Yesterday, soon after the RBA announced a cut in the cash rate, the big banks started to announce they would pass a portion of the 25 basis points to some mortgages, and also lift some term deposit rates. CBA and NAB were first off the rank, followed by ANZ and WBC. They would have pre-planned a response, by the way.

Lots has been written about how the banks are not passing the full rate on, but much of the discussion is ill informed. So we wanted to bring some perspective to the scene.

First, bank funding and the cash rate have become disconnected, such that changes to the cash rate do not mesh with the real-life treasury rates within the banks. This is partly because banks can access funding from several sources, including deposits, overseas capital markets, bonds and securitisation. You cannot assume an automatic cut in loan rates follows, just as you should not expect credit card rates (which have remained higher for longer) to follow. The RBA “rate lever”is actually quite weak – the dollar went up after!

There are a series of decisions which the banks take, weighing up funding, margin, profit and market/competition issues. They all do this independently, of course, but are functioning within the same market, and tend to act in similar ways – a sign of weak real competition, rather than collusion.

First we need to observe that the yield curve (a theoretical mapping of rates out over the next few years) is very, very low, thanks to an expectation of lower future rates, for longer.

Second, banks want deposits, because in the current uncertain international capital markets environment, they are local, and reliable. Some now have more than 60% of the book matched to deposits, much higher than pre-GFC.

Fourth, with demand easing for lending, and the battle centred on refinance and investment loans, banks are cutting their headline rates to get share, and in the process are cutting the once generous discounts from the headline rate.

Fifth, term deposits have a different impact on the bank’s balance sheet compared with call deposits, as a result of changes made last year to the liquidity rules and the upcoming Net Stable Funding rules.

Finally, we know that bad debts are rising, from mortgage defaults, especially in the mining centric states, from consumer debt, and from some corporates. We also know that major corporations are driving margins on their loans lower.

So, with all this in mind, they have to solve the complex equation.

First, they needed to give something to mortgage borrowers, it would be political dynamite not to do so. So they gave away about half the headline rate drop. Then they lifted term deposit rates, partly as a smokescreen, so they could argue they are sharing the gain. Actually, a quick calculation would show that in real dollar terms, giving away more on term deposits costs a lot less than cutting the mortgage rate further. So they can pocket the difference.

But next, for fixed rate mortgages, and term deposits, they are able to lock in generous margins, thanks to the shape of the yield curve. At a stroke, they are able to bolster and protect their absolute margins for the next 2-3 years. This double hedge means NIM is locked in to lift performance.

Some of this margin growth will be offset by the need to lift capital buffers, the rest is available for distribution, after offsetting rising losses, thus keeping dividend payouts in the target band, and so meet – especially investment managers – high expectations.

Once again the market lifted the dollar higher following the RBA rate cut, 14:30 yesterday.

The local action was swamped by US economic news which saw the USD fall against most currencies. Take that into account and the limited pass through of the rate cut to borrowers, and we can conclude the RBA strategy is shot.

On an international basis, the economy here is still quite strong (and much stronger than many others). It is time for economists to stop calling for ever more cuts, when it clearly won’t work. Time for some fresh thinking. Lets ask what will it take to switch lending to business, and get real economic momentum going, rather than more housing loans. Simply cutting rates ain’t working. And we deplete ammunition in the locker should we have a real economic crisis.

Come on RBA, look harder at macroprudential alternatives. Be more creative.

The Reserve Bank of Australia has lowered the cash rate to 1.5% in an effort to stimulate growth, boost inflation and encourage a fall in the Australian dollar.

The cut of 25 basis points from 1.75% is the last decision from outgoing RBA Governor Glenn Stevens. In a statement on the rate decision he says:

“Low interest rates have been supporting domestic demand and the lower exchange rate since 2013 is helping the traded sector. Financial institutions are in a position to lend for worthwhile purposes.”

Professor Richard Holden from UNSW says the cut was needed.

