APRA today published a letter relating to the Committed Liquidity Facility which is available to just 15 of the banks in Australia (The LCR banks). These have the back-stop option of calling on funds from the RBA to buttress their liquidity in case of need – so they can meet their obligations under the Basel III regime.

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports.

More evidence of a lack of a level playing field in the system, and how the regulators are supporting the big end of town. No surprise then that big players are regarded by the markets as too big to fail.

But as Australian Government debt is hurtling beyond $500 billion, I have to say their so called justification – lack of liquidity in the local securities (mainly Australian Government Securities and securities issued by the borrowing authorities of the states and territories) is wearing a bit thin.

Why is this facility needed at all?

This is what APRA said today:

The Australian Prudential Regulation Authority (APRA) is today releasing aggregate results on the Committed Liquidity Facility (CLF) established between the Reserve Bank of Australia (RBA) and certain locally incorporated ADIs that are subject to the Liquidity Coverage Ratio (LCR).

APRA implemented the LCR on 1 January 2015. The LCR is a minimum requirement that aims to ensure that ADIs maintain sufficient unencumbered high-quality liquid assets (HQLA) to survive a severe liquidity stress scenario lasting for 30 calendar days. The LCR is part of the Basel III package of measures to strengthen the global banking system.

In December 2010, APRA and the RBA announced that ADIs subject to the LCR will be able to establish a CLF with the RBA. The CLF is intended to be sufficient in size to compensate for the lack of sufficient HQLA (mainly Australian Government Securities and securities issued by the borrowing authorities of the states and territories) in Australia for ADIs to meet their LCR requirements. ADIs are required to make every reasonable effort to manage their liquidity risk through their own balance sheet management before applying for a CLF for LCR purposes.

Committed Liquidity Facility for 2019

All locally incorporated LCR ADIs were invited to apply for a CLF amount to take effect on 1 January 2019. All fifteen ADIs chose to apply. Following APRA’s assessment of applications, the aggregate Australian dollar net cash outflow (NCO) of the fifteen ADIs was estimated at approximately $381 billion. The total CLF amount allocated for 2019 (including an allowance for buffers over the minimum 100 per cent requirement) is approximately $243 billion.

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change.

Eligible Securities

Securities that ADIs can use under the CLF will include all securities eligible for the Reserve Bank’s normal market operations. In addition, for the purposes of the CLF, the Reserve Bank will allow ADIs to present certain related-party assets issued by bankruptcy remote vehicles, such as self-securitised residential mortgage-backed securities (RMBS). This reflects a desire from a systemic risk perspective to avoid promoting excessive cross-holdings of bank-issued instruments. Should the ADI lack a sufficient quantity of residential mortgages, other ‘self-securitised’ assets may be considered, with eligibility assessed on a case-by-case basis.

The Reserve Bank has discretion to broaden the eligibility criteria and conditions for the various asset classes at any time. The Bank will provide one years notice of any decision to narrow the criteria for the facility.

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

Margining

The initial margins that the Reserve Bank will apply to eligible collateral will be the same as those used in the Bank’s normal market operations. Consistent with current practice, each day the Bank will re-value all securities held under repurchase agreements at prevailing market prices.

Termination

Subject to the ADI having positive net worth, the Reserve Bank will give at least 12 months notice of any intention to terminate the CLF. The Bank’s commitment to any individual ADI will lapse if the fee is not paid.

