a reference and guide to analysing our current transition. The Commission should consult with statistical agencies and other experts.

In undertaking the study, the Commission should:

Identify regions which are likely, from an examination of economic and social data, to make a less successful transition from the resources boom than other parts of the country at a time when our economy is reconciling the impacts of globalization, technological and environmental change.

For each such region, identify the primary factors contributing to this performance. Identify distributional impacts as part of this analysis.

Establish an economic metric, combining a series of indicators to assess the degree of economic dislocation/engagement, transitional friction and local economic sustainability for regions across Australia and rank those regions to identify those most at risk of failing to adjust.

Devise an analytical framework for assessing the scope for economic and social development in regions which share similar economic characteristics, including dependency on interrelationships between regions.

Consider the relevance of geographic labour mobility including Fly-In/Fly-Out, Drive-In/Drive-Out and temporary migrant labour.

Examine the prospects for change to the structure of each region’s economy and factors that may inhibit this or otherwise prevent a broad sharing of opportunity, consistent with the national growth outlook.

Process

The Commission is to undertake an appropriate public consultation process including consultation with Commonwealth, State and Territory governments, as well as local government where appropriate.

The final report should be provided within 12 months of the receipt of these terms of reference, with an initial report provided in April.

The Productivity Commission has issued a Draft Report for comment on Data Availability and Use in Australian. If the recommendations are adopted this could become a fundamental force for change, and potentially create economic momentum, and greater competition from which consumers may benefit. There is enormous untapped potential in Australia’s data.

Crucially, the proposed reforms take Australia beyond the stage of viewing data availability solely through a privacy lens, in recognition that there is much more than privacy at stake when it comes to data availability and use. Tweaking existing structures and legislation will not suffice. Rather, fundamental and systematic changes are needed to the way Australian governments, business and individuals handle data.

In a nutshell, data currently collected via digital transactions would remain the property of the individual (rather than the company who happened to collect it), and this data could be traded by said consumer in return for better outcomes. The report also defines a hierarchy of data types, some of which would be private, and others more widely accessible.

By way of background, the review, was requested by Scott Morrison, Treasurer, following on from the 2014 Financial System Inquiry (the Murray Inquiry) which recommended that the Government task the Commission to review the benefits and costs of increasing the availability and improving the use of data. In addition, the 2015 Harper Review of Competition Policy recommended that the Government consider ways to improve individuals’ ability to access their own data to inform consumer choices. The Government agreed to pursue these two recommendations.

