A research discussion paper from the RBA – “How Australians Pay: Evidence from the 2016 Consumer Payments Survey” – provides further evidence of the migration to electronic and digital payment mechanisms, but also underscores that cash remains a critical payment mechanism for many, especially in the older age groups. Given the fast adoption of mobile payments, the 2016 data will already be out of date!

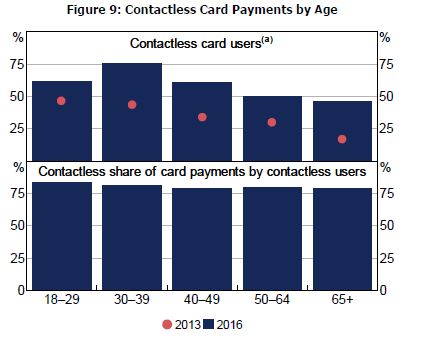

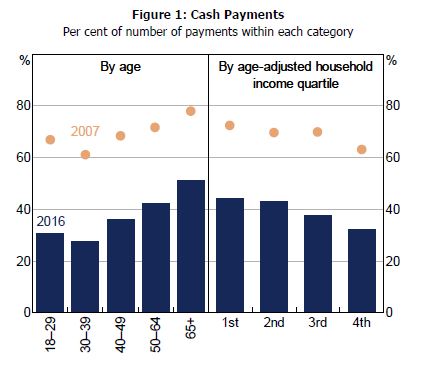

Using data recorded information on around 17 000 day-to-day payments made by over 1 500 participants during a week, the report shows that Australian consumers continued to switch from paper-based ways of making payments such as cash and cheques, towards digital payment methods (particularly debit and credit cards). Cards were the most frequently used means of payment in the 2016 survey, overtaking cash for the first time. Contactless ‘tap and go’ cards are an increasingly popular way of making payments, displacing cash for many lower-value transactions.

Despite these trends, cash still accounts for a material share of consumer payments and is intensively used by some segments of the population.

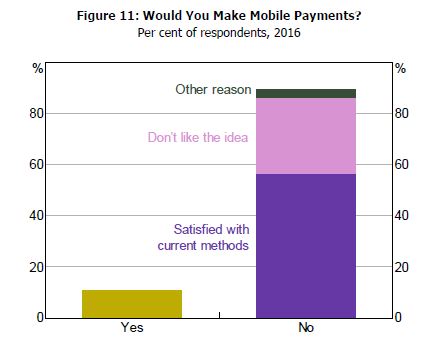

Payments using a mobile phone at a card terminal are a relatively new feature of the payments system and this technology was not widely used at the time of the survey. However, consumers are increasingly using their mobile phones to make online and person-to-person payments. Similarly, consumers are using automatic payments, such as direct debits, more frequently.

Speaking at CEDA today, RBA Deputy Governor Guy Debelle seemed to be intent on hosing down expectations of interest rate rises (in stark contrast to the RBA minutes earlier this week). He suggests that even if the Fed continues to lift their benchmark rate, it does not automatically follow we will see a rise here in Australia.

The neutral interest rate provides a benchmark for assessing the current stance of monetary policy. If the real policy rate – that is, the cash rate less inflation expectations – is below the neutral rate, then monetary policy is exerting an expansionary influence on the economy. If the real policy rate is above the neutral rate, then monetary policy is exerting a contractionary influence on the economy. The neutral rate is often associated with the turn of the 20th century Swedish economist Knut Wicksell and was picked up by Keynes. The previous Governor Glenn Stevens discussed the neutral rate in the Australian context more than a decade ago.

There was a discussion of the neutral rate at the most recent Board meeting, as detailed in the minutes of the meeting released earlier this week. No significance should be read into the fact the neutral rate was discussed at this particular meeting. Most meetings, the Board allocates some time to discussing a policy-relevant issue in more detail, and on this occasion it was the neutral rate.

The neutral interest rate aligns the amount of saving and investment in the economy at a level that is consistent with full employment and stable inflation. That is, the neutral rate is where the policy rate would settle down in the medium term when the goals of monetary policy are being achieved. Accordingly, most explanations of the neutral interest rate start with the factors that influence saving or investment. Developments that increase saving will tend to lower the neutral interest rate; developments that increase investment will tend to raise the neutral interest rate.