“At 1.0% per annum — well below the target band of 2-3% – there is even the risk of deflation. Growth is relatively weak—indeed, net disposable national income growth has been negative for several years. The labour market is fairly weak as well. All in all, a cut was very much in order,” he says.

In his statement, Glenn Stevens also addressed the concerns around Australia’s property market. He noted Australia’s banks have been cautious in lending to certain sectors like the property market and despite the possibility of a considerable supply of apartments emerging over the next few years, lending for housing has slowed this year.

However Professor Holden says Stevens is downplaying the risks.

“I think that’s something of a blip, and that the housing price inflation risks are very real. I think he called this one incorrectly,” he says.

The Commonwealth Bank of Australia announced it would pass on 13 basis points of the cut to owner occupiers and property investors, Professor Holden says Australians can expect the rest of the big four banks to do the same, apart from ANZ.

Economist Saul Eslake from the University of Tasmania says he still doesn’t believe there is a reason for the RBA to cut rates, as moderate growth and modest expansion in employment weren’t cause for alarm at the last rate cut.

“Inflation is substantially below the RBA’s 2-3% target – but the post-meeting statement didn’t indicate that the most recent inflation data had prompted a major downward revision to the inflation outlook, such as would warrant lower interest rates, as it did when it last cut rates back in May,” he says.

The RBA statement cited international pressures such as China’s slowing economy, but Mr Eslake says this more likely to impact Australia in medium term rather than here and now.

“China has probably done enough to ensure that it meets this year’s GDP growth target of 6.5%. But they’ve done it in a way that increases the risks of a financial crisis down the track – by getting their banks to fund the latest lending splurge (which has helped to revive the Chinese property market)…by borrowing in the wholesale markets rather than through customer deposits,” he says.

Phillip Lowe takes over next month as the new governor of the RBA and he may be faced with limited reserves of monetary stimulus after this cut.

Mr Eslake says reserves might be needed if Donald Trump were to win the United States Presidential election in November.

“If that prospect were to prompt a ‘rush for the exits’ on the part of foreign investors in the US, [it could] send the US dollar substantially lower and hence, possibly, sending other currencies, including the Australian dollar, much higher against the US dollar than the RBA would feel comfortable with.”

Economist Timo Henckel from ANU says the RBA will probably wait a few more rounds before cutting further.

“By historic standard, Australian interest rates are exceptionally low, and economists will want to see how these low rates affect the wider economy, a transmission mechanism that is complex and characterised by long and variable lags,” he says.

Author: Jenni Henderson, Assistant Editor, Business and Economy, The Conversation

At its meeting today, the Board decided to lower the cash rate by 25 basis points to 1.50 per cent, effective 3 August 2016.

The global economy is continuing to grow, at a lower than average pace. Several advanced economies have recorded improved conditions over the past year, but conditions have become more difficult for a number of emerging market economies. Actions by Chinese policymakers are supporting the near-term growth outlook, but the underlying pace of China’s growth appears to be moderating.

Commodity prices are above recent lows, but this follows very substantial declines over the past couple of years. Australia’s terms of trade remain much lower than they had been in recent years.

Financial markets have continued to function effectively. Funding costs for high-quality borrowers remain low and, globally, monetary policy remains remarkably accommodative.

In Australia, recent data suggest that overall growth is continuing at a moderate pace, despite a very large decline in business investment. Other areas of domestic demand, as well as exports, have been expanding at a pace at or above trend. Labour market indicators continue to be somewhat mixed, but are consistent with a modest pace of expansion in employment in the near term.

Recent data confirm that inflation remains quite low. Given very subdued growth in labour costs and very low cost pressures elsewhere in the world, this is expected to remain the case for some time.

Low interest rates have been supporting domestic demand and the lower exchange rate since 2013 is helping the traded sector. Financial institutions are in a position to lend for worthwhile purposes. These factors are all assisting the economy to make the necessary economic adjustments, though an appreciating exchange rate could complicate this.