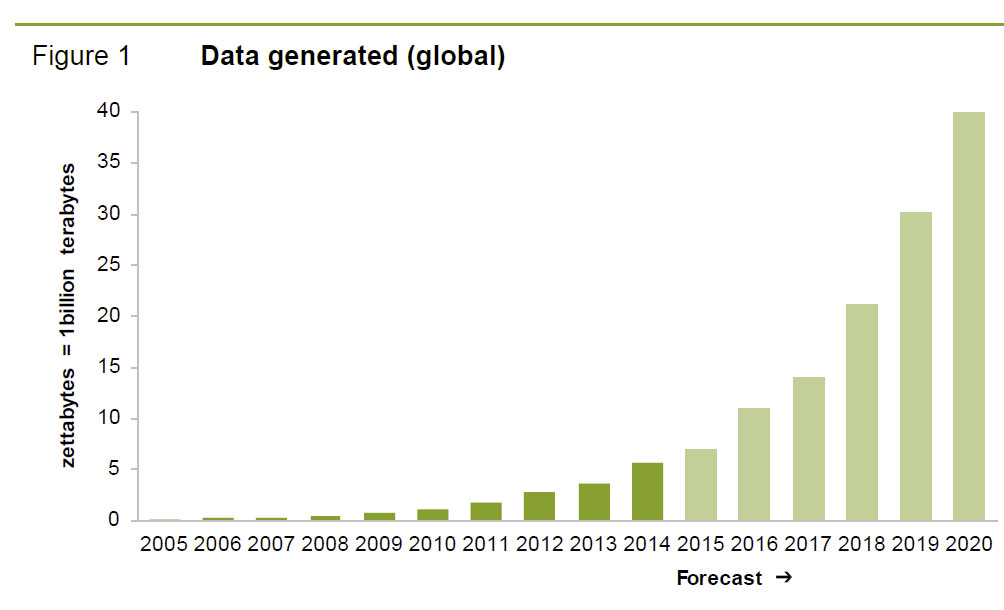

This is an important issue. On one hand, by some estimates, the amount of digital data generated globally in 2002 (five terabytes) is now generated every two days, with 90% of the world’s information generated in just the past two years.

Yet we are now only in the very nascent stage of the Internet of Things (whereby our business equipment, vehicles, appliances and wearable devices can communicate with each other and generate data), the upward trend in data generated is more likely than not to accelerate into the future.

The legal and policy frameworks under which public and private sector data is collected, stored and used (or traded) in Australia are ad hoc and not contemporary. The impetus for changes in governance structures around data — changes that deal head-on with the fact that data is increasingly digital, revealing of the activities and preferences of individual people or businesses, and held in the private sector — will not diminish. It is a global movement and, to its detriment, Australia is not participating.

Falling costs (per record) of digital data storage, and the spread of low-cost and powerful analytics tools and techniques to extract patterns, correlations and interactions from within data, are also making data analytics more usable and valuable. Yet much of the data being generated remains underutilised. Some estimate that up to 80% of data generated globally may prove to have no value (numerous duplicative digital photos, for example). But still, less than 5% of the potentially useful data is actually analysed to generate information, build knowledge, and thus inform decision making and action (EMC Corporation 2014). And some data that was previously of limited value is becoming valuable as new uses for it emerge, analytical capabilities improve, new linkages are established, or investments made to improve its quality. There is enormous untapped potential in Australia’s data.

In addition, whilst privacy is often said to be a concern, individuals still willingly and readily hand over personal information may seem a paradox. There are risks attached.

Because much of the data that is being generated is a byproduct of other activities, it was once easy for individuals to dismiss it as being of secondary importance. Today, that should not be the case. If you are using a product or service and not paying for it (or sometimes even when you are), then you are the product. This is perhaps most obvious by the ‘all or nothing’ nature of personal data requested in exchange for typically free online products and services. What you are consuming, how and when you are consuming it, is all being collected as data that is likely of more value to the supplier than whatever it is they are offering you.

Here is a summary of their main points:

Frameworks and protections developed for data collection and access prior to sweeping digitisation now need reform. This is a global phenomenon and Australia, to its detriment, is not yet participating.

The substantive argument in favour of making data more available is that opportunities to use it are largely unknown until the data sources themselves are better known, and until data users have been able to undertake discovery of data.

Lack of trust and numerous barriers to sharing and releasing data are stymieing the use and value of Australia’s data.

Marginal changes to existing structures and legislation will not suffice. The Commission is proposing reforms to data availability and use, aimed at moving from a system based on risk aversion and avoidance, to one based on transparency and confidence in data processes.

At the centre of proposed reforms is the introduction of a new Data Sharing and Release Act, a new National Data Custodian, and a suite of sectoral Accredited Release Authorities that will enable streamlined access to curated datasets.

A key element of the recommended reforms is to provide greater control for individuals over data that is collected on them by defining a new Comprehensive Right for consumers. This right would mean consumers:

– retain the power to view information held on them, request edits or corrections, and be advised of disclosure to third parties;

– have improved rights to opt out of collection in some circumstances; and

– have a new right to a machine-readable copy of data, provided either to them or to a nominated third party, such as a new service provider.

Broad access to key National Interest Datasets should be enabled.

– For datasets designated as national interest, all restrictions to access and use contained in a variety of national and state legislation, and other program-specific policies, would be replaced by new arrangements under the Data Sharing and Release Act.

– Datasets would be maintained as national assets, access would be substantially streamlined, and linkage with other National Interest Datasets would be feasible.