There are three main factors that, in my view, affect the neutral rate in Australia:

the economy’s potential growth rate

the degree of risk aversion

international factors.

One of the major determinants of the neutral interest rate is the economy’s potential growth rate. In an economy with a high potential growth rate, because it has strong productivity or population growth, the expectation of increased future demand provides a strong incentive for firms to invest and the prospect of higher real incomes reduces the incentives of households to save. Both of these forces will tend to raise the neutral interest rate. The economy’s potential growth rate tends to evolve quite slowly, and hence we should expect the neutral interest rate also to change only very gradually as a result of this influence.

Another influence on the neutral rate is the risk appetite of firms and households and the way risk has been priced into market interest rates. This influence can move rapidly. When risk aversion rises, firms require more compensation to make long-term investments with an uncertain return. At the same time, the increased risk aversion will cause households to save more. This lowers the neutral interest rate, as any given level of the policy rate is less expansionary because of the increased risk aversion. If there is an increase in risk aversion, it is also likely that there will be a widening in the spreads between the policy rate and market interest rates that determine the behaviour of households and firms. A given market interest rate will correspond to a lower policy rate if spreads widen. This will further lower the neutral interest rate.

Finally, in an open economy, where capital can move reasonably freely across borders, global interest rates will also influence domestic interest rates. This means that trends in overseas productivity growth, demographics and risk appetite will affect the neutral interest rate in Australia.

So how do we calculate the neutral interest rate? It is not directly observable. There are a number of different ways of estimating it from the behaviour of market interest rates and other economic variables. The shaded area in Graph 4 shows a range of plausible estimates for the neutral real interest rate obtained using a number of different approaches. As you can see, there is a reasonable amount of uncertainty about the exact level of the neutral rate.

Graph 4 also shows the (ex post) real cash rate calculated by deducting the trimmed mean inflation rate from the cash rate. When the real cash rate is above the neutral rate, the monetary policy stance is contractionary. When it is below, the stance is expansionary. As you look at the graph, you can see that this lines up with most assessments of the stance of monetary policy over the past 25 years. It suggests that monetary policy was clearly expansionary in the early 2000s, in 2008 and for the past five years or so.

Graph 4

The estimates of the neutral rate suggest that it was fairly stable for much of the 1990s up until 2007. In Glenn Stevens’ speech that I mentioned earlier, he noted that the neutral real cash rate at the time (2004) was probably somewhere between 2½ per cent and 3¾ per cent. This is consistent with the estimates shown here.

The graph shows a clear step down in all the estimates of the neutral rate in 2007/08 and that it has probably drifted lower since. It suggests that Australia’s neutral interest rate is currently around 150 basis points lower now than in 2007. This decline can largely be accounted for by a slowdown in potential growth and an increase in risk aversion.

The Bank estimates that Australia’s long-run potential growth rate has declined by around ½ percentage point from the mid 1990s. Part of the decline reflects slower labour force growth. The rest of the decline reflects a slowdown in trend productivity growth, which is common to many advanced economies. This slowdown in potential growth has probably translated about one-for-one into a decline in the neutral rate, though the decline has been gradual.

The sharper decline in the neutral rate in 2007/08 can be most easily related to the sharp increase in risk aversion with the onset of the financial crisis. This increased risk aversion probably accounts for most of the large fall in estimated neutral interest rates in Australia and abroad that occurred at this time. This heightened risk aversion has also contributed to an increase in spreads between the cash rate and market interest rates, which should have a roughly one-for-one effect on the neutral interest rate.

At the same time, increased risk aversion means that companies are investing less than one would expect given financing conditions and the economic outlook. Households are less willing than in the past to borrow in order to fund consumption. Although these effects are hard to quantify, they would both lower the neutral interest rate.

To return to a global perspective, Graph 5 compares the average estimate of the neutral interest rate for Australia to a range of international estimates. On average, the neutral interest rate estimates for Australia are similar to those of the United Kingdom and Canada, but higher than those for the United States and the euro area.

As is the case for Australia, estimates of neutral interest rates in other developed economies were fairly stable until around the mid 2000s and have fallen since then. The decline in the neutral rate was particularly sharp in 2007/08 and, again, most likely reflects the increase in risk aversion at the onset of the financial crisis.

Graph 5

Because trends in determinants of the neutral interest rate, such as productivity growth and risk appetite, tend to be highly correlated across advanced economies, it is hard to distinguish between international influences and domestic influences. But it is very likely that global factors have contributed to a decline in Australia’s neutral policy rate.