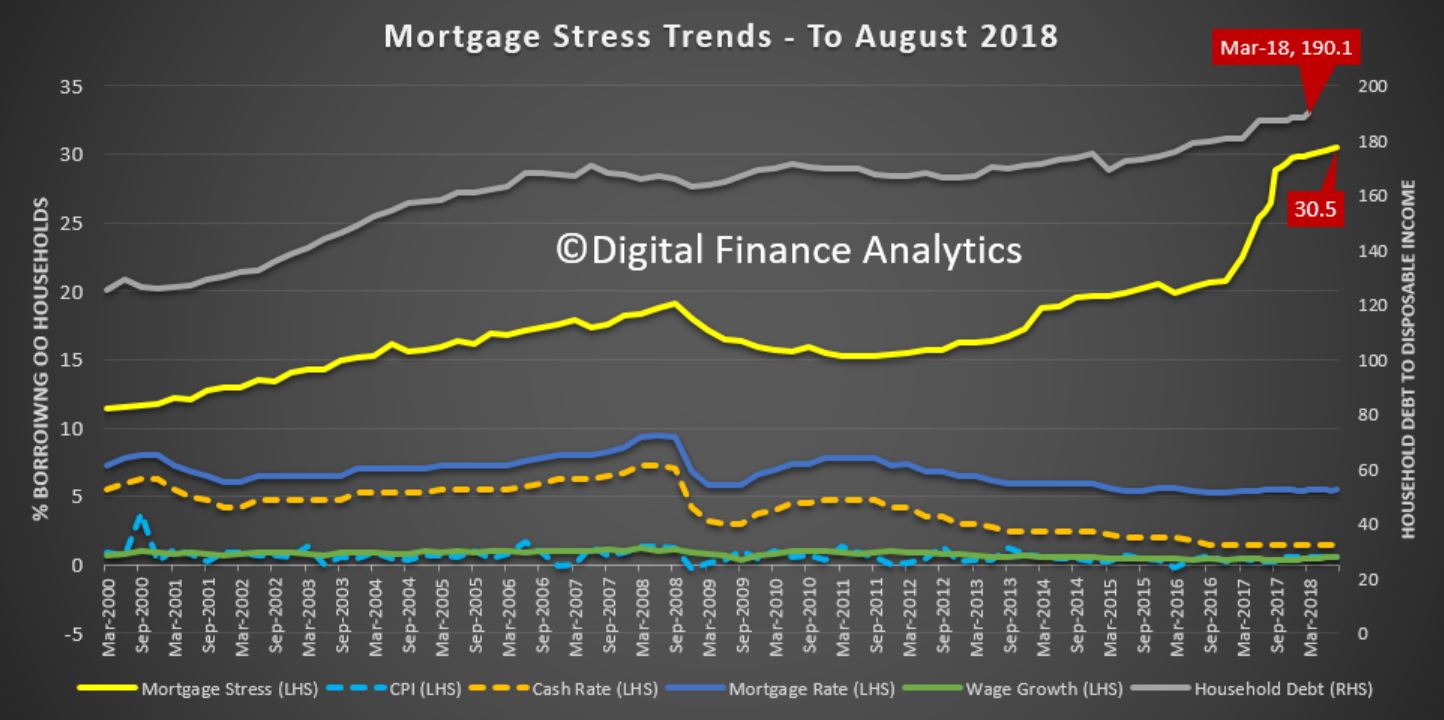

RBA Assistant Governor, Financial System, Michele Bullock discussed household debt in a recent speech. She concludes that “Household debt in Australia has risen substantially relative to income over the past few decades and is now at a high level relative to international peers. This raises potential vulnerabilities in both bank and household balance sheets. While the risks are high, there are a number of factors that suggest widespread financial stress among households is not imminent. It is nevertheless an area that we continue to monitor closely”. She included comments on households in regional areas, who are often overlooked in discussion.

She shows that housing debt is the main issue, that risks vary across households (and income bands), and that on an international comparison basis we are right up there. Household debt-to-income ratio has increased more than for many other countries.

Also she cites HILDA data up to wave 16. The fieldwork for this report was conducted between 2001 and 2016. So not very current in my view! Perhaps the current risks are higher thanks to continued poor lending practice, flat incomes and rising costs. Our mortgage stress data suggests this.

Household debt in Australia has been rising relative to income for the past 30 years (Graph 1). This graph shows the total household debt-to-income for Australia from the early 1990s until this year. Over that time it has risen from around 70 per cent to around 190 per cent. There are three distinct periods. The first, from the early 1990s until the mid-2000s, saw the debt-to-income ratio more than double to 160 per cent. Then there was a period from around 2007 to 2013 when the ratio remained fairly steady at 160 per cent. Finally, since 2013, the debt-to-income ratio has been rising again, reaching 190 per cent by 2018.

Graph 1

Australia has not been unique in seeing debt-to-income ratios rise. The median debt-to-income ratio for a range of developed economies has also risen over the past 30 years. But the Australian debt-to-income ratio has risen more sharply. In fact, Australia has moved from having a debt-to-income ratio lower than around two thirds of countries in the sample to being in a group of countries that have debt-to-income ratios in the top quarter of the sample. This suggests that there are both international and domestic factors at play when it comes to debt-to-income ratios.

There are two key international factors that have tended to increase the ability of households in developed countries, including Australia, to take on debt over the past few decades. The first is the structural decline in the level of nominal interest rates over this period, partly reflecting a decline in inflation but also a decline in bank interest rate margins as a result of financial innovation and competition. With lower interest payments, borrowers could service a larger loan. The second is deregulation of the financial sector. Through this period, the constraints on banks’ lending were eased significantly, allowing credit constrained customers to access finance and banks to expand their provision of credit.

But as noted, in Australia the household debt-to-income ratio has increased more than for many other countries. The increase in household debt over the past few decades has been largely due to a rise in mortgage debt. And an important reason for the high level of mortgage debt in Australia is that the rental stock is mostly owned by households. Australians borrow not only to finance their own homes but also to invest in housing as an asset. This is different to many other countries where a significant proportion of the rental stock is owned by corporations or cooperatives (Graph 2). This graph shows for a number of countries the share of dwellings owned by households on the bottom axis and the average household debt-to-income ratio on the vertical axis. There is a clear tendency for countries where more of the housing stock is owned by households to have a higher household debt-to income-ratio.

Graph 2

Potential vulnerabilities

This high level of household debt relative to income raises two potential vulnerabilities. First, because mortgage lending is such an important part of bank balance sheets in Australia, any difficulties in the residential mortgage market could translate to credit quality issues for banks (Graph 3). And since all of the banks have very similar balance sheet structures, a problem for one is likely a problem for all. This graph shows the share of banks’ domestic credit as a share of total credit over the past couple of decades. Australian banks have substantially increased their exposure to housing over this period and housing credit now accounts for over 60 per cent of banks’ loans. So the Australian banking system is potentially very exposed to a decline in credit quality of outstanding mortgages.

Graph 3

The risk that difficulties in the residential real estate market translate into stability issues for the financial institutions, however, appears to be currently low. The Australian banks are well capitalised following a substantial strengthening of their capital positions over the past decade. While lending standards were not bad to begin with, they have nevertheless tightened over the past few years on two fronts. The Australian Prudential Regulation Authority (APRA) has pushed banks to more strictly apply their own lending standards. And APRA has also encouraged banks to limit higher risk lending. Lending at high loan-to-valuation ratios has declined as a share of total loans, providing protection against a decline in housing prices for both banks and households. And for loans that continue to be originated at high loan-to-valuation ratios, the use of lenders’ mortgage insurance protects financial institutions from the risk that borrowers are unable to repay their loans. Overall, arrears rates on housing loans remain very low.