– Initial datasets that may be designated national interest and publicly released could include key registries of businesses, services or assets, and data on activity and usage in areas of substantial public expenditure.

Secure sharing of identifiable data held in the public sector and by publicly funded research bodies should be formalised and streamlined. By pre-approving data uses, trusted users would have more timely access to identifiable data through Accredited Release Authorities and ethics committees.

Reforming access to public sector data is a priority. Significant change is needed for Australia’s open government agenda to catch up with achievements in competing economies.

The incremental costs associated with more open data access and use — including possible impacts on individuals’ privacy and willingness to share data — are expected to be minimal, but they will exist. But greater use of Australia’s data can coexist with the management of these risks, including genuine safeguards and meaningful transparency to maintain community trust and confidence.

The Commission’s recommended approach incorporates recent progress in policy and practices around data management but is deliberately aimed at creating a new, comprehensive framework that should, by design, be capable of enduring beyond current policies, personnel and institutional structures. It takes account of the significant differences in data types and associated risks and uses of each, and recognises that while the incremental risks of making data more available might appear very small (given how much data is already in the public domain), incentives and trust nevertheless have to be maintained.

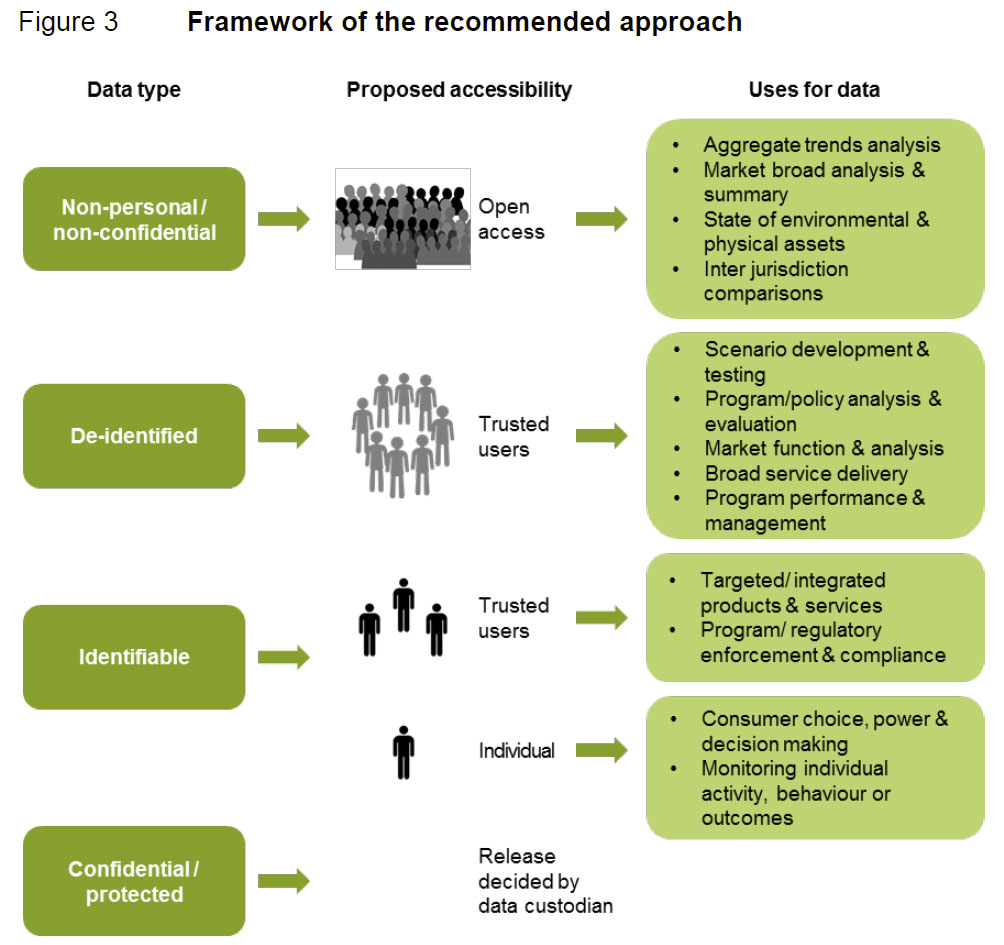

As part of the review, the Commission has developed a framework for their recommended approach.