So in short, the policy rate in Australia is low because the neutral rate is lower than it used to be as a result of both international and domestic developments. This means that the current (nominal) cash rate setting of 1½ per cent today is not as expansionary as a cash rate of 1½ per cent would have been in the 1990s or the first half of the 2000s.

Looking ahead, the neutral policy rate both here in Australia as well as in other advanced economies is likely to remain lower than it was in the past. It is plausible that the degree of risk aversion might abate in time, which would see the neutral rate rise from its current low level. But other developments contributing to the lower neutral rates, particularly lower potential growth rates, could be more permanent.

The chart below from JP Morgan underlines the dramatic shift seen in rate hike expectations following the release.

Source: JP Morgan

Using Australian overnight index swaps (OIS), it shows that markets are now close to fully priced for a rate hike by the middle of next year.

Quite a shift, helping to explain the surge in the Australian dollar and bond yields over the past 24 hours.

The upbeat tone of the minutes, in stark contrast to the July monetary policy statement released two weeks earlier, along with a discussion among board members as to the neutral policy level for interest rates in Australia, saw some jump to the conclusion that the RBA was priming markets for an increase in interest rates.

Looking at the scale of the market reaction, it’s clear many adopted just such a view.

While some think it’s a game-changer, Sally Auld, chief economist and head of Australia and New Zealand fixed income and FX strategy JP Morgan, does not share that view, suggesting that markets have jumped the gun in pricing in a hawkish shift from the RBA.

Here’s a snippet from a report she released today outlining four reasons why, in her opinion, markets got a little ahead of themselves:

First, it should be remembered that the RBA delivered a strong refute to expectations that it was shifting in a more hawkish direction just two weeks ago. It is not clear that enough has changed for the RBA to warrant a shift in emphasis so soon.

Second, even assuming that the RBA wanted to signal something different from the July Statement, was a paragraph on the neutral rate estimate in the minutes the way to execute this change in message? We doubt it.

Third, we should note that the agenda for RBA Board meetings often includes items for discussion that are not directly related to the assessment of economic conditions in the past month. This is particularly the case for the RBA Board, which unlike other central banks, is not comprised of professional economists. Rather, the majority of RBA Board members are usually drawn from business, and hence there is sometimes a need to “educate” Board members on theoretical topics that are related to economics and monetary policy. In this context, the discussion around the neutral rate doesn’t look so unusual.

Fourth, the conclusion that policy is already accommodative is not “new news”. The RBA has made such an assertion every month in the minutes since May this year.

A pretty solid critique of the market’s interpretation if there ever was one.

While the tone of the minutes was certainly more upbeat on the outlook for the economy and labour market conditions than the abbreviated policy statement, outside of the those areas and the discussion on neutral policy settings, there really wasn’t all that much new to garner from the minutes, including that current settings are “clearly expansionary”.

Rates are, after all, at the lowest level on record, even with the neutral policy setting now far lower than what was the case in the past.

Looking ahead, Auld says we’ll find out soon enough as to whether or not the RBA intended to deliver a hawkish message.

“A test of our view will come with speeches from the deputy governor and governor in coming days,” she says.

“While it is typically not the RBA’s ‘style’ to micro-manage unwanted market reactions — the AUD is not yet meaningfully overvalued and the RBA might welcome renewed talk of hikes as another way to jawbone an overextended housing market — we don’t expect either speech to validate current market pricing and anticipate that RBA officials will push back hard on the perception that the central bank is on the cusp of starting policy normalisation.”

The Reserve Bank has scared heavily-mortgaged households and pushed the Australian dollar to its highest level in two years by appearing to signal interest rate hikes.

In the minutes of its July 4 meeting, released on Tuesday, Australia’s central bank said it now estimates the “neutral” official cash rate to be 3.5 per cent – a full 200 basis points above where the cash rate is now.

That effectively means the RBA thinks it can substantially increase the cash rate, currently at a record-low 1.5 per cent, without curbing economic growth. Banks can be expected to eagerly pass on any rate rises to borrowers.

Many RBA watchers interpreted the inclusion of the estimate as a strong hint the central bank is now ‘hawkish’ (inclined to lift rates), as it is highly unusual for it to discuss the “neutral” rate at a policy meeting.

