In this extended show I discuss property investment, asses classes, risks, and fractional reserve banking (versus credit creation) with Adam Stokes, who runs a channel on YT with a focus on Crypto.

This is my version of the show, Adam posted his on his channel at https://youtu.be/OrXUlTuBBqE

You can find our earlier discussion here: https://youtu.be/m8RQztfl78c

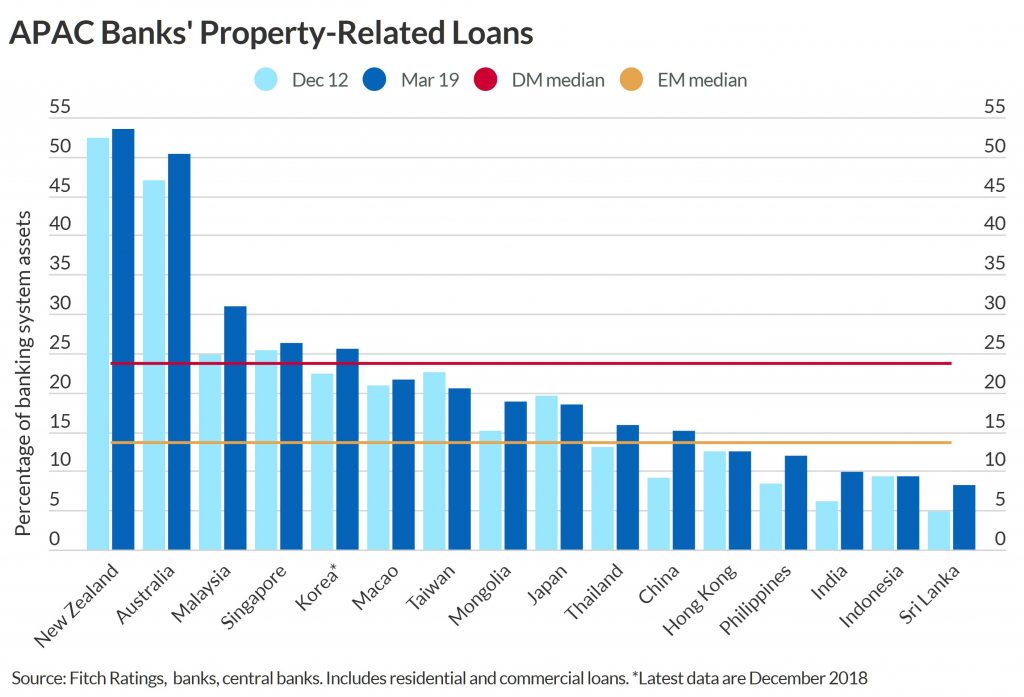

Banks in the Asia-Pacific region are increasingly exposed to property-related risks, Fitch Ratings says in a new report. The Australian and New Zealand banking sectors have the greatest exposure to property market stress, while banks in Sri Lanka, Mongolia and Vietnam have the least protection from loss-absorption buffers. We believe that regulatory oversight and macro-prudential policies should contain the direct effect of a residential property downturn on banks, especially in developed markets where loss-absorption buffers tend to be higher. However, accommodative monetary and economic policies could aggravate leverage.

Rising household debt increases risks for banks as borrowers’ debt-servicing capacity becomes more sensitive to economic factors, and a high reliance on property to collateralise loans exposes banks in a property market downturn. Regulators in most of the region’s developed markets have introduced macro-prudential measures to stem property-sector risks and to strengthen banking-sector resilience to potential property stress. We believe that policymakers will remain focused on measures that support stability and prevent risks of overheating, despite recent macro-prudential loosening in Australia, New Zealand and Taiwan to support their economies. We expect Hong Kong, Singapore and South Korea to maintain the tighter bias in their policy settings.

In general, developed economies in Asia have higher banking-sector exposure to property and more indebted household sectors than emerging countries. Australia and New Zealand are two stand-out cases, with household debt-to-GDP ratios of 129% and 94%, respectively, at end-2018. However, banking systems in developed markets have more experience of managing property cycles and stronger loss-absorption buffers, and the authorities’ proactive approach should cushion the impact on banks from a property market stress.

In emerging countries, banks’ exposure to the property sector tends to be lower, but risks are building in light of their strong property lending in recent years, due in part to governments relying increasingly on property to support their economies. Rapid credit growth often masks asset-quality issues, and rising property exposure makes banks more vulnerable to a property downturn, particularly where loss-absorption buffers are lowest (Mongolia, Sri Lanka and Vietnam). Property-related risks in India and Sri Lanka may be understated due to indirect exposures and limited data transparency.

Vietnamese banks appear susceptible in light of rapid consumer loan growth coupled with large legacy bad-debt issues and thin capital buffers. That said, a significant deterioration in Vietnam’s property market seems remote amid strong economic prospects.

In China, banks’ property

exposure has increased significantly over the past decade, but only to

15% of banking sector assets at end-March 2019, while household

debt-to-GDP had risen to 53% by end-2018 from 30% at end-2012. The risks

may be partly mitigated by macro-prudential and other measures, but the

Chinese authorities frequently intervene to manage the housing sector.

However, rising household debt adds to the challenges for domestic

consumption and the financial sector.

The latest discussion with Chris Bates, mortgage broker and financial planner, as we dissect the latest trends. Property prices higher, maybe in some places, but there are other more critical trends in play, and prospective buyers need to be careful!

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

Digital Finance Analytics (DFA) Blog

More From The Property Front Line - Chris Bates [Podcast]

The latest discussion with Chris Bates, mortgage broker and financial planner, as we dissect the latest trends. Property prices higher, maybe in some places, but there are other more critical trends in play, and prospective buyers need to be careful!

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

Blog")