They have given considerable thought to establishing an element in the Framework to enable wider access to high value, National Interest Datasets. The intention is to promote the development of a valuable suite of datasets — some of which are released publicly; others that will be shared with a smaller group of trusted data users. Designating datasets as national interest collections will also signify their value as resources collected in the national interest, not merely (as today) for compliance, record-keeping or audit.

The implications for companies who possess data – like the banks – might be shocked by the implications. Expect some resistance. That said, they see to consider comprehensive credit reporting something of a special case.

In some circumstances, collating consumer data may offer net public benefit in making markets more efficient. A specific case is covered in the terms of reference for this Inquiry: comprehensive credit reporting. The Productivity Commission has previously found comprehensive credit reporting to be desirable and, consistent with the approach of New Zealand, the United Kingdom and the United States, a voluntary approach to data input should continue to be pursued, unless it becomes clear that a critical mass of accounts is not achievable on that basis.

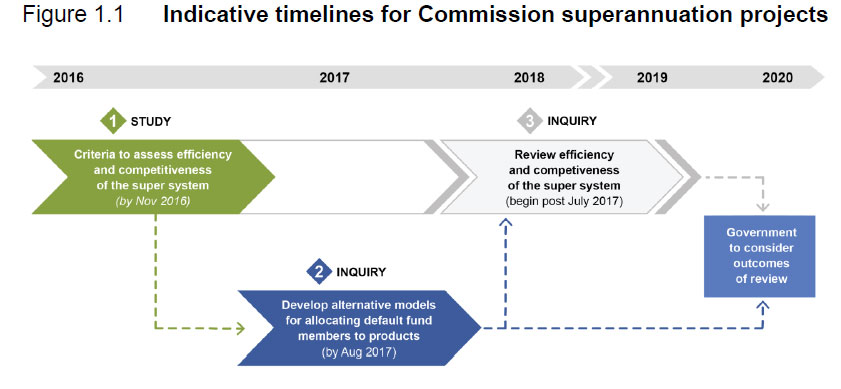

The Productive Commission has released an issues paper as part of its inquiry into the superannuation system. This starts to unpick the complex maze of issues surrounding superannuation and is part of the mandate from February 2016 given by the Government “to conduct: a study to develop criteria to assess the efficiency and competitiveness of the superannuation system; and an inquiry to develop alternative models for a formal competitive process for allocating default fund members to products”. The inquiry is part of a three stage process running to 2020.

The concept of defaults (and their presence in workplace instruments) has been integral to the development of Australia’s superannuation system, largely stemming from the decision to make superannuation compulsory and the inherent complexity that individuals face in making decisions about retirement incomes. Having no defaults is their preferred, objective baseline for this inquiry. Alternative allocative models would be assessed against this baseline, and their relative performance against the agreed assessment criteria.

They make the point that default superannuation arrangements in Australia have primarily arisen out of the workplace relations system, though employees not employed under the national system are generally covered by state‑based systems.

MySuper was introduced in 2013. MySuper products were designed to be simple and cost‑effective superannuation products replacing previous default products. The intention was to ensure members do not pay for any unnecessary features they do not need or use.

For the purposes of this inquiry, the Commission will be developing models to allocate default fund members (employees who do not make an active choice about their superannuation fund) to defaultproducts. There is no intermediate decision of selecting a default fund.

The Commission proposes to assess alternative models against five criteria:

members’ best interests: meeting the best interests of members, by maximising long‑term net returns and allocating members to products that meet their needs

competition: fostering competition between funds that drives innovation and cost reductions, facilitates new entrants to the market (contestability) and leads to efficient long‑term outcomes

integrity: minimising scope for the allocation process to be manipulated (or ‘gamed’), including by using clear metrics that are difficult to dispute and by holding funds accountable for the outcomes they deliver to members

stability: supporting a stable superannuation system, including by building trust and confidence in funds regulated by APRA

system‑wide costs: minimising the total costs to members, employers and funds, including costs associated with regulatory compliance, complexity, ‘churn’ and ‘gaming’, and minimising costs to government of implementing and administering the models.