But the second potential vulnerability – from high household indebtedness – is that if there were an adverse shock to the economy, households could find themselves struggling to meet the repayments on these high levels of debt. If they have little savings, they might need to reduce consumption in order to meet loan repayments or, more extreme, sell their houses or default on their loans. This could have adverse effects on the real economy – for example, in the form of lower economic growth, higher unemployment and falling house prices – which could, in turn, amplify the negative shock.

So what do the data tell us about the ability of households to service their debt? This graph shows the ratio of household mortgage debt to income (a subset of the previous graph on household total debt) on the left hand panel and various serviceability metrics on the right hand panel (Graph 4). The mortgage debt-to-income ratio shows the same pattern as total household debt-to-income – rising up until the mid-2000s then steadying for a few years before increasing again from around 2013. The dashed line represents the total mortgage debt less balances in ‘offset’ accounts. This shows that taking into account these ‘buffers’, the debt-to-income ratio has still risen, although not by as much. So households in aggregate have some ability to absorb some increase in required repayments.

Graph 4

In terms of serviceability, interest payments as a share of income rose sharply from the late 1990s until the mid-2000s reflecting both the rise in debt outstanding as well as increases in interest rates. Interest payments as a share of disposable income doubled over this period. Since the mid-2000s, however, interest payments as a share of income have declined as the effect of declines in interest rates have more than offset the effect of higher levels of debt. Indeed even total scheduled payments, which includes principal repayments, are lower than they were in the mid-2000s, as the rise in scheduled principal as a result of larger loans was more than offset by the decline in interest payments.

The risks nevertheless remain high and it is possible that the aggregate picture is obscuring rising vulnerabilities for certain types of households. Interest payments have been rising as a share of income in recent months, reflecting increases in interest rates for some borrowers, particularly those with investor and interest-only loans. Scheduled principal repayments have also continued to rise with the shift towards principal-and-interest, rather than interest-only, loans. There are therefore no doubt some households that are feeling the pressure of high debt levels. But there are a number of reasons why the situation is not as severe as these numbers suggest.

First, the economy is growing above trend and unemployment is coming down. While incomes are still growing slowly, good employment prospects will continue to support households meeting their repayment obligations. Second, as noted earlier, households have taken the opportunity over the past decade to build prepayments in offset accounts and redraw facilities. In fact, despite the continuing rise in scheduled repayments, actual repayments relative to income have remained quite steady as the level of unscheduled repayments of principal has declined and offset the rise in scheduled repayments. Third, as noted earlier, lending standards have improved over the past few years, resulting in an improvement in the average quality of both banks’ and households’ balance sheets. Much slower growth in investor lending, and declining shares of interest-only and high-loan-to-valuation lending have also helped to reduce the riskiness of new lending. And at the insistence of the regulator, banks have been tightening their serviceability assessments. In addition, strong housing price growth in many regions over recent years will have lowered loan-to-valuation ratios for many borrowers. As noted earlier, arrears rates remain very low.

The discussion above has focussed on the average borrower but what about the marginal borrower? For example, will the tightening standards result in some households being constrained in the amount they can borrow with flow-on effects to the housing market and the economy? Our analysis suggests that while we should remain alert to this possibility, it seems unlikely to result in a widespread credit crunch. The main reason is that most households do not borrow the maximum amount anyway so will not be constrained by the tighter standards. While the changes to lending standards have tended to reduce maximum loan sizes, this has primarily affected the riskiest borrowers who seek to borrow very close to the maximum loan size and this is a very small group. Most borrowers will still be able to take out the same sized loan.

It has also been suggested that the expiry of interest-only loan terms will result in financial stress as households have to refinance into principal-and-interest loans that require higher repayments. Again, this is worth watching, but borrowers have been transitioning loans from interest-only to principal-and-interest for the past couple of years without signs of widespread stress. Our data suggest that most borrowers will either be able to meet these higher repayments, refinance their loans with a new lender, or extend their interest-only terms for long enough to enable to them to resolve their situation. There appears to be only a relatively small share of borrowers that are finding it hard to service a principal-and-interest loan, which is to be expected given that over recent years, serviceability assessments for these loans have been based on the borrower’s ability to make principal-and-interest repayments. So far, the evidence suggests that the transition of loans from interest-only to principal-and-interest repayments is not having a significant lasting effect on banks’ housing loan arrears rates.

The distribution of household debt

So far, I have focussed on data for the household sector as a whole. But an important aspect of considering the risks inherent in household debt is the distribution of that debt. If most of the debt is held by households with lower or less stable income for example, it will be more risky than if a substantial amount of the debt is held by households with higher or more stable income. In this respect, the data suggest that we can have some comfort. This graph shows the shares of household debt held by income quintiles – the bottom 20 per cent of incomes, the next 20 per cent and so on up to the top 20 per cent of incomes (Graph 5). And it shows how these shares have changed from the early 2000s until 2015, the latest period for which the data are available. Around 40 per cent of household debt is held by households that are in the top 20 per cent of the income distribution and this share has remained fairly steady for the past 20 years. Furthermore, households in the second highest quintile account for a further 25 per cent of the debt. So in total two-thirds of the debt is held by households in the top 40 per cent of the income distribution. Nevertheless, around 15 per cent of the debt is held by households in the lowest two income quintiles. Whether or not this presents risks is not clear. Retirees are typically captured in these lower income brackets and if this debt is connected with investment property from which they are earning income, it may not be particularly risky.

