The latest minutes from the RBA continues the steady-as-we-go story, once again and so the cash rate remains on hold.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased due to both higher oil prices and some lift in wages growth. A further pick-up in inflation is expected given the tight labour markets and, in the United States, the sizeable fiscal stimulus. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions in the advanced economies remain expansionary but have tightened somewhat recently. Equity prices have declined and yields on government bonds in some economies have increased, although they remain low. There has also been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates have declined recently, after increasing earlier in the year. Standard variable mortgage rates are a little higher than a few months ago and the rates charged to new borrowers for housing are generally lower than for outstanding loans.

The Australian economy is performing well. Over the past year, GDP increased by 3.4 per cent and the unemployment rate declined to 5 per cent, the lowest in six years. The forecasts for economic growth in 2018 and 2019 have been revised up a little. The central scenario is for GDP growth to average around 3½ per cent over these two years, before slowing in 2020 due to slower growth in exports of resources. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Growth in household income remains low, debt levels are high and some asset prices have declined. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years and have been stronger than earlier expected. This has helped boost national income. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, although it is currently in the lower part of that range.

The outlook for the labour market remains positive. With the economy growing above trend, a further reduction in the unemployment rate is expected to around 4¾ per cent in 2020. The vacancy rate is high and there are reports of skills shortages in some areas. Wages growth remains low, although it has picked up a little. The improvement in the economy should see some further lift in wages growth over time, although this is still expected to be a gradual process.

Inflation remains low and stable. Over the past year, CPI inflation was 1.9 per cent and, in underlying terms, inflation was 1¾ per cent. These outcomes were in line with the Bank’s expectations and were influenced by declines in some administered prices due to changes in government policies. Inflation is expected to pick up over the next couple of years, with the pick-up likely to be gradual. The central scenario is for inflation to be 2¼ per cent in 2019 and a bit higher in the following year.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Growth in credit extended to owner-occupiers has eased but remains robust, while demand by investors has slowed noticeably as the dynamics of the housing market have changed. Credit conditions are tighter than they have been for some time, although mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

ANZ saw its cash profit fall by 5 per cent over in FY18 to $6.5 billion. The bank’s ROI fell 67 basis points to 11 per cent over the year, via InvestorDaily.

Under the leadership of CEO Shayne Elliott, ANZ is focused on become a simpler bank. Part of this strategy has involved selling off non-core assets in Asian markets and the announced sale of its wealth business to IOOF.

Collectively, the announced asset sales are expected to release $7.2 billion of CET1 capital. Meanwhile, “institutional reshaping” is poised to free up $4.5 billion, according to the group’s full-year result presentation.

One significant outcome of ANZ’s strategy will be the reshaping of its workforce, or full-time equivalent staff (FTE). Staff numbers have already fallen dramatically from just over 50,000 in 2015 to under 38,000 today.

ANZ has reduced its FTE numbers by 5151 over the last 12 months, from 43,011 in September 2017 to 37,860 today.

Chief executive Shayne Elliott said that while the bank does not have a target to reduce its FTE numbers, staff cuts will be a natural result of simplifying the bank.

“The outcome of our strategy of doing less things means less branches, fewer products to service and less need for contact centre and operational staff,” he said.

“It is an outcome rather than a target.

“There will be more. We have been really transparent with our staff about why we are changing and the need to change. While it is early days, we do keep in touch with former staff and most of them haven’t struggled to find alternative employment,” he said.

When he appeared before the House of Representatives inquiry in Canberra on 12 October, Mr Elliott said more than 200 staff from across the group had been dismissed over misconduct over the last year.

ANZ this week revealed that it has reduced variable remuneration paid to staff across the company by $124 million.

Royal commission costs

The major bank paid $55 million in legal costs for the royal commission in FY18, one of a number of expenses that the Hayne inquiry has generated.

Earlier last month, ANZ announced a $374 million hit to profits as part of its refunds to customers and related remediation costs.

“Clearly there will be a short-term impact on financials. You are seeing that now,” Mr Elliot said.

“It may continue a little bit more. We are hiring people in compliance and investing in systems to make sure we are compliant. But in the long-run I don’t believe it will lead to an increase in costs, I actually believe the opposite.

“I believe that the way to meet our obligations regarding the law or community expectations is by being simpler. So by doing less things and doing them well, taking out all the complexity, that will be lower cost, better for compliance and better for customers.”

However, RBA assistant governor Michelle Bullock believes the royal commission will have longer term impacts on costs for the big banks.

Ms Bullock observed that while the royal commission has brought to light some poor behaviour by the Australian banks, the direct financial impact on them has been relatively modest so far.

“The fines to date are relatively small compared with the major banks’ combined profits of around $30 billion per annum. But there are also costs from remediation of past behaviour, which have been reflected in banks’ profit announcements in recent times, and there is also the possibility of class actions,” she said.

“And there are also likely to be increased costs of compliance, which will be ongoing. More broadly, there has been very little share price growth over recent years, which has had an impact on shareholder returns. And changes to business models to address the risk of future misconduct could more permanently impact banks’ financial performance. These changes, however, are likely to increase the resilience of the financial sector in the medium term, even if at the expense of lower returns.”