Economist Stephen Koukoulas described the language as “aggressive”.

“RBA has just effectively tightened monetary policy: the 3.5 per cent neutral rate reference will see AUD go to the moon and [interest rate] hikes priced in,” he wrote on Twitter.

The Australian dollar jumped up higher after the minutes were released at 11:30am on Tuesday – a sign that investors interpreted the statements to flag rate rises. The Aussie strengthened against the US dollar from around 78 US cents to over 79 US cents by late afternoon.

James Glynn, senior economics reporter at the Wall Street Journal, described the minutes as “hawkish”.

“Talking openly about a 3.5 per cent neutral rate will allow RBA to assist APRA in doing a job on the housing market.”

The official cash rate has been at a record-low 1.5 per cent since August last year, as the central bank tries to help the Australian economy recover from the aftereffects of the global financial crisis 10 years ago.

This record low rate, followed more or less by the commercial banks, has helped jobs – but also ballooned house prices and household debt, especially in Sydney and Melbourne.

Another line in the RBA minutes suggested it knew full well what it was doing by publishing such a market-sensitive number.

“The implications of statements by central banks in the major economies for the future path of monetary policy had been a focus for financial market participants more recently,” the RBA board said.

However, there were sceptics.

Sally Auld, economist at JP Morgan, said the bank’s discussion of the neutral rate was unlikely to be “interpreted as some sort of signal”.

“We don’t think this is the case – after all, the discussion is sympathetic with the RBA’s consistent description of policy settings over the past year as accommodative,” Ms Auld wrote in a research note.

The RBA did note there was “significant uncertainty” around estimates of the neutral rate.

Other complicating factors were that the minutes explicitly said that “holding the accommodative stance of monetary policy unchanged” would be “consistent with sustainable growth in the economy and achieving the inflation target over time”.

This is where the RBA usually heralds interest rate rises.

Another reason to doubt the RBA’s intentions was that it said “developments in the labour and housing markets continued to warrant careful monitoring”.

All eyes will be on the release of the latest labour market figures on Thursday.

The spike in the Australian dollar after the release of the minutes, and the steady appreciation against the US dollar in recent days, are likely to worry the central bank.

This is because the RBA said in the minutes that an “appreciating exchange rate would complicate” Australia’s economic growth.

A number of interesting comments were contained in the RBA minutes for July, released today. Bank margins are increasing, and the next move in the cash rate is more likely up, not down (though complicated by exchange rates).

There was a decline in dwelling investment, a rise in household spending in April, after a fall in the first quarter, and a rotation from investment lending to owner occupied lending. The underemployment rate, which measures the number of part-time workers wanting to work more hours, had remained elevated.

“Auction clearance rates in Sydney and Melbourne had softened recently, suggesting that conditions in these markets had eased somewhat. Housing prices in Perth and apartment prices in Brisbane had fallen further. Members noted that there had been several periods in the preceding decade in which housing prices had fallen, or growth had slowed significantly, in different parts of the country”.

“Members discussed trends in the composition and cost of Australian banks’ funding. Deposits, which are generally a relatively low-cost form of funding, had increased as a share of funding over recent years, to around 60 per cent, while the share of debt funding, particularly at short maturities, had declined. The cost of both types of funding had declined further since late 2016. Members noted that, over the same period, banks’ lending rates had increased slightly, driven by increases in housing lending rates for investors and on interest-only loans. As a result, the implied spread between the estimated average outstanding lending and funding rates for banks was estimated to have increased slightly”.

“Members discussed the Bank’s work estimating the neutral real interest rate for Australia. The various estimates suggested that the rate had been broadly stable until around 2007, but had since fallen by around 150 basis points to around 1 per cent. This equated to a neutral nominal cash rate of around 3½ per cent, given that medium-term inflation expectations were well anchored around 2½ per cent, although there is significant uncertainty around this estimate. Members noted that some of this decline could be attributed to lower potential output growth, but the increase in risk aversion around the time of the global financial crisis was likely to have been a more important factor, given that the bulk of the decline in the estimated neutral real interest rate had occurred around that time. Estimates of neutral real interest rates for other economies had shown a similar decline. All estimates of the neutral real interest rate for Australia suggested that monetary policy had been clearly expansionary for the preceding five years or so. It was also noted that a reduction in risk aversion and/or an increase in the potential growth rate could see the neutral real interest rate rise again”.