Graph 5

Another potential source of risk in the distribution of debt is the age of the head of the household. As noted, a regular, stable income is important for servicing debt so people in the middle stages of their careers typically have better capacity to take on and service debt. The next graph shows the shares of debt for various age groups for owner occupiers, and how they have moved over the past couple of decades (Graph 6).

Graph 6

Households in which the head is between the ages of 35 and 54 account for around 60 per cent of the debt. But there does appear over time to be a tendency for a higher share of owner occupier debt to be held by older age groups. In part, the growing share reflects structural factors like lower interest rates. More importantly, it is not clear whether the higher share of debt increases the risk that these households will experience financial stress. On the one hand, it might indicate that in recent years, people have been unable to pay down their debt by the time they retire. If they continue to have large amounts of debt at the end of their working life, they might therefore be vulnerable. On the other hand, people are now remaining in the workforce for longer, possibly a response to better health and increasing life expectancies. They also hold more assets in superannuation and have more investment properties. This improves their ability to continue to service higher debt. And there is no particular indication that older people have higher debt-to-income or debt servicing ratios than younger workers.

So while the economy wide household debt-to-income ratio is high and rising, the distribution of that debt suggests that a large proportion of it is held by households that have the ability to service it. It nevertheless bears watching.

Regional dimensions

I thought I would finish off with some remarks about regional versus metropolitan differences. From a financial stability perspective, we are mainly focussed on the economy as a whole. But we still need to be alert to pockets of risk that have the potential to spill over more broadly. These risks may have important regional dimensions, particularly to the extent that individual regions have less diversified industrial structures and are thus more vulnerable to idiosyncratic shocks. One recent example has been the impact of the downturn in the mining sector on economic conditions in Western Australia, and the subsequent deterioration in the health of household balance sheets and banks’ asset quality. The potential for the drought in eastern Australia to result in household financial stress is another.

Data limitations make it difficult to drill down too far into particular regions. So I am going to focus here on a general distinction between metropolitan areas and the rest of Australia. As noted above, there tends to be a relationship between debt and housing prices. As housing prices rise, people need to borrow more to purchase a home and with more ability to borrow, people can bid up the prices of housing. So one place to look for a metro/regional distinction might be housing prices.

While there is clearly a difference in the absolute level of housing prices in cities and regional areas, over the long sweep, movements in housing prices in the regions have pretty much kept up with those in capital cities (Graph 7). This graph shows an index of housing prices for each of the states broken down into capital city and rest of the state. While there are periods where growth in housing prices diverge, most obviously in NSW and Victoria in recent years, they follow a very similar pattern. This partly reflects the fact that some cities that are close to the capitals tend to experience similar movements in house prices as the capitals.

Graph 7

What about housing debt in regional areas? The data suggest that the incidence of household indebtedness is broadly similar in the capital cities and in the regions (Graph 8). In 2015, the latest year for which we have data, around 50 per cent of regional households were in debt compared with around 45 per cent of households in capital cities. But in previous years this was reversed. At a broad level, the proportion of households in debt seems fairly similar.

Graph 8

Incomes and housing prices tend to be lower on average in regional areas than cities so we might expect debt to also be lower. But how do debt-to-income ratios compare? This next graph shows debt-to-income ratios for cities and regional areas at various points over the past 15 years (Graph 9). In general, average debt-to-income ratios for indebted households in capital cities tend to be a bit higher than those for indebted households in regional Australia. But it is not a huge difference and it mostly reflects the fact that people with the highest incomes – and therefore, higher capacity to manage higher debt-to-income ratios – tend to be more concentrated in cities. In general, it seems that regional households’ appetite for debt is very similar to that of their city counterparts.

The RBA has left the cash rate on hold once again, and there is no real indication of this changing in the months ahead. We are in a holding pattern for some time to come. They flag concerns about household consumption. We agree.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions remain expansionary, although they are gradually becoming less so in some countries. There has been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates are higher than they were at the start of the year, although they have declined somewhat since the end of June. These higher money-market rates have not fed through into higher interest rates on retail deposits. Some lenders have increased mortgage rates by small amounts, although the average mortgage rate paid is lower than a year ago.

The Bank’s central forecast is for growth of the Australian economy to average a bit above 3 per cent in 2018 and 2019. In the first half of 2018, the economy is estimated to have grown at an above-trend rate. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years due to rises in some commodity prices. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, but it has depreciated against the US dollar along with most other currencies.

The outlook for the labour market remains positive. The unemployment rate has fallen to 5.3 per cent, the lowest level in almost six years. The vacancy rate is high and there are reports of skills shortages in some areas. A further gradual decline in the unemployment rate is expected over the next couple of years to around 5 per cent. Wages growth remains low, although it has picked up a little recently. The improvement in the economy should see some further lift in wages growth over time, although this is likely to be a gradual process.