Supervisory measures have strengthened lending standards in the housing market. Separately, a number of lenders are also taking a more cautious attitude to lending in certain segments. The most recent information suggests that dwelling prices have been rising only moderately over the course of this year, with considerable supply of apartments scheduled to come on stream over the next couple of years, particularly in the eastern capital cities. Growth in lending for housing purposes has slowed a little this year. All this suggests that the likelihood of lower interest rates exacerbating risks in the housing market has diminished.

Taking all these considerations into account, the Board judged that prospects for sustainable growth in the economy, with inflation returning to target over time, would be improved by easing monetary policy at this meeting.

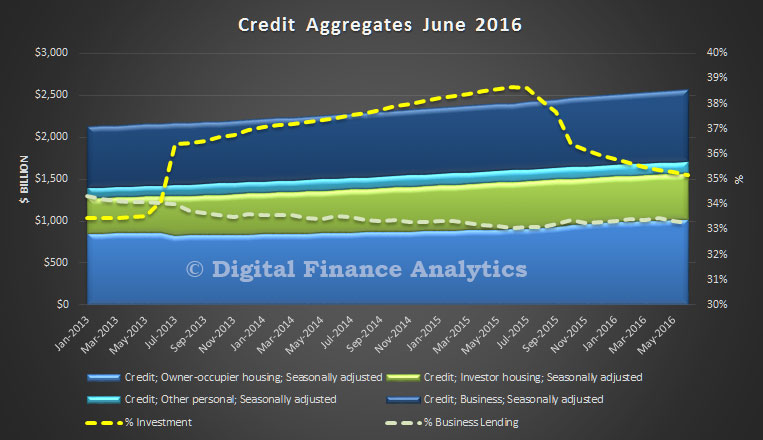

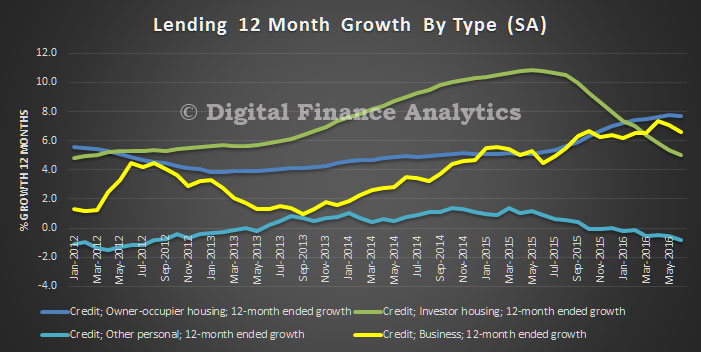

The June 2016 Credit Aggregates from the RBA, released today, shows that total lending for housing rose $6.6 billion or 0.42% in the month, making an annual rate of 6.7%, compared with 7.3% a year ago. Total loans outstanding for housing were $1,569 billion, another record.

Loans for investment housing rose by 0.1% or $0.6 billion, whilst lending for owner occupation rose 0.6% or $6.1 billion. Again we saw considerable shifts between owner occupied and investment loans in the month due to re-classifications, so there is still noise in the data. That said 35.1% of all housing loans are for investment purposes, down from 35.3% last month.

Business lending fell by 0.11% seasonally adjusted, or $0.9 billion, giving an annual growth rate of 6.6%, up from 4.4% last year. However, the proportion of lending for business fell again to 33.2% of all loans, a worrying continued falling trend. Personal credit also fell a little.

Still we see more lending for housing rather than to business. Not good news for the economic outlook.

The RBA notes

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $42 billion over the period of July 2015 to June 2016 of which $1.3 billion occurred in June. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

The Council of Financial Regulators (CFR) has issued a report to Government on the potential impact of Brexit on the Australian economy. It takes into account developments up to and including Tuesday 5 July. They conclude that the outcome of the vote on 23 June represented an appreciable negative shock, but the impact on domestic and international financial systems and markets was well-contained and orderly. On the evidence to date, they say it suggests that the domestic and international financial reform agenda adopted following the financial crisis is on the right track.