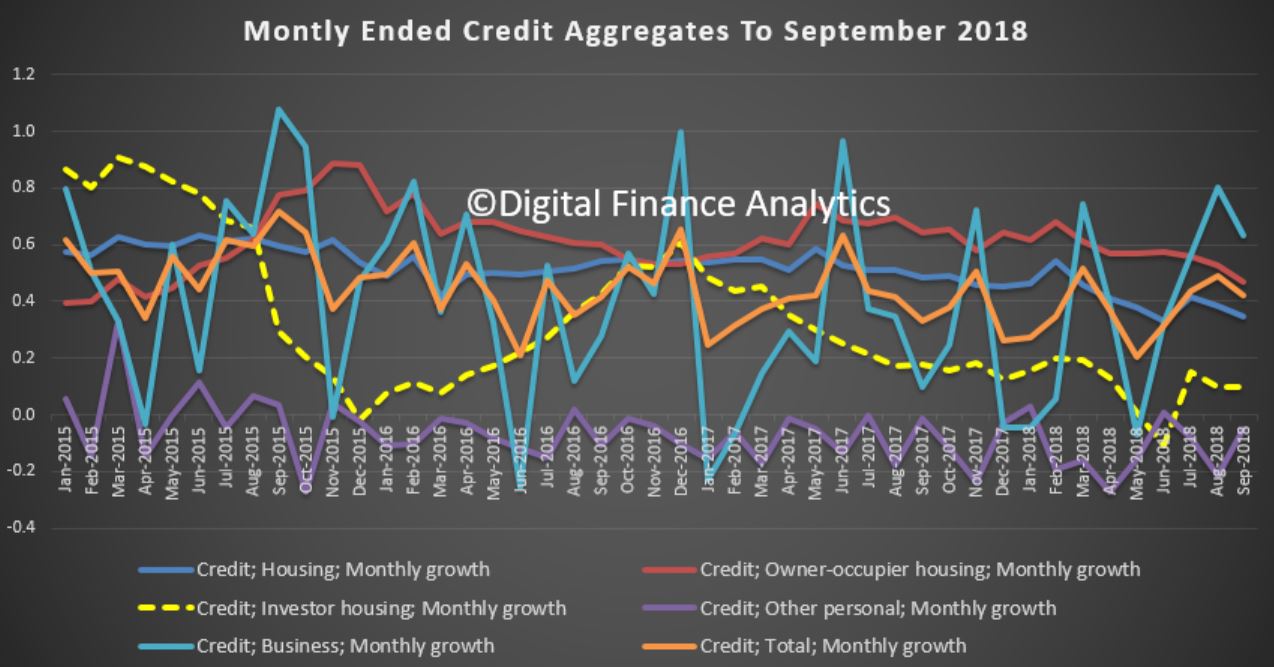

The latest Credit Aggregates from the RBA to September 2018 continues to show an easing of credit growth. Total credit, across all categories rose seasonally adjusted by $14.41 billion or 0.5%, to $2.8 trillion.

Within that owner occupied lending rose 0.5% or $5.5 billion to $1.19 trillion while investment lending rose 0.1% or $0.52 billion to $593 billion. Other personal lending was flat, and business lending rose 0.9% to $943 billion, up $8.4 billion.

Investor loans fell again to 33.1% of all housing lending, while business lending rose a little to 32.7% of all lending.

The monthly movements are still noisy…

… but the 12 month ended data shows how investor lending continues to slow, owner occupied lending growth is slowing, and overall lending for housing growth is slowing to 5.2%.

This is a problem for the banks in that to maintain profitability as assets grow, they need the rate of growth of housing loans to RISE not slow down. Even at these levels (with some growth) household debt will rise relative to loans, so again it highlights the fundamental problem we have in the system at the moment.

Lending in the less regulated Non bank sector still appears to be growing more strongly than ADI lending.

The Reserve Bank of Australia has echoed Westpac’s warning that the impact of the royal commission could see further reductions in the availability of credit, sparking broader fears for the economy.

But of course they were the architect of the credit boom, with too low interest rates and inappropriate monetary settings. Rich then they now flick the blame to the Commission, which is simply underscoring the need to get back to a more normal regime….

In the minutes of its October meeting on monetary policy, the Reserve Bank notes that members discussed the release of the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

“The report contains many questions covering a broad range of issues, but at this stage provides relatively little indication of the recommendations that are likely to be made in the final report,” the minutes said

“Members observed that while the regulators had already overseen a tightening of lending standards, and a degree of tightening of lending standards had been implemented by banks in anticipation of the commission’s findings, it was possible that banks could tighten lending conditions further given the issues raised in the report.

“Members noted that it would be important to monitor the future supply of credit to ensure that economic activity continued to be appropriately supported.”

The RBA’s comments come after Westpac chief executive Brian Hartzer used his opening statement at a parliamentary inquiry this month to warn against further regulation of lenders in response to the Hayne royal commission.

Appearing before the House of Representatives standing committee on economics, Westpac CEO Brian Hartzer urged legislators to consider the “second-order effects” of further regulation that may be introduced to reduce misconduct off the back of the commission.

“New regulations and tougher sanctions alone are not going to solve the risk of poor conduct,” Mr Hartzer said.

Mr Hartzer expressed support for an observation noted by commissioner Kenneth Hayne in his interim report, which suggested that simplifying regulation could reduce poor consumer outcomes.

The major bank CEO warned that further regulation could exacerbate the slowdown in credit and housing market conditions and impede economic growth.

“[In] striving to address the issues that have led to misconduct, it’s important that policymakers remain live to the potential second-order effects of new legislation and regulation,” the CEO continued.

“While overall economic growth remains sound, we are seeing increasing uncertainty, especially among the consumer and small business sectors.

“House prices are falling, income growth has been low, and consumer spending is likely to be affected by people’s confidence in the value of their home.

“Therefore, regulatory changes that impact how much individuals can borrow, the cost and availability of credit for business, or the availability and affordability of suitable financial advice, should be considered carefully.”

Tony Richards, RBA Head of Payments Policy Department spoke at the Chicago Payments Symposium, Federal Reserve Bank of Chicago and described the progress on the new payments platform – NPP. 2 million PayID registrations have been achieved so far, and the volume of payments has already outpaced cheques in the system.

Initial NPP operations

After industry testing through much of 2017, the NPP became operational for industry ‘live proving’ in November 2017. It was launched for public use on 13 February this year. This involved around 50 institutions initially, with this number now having increased to around 65 institutions.

