The latest 62 page edition of the RBA Financial Stability Review has been released, and it continues their line “of some risks, but no worries”. International economic conditions, and business confidence are, they say, on the improve while Australian household balance sheets and the housing market remain a core area of interest. The potential impact of rising rates and flat income are discussed, once again, but little new is added into the mix.

From a financial stability perspective, banks hold more capital, have tightened lending standards, and shadow banking is under control.

The key domestic risks in the Australian financial system continue to stem from household borrowing. Household indebtedness, most of which is mortgage borrowing, is high and gradually rising against a backdrop of low interest rates and weak income growth. While some households have taken advantage of low interest rates to make excess mortgage payments, others have increased their borrowing. Higher interest rates, or falls in income, could see some highly indebted households struggle to service their debt and so curtail their spending.

Prepayments are an important dynamic in the Australian mortgage market as they allow households to build a financial buffer to cushion mortgage rate rises or income falls. Aggregate mortgage buffers – balances in offset accounts and redraw facilities – remain around 17 per cent of outstanding loan balances, or over 2½ years of scheduled repayments at current interest rates.

These aggregates, however, mask substantial variation; about one-third of mortgages have less than one months’ buffer Not all of these are vulnerable given some borrowers have fixed rate mortgages that restrict prepayments, and some are investor mortgages where there are incentives to not pay down tax deductible debt. This leaves a smaller share of potentially vulnerable borrowers with new mortgages who have yet to accumulate prepayments, and borrowers who may not be able to afford prepayments. Partial data suggest that the share of households with only small buffers has declined in recent years, in part due to declines in mortgage rates. Households with small buffers also tend to be lower-income or lower-wealth households, which could make them more vulnerable to financial stress.

Household indebtedness is high and, against a backdrop of low interest rates and weak income growth, debt levels relative to income have continued to edge higher. Steps taken by regulators in the past few years to strengthen the resilience of balance sheets, including limiting the pace of growth of investor lending, discouraging loans with high loan-to-valuation ratios (LVRs) and strengthening serviceability metrics, have seen the growth in riskier types of lending moderate. The most recent focus has been on limiting interest-only lending, and banks have responded by further reducing lending with high LVRs for interest-only loans, increasing interest rates for some types of mortgages and significantly reducing interest-only lending.

The tightening of banks’ lending standards for property loans is constraining some households and developers but, in doing so, making the balance sheets of both borrowers and lenders more resilient. Conditions are relatively weak in the Brisbane apartment market, with a large increase in supply reflected in declines in prices and rents. There are, however, few signs of significant settlement difficulties to date. More generally, while housing market conditions vary across the country, there are signs of easing of late, particularly in Sydney and Melbourne where conditions have been strongest.

With the tightening of lending standards, there is a potential that riskier lending migrates into the non-bank sector. To date, non-bank financial institutions’ residential mortgage lending has remained small though their lending for property development has picked up recently. While the banking system has minimal exposure to the non-bank financial sector, growth in finance outside the regulated sector is an area to watch.

Here are some of the other nuggets:

Very low interest rates have also contributed to strong growth in property prices internationally as investors search for yield. To the extent that prices have moved beyond what their underlying determinants suggest, this increases the risk of sharp price falls if interest rates were to rise suddenly or if risk sentiment were to deteriorate.

While household debt levels are high, and rising, to date the impact on households’ ability to service their debt has been muted by falls in interest rates to historically low levels. Nonetheless, highly indebted households are more likely to struggle to repay their debts, or substantially reduce their consumption, in response to a negative shock, such as a rise in unemployment, an unexpectedly large increase in interest rates or a sharp fall in housing prices.

The distribution of debt is also important in identifying where risks lie as typically it is not the ‘average’ household that gets into financial In Canada and Sweden, for example, the risks from high household debt may be heightened since the debt is concentrated among younger and low‑to-middle-income households, who are likely to be more vulnerable

to negative shocks.

Further, interest-only (IO) lending has been identified as increasing risks in some jurisdictions.4 Households with IO loans remain more indebted throughout the life of the loan than if they had been paying down the loan principal, making them more vulnerable to higher interest rates, reduced income, or lower housing prices. Such households are also more vulnerable to ‘payment shock’ due to the increase in repayments following the end of the interest-only period of the loan.

Global experience is that the culture within banks can have a major bearing on how a wide range of risks are identified and managed. There have been a number of examples where the absence of strong positive culture has given rise to a deterioration in asset performance, misconduct and loss of public trust. In Australia, there have also been examples of weak internal controls causing difficulties for some banks. These include in the areas of life insurance, wealth management and, more recently, retail banking. In August, AUSTRAC (the Australian Transaction Reports and Analysis Centre) initiated civil proceedings against the Commonwealth Bank of Australia for breaches of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006. In the current environment where investors still expect high rates of return, despite regulatory and other changes that have reduced bank ROE, banks need to be careful of taking on more risk to boost returns.

A central element to address this issue is to ensure that banks build strong risk cultures and governance frameworks. Regulators have therefore heightened their focus on culture and the industry is taking steps to improve in this area.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy have improved. Labour markets have tightened and above-trend growth is expected in a number of advanced economies, although uncertainties remain. Growth in the Chinese economy is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. Australia’s terms of trade are expected to decline in the period ahead but remain at relatively high levels.

Wage growth remains low in most countries, as does core inflation. Headline inflation rates are generally lower than at the start of the year, largely reflecting the earlier decline in oil prices. In the United States, the Federal Reserve has indicated that it will begin the process of balance sheet normalisation in October and that it expects to increase interest rates further. In the other major economies, there is no longer an expectation of additional monetary easing. Financial markets have been functioning effectively and volatility remains low.

The Australian economy expanded by 0.8 per cent in the June quarter. This outcome and other recent data are consistent with the Bank’s expectation that growth in the Australian economy will gradually pick up over the coming year.

Over recent months there have been more consistent signs that non-mining business investment is picking up. A consolidation of this trend would be a welcome development. Business conditions as reported in surveys are at a high level and capacity utilisation has risen. A large pipeline of infrastructure investment is also supporting the outlook. Against this, slow growth in real wages and high levels of household debt are likely to constrain growth in household spending.

Employment has continued to grow strongly over recent months. Employment has increased in all states and has been accompanied by a rise in labour force participation. The various forward-looking indicators point to solid growth in employment over the period ahead, although the unemployment rate is expected to decline only gradually over the next couple of years.

Wage growth remains low. This is likely to continue for a while yet, although the stronger conditions in the labour market should see some lift in wage growth over time. Inflation also remains low and is expected to pick up gradually as the economy strengthens.

The Australian dollar has appreciated since mid year, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to continued subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Growth in housing debt has been outpacing the slow growth in household incomes for some time. To address the medium-term risks associated with high and rising household indebtedness, APRA has introduced a number of supervisory measures. Following some tightening in credit conditions, growth in borrowing by investors has slowed a little recently. In the housing market, conditions continue to vary considerably around the country. Housing prices have been rising briskly in some markets, while in others they have been declining. In Sydney, where prices have increased significantly, there have been further signs that conditions are easing. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases remain low in most cities.