“The pipeline of residential construction was expected to support dwelling investment over the forecast period. The economic outlook continued to be supported by the low level of interest rates. The depreciation of the exchange rate since 2013 had also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment“.

Given the recent strength of the dollar, this could put the cat among the pigeons!

The Reserve Bank may hold rates for as long as a year, but mortgage borrowers could be punished anyway by rising house prices and gouging by the banks.

Australia’s central bank held the official cash rate at 1.5 per cent for the tenth time on Tuesday. It hasn’t moved since a 25 basis point cut in August 2016.

But this hasn’t stopped the banks. They have refused to pass on the full benefit of the RBA’s record-low rates in order to offset costs and prop up profits.

Analysis by The New Daily of official data published on Tuesday showed that the gap between the RBA rate and the standard rate banks quote to mortgage borrowers is around the widest in 20 years.

RMIT economist Dr Ashton De Silva, an expert on the housing market, said it was “conceivable” that banks could widen this gap even further in coming months in response to rumblings in the global economy.

He pointed to the impact of Brexit and the Federal Reserve pushing up rates in the US as factors that could force Australian banks to pay more to borrow overseas and pass on the costs to owner-occupiers.

This spread between the official rate – which the RBA insists is still the “main driver” of bank funding costs – and the Standard Variable Rate banks quote to prospective customers is sitting perilously close to four percentage points, the biggest margin since 1994.

The SVR is higher than what most customers actually pay, but the gap is similar for discounted rates.

The good news for borrowers is that the RBA probably won’t hike rates for a few months more, according to the market.

The futures market is tipping rates won’t rise until next year, and even then, not by much. The ‘yield curve’ in that market shows rates are expected to reach about 1.75 per cent by November 2018.

But that’s not much relief if the banks push up rates in the interim in response to rising borrowing costs.

Martin North at Digital Finance Analytics said lenders were likely to continue penalising investors and interest-only borrowers, while leaving owner-occupier rates roughly where they are.

“Last year there was a massive race to the bottom in terms of discounts to try to gain volume and share. Many banks dented their margins in the process,” Mr North told The New Daily.

“They’ve now got the perfect cover, thanks to APRA’s regulatory intervention, and so I’d expected to see mortgage rates continuing to grind higher, particularly for investors and anyone on interest-only.”

The RBA’s cash rate may be the “main driver” of bank funding costs, but it’s not the only driver. Australian banks also borrow heavily in overseas money markets such as London and New York, where central banks are eyeing rate hikes, and from term deposits in Australia.

Owner-occupier mortgage rates are still lower than they were in 2011, when the RBA began cutting. Since then, the official cash rate has fallen by almost 70 per cent, from 4.75 to 1.5 per cent.

The problem for borrowers is that rising house prices (fuelled in part by low rates) are negating the benefits.

Rate cuts are supposed to give households more disposable income by reducing their mortgage repayments.

But interest is only half a mortgage. The rest is ‘principal’, which is being pushed up by higher property values, especially in Sydney and Melbourne.

This means the total amount of money we’re repaying to banks is high and staying high, despite what the RBA has been doing.

The Bank for International Settlements has estimated that the average Australian household spent 15.3 per cent of income on interest and principal repayments (a measure known as the ‘debt service ratio’) over the last three months of 2016, its latest estimate.

This is back to levels last seen in 2013, which means the benefits of low rates must be getting swamped by house price rises.

Australia’s debt service ratio is now third behind the Netherlands (17.4pc) and Denmark (15.9pc), putting us above a comparable economy like Canada (12.3pc) and well above bigger economies such as the USA (8.2pc) and United Kingdom (9.7pc).

The RBA held the cash rate again. They are it appears firmly on hold for the next few months, with little indication of if and when that might change.

Once again housing, and household debt got a run, but there was little which was new.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The broad-based pick-up in the global economy is continuing. Labour markets have tightened further in many countries and forecasts for global growth have been revised up since last year. Above-trend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. The rise in commodity prices over the past year has boosted Australia’s national income.

Headline inflation rates, having moved higher over the past year, have declined recently in response to lower oil prices. Wage growth remains subdued in most countries, as does core inflation. Further increases in US interest rates are expected and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively and volatility has been low.

As expected, GDP growth slowed in the March quarter, partly reflecting temporary factors. The Australian economy is expected to strengthen gradually, with the transition to lower levels of mining investment following the mining investment boom almost complete. Business conditions have improved and capacity utilisation has increased. Business investment has picked up in those parts of the country not directly affected by the decline in mining investment. At the same time, consumption growth remains subdued, reflecting slow growth in real wages and high levels of household debt.

Indicators of the labour market remain mixed. Employment growth has been stronger over recent months. The various forward-looking indicators point to continued growth in employment over the period ahead. Wage growth remains low, however, and this is likely to continue for a while yet. Inflation is expected to increase gradually as the economy strengthens.

The outlook continues to be supported by the low level of interest rates. The depreciation of the exchange rate since 2013 has also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment.

Conditions in the housing market vary considerably around the country. Housing prices have been rising briskly in some markets, although there are some signs that these conditions are starting to ease. In some other markets, prices are declining. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases are the slowest for two decades. Growth in housing debt has outpaced the slow growth in household incomes. The recent supervisory measures should help address the risks associated with high and rising levels of household indebtedness. Lenders have also announced increases in mortgage rates for investor and interest-only loans.

Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

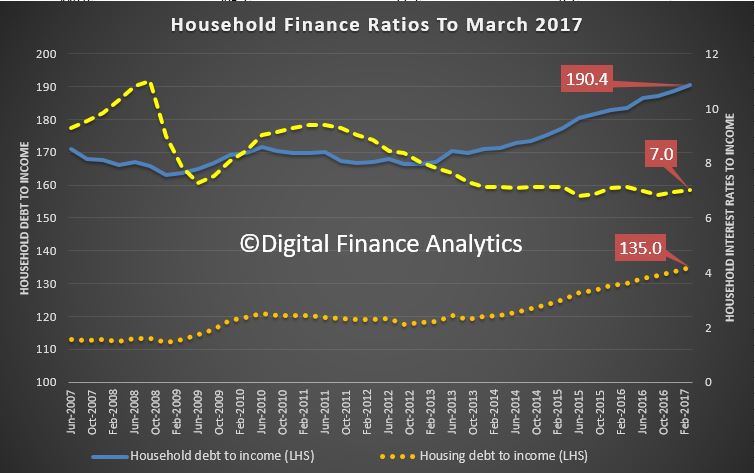

The ratio of household debt to annualised household disposable income , rose to 190.4, the ratio of housing debt to annualised household disposable income rose to 135, and worryingly the ratio of interest payments on housing debt to quarterly household disposable income has risen to 7.0, thanks to the out of cycle rate hikes and flat or falling incomes. Of course failing cash rates helped households out, but the lending standards were not adjusted until too late.

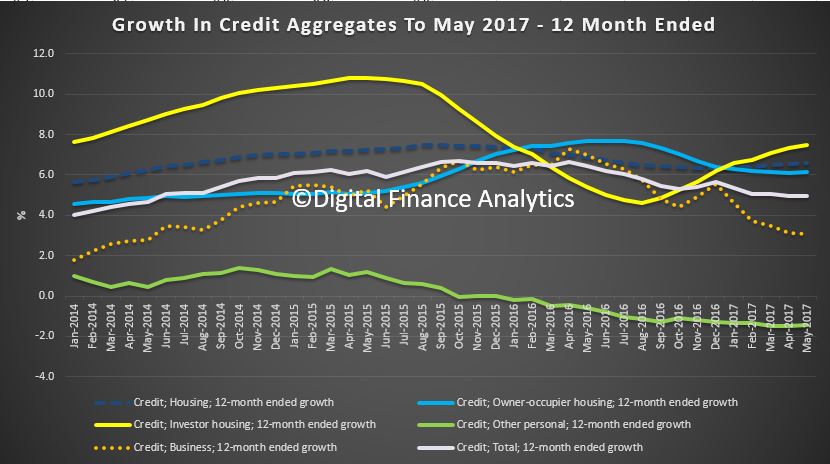

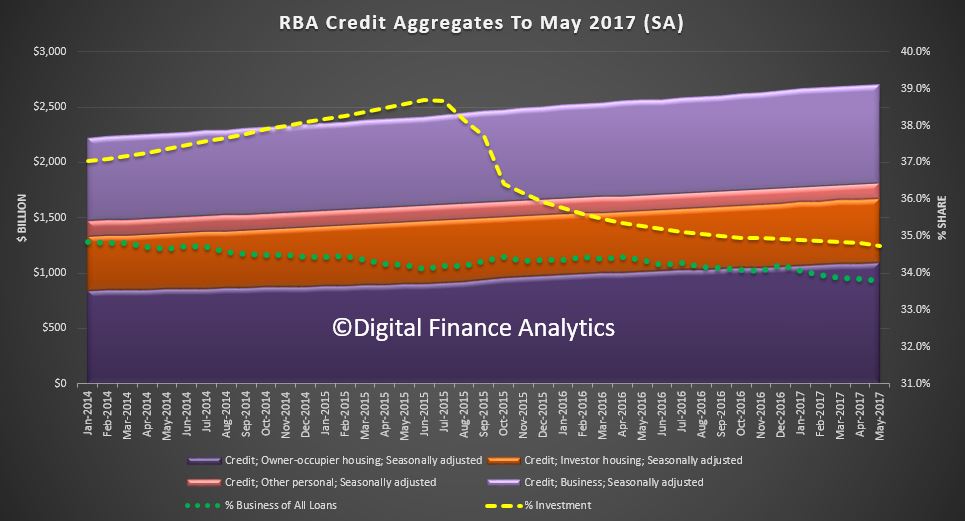

The adjusted 12 month growth trends tells it all. Investment loans still running ahead of owner occupied lending, business credit slowing and other personal lending falling. Total credit grew 5% in the year (compared with 6.4% last year), Housing credit grew at 6.6%, compared with 6.9% a year ago, and business credit grew at 3.1% compared with 7% a year ago. These are worrying trends, and makes future economic growth less certain. However, bank profits will be bolstered thanks to ongoing mortgage growth, and the benefit of the recent mortgage repricing, under the alibi of regulatory pressure. Just remember households have to repay this debt at some point, and interest rates will grind higher. Risks continue to rise.

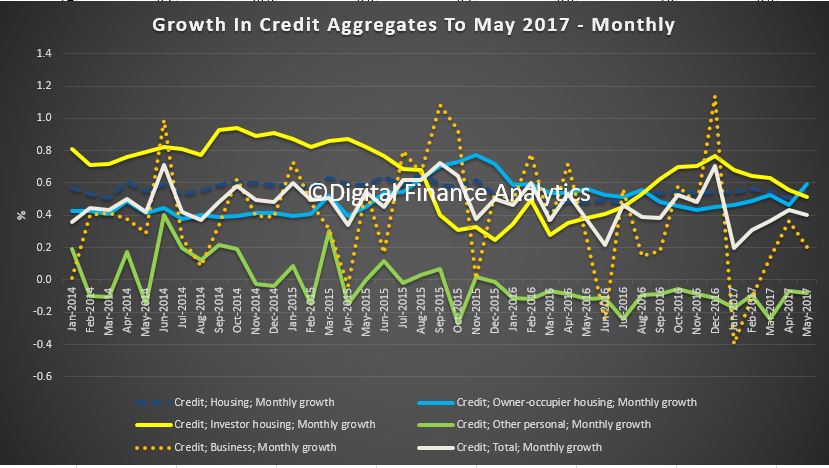

The more noisy, monthly series shows housing grew at 0.6% compared with 0.5% last month, whilst business grew 0.2% compared with 0.4% last month.

Growth in the aggregates show the proportion of investment loans fell just a little, while business lending as a proportion of all lending fell again.

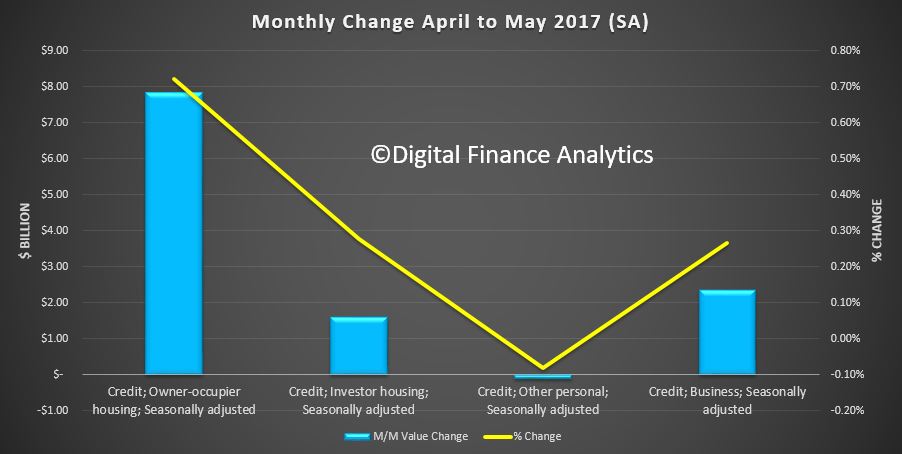

Here are the month on month moves. Owner occupied lending rose $7.8 billion (0.72%) and investment lending rose $1.6 billion (0.28%), both seasonally adjusted.

The RBA says more loans – $1.4 billion – were switched from investment to owner occupied loans, so the true state of play remains uncertain. $53 billion switched is a big number.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $53 billion over the period of July 2015 to May 2017, of which $1.4 billion occurred in May 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

It also appears the non-bank sector is growing (take the RBA aggregate from the APRA number earlier reported). $1.67 billion, less $1.56 billion = 0.11 trillion.

A widely-misreported warning of eight rate hikes in two years would in fact be good news for the economy, according to the man who made the prediction.

Dr John Edwards, former economic advisor to Paul Keating, former RBA board member and former chief economist at HSBC, struck fear into the hearts of mortgage holders this week by supposedly forecasting that the official cash rate would rise from 1.5 to 3.5 per cent by the end of 2019.

He actually wrote that the RBA would be forced to lift rates to 3.5 per cent onlyif the Australian economy substantially improved.

“This implies that within three years Australia’s economic world has returned to more-or-less normal, with wages growth of 3.5 per cent, inflation of 2.5 per cent, and output growth of 3 per cent,” Dr Edwards said.

He admitted such a rosy outcome might never eventuate.

“The pace of tightening will anyway be governed by the strength of the economy,” he wrote.

“If household spending weakness, if the long expected firming of non-mining business investment is further delayed, if the Australian dollar strengthens, if employment growth is persistently weak, then the trajectory of rate rises will be less steep and the pace less rapid.”

The piece prompted warnings that households would be forced to pay hundreds more a year in mortgage repayments, but Dr Edwards himself feared no such disastrous outcome: “The increases will cause less distress than will be widely observed.”

He said this was because housing interest payments were at 7 per cent of household disposable income, compared to 9.5 per cent in 2011 and 11 per cent just before the US-triggered global financial crisis.

These figures ignore the enormous impact of principal repayments. But the latest census data confirmed his point, showing that most parts of Australia were paying less overall on their mortgages than five years ago.

Dr Stephen Koukoulas, former economic adviser to Julia Gillard, said the economy would have to be “on fire” to necessitate eight rate rises, which would be “fantastic” news for workers.

He said GDP growth would have to be closer to 5 per cent, inflation 4 per cent and unemployment 3 per cent for the RBA to push the cash rate up by 200 basis points.

“If it comes to pass, it’ll be because the economy is in an inflation-inspired boom,” Dr Koukoulas told The New Daily.

Such a boom would help regular Australians because inflation is largely driven by household consumption, and “you need wages growth to underpin household consumption”.

A key factor is that the RBA sets the cash rate to target core inflation of 2 to 3 per cent over the medium term.

Because inflation has been below target for so many years, the central bank might allow it to sit at 3.2 or 3.3 per cent for a similar period of time, Dr Koukoulas said.

“There is a serious discussion among central banks that because of the hangover of the GFC, with low inflation still being recorded, let’s tolerate a year or two of above target inflation and let the unemployment rate get back down a little bit.”

Core inflation would only sit persistently above 3 per cent over the next two years if workers were “swimming in cash”, offsetting higher mortgage payments, which Dr Koukoulas said was an “improbable” but “fantastic” scenario.

Tom Kennedy, economist at JP Morgan, saw no such wage boom on the horizon.

In a research note on Thursday, he said next month’s minimum hourly wage increase of 3.3 per cent would be wholly offset by the much-publicised reduction in Sunday penalty rates.

Structural changes, such as underemployment and the increasing share of lower-paid services jobs, meant that the unemployment rate (currently 5.5 per cent) “most likely understates the slack” in the labour market, Mr Kennedy wrote.

Workers would have to get substantially more jobs and hours to enjoy wage rises, he said.