Inflation is around 2 per cent. The central forecast is for inflation to be higher in 2019 and 2020 than it is currently. In the interim, once-off declines in some administered prices in the September quarter are expected to result in headline inflation in 2018 being a little lower, at 1¾ per cent.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Housing credit growth has declined to an annual rate of 5½ per cent. This is largely due to reduced demand by investors as the dynamics of the housing market have changed. Lending standards are also tighter than they were a few years ago, partly reflecting APRA’s earlier supervisory measures to help contain the build-up of risk in household balance sheets. There is competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The RBA has released their Corporal Plan for 2018/2019. In the section on Financial Stability they call out specific risks in the home lending market, relating to credit quality.

During 2018/19 to 2021/22, the main risks to financial stability will most likely continue to relate to credit quality. Notably, banks’ large exposure to a potential deterioration in housing loan performance is expected to remain a key issue, requiring ongoing monitoring by both banks and regulators.

They also highlight the role of the Council of Financial Regulators (CFR), and the issues raised by the Productivity Commission and Royal Commission:

The Reserve Bank works with other regulatory bodies in Australia to foster financial stability. The Governor chairs the Council of Financial Regulators (CFR) – comprising the Reserve Bank, the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC) and the Australian Treasury – whose role is to contribute to the efficiency and effectiveness of regulation and the stability of the financial system. The Bank’s central position in the financial system, and its position as the ultimate provider of liquidity to the system, gives it a key role in financial crisis management, in conjunction with the other members of the CFR.

The Reserve Bank will continue working with the other CFR agencies to support financial stability. In the period ahead this will be informed by the Financial Sector Assessment Program review of Australia being conducted by the International Monetary Fund during 2018. The Bank and other CFR agencies

will also carefully consider the implications for the resilience of the financial sector arising from findings and recommendations of the final report of the Productivity Commission’s review of competition in the financial system, as well as the outcomes of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. The Bank will also continue working with APRA and with other regulators to monitor and, where necessary, respond to risks that may emerge from economic and financial shocks emanating from Australia or abroad.