The five criteria collectively capture competition and efficiency. These criteria essentially relate to the benefits and costs of each model, and will be assessed from the perspective of the community as a whole. As noted, the Commission proposes to assess benefits and costs relative to a baseline scenario of no default system.

Some of the models being tabled are:

Administrative model

In an administrative model, a government body would use a ‘filter’ to determine which products are eligible to be used as defaults. This filter (the regulatory mechanism) would be akin to a set of minimum standards that products must meet. The filter would not rank the relative performance of products.

Market‑based models

A market‑based model would involve some form of explicit and formalised process through which products compete to be deemed eligible as defaults: in other words, some form of a tender or reverse auction process. Numerous variations in design have been proposed in the literature and exist in practice. However, at its heart, the market model involves superannuation funds bidding for the right to receive contributions from default members.

Active choice by employees

The baseline to be used in this inquiry is that there is no default system at all. After nearly 25 years’ experience, it could be even argued that this itself be a new allocation model, where employees themselves must make an active choice of superannuation product. This would remove the employer’s responsibility for choosing a default fund and place the onus on the employee, who may be better placed to make a decision in his or her own best interests. However, research on an active choice model (without defaults) is scarce. Most countries that have employer‑funded superannuation also have some variant of a default option.

An active choice model need not be completely decentralised. A filter or a market‑based mechanism could be used to narrow choices or ‘nudge’ members to high‑performing fund.

They are seeking submissions and alternative suggestions for models by 28 October 2016.

The Productivity Commission has released its draft report on the Superannuation Industry, which outlines a framework for a review over the next few years. The report says that information about funds are confusing and incomplete. As a result, even the most literate households in the community have difficulty in choosing between funds. Many put off making decisions about super until close to retirement.

However, the review process as outlined in the report is long-winded, and as a result, little will change for several years.

This study is stage 1 of a 3 stage process, and stems from the Australian Government’s response to recommendations made in the 2014 Financial System Inquiry (FSI). Stage 1 involves developing criteria to assess the efficiency and competitiveness of the system.

Many recent reviews, including the FSI, have made observations relating to perceived shortcomings in the system. The criteria developed in this study will provide a useful and enduring framework for any future assessments (including by regulators) and reforms.

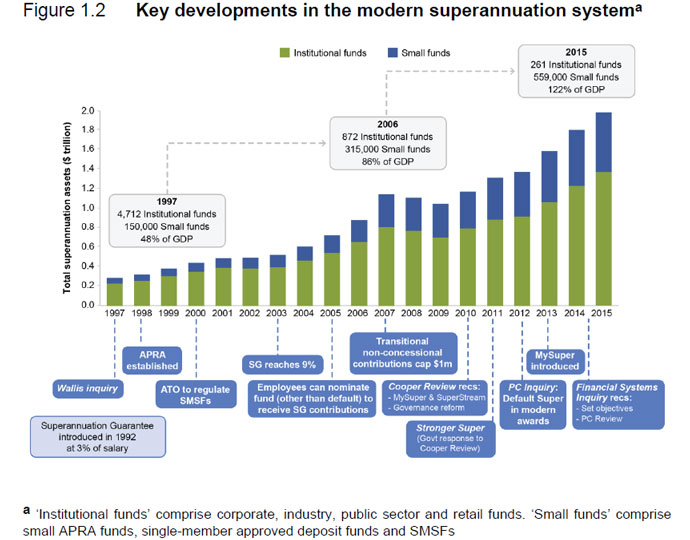

Currently, there is about $2 trillion in funds under management held by over 250 institutional funds and over 556 000 self-managed superannuation funds. The average account balance is just over $67 000. But averages can be misleading, given the distribution of account balances.

This study stems from the recommendations of the 2014 Financial Services Inquiry (FSI), which considered some of the issues in the superannuation system as part of a broader review of the performance of the Australian financial system. The FSI suggested a Productivity Commission inquiry into the efficiency and competitiveness of the superannuation system should occur by 2020.

In response, the Government tasked the Commission to develop and release criteria to assess the efficiency and competitiveness of the superannuation system (stage 1). These criteria will then be used to inform a review of the system following the full implementation of the MySuper reforms by mid-2017 (stage 3). While aspects of the Australian superannuation system have been reviewed in the past, stage 3 will be the first comprehensive review specifically assessing the efficiency and competitiveness of the entire system.

The Commission has also been tasked with examining alternative models for a formal competitive process for allocating default fund members to products (stage 2). The Commission will begin work on stage 2 in late September. Indicative timelines for the three stage process are outlined in figure 1.1.

The super industry has evolved to the point where around 20% of household assets are in the sector, worth more than $2 trillion. The number of accounts peaked at about 32 million in 2009-10, and is now down to just under 30 million. The number of small funds has been driven by the increasing popularity of SMSFs. In 2001, there were about 210 000 SMSFs, but this had more than doubled to over 550 000 by June 2015.

The level of funds under management and average account balances should continue to increase at substantial pace over the next few decades. Most projections forecast continued strong growth until the mid-2030s with between $5 trillion and $6.3 trillion under management, representing between 130 to 180 per cent of GDP, depending on the assumptions employed. Despite the projected growth in absolute size, there is still some uncertainty about whether a mature system in the 2030s will actually provide adequate retirement incomes, although sometimes it can be difficult to distinguish substance from self interest in such claims.

They highlight that the super market is unique, as demand is driven by government policy around compulsory contributions and concessional tax treatment. Many participants though are constrained from making an active choice, the system uses a default model and there are “cognitive constraints and behavioural biases”. Moreover, there are more than 40,000 investment products offered by funds. However, as a defined contribution scheme, risks fall to the members.

The system is highly regulated, and principal-agent relationships abound.

They conclude “The design, size, diversity and complexity of the superannuation system distinguish it from typical markets. Therefore the assessment framework has a focus on incentives and drivers (inputs or processes) of particular outcomes, as well as the outcomes themselves. Importantly, no single criterion or indicator can be used to adequately assess its competitiveness and/or efficiency. In some cases, the assessment will focus on a particular element of the system and in other cases, the system as a whole. Finally, the assessment framework will need to be sufficiently flexible to accommodate the dynamic and segmented nature of the system and policy-induced constraints on the system’s competitiveness and efficiency.”

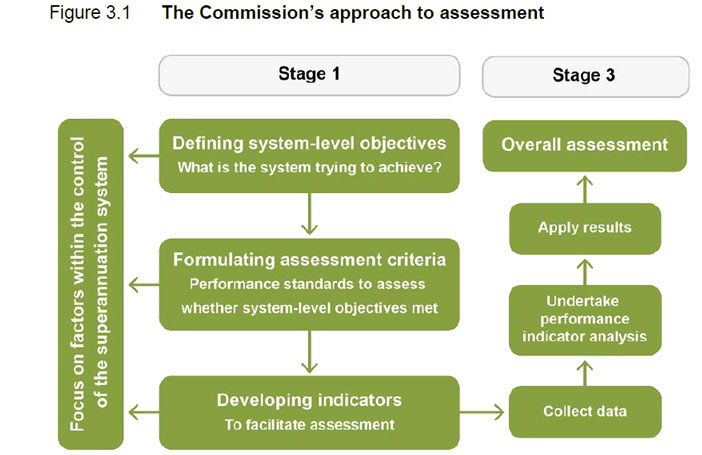

The report then describes the Commission’s approach to the assessment of the system.

Beyond that, they also describe some of the mechanics within the system which will also be investigated though the review along with governance and regulation.

The deadline for making a written submission to the Productivity Commission on the framework in the report is Friday 9 September 2016.