The low level of interest rates is continuing to support the Australian economy. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

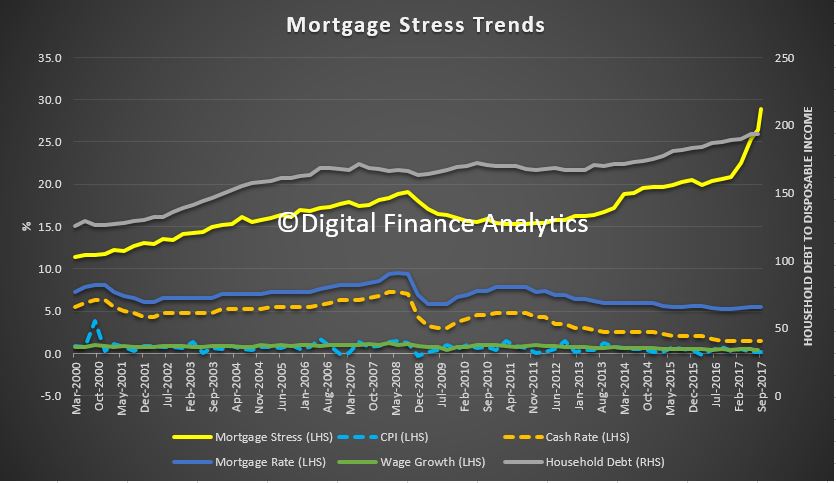

Mortgage stress rose again in September according to Digital Finance Analytics analysis, crossing the 900,000 household rubicon for the first time. The latest RBA data shows household debt to income rose again in June, to 193.7, further confirmation of Australia’s debt problem.

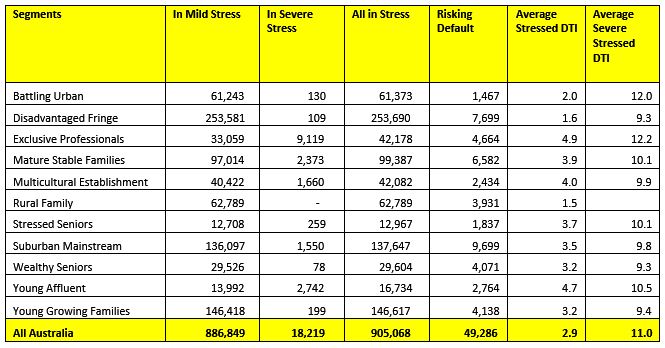

Across the nation, more than 905,000 households are estimated to be now in mortgage stress (last month 860,000) and more than 18,000 of these in severe stress. This equates to 28.9% of households. A rising number of more affluent households are being impacted as the contagion of mortgage stress continues to spread beyond the traditional mortgage belts. We estimate that more than 49,000 households risk default in the next 12 months, up 3,000 from last month.

Watch the video to learn more, and count down the latest top 10 post codes. We had some new regions “promoted” into the list this time.

The main drivers of stress are rising mortgage rates and living costs whilst real incomes continue to fall and underemployment remains high. Some households are now making larger mortgage repayments following out of cycle interest rate rises, and are simultaneously facing higher power prices, council rates and childcare costs. This remains a deadly combination and is touching households across the country, not just in the mortgage belts.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end September 2017. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cashflow) does not cover ongoing costs. Households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell. The debt-to-income (DTI) ratios in severely stressed households are on average eleven times their current annual incomes and this is high on any measure. The combined statistics suggest there are continuing concerns about underwriting standards.

We revised our expectation of potential interest rate rises, given the stronger data on the global economy. Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes.

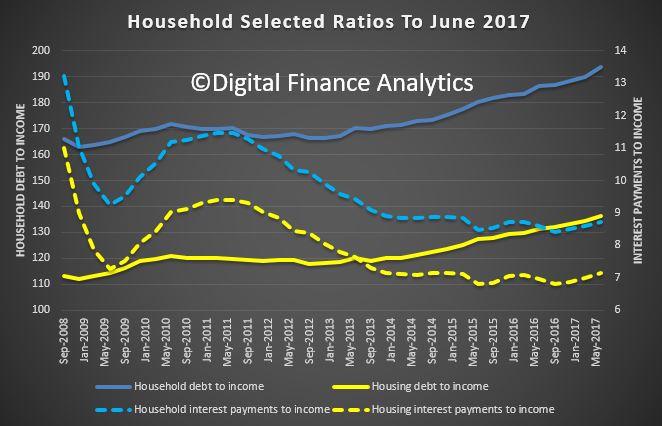

Martin North, Principal of Digital Finance Analytics said that “continued pressure from low wage and rising costs means those with bigger mortgages are especially under the gun. These stressed households are less likely to spend at the shops, which will act as a further drag anchor on future growth. The number of households impacted are economically significant, especially as household debt continues to climb to new record levels”. The latest household debt to income ratio is now at a record 193.7.[1]

Gill North, joint Principal of Digital Finance Analytics and a Professorial Research Fellow in the law school at Deakin University, citing her recent research, suggests the Australian house party has been glorious – but the hangover may be severe and more should be done to mitigate future risks and harm to highly indebted households and the nation.[2]

She notes that at the beginning of 2016 the RBA and APRA stood largely aloof from concerns around levels of household debt and the major risk was complacency. While the RBA and APRA have been more vocal since and have taken steps to tighten lending standards, she calls for additional measures and highlights the continuing vulnerability of many households without financial buffers for adverse contingencies.[3]

Regional analysis shows that NSW has 238,703 households in stress (238,755 last month), VIC 243,752 (236,544 last month), QLD 168,051 (146,497 last month) and WA 124,754 (118,860 last month). The probability of default rose, with around 9,300 in WA, around 9,100 QLD, 12,800 in VIC and 13,100 in NSW.

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The Sept 2017 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The Sept 2017 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

[1] RBA E2 Household Finances – Selected Ratios June 2017

[2] Gill North ‘The Australian House Party Has Been Glorious – But the Hangover May Be Severe: Reforms to Mitigate Some of the Risks’ in R Levy, M O’Brien, S Rice, P Ridge and M Thornton (eds), New Directions For Law In Australia (ANU Press, Canberra, 2017). An earlier version of this book chapter is available at https://ssrn.com/author=905894.

[3] See also, Gill North, ‘Regulation Governing the Provision of Credit Assistance & Financial Advice in Australia: A Consumer’s Perspective’ (2015) 43 Federal Law Review 369. An earlier draft of this article is available at https://ssrn.com/author=905894.

The RBA has updated its E2 Household Finances Selected Ratios to June 2017. As a result, we see another rise in the ratio of household debt to income, and housing debt to income. Both are at new record levels.

In addition, we see the proportion of income required to service these debts rising, as out of cycle rates rises hit home. These ratios are below their peaks in 2011, when the cash rate was higher, but it highlights the risks in the system should rates rise.

We discuss this further in our September Mortgage Stress Data, to be released shortly. The debt chickens will come home to roost!

But the policy settings are wrong, debt cannot continue to grow at more than three times cpi or wage growth.