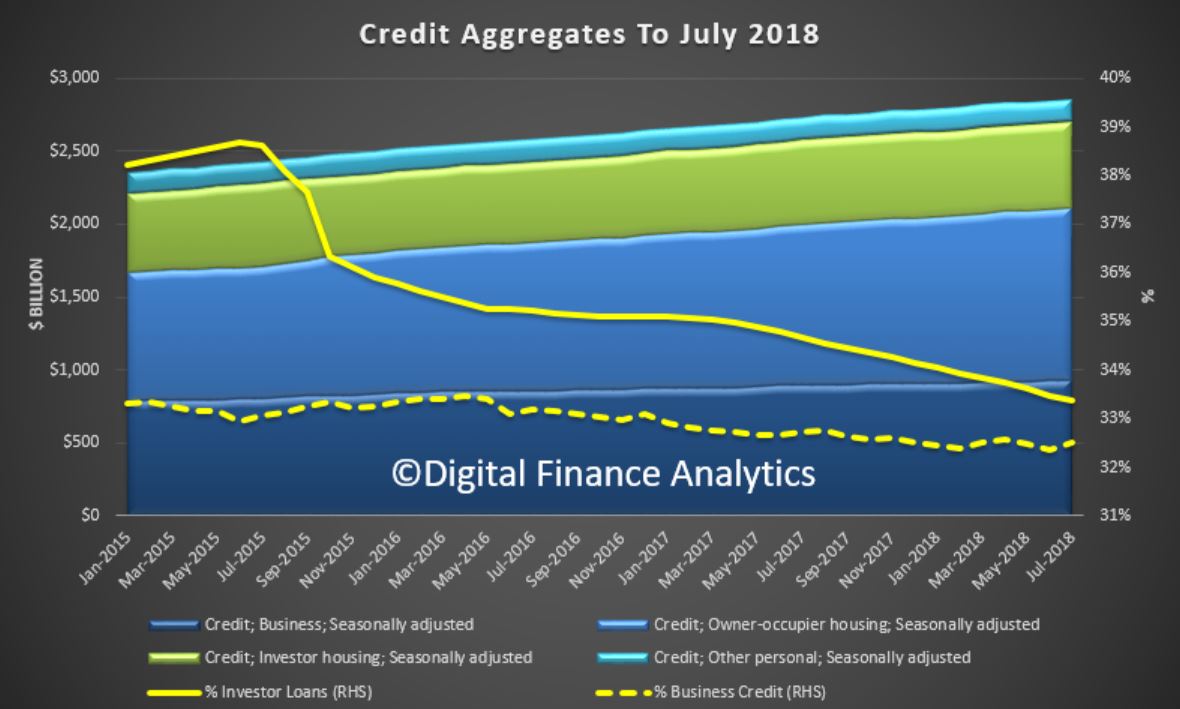

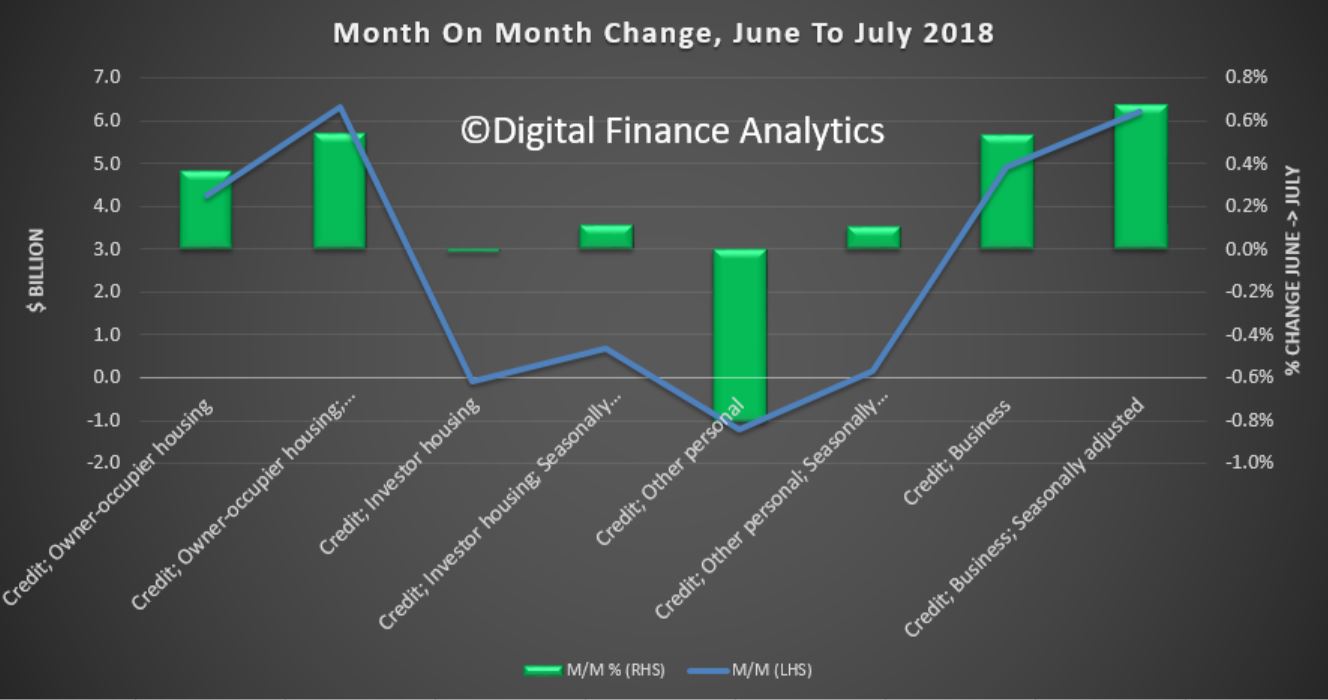

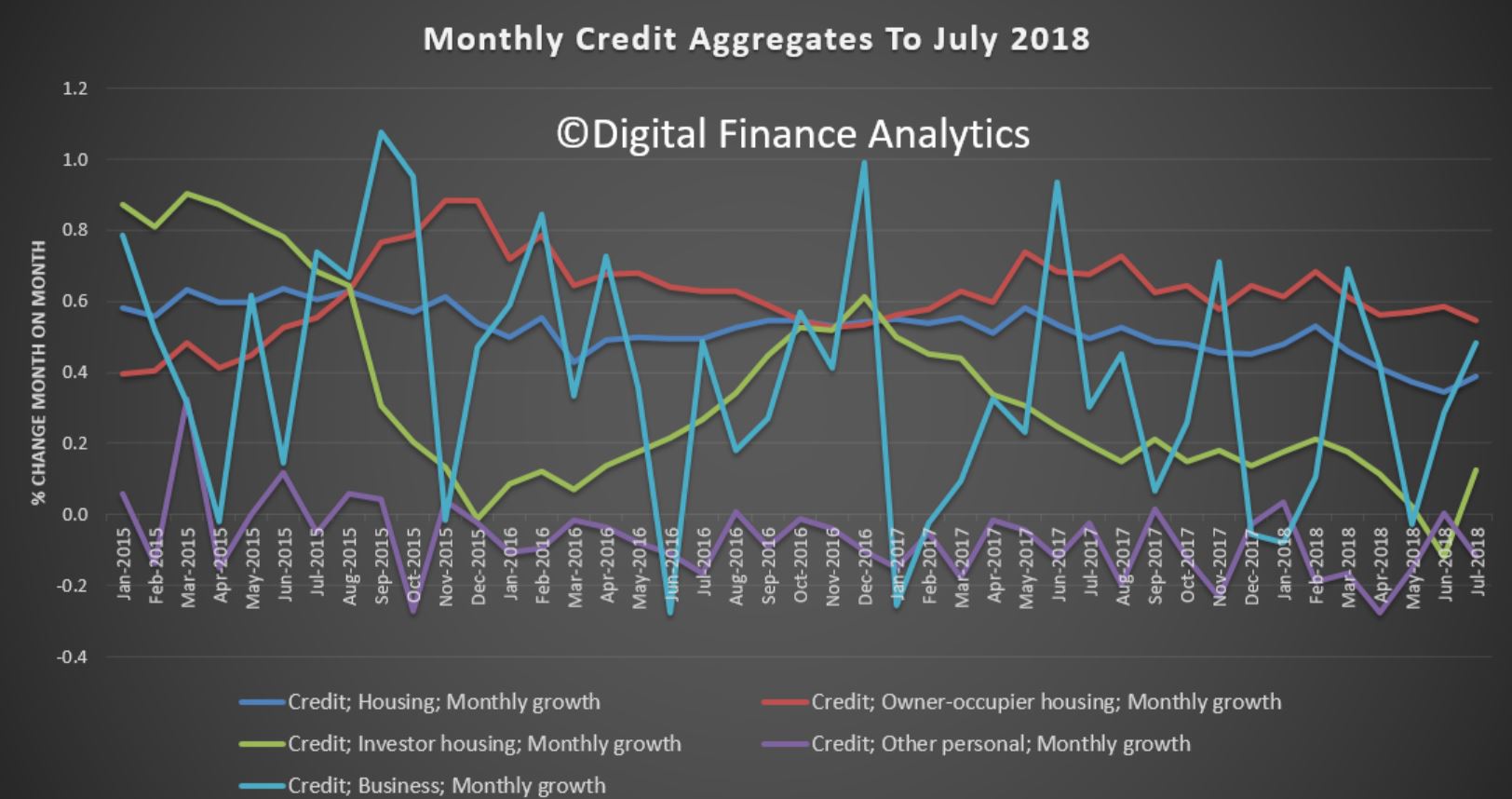

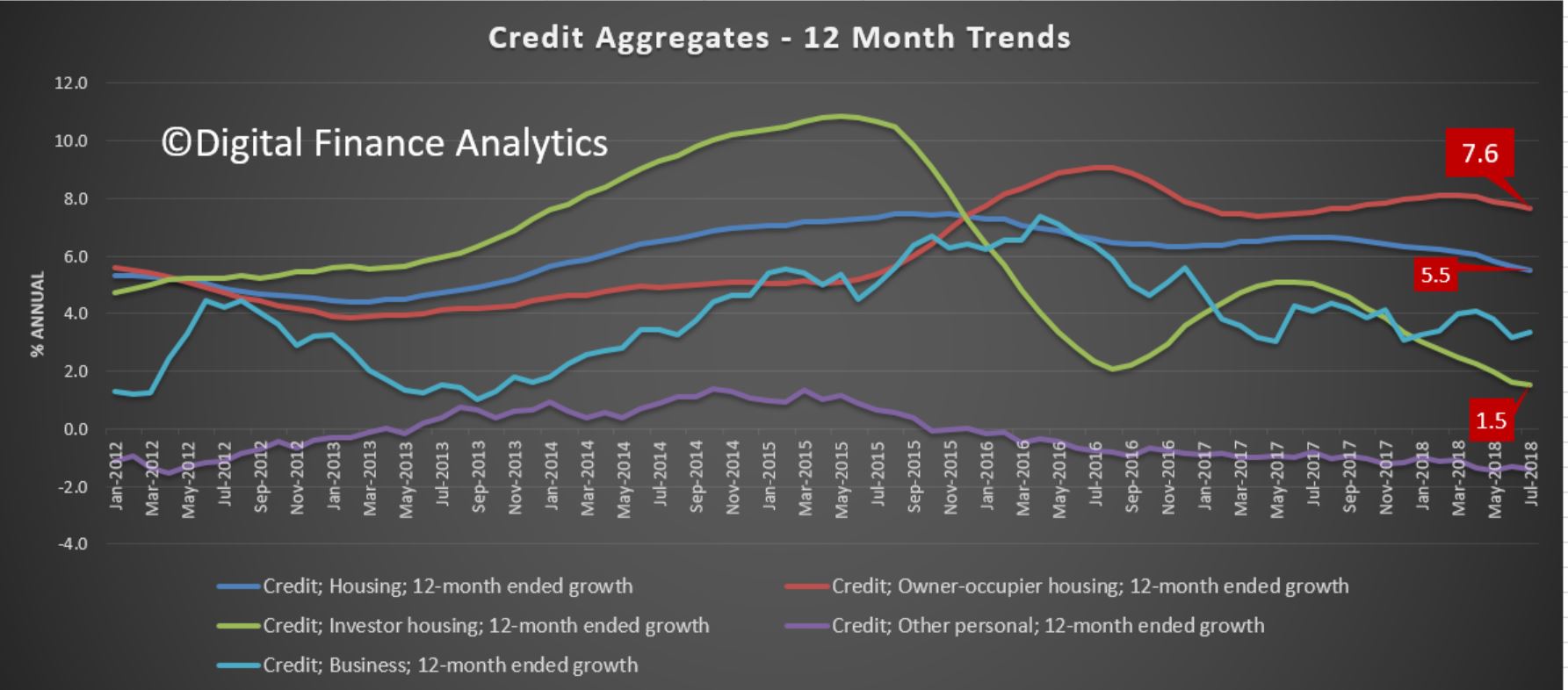

The monthly RBA credit aggregates for July are out today. Total credit for housing rose 0.2% in the month, to $1.77 trillion, with owner occupied credit up 0.5% to $1.18 trillion and investment lending down 0.1% to $593 billion. Investment housing credit fell to 33.4% of the portfolio, and business credit was 32.5%.

Interestingly the RBA’s seasonally adjusted numbers lifted credit growth from the non-adjusted set, but we are skeptical of these adjustments, given the current abnormal conditions in the market (especially taking into account the APRA data today).

That said, the trends tell the story, with the noisy monthly chart

less easy to read than the annual charts. Owner occupied housing is growing at 7.6%, investment housing at 1.5% and overall housing at 5.5%.

We still see some growth in the non-bank sector, and this month the RBA reported NO switching between investment and owner occupied loans.

So overall, the credit tightening continues to bite and investors are at the sharp end. No reason to think this will change, as it is driven by more responsible lending practices.

RBA Deputy Governor Guy Debelle spoke on Inflation. He looked at the trends, and also the segmental breakup. We will look at the first part of the speech where he discussed the overview and then dive into the housing related elements.