As with any completely new payment system, financial institutions have mostly taken a staged approach in their rollout strategies, gradually introducing services, channels and customer segments. In some cases this was to manage risk and allow them to fine-tune their systems and processes, while in other cases it has reflected different stages of readiness. The major banks have mainly focused initially on providing payment capabilities to consumers ahead of businesses, with the rollout to consumers now at a fairly advanced stage.

At this point, there are more than 50 million Australian bank accounts accessible via the NPP, with that number growing steadily. The number of PayID registrations has just reached 2 million – Australia has a population of 25 million. And monthly volumes and values of NPP transactions have been growing strongly.

One interesting statistic is that the number of payments occurring through the NPP has already surpassed the number of cheques that are being written by Australian households, businesses and government entities

An international comparison also offers another interesting metric. While each country is its own special case, it appears that the adoption of the NPP is proceeding at least as quickly as occurred for some other fast-payment systems

As long as the rollout of NPP to households has not been completed, advertising of Osko by BPAY has been limited, but I would expect that this will be picking up, and that financial institutions will also be doing more promotion of real-time payments to their customers. So I would expect the value and volume of NPP transactions to continue to grow strongly.

Some early lessons learned

While the NPP was launched less than eight months ago, I think one can make a number of observations that may be of interest to this audience regarding its design and build, as well as its operation to date.

The presence of a well-resourced project office (from KPMG as well as from APCA and then NPPA) that was independent of the participants was important in the design, build and test phases. This ensured high quality papers for meetings, brought skills that might not have been readily available from participants, and provided independent perspectives during debates about the design and build

Having three aggregators (or service providers) involved as participants was important in ensuring the broad reach (and public legitimacy) of the NPP. The majority of the institutions that were ready to go on Day 1 were small banks, credit unions and building societies using the services of aggregators.

While the build of the Basic Infrastructure and FSS in the centre were major projects, the internal builds for NPP participants were the most challenging tasks. The systems of large banks are inevitably extremely complex, and upgrading them to allow real-time posting and 24/7 operation has taken longer than expected for some. Banks have also placed significant focus on ensuring that their fraud detection systems can support real-time payments.

Ubiquity (or near-ubiquity) is important. It is hard for a new payment system or for individual participants to go out and market aggressively to customers until a critical mass of institutions and accounts are on board. However, balancing this point and the previous one is a challenge. Decisions to launch to the public can only occur once a critical mass of participants is ready, but a program cannot be expected to move at the pace of the slowest participant.

Real-time settlement is going well. The challenges raised by out-of-hours and weekend operations can be met by appropriate central bank liquidity arrangements. Banks can easily move the balances in their Exchange Settlement accounts between the FSS and the RBA’s main RTGS system during normal business hours. These balances are then all moved into the FSS overnight and on weekends. In addition the Reserve Bank introduced a new liquidity facility for open-dated repos, which are available to holders of Exchange Settlement accounts at no penalty relative to the Bank’s policy rate.

Five or six years ago, some banks may have questioned the case for moving to real-time payments, however no one is questioning that case now. Indeed, the early signs are that banks are looking to move their Direct Entry payments over to the fast rails sooner than was earlier expected. Similarly, the decision to move to the ISO 20022 message format and richer data will be an important one for future innovation.

It was important to have the Addressing Service ready to launch on Day 1. PayIDs get around the problems of end-users having to enter lots of numbers, give certainty about the recipient, help avoid ‘fat finger’ problems and mistaken payments, and can reduce fraud.

The involvement of the central bank – from the policy side, as well as in the delivery of settlement arrangements and as a banking service provider – has been important. I suspect that some industry participants may initially have had some concerns about having the Reserve Bank involved, but that they would recognise now that our involvement helped to get some key aspects of the design, build, and business rules right.

The fact that the Basic Infrastructure will be operated as an industry utility available to all, with commercial payment services to be provided by separate overlay services, was also helpful in getting agreement among participants in the design phase.

With the initial build mostly complete, the industry has ambitious plans for additional NPP functionality. While some of this could potentially be delivered via overlay services, it is likely that there will be additional central functionality provided or arranged by NPPA – for example, possibly a central consent and mandate service that could be used to enable direct debits though the NPP. As NPPA increases its capabilities, it may also look to new means of providing functionality. On Friday it announced an API framework with three sample APIs.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased due to both higher oil prices and some lift in wages growth. A further pick-up in inflation is expected given the tight labour markets, and in the United States, the sizeable fiscal stimulus. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions in the advanced economies remain expansionary, although they are gradually becoming less so in some countries. Yields on government bonds have moved a little higher, but credit spreads generally remain low. There has been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates are higher than they were at the start of the year, although they have declined since the end of June. In response, some lenders have increased their standard variable mortgage rates by small amounts, while at the same time reducing mortgage rates for some new loans.

The latest national accounts confirmed that the Australian economy grew strongly over the past year, with GDP increasing by 3.4 per cent. The Bank’s central forecast remains for growth to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Growth in household income remains low and debt levels are high. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years due to rises in some commodity prices. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, but it has depreciated against the US dollar along with most other currencies.

The outlook for the labour market remains positive. The unemployment rate is trending lower and, at 5.3 per cent, is the lowest in almost six years. The vacancy rate is high and there are reports of skills shortages in some areas. A further gradual decline in the unemployment rate is expected over the next couple of years to around 5 per cent. Wages growth remains low, although it has picked up a little. The improvement in the economy should see some further lift in wages growth over time, although this is likely to be a gradual process.

Inflation is around 2 per cent. The central forecast is for inflation to be higher in 2019 and 2020 than it is currently. In the interim, once-off declines in some administered prices in the September quarter are expected to result in inflation in 2018 being a little lower than otherwise.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Growth in credit extended to owner-occupiers remains robust, but demand by investors has slowed noticeably as the dynamics of the housing market have changed. Credit conditions are tighter than they have been for some time, although mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

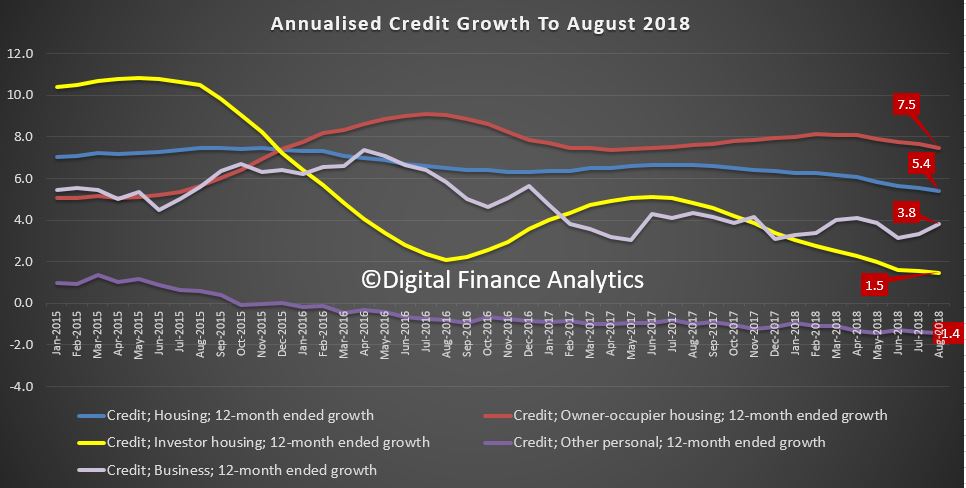

The 12 month growth by category shows that owner occupied lending is still growing at 7.5% annualised, while investment home loans have fallen to 1.5% on an annual basis. Overall housing lending is growing at 5.4% (compared with APRA growth of 4.5% over the same period, so the non-banks are clearly taking up some of the slack). Still above wages and inflation. Household debt continues to rise.

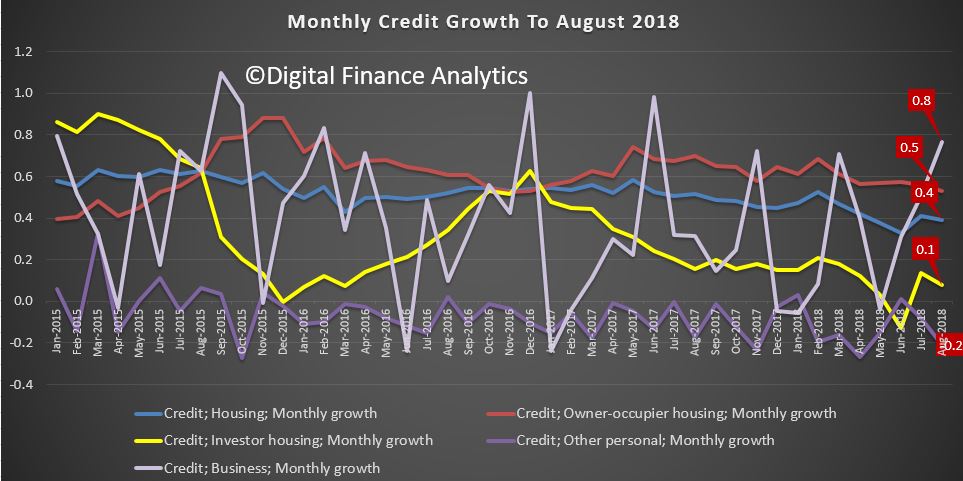

The more noisy monthly data shows investor loans slowing, while business lending is up. Personal credit continues to slide.

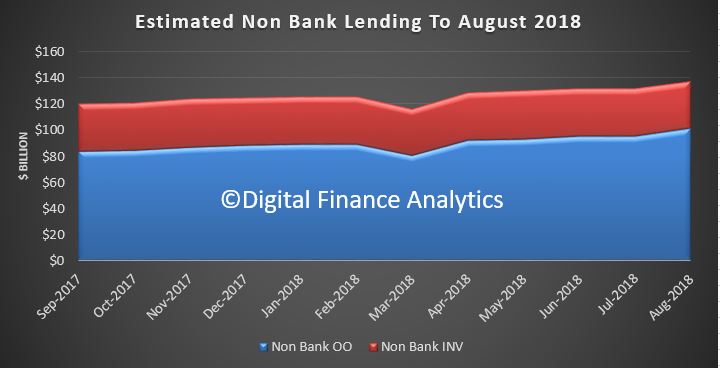

The non-bank sector (derived from subtracting the ADI credit from the RBA data) shows a significant rise up 5% last month in terms of owner occupied loans. This is indicative, as there are timing and other issues when making this comparison, but its the best available. This is consistent with our survey data which slows that non-banks are indeed seeking to grow their books under the lighter non-ADI regulation.

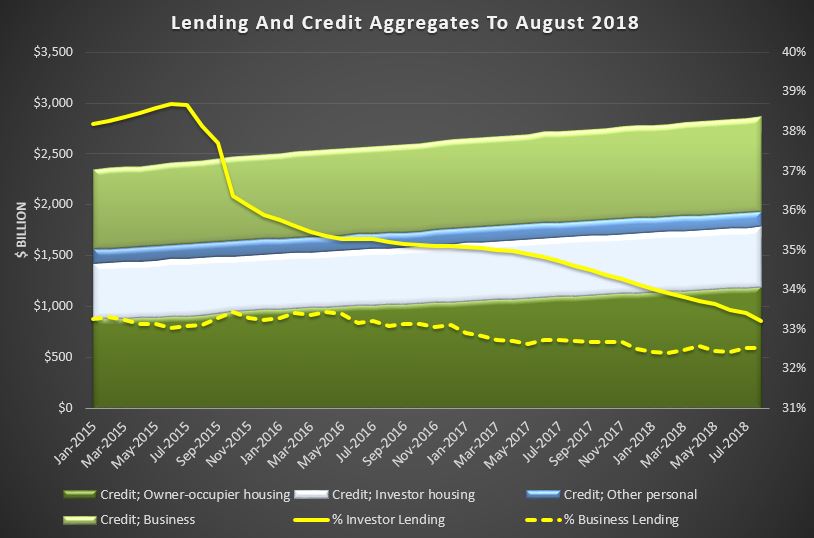

Finally, total lending lose to 1.78 trillion, with owner occupied loans at $1.2 trillion and investment loans at $593 billion. The mix of loans fell to 33.2% of housing loans for investment lending. Business lending was $934 billion, comprising 32.5% of all credit.

In summary, housing debt is still rising too fast . Period. APRA needs to look at the non-banks. And quickly.

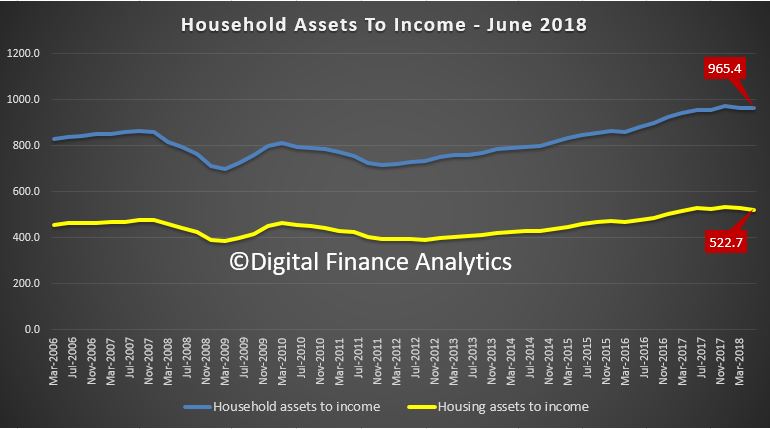

The RBA has updated their battery of statistics to June 2018 today. As always we go to the households ratios series –E2 HOUSEHOLD FINANCES – SELECTED RATIOS

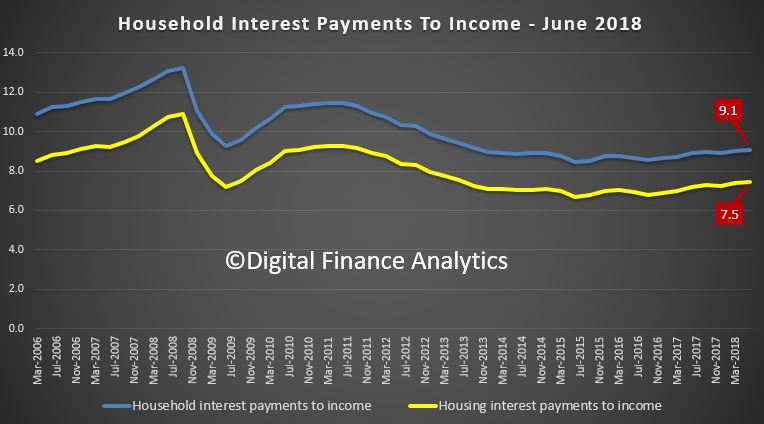

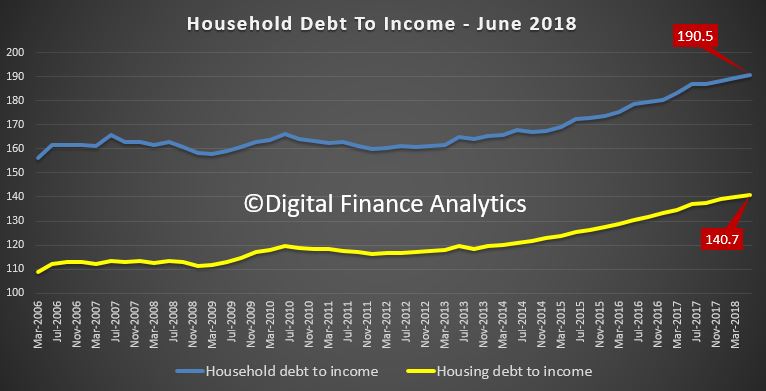

In short the debt to income is up again to 190.5, the ratio of interest payments to income is up, meaning that households are paying more of their income to service their debts, and the ratio of debt to home values are falling. All three are warnings. The policy settings are not right.

In more detail, we need to highlight that these ratios are for ALL households, whether they borrow or not, and also include small firms.

On average the value of household assets to income is up thanks to rising stock markets, but the value of housing assets to income is FALLING, as home prices slide. Expect more of this ahead.

Looking at interest payments, these are rising, whether you look at housing debt or all debt. This is a combination of more debt. bigger loans, and some higher interest rates. Expect more ahead. OK, interest payments were higher when interest rates were higher, but the lose lending standards have enabled people to get bigger loans so they are move leveraged. As rates rise higher, this pressure multiplies.

Finally, the household debt to income is higher again at 190.5 now, and the housing debt to income is higher too.

Again on these numbers there is no justification to loosen lending standards, in fact to avoid a traffic accident later they still need to be tightened further.

There was an interesting speech from RBA Assistant Governor (Financial Markets) Christopher Kent entitled “Money – Born of Credit“.

The first fascinating point was his confirmation that loans create deposits (rather than deposits creating loans, which was the traditional view of how banks worked). This is a critical pivot, because it means banks can create ever more loans, provided borrowers are prepared to borrow. This is something I have discussed many times, and recently with Steve Keen on the DFA YouTube Channel. It has profound implications for monetary policy.

Control of credit in this model becomes critical.

The second is that he then tries to explain why inter bank lending rates remain elevated for Australian banks. I think he is less successful here, because the obvious missing link in the risk premium which is now in place (given the litany of issues raised by the Royal Commission, regulatory pressure, and potential class actions).

Our banks are having to pay more for their funding because of their recent track record, and this is not going to flip back anytime soon, in my view.

Here is the speech which is worth reading.

Most of us would put cold hard cash at the top of our list when we think of money. Others would include funds they have on deposit at a bank. Some might contemplate broader measures of their wealth. Historians would be tempted to tell us about the role of precious metals, coins, salt, shells and even rum when the topic of money is raised. When thinking about the role that money plays in an economy, economics teachers and academics might educate us about money multipliers, the velocity of money and money demand and supply functions. Keen students of episodes of high inflation would discuss Milton Friedman and the notion that inflation is ‘always and everywhere’ a monetary phenomenon. Given this, concerned citizens might be worried about what they see as the ability of private banks to create money via the extension of credit, seemingly at will.

While there are many interesting aspects of money, today I want to focus on the questions of how money is created and how money relates to lending or credit. Along the way, I’ll also review what’s been happening to both money and credit in Australia over recent decades. The process of money creation is often subject to a degree of confusion, in part because the explanation draws upon a combination of disciplines – accounting, banking and economics.

What Is Money?

It is relatively standard practice to define money according to its ability to do each of the following three things:

money can be used for transactions – it facilitates the exchange of goods, services or assets thereby avoiding the substantial costs associated with barter

money is a store of value – it’s worth does not fluctuate wildly, nor does it degrade rapidly over time, and

money acts as a commonly accepted unit of account – it provides a convenient means of comparing the value of a range of different goods, services or assets.

Banknotes and coins – otherwise known as currency – satisfy each of these functions. Currency long ago pushed aside other physical forms of money.

Currently, there is around $75 billion of currency in circulation in Australia (outside of the banking system). However, despite its usefulness, currency represents only a small share of money in modern economies.

Most money consists of deposits in banks, building societies and credit unions (simply referred to here as banks). Just as I can pay for my morning coffee using currency, I can also transfer funds in my bank deposit to the café’s account. In either case, the café owner receives a liquid store of value which they are confident will be accepted by others.

Not all bank deposits are equally liquid – for instance, it can take some time to gain access to funds in a term deposit. For this reason, it is common to construct a range of different ‘monetary aggregates’, from the more liquid narrower forms money – such as M1, which includes currency and current deposits at banks – to ‘broad money’, which also captures less liquid deposits and other financial products that share the characteristics of money discussed earlier (Table 1; Graph 1); for example, broad money includes certificates of deposit or short-term debt securities. For convenience, in what follows I’m going to focus on broad money.

Table 1: Monetary Aggregates

Measure

Description(a)

Currency

Notes and coins held by the private non-bank sector

Money base

Currency + banks’ holdings of notes and coins + deposits of banks with the Reserve Bank + other Reserve Bank liabilities to the private non-bank sector

M1

Currency + current (cheque) deposits of the private non-bank sector at banks

M3

M1 + all other deposits of the private sector at banks (including certificates of deposit) except deposits of authorised deposit-taking institutions (ADIs) + all deposits of the private non-ADI sector at credit unions and building societies (CUBS)

Broad money

M3 + other deposit-like borrowings of all financial intermediaries (AFIs) from the non-AFI private sector (such as short-term debt securities)

(a) These descriptions abstract from some detail. See the Financial Aggregates release for more information.

Graph 1

Broad money represents a relatively liquid form of wealth held by Australian households and businesses. It includes currency, deposits and deposit-like products.[1] Unlike ancient forms of physical money – think shells or gold found in the natural environment – these are liabilities issued by authorised deposit-taking institutions (ADIs) and other financial intermediaries.[2] Broad money in Australia is currently around $2 trillion or 115 per cent of the value of annual economic output as measured by nominal GDP; most of that is in the form of banking deposits. Over the past decade, the share of broad money represented by term and other bank deposits has increased in importance at the expense of holdings of current deposits and other borrowings from the private sector.

How Is Money ‘Created’?

Australia’s banknotes are produced by the Reserve Bank of Australia and account for most (about 95 per cent) of the value of Australian currency. The rest is accounted for by coins produced by the Royal Australian Mint.

Banks purchase banknotes from the Reserve Bank as required to meet demand from their customers and, in turn, the Reserve Bank ensures that it has sufficient banknotes on hand to meet that demand. Previous research by the Reserve Bank points to a number of drivers of demand for banknotes. The most important is the size of the economy.[3] This is consistent with people holding some fraction of their income in this most liquid form of money in order to undertake transactions.[4] Some share of demand is also accounted for by the desire for a liquid store of wealth. The value of banknotes in circulation as a share of nominal GDP has actually increased over recent years (to around 4 per cent), which suggests that this source of demand has grown strongly. This increase has been observed in a range of countries and is consistent with the low level of interest rates, which has reduced the opportunity cost of holding money (compared with holding interest-bearing deposits).

When customers withdraw currency from an ATM or a bank branch, the value of their deposit holdings declines and the value of their currency holdings increases. The stock of broad money, however, is unchanged.

As I mentioned earlier, the vast bulk of broad money consists of bank deposits. These banking liabilities are created when an Australian household or business has funds credited to their deposit account at an Australian bank. One way this can occur, for example, is when a business deposits currency it has earned with its bank. Again, such transactions add to deposits but do not create money because the bank customer is simply exchanging one type of money (currency) for another (a deposit).

Money can be created, however, when financial intermediaries make loans. Accordingly, the concepts of money and credit are closely linked in a modern economy, albeit not one for one. When a bank extends a loan, it makes money available to the borrower, for example, to buy a car, a house or equipment for a business. The bank may credit the deposit account of the borrower, who withdraws the funds to make their purchase. Alternatively, the bank may directly credit the deposit account of the seller on behalf of the borrower. In either case, the loaned funds will tend to find their way into a deposit somewhere in the banking system. This process adds to the supply of money.

If I stopped here, you might be left with the impression that the process of lending allows the banking system to create endless quantities of money at no cost. However, the process of money creation is constrained in numerous ways and depends on the behaviour of borrowers, banks and regulators, as well as the stance of monetary policy.

In the first instance, the process of money creation requires a willing borrower. That demand will depend, among other things, on prevailing interest rates as well as broader economic conditions. Other things equal, lower interest rates or stronger overall economic conditions will tend to support the demand for credit, and vice versa.

The bank then has to be willing and able to issue the loan:

It has to satisfy itself that the borrower can service the loan.

The bank must maintain a sufficient share of its assets in liquid form to meet any drawdowns relating to the new loan, as well as meeting any withdrawals from existing depositors.[5] Otherwise, the bank runs the risk of failing to meet its obligations when they fall due.

The bank’s loans and other assets need to be backed by adequate capital. Capital is needed to absorb unexpected losses arising from defaults or other sources of variation in the value of assets.

The interest rates charged on loans must cover expected losses on the loan portfolio, as well as the costs of deposits and other sources of funding. Revenues from loans and other assets will also have to cover the operating costs of the bank, while allowing it to earn a profit so that shareholders can earn a reasonable return on the bank’s capital.

All of these considerations imply that money creation occurs at some cost, which serves to constrain the extent of lending. These constraints are reinforced by regulatory requirements for liquidity, capital adequacy and lending standards set by the Australian Prudential Regulation Authority. Other things equal, anything that reduces the willingness or ability of banks to make loans can be expected to result in lower growth of (system-wide) money.

It’s also worth emphasising that the process of money creation is not the result of the actions of any single bank – rather, the banking system as a whole acts to create money. A single bank may make loans by drawing on its liquid assets, yet not receive the corresponding deposits created in return. Before extending further loans, that bank would need to raise funds in other ways – for example, by issuing debt or equity securities or by waiting for its deposits and liquid assets to rise via other means.[6]

Graph 2 illustrates how the process of money creation can work. It shows an example of an increase in loans of $100 billion. However, the increase in loans in this case leads to an increase in deposits of $60 billion; in other words, the changes are not one for one. This is because there are other sources of funding besides deposits – and indeed, loans are not the only assets held by banks. In the example shown, other funding comes from issuance of debt and equity. The shares from different sources are in line with the actual funding behaviour of the banking system over recent years (Graph 3).

Graph 2

Graph 3

In summary, changes in the stock of broad money are the result of a myriad of decisions, including those of banks, their borrowers, creditors and shareholders. And these decisions take place within the framework of a range of regulatory and institutional arrangements. It is worth noting that the Reserve Bank does not target a particular level or growth rate of money (although it has done so under a previous monetary policy regime).[7] Instead, the Reserve Bank has some influence on the money stock via the effect of its interest rate target for the overnight cash rate on other interest rates in the economy. These in turn affect the cost of borrowing and economic conditions more generally. Ultimately, borrowing and lending decisions – and thus the creation of money – are constrained by the need for prudent banking behaviour, the budget constraints of borrowers and the profitability of lenders.

One final word on the creation of money is that as fun as it is to teach students about traditional money multipliers, I don’t find them to be a very helpful way of thinking about the process. In Australia, simple regulatory regimes – which had earlier required banks to hold a minimum share of their deposits as reserves with the Reserve Bank – have been replaced with modern prudential regulation and market discipline. Again, the demand for and supply of credit is the real driver of money. That point can be reinforced by examining the behaviour of credit and money over time.

What Has Money Been Doing and Why?

Given that money is used for transactional purposes and as a store of value, it makes sense that most of the time it would at least keep pace with growth in the value of nominal spending. Indeed, in Australia it has grown faster than that over the past 40 years, roughly doubling as a share of nominal GDP (Graph 4).

Growth of credit has been stronger still, roughly tripling as a share of nominal GDP, from under 50 per cent in the early 1980s to over 150 per cent currently. A closer look at the banks’ balance sheets shows how these changes have occurred.

Graph 4

In 1980, Australian banks held more than 80 per cent of their liabilities as deposits (worth around $47 billion at the time) (Graph 5). This deposit base was more than sufficient to fund loans of about 60 per cent of assets (worth $34 billion). The majority of the remaining assets were held in the form of securities (mostly government bonds).[8]

Graph 5

As banks grew through the next four decades or so, there was a marked change in the composition of their balance sheets. These changes reflected choices by both banks and the private sector and were strongly influenced by the deregulation of the financial system. In particular, constraints on banks’ business activities were progressively removed in the 1970s and early 1980s (for example, the interest rates they could charge and pay, their product offerings, lending volumes and their asset holdings). This was associated with significant changes in banks’ abilities to attract and use different funding sources to support balance sheet growth.[9] By the early 1990s, Australians’ demand for credit from banks became larger than the sum of all of their deposits.

Following a period of slower growth around the early 1990s recession, credit growth picked up again and continued to grow much more quickly than money. To enable this, a greater proportion of bank funding during this period was drawn from sources other than deposits. Much of it owed to an increase in the issuance of debt securities, which was supported, in part, by a strong appetite from non-residents for Australian bank debt.

These trends continued until the global financial crisis. Following the crisis, credit growth fell for a while (reflecting a decline in both the supply of and demand for credit). At the same time, the stock of (broad) money increased noticeably, rising by around $1.1 trillion dollars, from around 80 per cent of GDP in 2007 to around 115 per cent in 2018. This strong growth reflected a sharp increase in the share of funding sourced from deposits at the expense of short-term debt securities, consistent with banks seeking more stable funding. Meanwhile, households and businesses increased the share of their assets held in the form of deposits.

While loans have grown dramatically in nominal terms, to around $2.6 trillion today, the share of loans on banks’ balance sheets is the same as it was in 1980 (Graph 6).[10] In contrast, and notwithstanding the increase in deposits since the global financial crisis, the share of deposits has declined over the past 40 years from above 80 per cent to around 50 per cent of banks’ balance sheets.[11] Currently, a sizeable share of banks’ liabilities is in the form of bonds on issue – a source of funding that was less important in 1980.[12] Banks also have a much larger share of ‘other liabilities’ (such as those to non-residents and related parties, which are not included in domestic monetary aggregates).

Graph 6

Looking back, it is clear that there have been many instances of sustained gaps between the growth of deposits – and broad money more generally – and the growth of credit (Graph 7). While broad money growth outpaced credit growth for most of the period since the financial crisis, this was not the experience of the two decades or more prior to the crisis, when credit typically outpaced broad money.

Graph 7

This long history suggests that we should not be concerned about a so called deposit ‘funding gap’. Some commentators have suggested that the recent decline in the growth rate of money has left banks with insufficient deposit funding to support credit growth. According to this hypothesis, banks have been forced to seek other forms of funding, including from short-term money markets, which, so the argument goes, can help to explain the notable rise in rates in those markets in recent months.[13]

What are we to make of this hypothesis? First, such a gap between the growth of deposits and credit has been commonplace over recent decades – and conditions in short-term money markets were benign through much of those earlier episodes. Second, loans are not the only assets on banks’ balance sheets; indeed, in recent quarters, growth in these other assets has been particularly slow – slower than both credit and deposits (Graph 8). So deposit growth has more than matched the growth in total assets.

Graph 8

Third, if some banks really did have insufficient deposit funding, we would expect to see them competing more vigorously for deposits by raising interest rates on those products. But retail deposit rates have been flat to down over the past year (Graph 9).

Graph 9

In short, there is little evidence that there is any relationship between the slowing of deposit growth and recent funding pressures in short-term money markets. More generally, given my earlier discussion about the extension of credit leading to the creation of banking system deposits, worrying about slower deposit growth impinging on the banking system’s ability to generate credit is putting the cart before the horse.

What Can Money or Credit Tell Us about Broader Economic Developments?

Given this discussion, it is worth asking whether the behaviour of money can tell us anything useful about broader economic developments and, if so, is it more or less useful than the behaviour of credit?

I’m going to address these questions in a very narrow way by examining whether the growth of broad money or credit provides any useful statistical information about the growth of nominal GDP. Because data for money and credit are available about five weeks ahead of the quarterly GDP release, we can examine whether growth in the current quarter of these series provides any additional information about the likely outcome for nominal GDP this quarter. This exercise is intended to merely determine whether money or credit are useful indicators of GDP. It is not intended to demonstrate whether a causal link exists between money or credit and GDP. (Indeed it is possible that the direction of causation runs in either or both, directions.)

I start with a simple model of quarterly nominal GDP growth as a function of recent lags of nominal GDP growth (Model 1 in Table 2). The model is estimated over the inflation-targeting period. This simple model is not particularly useful; lags of nominal GDP growth explain only about 8 per cent of the variation in the current growth of nominal GDP. But it gives us a useful baseline for comparison.

Table 2: Simple Models of Nominal GDP Growth(a)March quarter 1993 – June quarter 2018

Model 1

Model 2

Model 3

Model 4

Constant

1.14**

0.85**

0.88**

0.70**

GDP growth(b)

0.21

0.04

−0.06

−0.08

Broad money growth(c)

0.26*

0.16

Credit growth(c)

0.31**

0.25**

R-squared

0.08

0.15

0.17

0.22

Adjusted R-squared

0.04

0.07

0.09

0.10

(a) Quarterly data; ** indicates statistical significance at the 5 per cent level; * indicates statistical significance at the 10 per cent level

(b) Coefficient presented is the sum of the coefficients on the past four lags of quarterly nominal GDP growth; statistical significance is based on a joint significance test for these coefficients

(c) Coefficients presented are the sum of the coefficients on the current and past four lags of quarterly broad money or credit growth; statistical significance is based on joint significance tests for these coefficients

Sources: ABS, RBA

Adding current and past lags of money growth to the baseline model doesn’t improve its performance much; the sum of the coefficients on the money terms are statistically significant, but only at a 10 per cent level (Model 2). Similarly, adding current and past lags of credit growth improves the model’s explanatory power only slightly; however, the sum of coefficients on the credit terms are statistically significant at the 5 per cent level (Model 3). Interestingly, if both money and credit terms are included at the same time, only credit growth is statistically significant (Model 4). This suggests that credit growth is a marginally more useful statistical indicator of the growth of economic activity than money growth; again, I should stress that the contribution of the credit variable to the model in terms of its additional explanatory power is very modest.[14]

Conclusion

Currency in circulation has increased as a share of nominal GDP – indeed it’s as high as it’s been in many decades. But the increase in money, which includes bank deposits, has been even greater over the same period. That increase has been driven by the extension of credit, which depends on the decisions of borrowers and lenders. Banks have been able to fund that additional credit via growth in other sources of funding, including debt securities and equity. The recognition that deposits are created by the banking system via the extension of credit suggests that we should not be concerned about the banking system facing a deposit funding gap. Moreover, it is consistent with simple empirical analysis that suggests that credit is a marginally more useful indicator of the near-term growth in the value of economic activity than money.