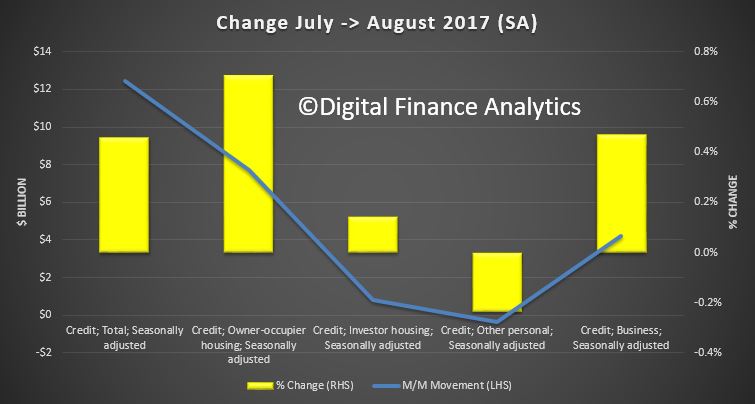

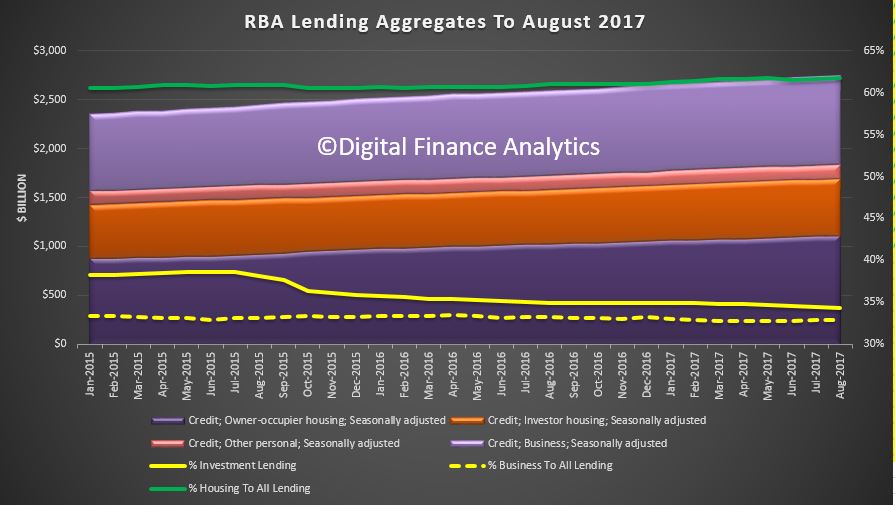

The latest RBA data on credit, to August 2017 tells a somewhat different story to the APRA data we discussed already. There were clearly adjustments in the system [CBA in particular?] and the non-bank sector is picking up some of the slack.

Overall housing credit rose 0.5% in August, and 6.6% year-ended August 2017. Personal credit fell again, down 0.2%, and 1.1% on a 12 month basis. Business credit also rose 0.5%, or 4.5% on annual basis. But overall lending for housing is still growing.

Here are the month on month (seasonally adjusted) movements. Owner occupied lending up $17.5 billion (0.68%), investment lending up $0.8 billion (0.14%), personal credit down $0.4 billion (-0.24%) and business lending up $4.2 billion or 0.47%.

As a result, the proportion of credit for housing (owner occupied and investor) still grew as a proportion of all lending.

Another $1.7 billion of loans were reclassified in the month. This will give an impression of greater slowing investment loan growth as a result.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $58 billion over the period of July 2015 to August 2017, of which $1.7 billion occurred in August 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

In short, the global economy is on the up, central banks are beginning to remove stimulus, and locally, wage growth is low, despite reasonable employment rates. Household debt is extended, but in the current low rates mostly manageable, but the medium term risks are higher. Business conditions are improving.

He then discusses the growth path from here, including the impact of higher debt on household balance sheets. We will need to deal with the higher level of household debt and higher housing prices, especially in a world of more normal interest rates. In this environment, a small shock could turn into a more serious correction as households seek to repair their balance sheets.

The Current Chapter

The storyline of the current chapter is well known. It has had two main plot lines.

The first was a troubled global economy. A decade ago we had the global financial crisis and the worst recession in many advanced economies since the 1930s. A gradual recovery then took place, but it was painfully slow. Recently, things have improved noticeably and unemployment rates in some advanced economies are now at the lowest levels in many decades. Throughout this chapter, central banks have mostly worried that inflation rates might turn out to be too low, not too high. Interest rates have been at record lows. And workers in advanced economies have experienced low growth in their nominal wages. So it’s been a challenging international backdrop.

The second plot line was the resources boom. Strong growth in China saw strong growth in demand for resources. Prices rose in response, with Australia’s terms of trade reaching the highest level in at least 150 years (Graph 1). Then an investment boom took place in response to the higher prices, with investment in the resources sector reaching its highest level as a share of GDP in over a century. And now we are seeing the dividends of this, with large increases in Australia’s resource exports.

Graph 1

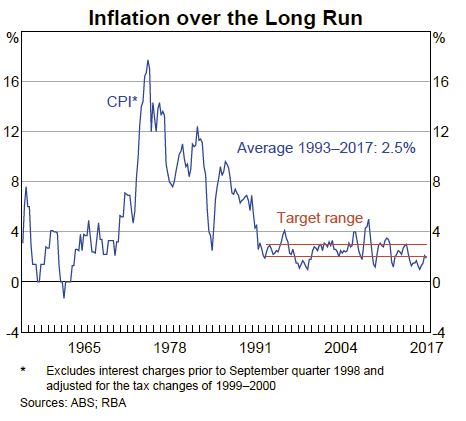

Overall, it has been a reasonably successful chapter in Australia’s economic history. Real income per person is around 20 per cent higher than it was in the mid 2000s and real wealth per person is 40 per cent higher. Australia is one of the few advanced economies that avoided a recession in 2008. And the biggest mining boom in a century did not end in a crash, as previous booms did. Our interest rates remained positive, unlike those in many other advanced economies. Since the mid 2000s, the unemployment rate has averaged 5¼ per cent, a better outcome than in the previous three decades. Inflation has averaged 2½ per cent. And over this period, GDP growth has averaged 2¾ per cent, higher than in most other advanced economies.

So, taking the period as a whole, it is a positive picture.

At the same time, though, as the chapter draws to a close, we do face some issues. I would like to highlight three of these.

The first is the recent slow growth in real per capita income. For much of the past two decades, real national income per person grew very strongly in Australia (Graph 2). We benefited from strong productivity growth, higher commodity prices and more of the population working. In contrast, since 2011 there has been little net growth in real per capita incomes. This change in trend is proving to be a difficult adjustment. The solutions are strong productivity growth and increased labour force participation.

Graph 2

A second issue is the unusually slow growth in nominal and real wages. Over the past four years, the increase in average hourly earnings has been the slowest since at least the mid 1960s (Graph 3). This is partly a consequence of the unwinding of the mining boom but there are structural factors at work as well. The slow growth in wages is putting a strain on household budgets and contributing to low rates of inflation.

Graph 3

A third issue is the high level of household debt and housing prices. Over recent times, Australians have borrowed a lot to purchase housing. This has added to the upward pressure on housing prices, especially in our two largest cities, where structural factors are also at work. Australians are coping well with the higher level of debt, but as debt levels have increased relative to our incomes so too have the medium-term risks. The very high levels of housing prices in our largest cities are also making it difficult for those on low and middle incomes to buy their own home.

So as we turn the final pages of this chapter, these are some of the issues we face. But as we turn these pages, we also see improvements on a number of fronts.

Business conditions, as reported in surveys, are at the highest level in almost 10 years. There are also growing signs that private investment outside the resources sector is picking up. We have been waiting for this for some time. For a number of years, animal spirits had been missing, with many firms preferring to put off making decisions about capital spending. It appears that some of this reluctance to invest is now passing. According to the June quarter national accounts, private non-mining business investment increased strongly over the first half 2017, to be around 10 per cent above the level at the start of 2016. Non-residential building approvals have increased to be above the levels of recent years and there is a large pipeline of public infrastructure investment to be completed (Graph 4). The decline in mining investment has also largely run its course.

Graph 4

There has also been positive news on the employment front. Over the past year, the number of people with jobs has increased by more than 2½ per cent, a positive outcome given that the working-age population is increasing at around 1½ per cent a year. Growth in full time employment has been particularly strong. The various forward-looking indicators suggest that labour market conditions will remain positive in the period immediately ahead.

Here in Western Australia, there are also some signs of improvement after what has been a difficult few years. The drag from declining mining investment is diminishing. Businesses are feeling more positive than they were a year ago and employment has been rising after a period of decline. At the same time though, conditions in the housing market remain difficult, with housing prices and rents continuing to fall in Perth. Weak residential construction has also weighed on aggregate demand over the first half of this year, although building approvals and liaison reports point to some stabilisation in the period ahead (Graph 5).

Graph 5

For Australia as a whole, the recent national accounts – which showed a healthy increase in output of 0.8 per cent in the June quarter – were in line with the Bank’s expectations. These, and other recent data, are consistent with the Reserve Bank’s central scenario for GDP growth averaging around the 3 per cent mark over the next couple of years. This is a bit faster than our current estimate of trend growth in the Australian economy, so we expect to see a gradual decline in the unemployment rate. This should lead to some pick-up in wage growth, although we expect this to be a gradual process given the structural factors at work that I have spoken about on previous occasions. We can also expect to see a gradual increase in inflation back towards the middle of the 2 to 3 per cent medium-term target range.

There are clearly risks around this central scenario. We would like to see the improvement in business investment consolidate and a continuation of job growth at a rate at least sufficient to absorb the increase in Australia’s workforce. Some pick-up in wage growth in response to the tighter labour market would also be a welcome development. So these are some areas to watch. But as things stand, the economy does look to be improving.

The Next Chapter

I would now like to lift my gaze a little and turn to the next chapter in our economic story. I would like to sketch out four of the possible plot lines, acknowledging that, as in all good stories, there are likely to be plenty of surprises along the way.

Shifts in the global economy

A first likely plot line, as it has been in previous chapters, is the ongoing shift in the global economy. Here, changes in technology and further growth in Asia are likely to be prominent themes.

In some quarters there is pessimism about future prospects for the global economy. The pessimists cite demographic trends, high debt levels, increasing regulatory burdens that stifle innovation and political issues. They see a future of low productivity growth and only modest increases in average living standards.

It’s right to be concerned about the issues that the pessimists focus on, but I am more optimistic about the ability of technological progress to propel growth in the global economy, just as it has done in the past. We are still learning how to take advantage of recent advances in technology, including the advances in the tools of science. In time we will do this and new industries and methods of production will evolve, some of which are hard to even imagine today. So there is still plenty of upside. The challenge we face is to make sure that the benefits of technological progress are widely shared. How well we do this could have a major bearing on the next chapter.

Beyond this broad theme, it is appropriate to recognise the important leadership role that the United States plays in the global economy. If the US economy does well, so does most of the rest of the world. The United States has long been a strong supporter of open markets and a rules-based international system. It has been the breeding ground for much of the progress in technology. And it has been a safe place for people to invest and an important source of financial capital for other countries. It is in our interests that the United States continues to play this important role. A retreat would make our lives more complicated.

Another important influence on the next chapter is how things play out in China. While growth in China is trending lower, the share of global output produced in China will continue to rise, as per capita incomes converge towards those in the more advanced economies (Graph 6). As this convergence takes place, the structure of the Chinese economy will change and so too will China’s economic relationship with Australia. Exports of resources will continue to be an important part of that relationship, but increasingly trade in services and other high valued-added activities, including food, will become more important. Notwithstanding this, there are risks on the horizon, with the Chinese economy going through some difficult adjustments. One of these is the switch from a growth model based on industrial expansion to one based more on services. Another is managing an increasingly large and complex financial system. Australia has a strong interest in China successfully managing these challenges.

Graph 6

Another shift in the global economy that could shape the next chapter is the growth of other economies in Asia. Developments in India and Indonesia bear especially close watching. Both of these countries, especially India, have very large populations, and per capita incomes are still quite low. In time, the effects of economic progress in these countries and others in the region could be expected to have a substantial effect on the Australian economy, just as the development of China has.

Normalisation of monetary conditions

A second likely plot line of the next chapter is a return to more normal monetary conditions globally. Since the financial crisis we have been through an extraordinary period in monetary history. Interest rates have been very low and even negative in some countries. Central banks have greatly expanded their balance sheets in order to buy assets from the private sector (Graph 7). This period of monetary expansion is now drawing to a close.

Graph 7

Some normalisation of monetary conditions globally should be seen as a positive development, although it does carry risks. It is a sign that economic growth in the advanced economies has become self-sustaining, rather than just being dependent on monetary stimulus. It would also lift the return to many savers who have been receiving very low returns on interest-bearing assets for a decade now.

On the other side of the ledger, periods of rising interest rates globally have, historically, exposed over-borrowing somewhere in the global system. Investment strategies that looked sensible when interest rates were very low tend not to look so good when interest rates are higher.

We can take some comfort from the major efforts over the past decade to improve the resilience of the global financial system. But at the same time, investors have increasingly been prepared to take more risk in the search for yield. Many continue to expect a continuation of low rates of inflation and low interest rates, despite quite low unemployment rates in a number of countries. So this is an area that is worth watching. If higher interest rates are the result of a surprise increase in inflation, financial markets could be in for a difficult adjustment.

A rise in global interest rates has no automatic implications for us here in Australia. Notwithstanding this, an increase in global interest rates would, over time, be expected to flow through to us, just as the lower interest rates have. Our flexible exchange rate though gives us considerable independence regarding the timing as to when this might happen.

Higher levels of debt

This brings me to a third plot line: that is, how we deal with the higher level of household debt and higher housing prices, especially in a world of more normal interest rates.

It is likely that higher levels of household debt change household spending patterns. Having increased their borrowing, households are less inclined to let consumption growth run ahead of growth in incomes for too long. Higher levels of debt also mean that household spending could be quite sensitive to increases in interest rates, something the Reserve Bank will be paying close attention to.

To date, households have been coping reasonably well with the higher debt levels. The aggregate debt-to-income ratio has trended higher, but the ratio of interest payments to income is not particularly high, given the low level of interest rates (Graph 8). Housing loan arrears remain low, although they have increased a little recently, especially here in Western Australia.

Graph 8

Over recent times, one issue that the Reserve Bank has focused on is the build-up of medium-term risks from growth in household debt persistently outpacing that in household income. Our concern has been that, in this environment, a small shock could turn into a more serious correction as households seek to repair their balance sheets. We have been working with APRA through the Council of Financial Regulators to address this risk. The various measures are having a positive impact in improving the resilience of household balance sheets.

A broadening of the drivers of growth

The fourth likely plot line is a broadening of the drivers of growth in the Australian economy. How the next chapter in our economic history turns out depends partly on our ability to lift productivity growth across a wide range of industries. The resources sector will, no doubt, continue to make an important contribution to the Australian economy, but it is unlikely that it will shape the next chapter in our economic history as it did the current chapter. With another major upswing in the terms of trade unlikely and the working-age share of our population having peaked as the population ages, improving productivity will be key to growth in our national income.

The drivers of growth are changing: they increasingly depend on our ability to produce innovative goods and services in a rapidly changing world. In this world, it is difficult to make precise predictions about where the jobs and growth in our economy are going to come from in the future. But it seems clear that we will be best placed to take advantage of whatever possibilities arise if businesses and our workforce are innovative and adaptable.