We continue to hold the view that the official measure has very little to do with the real exp[experience of many households.

The inflation rate is currently just over 2 per cent (Graph 1). This is consistent with the inflation target for the Reserve Bank agreed between the Governor and the Treasurer. However, that follows a period where inflation has been a little below target for a number of quarters. While inflation has averaged 2½ per cent since the inflation target was introduced, over the past three years it has averaged 1.8 per cent (Table 1).

Graph 1

How broad based has the recent decline in inflation been? In 2016, only around one-quarter of the CPI basket had an inflation rate of above 2.5 per cent. In the June quarter this had risen but only to 40 per cent. To look at it another way, in recent quarters around 80 per cent of the basket had an inflation rate below its inflation-targeting average (Graph 2).

Graph 2

There are a number of macroeconomic forces at work that have contributed to these outcomes, but today I am going to focus on some of the individual price developments that underpin the aggregate inflation outcome. I will examine pricing dynamics at a more disaggregated level and how these dynamics have changed in recent years. An understanding of these changing dynamics and what might be behind them is useful in assessing the outlook for inflation. Important drivers of recent lower outcomes include competition in the retail sector, historically low increases in rents, low wages growth and slower growth in some administered prices.

Table 1: Inflation by Component(a)

Effective weight

Average since 1993

Average since 2015

Retail

30

1.2

−0.1

Consumer durables(b)

15

0.1

−0.8

Food(c)

7

2.4

−0.1

Fruit and vegetables

2

3.2

1.1

Alcoholic drinks

4

2.7

1.6

Non-alcoholic drinks

1

2.3

−0.5

AVC and telecommunications equipment

4

−2.8

−4.7

Housing(d)

17

3.0

1.9

New dwelling purchase

8

3.5

2.8

Rents

7

2.9

0.7

Dwelling maintenance and repair

2

2.2

2.2

Administered prices

19

4.4

3.8

Utilities

4

4.5

4.2

Education

4

5.1

3.2

Health

5

4.3

4.0

Other administered

5

4.0

3.6

Market services(e)

18

2.9

2.0

Tobacco

3

8.4

13.9

Automotive fuel

3

3.3

6.7

Holiday travel and accommodation

6

2.2

0.8

Headline CPI(f)

100

2.5

1.8

Trimmed mean(f)

70

2.6

1.8

(a) Adjusted for the tax changes of 1999-2000

(b) Excludes audio, visual and computing equipment

(c) Excludes fruit, vegetables, meals out and takeaway food

(d) Excludes administered prices

(e) Excludes domestic travel and telecommunications equipment and services

(f) Excludes interest charges and indirect deposit and loan facilities

Sources: ABS; RBA

Housing

The cost of housing services has a large weight in the CPI, with the weight about equally split between the cost of building a new home and the cost of renting (Graph 8). There have been quite divergent dynamics in each of these two components in recent years.

Graph 8

New dwelling costs

New dwelling cost inflation, which has an 8 per cent weight in the CPI basket, has tended to move closely with the residential building cycle over time (Graph 9). However, despite the historically high level of activity in housing construction over recent years, new dwelling cost inflation has been running at a bit below its long-run average. During the late 2000s, new dwelling cost inflation was higher than it is currently because the residential construction sector was competing for materials and labour with the resources sector in the midst of its investment boom. This competition for inputs has clearly abated. Wages growth in housing construction has been generally contained except for some particular skills such as bricklayers, in part because workers have been moving from the resources sector as projects there finished and also reflecting the general slow pace of wages growth in the economy. Reports from liaison suggest that competition for inputs between public infrastructure projects and high-rise residential developments has put some upward pressure on new dwelling cost inflation in Sydney and Melbourne. This includes competition for labour such as engineers and project managers, as well as competition for materials such as concrete. Liaison contacts suggest that firms have also been able to limit cost inflation by switching to lower-cost building materials.

Graph 9

Rents

The pace of rent inflation has been falling since 2008, and year-ended rent inflation is around its lowest level since the mid 1990s. This has been a considerable drag on inflation: rental inflation was nearly 3 percentage points lower per annum in the past three years than in the previous twenty, which has reduced aggregate inflation by nearly 0.2 percentage points per annum in recent years.

The decline in rent inflation can be attributed to a mix of supply and demand side developments. As mentioned, housing construction activity has grown strongly in recent years, which has increased the supply of rental properties. Growth in the housing stock has outstripped population growth since 2014, which put downward pressure on rents. Furthermore, rents are changed relatively infrequently and can be indexed to CPI inflation, so there is a self-reinforcing dynamic to this too.

The national rent inflation series masks considerable variation across capital cities. Rent inflation has been much lower in Perth than in other capital cities in recent years, indeed rents have been falling in Perth at quite a rapid rate for a number of years. The vacancy rate in Perth – that is, the share of properties that are vacant and available to rent – has more than doubled since 2008.

But slower growth in rents is not just a Perth story. Rent inflation in Sydney and Melbourne has slowed considerably in recent years reflecting the substantial additions to the dwelling stock in these cities, and notwithstanding the faster population growth, particularly in Melbourne. Rents are flat in Brisbane and Adelaide. Only in Hobart are rents growing at a high rate.

We expect the pace of rent inflation to increase gradually over the next couple of years. The vacancy rate has declined over the last year, and newly advertised rent growth has increased. However, it will take some time for the flow of new rents to materially affect the stock of rents captured in the CPI.

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports.

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports.