The AFR says Bankwest has changed its affordability calculators for investor loans, such that the tax benefits are now excluded from the assessment. This reduces the amount prospective investors can get in a loan, and it also may impact some existing customers.

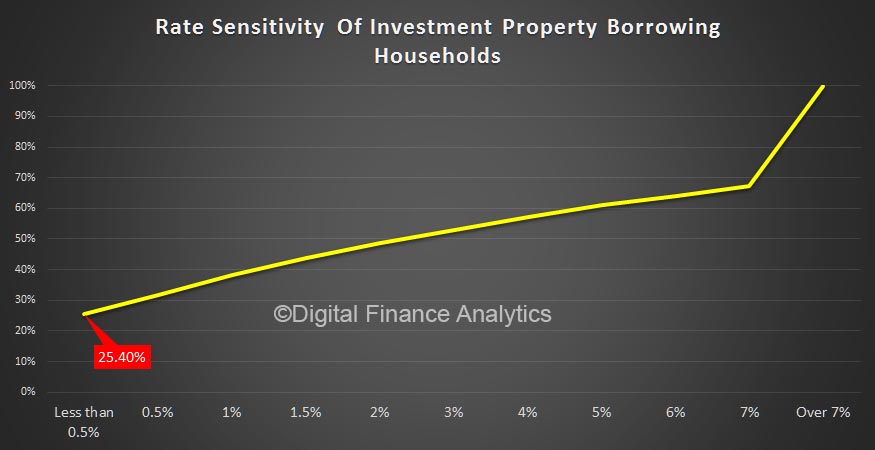

The post-tax affordability assessment explains why on one hand some banks have been able to lend hard on investor loans yet on the other hand, on a pre-tax basis many investors have little wriggle room if rates raise, as we highlighted recently.

Note though that not all lenders were so generous in their handling of tax benefits, and Bankwest appears now to have revised their approach to meet APRA guidelines – see specifically APG 223 within the Residential Mortgage Lending prudential practice guide.

Another market change which will further rightly tighten investor lending.

Another market change which will further rightly tighten investor lending.

The move was confirmed by The Real Estate Conversation.

Bankwest has confirmed it will remove the tax advantages of negative gearing when determining whether or not applicants are eligible for investor loans.

The changes will mean the amount investors can borrow will be lower, and could result in the bank, a subsidiary of the Commonwealth Bank, writing fewer investment loans.

The Commonwealth Bank is expected to announce similar moves.

The Australian Financial Review reports of speculation Bankwest and the Commonwealth Bank are close to breaching the Australian Prudential Regulation Authority’s 10 per cent growth cap for investor loans.

Mark Chapman, a director of tax accountants H&R Block, told The Australian Financial Review the change would be most dramatic for existing borrowers, who will have to deal with altered rules.

“The impact of Bankwest’s decision on new borrowers is not too bad – they can just borrow through another bank,” he said. But for existing BankWest borrowers, the change is retrospective he said.

“They borrowed in good faith from this bank under one set of rules, now they are having another set of rules imposed on them.”

“For customers who operate their investment property at a loss, where the income of the investment property does not exceed the costs, the related tax benefit will no longer be included in Bankwest’s calculation for serviceability of the loan,” the spokesperson said.

The changes will impact all new applications involving an investment lending facility as well as any existing deals which may require a new serviceability calculation.