Australia is fortunate to have a natural resource base that provides an important source of national income, and this will remain the case. But in this next chapter we will need to look more directly to the skills of our workers and our businesses to drive economic growth. If we are to take advantage of the opportunities that are offered by technology and growth in Asia, we need a flexible workforce with strong skills in the areas of problem solving, critical thinking and communication. Investment in human capital will be one of the keys to success. We also need a competitive business environment that encourages innovation. How well the next chapter turns out will depend on how we do in these areas.

So, in summary these are some of the themes we might expect to see in the next chapter – the impact of technology and the growth of Asia; the normalisation of monetary conditions; the effects of higher levels of household debt; and the capability of our workforce and businesses to be flexible, innovative and adaptable.

This is, obviously, not a complete list. There are clearly other factors that could have a major influence on the storyline, including how geopolitical tensions are resolved and how we adjust to climate change. And no doubt there will be surprises as well.

But overall, I remain optimistic about how this next chapter might unfold. While we have our challenges, some of which I have talked about, we also have some advantages. We have a strong institutional and policy framework, a skilled, growing and diverse population and a wealth of mineral and agricultural resources. We have strong links to Asia, the fastest growing part of the global economy. We also have a flexible economy with a demonstrated capacity to adjust to a changing world.

These factors should give us confidence about our future. But we can’t rest on this and there are a number of significant risks. The world is a competitive place and the global economy is continuing to go through some challenging adjustments. If we are to do well in this world, we need to keep investing in both physical and human capital. We also need to keep investing in policy reform.

Finally, I have said relatively little about monetary policy today. This is partly because there are other forces that are likely to be more important in shaping the next chapter of the Australian economy. Monetary policy has an important role to play in supporting the economy as it goes through the current period of adjustment. It can also help stabilise the economy when it is hit by future shocks. Monetary policy can make for a more predictable investment climate by keeping inflation low and stable. Having a competent, analytical, transparent and independent central bank can also be a source of confidence in the country. But beyond these effects, monetary policy has little influence on the economy’s potential growth rate.

Over recent times, the Reserve Bank Board has not sought to overly fine-tune things. We have provided support and allowed time for the economy to adjust to the new circumstances. In its decisions, the Board has been careful to balance the benefit of providing this support with the risks that can come from rising household debt. As things currently stand, we look to be on course to make further progress in reducing unemployment and moving towards the midpoint of the medium-term inflation target. This would be a good outcome.

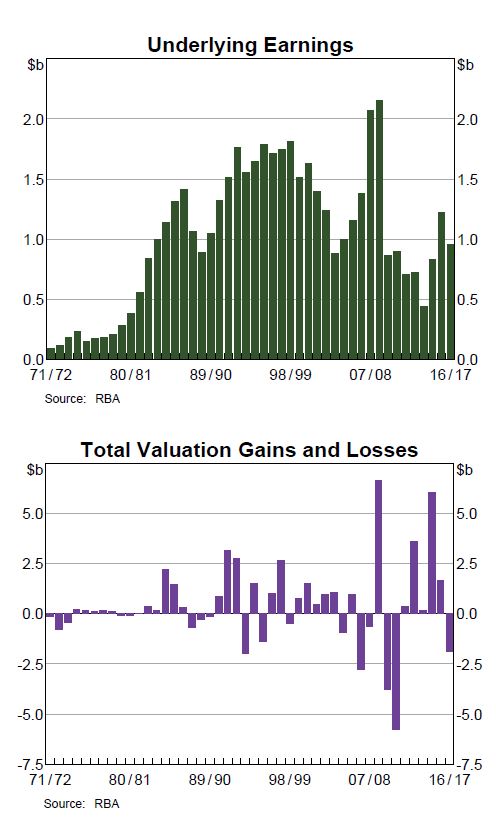

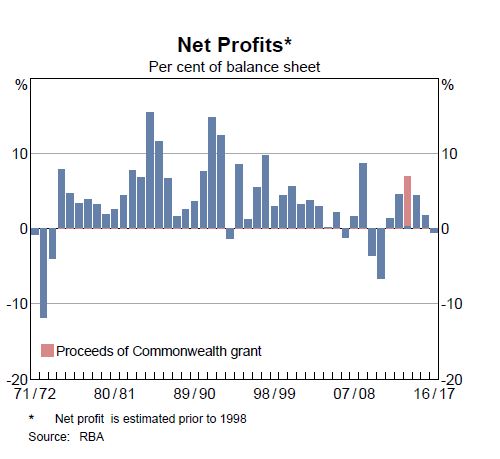

The RBA published their Annual Report for 2017. They reported an accounting loss of $897 million, or 0.5 per cent of the balance sheet, in 2016/17. The Bank’s underlying earnings were offset by net valuation losses of $1 857 million. The Treasurer, after consulting the Board, determined that all earnings available for distribution in 2016/17, a sum of $1 286 million, would be paid as a dividend to the Commonwealth.

The Reserve Bank of Australia is established by statute as Australia’s central bank. Its enabling legislation is the Reserve Bank Act 1959. The Bank pursues national economic policy objectives. Its responsibility for monetary policy is set out in section 10(2) of the Reserve Bank Act, which states:

It is the duty of the Reserve Bank Board, within the limits of its powers, to ensure that the monetary and banking policy of the Bank is directed to the greatest advantage of the people of Australia and that the powers of the Bank … are exercised in such a manner as, in the opinion of the Reserve Bank Board, will best contribute to: (a) the stability of the currency of Australia; (b) the maintenance of full employment inAustralia; and(c) the economic prosperity and welfare of the people of Australia.

Policies in pursuit of these objectives have found practical expression in a flexible, medium-term inflation target, which has formed the basis ofAustralia’s monetary policy framework since the early 1990s. The policy objective is for consumer price inflation to average between 2 and 3 per cent over time.

Australia’s financial stability policy framework includes mandates for financial stability for both APRA and the Reserve Bank. APRA is responsible for prudential supervision of financial institutions and the Bank is responsible for promoting overall financial system stability. In the event of a financial system disturbance the Bank and relevant agencies would work to mitigate the risk of systemic consequences. The Bank’s responsibility to promote financial stability does not, however, equate to a guarantee of solvency for financial institutions and the Bank does not see its balance sheet as being available to support insolvent institutions. Nevertheless, the Bank’s central position in the financial system – and its position as the ultimate provider of liquidity to the system – gives it a key role in financial crisis management, in conjunction with the other members of the Council of Financial Regulators (CFR).

The Reserve Bank holds a range of financial assets to pursue its monetary policy objectives and support an efficient and orderly payments system in Australia. The Reserve Bank’s balance sheet was $194 billion on 30 June 2017, compared with $167 billion a year earlier.

The Reserve Bank’s earnings arise from two sources: underlying earnings – comprising net interest and fee income, less operating costs – and valuation gains or losses. Net interest income arises because the Bank earns interest on almost all of its assets, albeit currently at low rates, while it pays no interest on a large portion of its liabilities, such as banknotes on issue and capital and reserves. Fees paid by authorised deposit-taking institutions associated with the Committed Liquidity Facility also make a significant contribution to underlying earnings.

Valuation gains and losses result from fluctuations in the value of the Reserve Bank’s assets in response to movements in exchange rates or in yields on securities.

In 2016/17, the Reserve Bank’s underlying earnings were $960 million, which was $263 million lower than the previous year because of lower net interest income resulting from a decline in the net interest margin. The reduced interest margin reflected, in part, the decline in short-term interest rates in Australia compared with the previous year. Underlying earnings remained at historically low levels with interest rates around the world also typically remaining low.

The Reserve Bank’s underlying earnings were offset by net valuation losses of $1 857 million, primarily from the appreciation of the Australian dollar during the year. The net valuation loss was composed of an unrealised valuation loss of $2 179 million offset by net realised gains of $322 million, largely as a result of the sale of foreign currency in the normal course of managing the portfolio of foreign reserves; these transactions had no effect on the value of the Australian dollar. The realised gains came from sales of assets on which unrealised gains had been recorded in earlier years, and therefore they acted to deplete the balance of the unrealised profits reserve, as discussed further below.

The net outcome was that the Reserve Bank recorded an accounting loss of $897 million, or 0.5 per cent of the balance sheet, in 2016/17.

Despite the accounting loss in 2016/17, earnings were still available for distribution, as the net unrealised valuation loss of $2 179 million was absorbed by the unrealised profits reserve in accordance with the Reserve Bank Act as explained above. This left earnings available for distribution amounting to $1 286 million in 2016/17, compared with $4 612 million in the previous year, reflecting both lower underlying earnings and smaller realised gains.

The Treasurer, after consulting the Board, determined that all earnings available for distribution in 2016/17, a sum of $1 286 million, would be paid as a dividend to the Commonwealth.

The RBA published a research discussion paper “The Property Ladder after the Financial Crisis: The First Step is a Stretch but Those Who Make It Are Doing OK”. Good on the RBA for looking at this important topic. But we do have some concerns about the relevance of their approach.

This paper investigates how things have changed since the GFC for those stepping onto the property ladder. Is ‘generation rent’ an important trend? Are people buying first homes taking on ‘too much’ debt? And what implications does this have for our understanding of the growing level of aggregate household debt?

They highlight the rise of those renting, and attribute this largely to rising home prices. As a piece of research, it is interesting, but as it stops in 2014, does not tell us that much about the current state of play! However, they conclude:

The results we find in this paper are very much bittersweet. On the one hand, we find that fewer people are making the transition from renters to home owners than prior to the crisis. Given research that links the rise in inequality to changes in home ownership patterns, this could have significant longer-term consequences for the distribution of wealth in Australia. On the other hand, those households that do make the transition are more financially secure than earlier cohorts. So the rise in aggregate and individual debt ratios do not appear to be associated with an increase in household financial vulnerability – at least as far as first home buyers are concerned.

We attribute much of this change to the increase in housing prices and the associated hurdle that deposit requirements represent. While saving a deposit is a stretch, it is also a sign of financial discipline that is associated with fewer subsequent difficulties. Thus, while the first step on the property ladder is more of a stretch than before the crisis, those who do make the step are, on average, better placed to pay off their loans than prior to the crisis.

A few points to note.

First, the RBA paper uses HILDA data to 2014, so it cannot take account of more recent developments in the market – since then, incomes have been compressed, mortgage rates have been cut, and home prices have risen strongly in most states, so the paper may be of academic interest, but it may not represent the current state of play. Very recently, First Time Buyers appear to be more active.

More first time buyers are getting help from parent, and their loan to income ratios are extended, according to our own research.

Also, they had to impute those who are first time buyers from the data, as HILDA does not identify them specifically. Tricky!

The past three wealth modules of the survey (2006, 2010 and 2014) have included a variable, ‘rpage’, which asks the household reference person whether they have ever owned residential property and, if so, the age at which they first acquired, or started buying, this property.

Another variable, ‘hspown’, available in the 2001 and 2002 surveys only, asks households whether they still live in their first home. This variable allows us to identify FHBs directly for these years.

We combine the information from ‘hspown’ and ‘rpage’ into the one variable identifying indebted FHBs. For 2001 and 2002 we use the ‘hspown’ variable and the ‘rpage’ variable is used thereafter.

The percentage of owner-occupier households identified as FHBs in any given year is, on average, between 1 and 2 per cent over the course of the survey, which is broadly in line with aggregate measures. This corresponds to between 50 and 100 households each year.

So a very small sample.

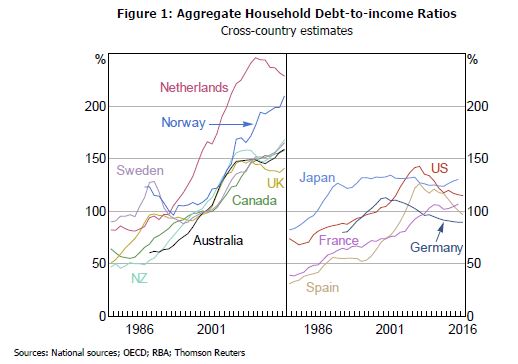

Next, the RBA cited the aggregate household Debt-to-income Ratios cross-country estimates. Rising trends are apparent in many countries.

They then proceeded to explain the drawbacks of this data set.

Notwithstanding this statistic’s frequent use, it has a number of drawbacks. First, it compares a stock of debt with a flow of income rather than, say, a stock of debt against a stock of assets or a flow of repayments against a flow of income. This mixing of concepts means that it is not clear what a reasonable benchmark for the level of debt to income might be. There are also important distributional considerations that affect what meaning can be attached to the aggregate values. At heart these issues stem from the fact that, while it is tempting to interpret higher aggregate debt-to-income ratios through a representative consumer lens, it is misleading. Of particular note is that the aggregate ratio places more weight on high-income households, which can be misleading. Higher-income households can support higher debt-to-income ratios than lower-income households. This is primarily because a smaller fraction of a higher-income household’s expenditure needs to be devoted to necessities leaving more available to spend on other things. There are also other dimensions in which borrowers may differ, such as their risk of unemployment and their ability to obtain funds in an emergency, that would affect the inherent riskiness of any given debt level.

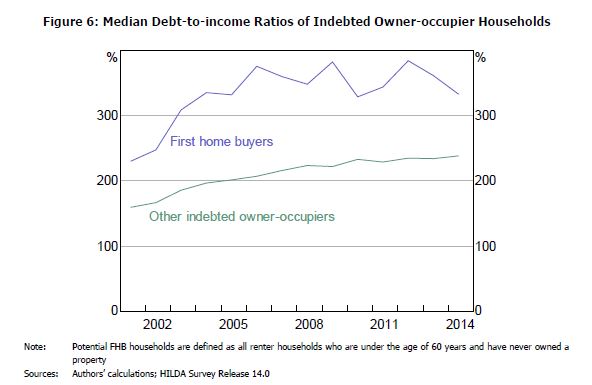

Fourth, they show that first time buyers have a higher mean debt-to-income ratio compared with other borrowers.

Turning first to the aggregated data, we can see in Figure 6 that the debt-to-income ratio of FHBs is substantially higher than that of all other indebted owner-occupiers. This reflects the fact that FHBs are at the beginning of their loan life cycle. That is, before they have had the opportunity to pay down their loan. Comparing the pre- and post-GFC periods, we see that the median FHB debt-to-income ratio was around 330 per cent in 2014, up approximately 40 per cent from the ratio of 230 per cent in 2001. FHBs are taking on more debt than in the past.

Actually, more recent data shows that Debt-to-Incomes are even more extended, with some FTB’s in Sydney at a ratio of 7x income (according to our more recent surveys).

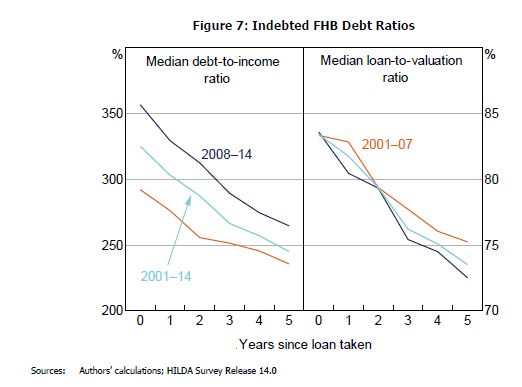

Finally, they show that “despite higher debt levels, households who became indebted FHBs post-2007 appear to be paying down their mortgages and reducing their debt-to-income ratios at the same rate, or slightly faster, than households who took on a mortgage before 2007”.

In the year after taking out a loan, the reduction in the debt-to-income ratio for FHBs in the post-2007 period was around 8 per cent, compared to 5 per cent for the pre-2007 cohort. After three years, the debt-to-income ratio for FHBs in the pre- and post-2007 periods has decreased by 14 and 18 per cent, respectively. Given that these rates of amortisation are significantly higher than those associated with required repayments or interest rate changes over this period, it seems that these are voluntary choices rather than the consequence of changes to required repayment schedules. The median loan-to-valuation ratio of FHBs in the post-financial crisis period also decreases by more than for the previous cohort, although this is likely due to the rise in housing prices increasing the denominator of this ratio over time.

So, while there are some general conclusions, we are not sure the work really adds much to the current debate on housing affordability, housing debt, and the current stresses which households, especially first time buyers are experiencing.

RBA Deputy Governor Guy Debelle spoke about Interest Rate Benchmarks at FINSA today. He made three points:

First, the longevity of LIBOR cannot be assumed, so any contracts that reference LIBOR will need to be reviewed.

Second, actions to ensure the longevity of BBSW are well advanced. While these changes entail some costs, the cost of not doing so would be considerably larger.

Third, consider whether risk-free benchmarks are more appropriate rates for financial contracts than credit-based benchmarks such as LIBOR and BBSW.

Today I am going to talk again about interest rate benchmarks, as recently there have been some important developments internationally and in Australia. These benchmarks are at the heart of the plumbing of the financial system. They are widely referenced in financial contracts. Corporate borrowing rates are often priced as a spread to an interest rate benchmark. Many derivative contracts are based on them, as are most asset-backed securities. In light of the issues around the London Inter-Bank Offered Rate (LIBOR) and other benchmarks that have arisen over the past decade, there has been an ongoing global reform effort to improve the functioning of interest rate benchmarks.

I will focus on the recent announcement by the UK Financial Conduct Authority (FCA) on the future of LIBOR, and the implications of this for Australian financial markets. I will then summarise the current state of play in Australia, particularly for the major interest rate benchmark, the bank bill swap rate (BBSW). Our aim is to ensure that BBSW remains a robust benchmark for the long term. I will also discuss the important role for ‘risk-free’ interest rates as an alternative to credit-based benchmarks such as BBSW and LIBOR.

The Future of LIBOR and the Implications for Australia

LIBOR is the key interest rate benchmark for several major currencies, including the US dollar and British pound. Just over a month ago, Andrew Bailey, who heads the FCA which regulates LIBOR, raised some serious questions about the sustainability of LIBOR. The key problem he identified is that there are not enough transactions in the short-term wholesale funding market for banks to anchor the benchmark. The banks that make the submissions used to calculate LIBOR are uncomfortable about continuing to do this, as they have to rely mainly on their ‘expert judgment’ in determining where LIBOR should be rather than on actual transactions. To prevent LIBOR from abruptly ceasing to exist, the FCA has received assurances from the current banks on the LIBOR panel that they will continue to submit their estimates to sustain LIBOR until the end of 2021. But beyond that point, there is no guarantee that LIBOR will continue to exist. The FCA will not compel banks to provide submissions and the panel banks may not voluntarily continue to do so.

This four year notice period should give market participants enough time to transition away from LIBOR, but the process will not be easy. Market participants that use LIBOR, including those in Australia, need to work on transitioning their contracts to alternative reference rates. This is a significant issue, since LIBOR is referenced in around US$350 trillion worth of contracts globally. While a large share of these contracts have short durations, often three months or less, a very sizeable share of current contracts extend beyond 2021, with some lasting as long as 100 years.

This is also an issue in Australia, where we estimate that financial institutions have around $5 trillion in contracts referencing LIBOR. Finding a replacement for LIBOR is not straightforward. Regulators around the world have been working closely with the industry to identify alternative risk-free rates that can be used instead of LIBOR, and to strengthen the fall-back provisions that would apply in contracts if LIBOR was to be discontinued. The transition will involve a substantial amount of work for users of LIBOR, both to amend contracts and update systems.

Ensuring BBSW Remains a Robust Benchmark

The equivalent interest rate benchmark for the Australian dollar is BBSW, and the Council of Financial Regulators (CFR) is working closely with industry to ensure that it remains a robust financial benchmark. BBSW is currently calculated from executable bids and offers for bills issued by the major banks. A major concern over recent years has been the low trading volumes at the time of day that BBSW is measured (around 10 am). There are two key steps that are being taken to support BBSW: first, the BBSW methodology is being strengthened to enable the benchmark to be calculated directly from a wider set of market transactions; and second, a new regulatory framework for financial benchmarks is being introduced.

The work on strengthening the BBSW methodology is progressing well. The ASX, the Administrator of BBSW, has been working closely with market participants and the regulators on finalising the details of the new methodology. This will involve calculating BBSW as the volume weighted average price (VWAP) of bank bill transactions. It will cover a wider range of institutions during a longer trading window. The ASX has also been consulting market participants on a new set of trading guidelines for BBSW, and this process has the strong support of the CFR. The new arrangements will not only anchor BBSW to a larger set of transactions, but will improve the infrastructure in the bank bill market, encouraging more electronic trading and straight-through processing of transactions. The critical difference between BBSW and LIBOR is that there are enough transactions in the local bank bill market each day relative to the size of our financial system to calculate a robust benchmark.

For the new BBSW methodology to be implemented successfully, the institutions that participate in the bank bill market will need to start trading bills at outright yields rather than the current practice of agreeing to the transaction at the yet-to-be-determined BBSW rate. This change of behaviour needs to occur at the banks that issue the bank bills, as well as those that buy them including the investment funds and state treasury corporations. The RBA is also playing its part. Market participants have asked us to move our open market operations to an earlier time to support liquidity in the bank bill market during the trading window, and we have agreed to do this.

While we all have to make some changes to systems and practices to support the new methodology, the investment in a more robust BBSW will be well worth it. The alternative of rewriting a very large number of contracts and re-engineering systems should BBSW cease to exist would be considerably more painful.

The new regulatory framework for financial benchmarks that the government is in the process of introducing should provide market participants with more certainty. Treasury recently completed a consultation on draft legislation that sets out how financial benchmarks will be regulated, and the bill has just been introduced into Parliament. In addition, ASIC recently released more detail about how the regulatory regime would be implemented. This should help to address the uncertainty that financial institutions participating in the BBSW rate setting process have been facing. It should also support the continued use of BBSW in the European Union, where new regulations will soon come into force that require benchmarks used in the EU to be subject to a robust regulatory framework.

Risk-free Rates as Alternative Benchmarks

While the new VWAP methodology will help ensure that BBSW remains a robust benchmark, it is important for market participants to ask whether BBSW is the most appropriate benchmark for the financial contract.

For some financial products, it can make sense to reference a risk-free rate instead of a credit-based reference rate. For instance, floating rate notes (FRNs) issued by governments, non-financial corporations and securitisation trusts, which are currently priced at a spread to BBSW, could instead tie their coupon payments to the cash rate.

However, for other products, it makes sense to continue referencing a credit-based benchmark that measures banks’ short-term wholesale funding costs. This is particularly the case for products issued by banks, such as FRNs and corporate loans. The counterparties to these products would still need derivatives that reference BBSW so that they can hedge their interest rate exposures.

It is also prudent for users of any benchmark to have planned for a scenario where the benchmark no longer exists. The general approach that is being taken internationally to address the risk of benchmarks such as LIBOR being discontinued, is to develop risk-free benchmark rates. A number of jurisdictions including the UK and the US have recently announced their preferred risk-free rates.

One issue yet to be resolved is that most of these rates are overnight rates. A term market for these products is yet to be developed, although one could expect that to occur through time. Another complication is that the risk-free rates are not equivalent across jurisdictions. Some reference an unsecured rate (including Australia and the UK) while others reference a secured rate like the repo rate in the US.

As the RBA’s operational target for monetary policy and the reference rate for OIS (overnight index swap) and other financial contracts, the cash rate is the risk-free interest rate benchmark for the Australian dollar. The RBA measures the cash rate directly from transactions in the interbank overnight cash market, and we have ensured that our methodology is in line with the IOSCO benchmark principles. However, the cash rate is not a perfect substitute for BBSW, as it is an overnight rate rather than a term rate, and doesn’t incorporate a significant bank credit risk premium.

A focus on household debt, risks of lower rates, and a discussion about why individual lenders may be myopic about risk. The long term trajectory of rates will be higher. Perhaps.

For some time, the Board has been seeking to balance the benefits of stimulatory monetary policy with the medium-term risks associated with high and rising levels of household debt.

The current low level of interest rates is helping the Australian economy. It is supporting employment growth and a return of inflation to around its average level. Encouragingly, growth in the number of Australians with jobs has picked up over recent months and the unemployment rate has come down a bit. The investment outlook has also brightened. Inflation has troughed and it is likely to increase gradually over the next couple of years. These are positive developments. Even so, it will be some time before we are at what could be considered full employment in Australia and before underlying inflation is at the mid-point of the medium-term target range. This means that stimulatory monetary policy continues to be appropriate.

The Board has been conscious that attempting to achieve faster progress on unemployment and inflation through yet lower interest rates would have added to the risks in household balance sheets. Lower rates would have encouraged faster growth in household borrowing and added to the medium-term risks facing the economy. Our judgement has been that it was not in the public interest to encourage an already highly indebted household sector to borrow even more. More borrowing might have helped today, but it could come at a future cost.

So the Board has been prepared to be patient and has not sought to overly engineer or fine-tune things. In our view, the balance we have struck is appropriate and it is likely that the economy will pick up from here as the drag from declining mining investment comes to an end. Our central scenario is for growth of around 3 per cent over the next couple of years and for the unemployment rate to move lower gradually.

In striking the appropriate balance in our policy setting, we have paid close attention to trends in household borrowing, given the already high levels of debt. Over the past four years, household borrowing has increased at an average rate of 6½ per cent, while household income has increased at an average rate of just 3½ per cent. Given this, the RBA has worked closely with APRA to ensure that lending practices remain sound. Rightly, APRA has had a strong focus on loan serviceability calculations. In some cases, loans were being made where the borrower had only the slimmest of spare income. APRA has also introduced restrictions on growth of investor loans and restrictions on interest-only lending. This has been the right thing to do.

One might ask why lenders themselves did not do more to constrain their activities in these areas, given the earlier trends were adding to risk in the overall system. When everything is going well, it appears that any single institution has difficulty pulling back. Each worries about their competitive position and about the market reaction. Individual institutions are also more likely to focus on their own risks, rather than the risks to the system as a whole. This means that supervisory measures can be useful in helping the whole system pull back. Ideally, such measures would not be needed, with instead the appropriate level of restraint coming out of lenders’ holistic risk assessments. But when this does not occur, supervisory measures can play a constructive role. Most lenders are now operating comfortably within the new restrictions and these measures are not unduly restraining the supply of overall housing credit.

One of the factors that has a bearing on current discussions of household debt is the slow growth in household incomes. Over the past four years, nominal average hourly earnings have grown at the slowest rate in many decades. This means that borrowers haven’t been able to rely on rising incomes to reduce the real value of the debt repayments in the way they used to; debt-service ratios will stay higher for longer. This is something that both lenders and borrowers need to take into account.

The slow growth in wages is a common experience across most advanced economies today. It lies behind the sense of dissatisfaction that is being felt in many communities. The reasons for this slow growth in wages are complex. Part of the explanation is a perception of greater competition from both globalisation and technology. An increased sense of uncertainty among workers is also likely to be playing a role, as is a change in the bargaining environment.

The slow growth in wages is contributing to low inflation outcomes globally. My expectation is that this is going to continue for a while yet, given that the structural factors at work are likely to persist. But I am optimistic enough that I don’t see it as a permanent state of affairs. It is likely that, as our economy strengthens and the demand for labour picks up, growth in wages will pick up too. The laws of supply and demand still work. Even at the moment, we see some evidence through our liaison program that in those pockets where the demand for labour is strong, wages are increasing a bit more quickly than they have for some time. The Reserve Bank’s central scenario is that, over time, this will become a more general story.

On another matter, over the past few months there has been quite a lot of interest in the regular special papers considered by the Board. This followed the release of the minutes of the July meeting, which recorded that the Board had held a discussion of the neutral interest rate (that is, the rate at which monetary policy is neither expansionary nor contractionary).

The main conclusion from that discussion was that, in future, it was likely that the average level of the cash rate would be lower than it was before the financial crisis. This reflects slower trend growth in the economy and a shift in the balance between savings and investment. When people want to save more and invest less, the return on the risk-free asset is lower. These same forces are at work around the world, so that the average level of interest rates globally is likely to be lower than before the financial crisis.

A second conclusion from our discussion was that the cash rate is around 2 percentage points below our current estimate of the neutral rate. As we make further progress on both unemployment and inflation, we could expect the cash rate to move towards this neutral rate over time.

It is worth repeating that the Board’s consideration of these issues carries no particular message about the short-term outlook for monetary policy. The discussion was part of our regular in-depth reviews of important issues. As is appropriate, these discussions are reflected in our minutes. I hope that you see Australia’s central bank as transparent, analytical, rational and independent. We seek to look at issues in detail and from different angles and to explain our thinking to the public. While not everybody agrees with our decisions, we do our best to explain those decisions and the framework we use to make them.

Household indebtedness is high and, against a backdrop of low interest rates and weak income growth, debt levels relative to income have continued to edge higher. Steps taken by regulators in the past few years to strengthen the resilience of balance sheets, including limiting the pace of growth of investor lending, discouraging loans with high loan-to-valuation ratios (LVRs) and strengthening serviceability metrics, have seen the growth in riskier types of lending moderate. The most recent focus has been on limiting interest-only lending, and banks have responded by further reducing lending with high LVRs for interest-only loans, increasing interest rates for some types of mortgages and significantly reducing interest-only lending.