The CFR is comprised of the Reserve Bank of Australia (RBA); the Australian Prudential Regulation Authority (APRA); the Australian Securities and Investments Commission (ASIC); and the Treasury. The report is informed by CFR agencies’ close consultation with their respective counterparts in the UK, Europe and other jurisdictions.

It is uncertain how the UK’s exit will proceed and what the associated impacts on the stability of the rest of the EU will be. This will be a source of continuing uncertainty and market volatility for some time, against the backdrop of an already fragile global economy. Significant shocks could also come from other sources. While the Australian financial system has weathered the immediate reaction to the vote well, the event underscores the importance of pressing ahead with further reforms to enhance our system’s resilience.

The short-run negative effect on economic activity in Australia, through channels such as reduced trade, lower commodity prices and financial linkages, is expected to be very limited for several reasons. The effect on global activity is expected to be small, Australian trade is oriented more towards Asia than Europe, and Australian banks have limited direct exposure to the UK and Europe and are well-placed to handle disruptions to funding markets.

The medium- to longer-term implications for the UK and Europe, and the global economy more broadly, will depend on the degree and persistence of uncertainty, and the length and outcome of negotiations on exit. In the UK, business investment growth was already weak prior to Brexit and is likely to weaken further, at least until the nature of any future trade agreement with the EU, by far the UK’s largest export market, is known. Some firms may also choose to relocate from the UK to EU countries if their businesses depend on access to the single market. Concerns over job security and negative wealth effects will be a drag on household spending. Prior to Brexit, the IMF indicated that should Britain vote to leave the EU, GDP in the EU could be lower by up to 0.5 percentage points and GDP in the rest of the world could be up to 0.2 percentage points lower by 2018.2 There is a significant degree of uncertainty around the estimated economic impact of Brexit. The IMF forecast a wide variation in output losses across individual economies, reflecting differing trade and financial exposures to the UK, as well as the policy space to respond to negative spill-overs.

Beyond the central forecasts, the Brexit result has arguably added to global tail risks, particularly through heightened risk in Europe. The result could potentially strengthen exit momentum within euro area countries, which if successful would be considerably more disruptive given the common currency. Ongoing banking sector fragility also remains a potential trigger for political discord and financial instability. European banks have been grappling with weak profitability and a high stock of non-performing loans for many years, which has been reflected in low share price valuations. Market movements reflect increased apprehension about banks in a number of European countries post Brexit, most notably Italy, where the Italian Government has been denied permission by the EU to inject capital into its banking system. The newly established European bank resolution framework, which favours bail-in of private creditors and substantially precludes government support, is largely untested.

Overall, tail risk considerations aside, the implications of Brexit for the Australian economy are not likely to be significant, but will depend upon the nature and length of the transition to new arrangements. Australia has proved resilient during past periods of financial market volatility and remains well placed to manage the economic and financial market response from the UK referendum outcome. Additionally, Australia has a relatively small direct trade exposure to both the UK (2.8 per cent of goods and services exports) and the rest of the EU (4.6 per cent of goods and services exports). However, Australia’s major trading partners have larger exposures to these markets. For example, the EU (including the UK) accounts for 15.6 per cent of China’s goods exports and 18.2 per cent of the US’s goods exports. A sharp slowdown in the EU economies with spill-overs into other major economies would place downward pressure on the demand for Australia’s exports.

The Australian economy may also be affected if the UK transition out of the EU is not orderly and uncertainty remains heightened for a significant period. This poses some downside risk to the domestic outlook, with negative wealth and confidence effects having the potential to affect household consumption and business investment.

The strengthening of the banking system’s capital position over recent years to meet the new ‘Basel III’ requirements represents a material increase in the banking sector’s ability to withstand a significant deterioration in asset quality. The Financial System Inquiry highlighted the importance of ensuring the soundness of the financial system. The Government endorsed its recommendation that capital standards be set such that bank capital ratios are ‘unquestionably strong’. While Australian banks are well-capitalised, a further increase in capital ratios is likely to be required over the coming years to satisfy the ‘unquestionably strong’ benchmark. The Government has also endorsed the implementation by APRA, over

time and in line with emerging international practice, a framework for loss absorbing and recapitalisation capacity.

APRA is also introducing further reforms to strengthen the resilience of the banking system. Of particular note, on 1 January 2018, APRA will implement the Basel III Net Stable Funding Ratio (NSFR) to discourage banks from being overly reliant on less stable sources of funding. The NSFR will be part of APRA’s prudential liquidity rules and will complement the Liquidity Coverage Ratio – introduced on 1 January 2015 – that requires banks to hold sufficient ‘high quality liquid assets’ to withstand a 30-day period of stress. APRA is currently consulting with the industry on the design of the NSFR and intends to finalise proposals by the end of 2016.

Consistent with the Government’s response to the FSI, further work is needed to clarify and strengthen regulators’ powers in the event a prudentially regulated financial entity or financial market infrastructure faces distress. A recent peer review by the Financial Stability Board identified some gaps and deficiencies in the Australian resolution framework and work is progressing on this as a matter of priority.

More broadly, such episodes of significant shocks and market volatility reinforce the value of Australia’s financial (and economic) policy frameworks. The separation of responsibility for prudential regulation and market conduct regulation (between APRA and ASIC), the operation of independent monetary policy and a floating exchange rate continue to serve us well.

The Reserve Bank of Australia (RBA) looks set to cut interest rates aggressively over the next 18 months, but it’s unlikely to result in any meaningful decline in the level of the Australian dollar.

That’s the view of James McIntyre, an analyst at Macquarie Research who has been on the money of late when it comes to Australian interest rates. He believes that additional monetary policy easing from the Bank of Japan and Bank of England, among others, along with a less aggressive rate hike schedule from the US Federal Reserve, will keep the Aussie well supported in the year’s ahead.

“With a diminished outlook for monetary policy divergence the prospects for a lower A$ have weakened,” says McIntyre.

“We remain of the view that the RBA will need to cut rates further, dragged down by a disinflationary outlook. But with easing elsewhere, those rate cuts are unlikely to deliver significant A$ weakness. Rather, rate cuts are now likely to be needed to contain A$ upside. Although the RBA is cutting, we don’t think it will be cutting fast, or far, enough.”

As a result, McIntyre believes that it will be hard for the AUD/USD to break below the 70 US cent level, an area that the currency ventured below earlier this year.

“In the absence of a shock, we think that the hit to global growth and shift towards a less restrictive monetary policy stance is likely to support the A$. A firmer currency will dampen the inflation outlook, and also provide less impetus for economy’s rebalancing,” he says.

As shown in the chart below, supplied by Macquarie, the bank now expects the AUD/USD to bottom out at 72 cents in 2017, a far cry from the 65 cent level seen just three months ago.

Along with hindering Australia’s economic transition (Macquarie now sees GDP growth of 2% in 2017, down from 2.5% forecast previously), McIntyre believes that strength in the Aussie could help to boost migration levels, further exacerbating disinflationary pressures that already exist within the domestic economy.

“We see this as weighing further on the inflation outlook, as the economy will struggle to grow fast enough to keep up with potential, absorb spare capacity, and generate inflation,” he says.

In order to help counteract disinflationary forces, McIntyre believes that the RBA will have to cut rates lower, sooner and for longer than what many in financial markets currently believe.

“We retain our base case for a 25bp August rate and our forecast for a 1% cash rate trough,” he says. “We now expect the RBA will reach that low sooner, in 2Q17.”

The latest RBA minutes, published today do not provide much extra insight, other than saying the longer-term impact of Brexit is yet unknown, and local economic signals remain mixed. Looks like August will provide the data point to determine possible next steps.

GDP growth in Australia’s major trading partners looked to have remained slightly below average over recent months, in line with earlier forecasts. GDP growth in China appeared to have eased further, which was continuing to affect economic conditions throughout the Asian region. Monetary policy remained very accommodative across the major economies and was expected to remain so given that inflation was below most central banks’ targets, despite improvements in labour markets leading to full employment in several large advanced economies.

The United Kingdom’s vote to leave the European Union had led to considerable financial market volatility, which had since settled. Financial markets had functioned effectively throughout the episode and borrowing costs for high-quality borrowers remained low. Any effects of the referendum outcome on UK and global economic activity remained to be seen. In any event, the referendum result implied a period of uncertainty about the outlook for the United Kingdom and the European Union. In the absence of significant financial dislocation, the staff’s central case was that this uncertainty was expected to have only a modest adverse effect on global economic activity.

Commodity prices had generally increased since the previous meeting. At the time of the present meeting, the Australian dollar (in trade-weighted terms) was around the levels assumed in the forecasts at the time of the May Statement on Monetary Policy.

In the domestic economy, the transition of economic activity to the non-resources sector was now well advanced and recent data suggested that growth had continued at a moderate pace in the June quarter. Low interest rates were continuing to support household spending and the lower exchange rate since 2013 had continued to assist the traded sector of the economy. Members noted that an appreciating exchange rate could complicate the necessary economic adjustments.

Recent data showed that conditions in the labour market had been more mixed of late. The unemployment rate had remained around 5¾ per cent for most of 2016, having fallen noticeably over 2015. Inflation was still expected to remain quite low for some time given very subdued growth in labour costs and very low cost pressures elsewhere in the world.

Indicators of conditions in housing markets had been somewhat mixed over recent months. Housing prices were recorded as having risen in Sydney and Melbourne in April and May, but were little changed in June. Building approvals remained elevated at levels that would add to the considerable amount of dwelling construction work already in the pipeline. Considerable supply of apartments was scheduled to come on stream over the next few years, particularly in the eastern capital cities. At the same time, however, housing credit growth had eased, in line with a lower turnover of housing and the earlier tightening in banks’ lending standards following the announcement of supervisory measures. Various state government measures and changes to bank lending requirements were likely to temper foreign investor demand for housing.

Taking account of the available information, the Board judged that holding monetary policy steady would be the most prudent course of action at this meeting. The Board noted that further information on inflationary pressures, the labour market and housing market activity would be available over the following month and that the staff would provide an update of their forecasts ahead of the August Statement on Monetary Policy. This information would allow the Board to refine its assessment of the outlook for growth and inflation and to make any adjustment to the stance of policy that may be appropriate.

The latest RBA chart pack, released today includes data on household debt. Debt a a percentage of disposable income is up again, to an all time high. This is driven by flat income growth, and ever more home loan borrowing. Even after the May interest rate cut, interest paid as a proportion of disposable income has risen.

This is of course an average, and segmented data contains considerable variation.

The world still needs the central banks to bail us out of trouble but the impact of monetary policy is complicated in a world of zero or near-zero interest-rate policy (ZIRP) and negative interest-rate policy (NIRP).

Money presents us with three alternatives: we can spend it, save it or invest it. Most households and governments do the first; financial institutions take the third option; and virtually no one saves. Except Asia, obviously.

In 2008, spending and investment froze during the global financial crisis (GFC). This forced central banks and governments to ultimately adopt unorthodox and largely unprecedented strategies. Two tools were available to governments: fiscal stimulus and looser monetary policy. Most governments adopted a mix of both.

However, there are political and financial limits to fiscal policy, particularly as governments grew increasingly overextended during the GFC. Consequently, since 2008, monetary policy has largely displaced fiscal policy as means of generating economic stimulus. Except in Sydney, at the Reserve Bank of Australia (RBA).

ZIRP it. ZIRP it good

The Bank of Japan (BoJ) was the first to adopt ZIRP, as it sought to deal with the aftershocks of the Heisei recession of the early 1990s. This was referred to as Japan’s “lost decade”, as it experienced stagnant growth, a condition still bedevilling the country today, despite the best efforts of Abenomics.

As the global financial crisis emerged throughout 2007–08, the US Federal Reserve, the European Central Bank (ECB) and the Bank of England sank hundreds of billions of their respective currencies into their foundering financial sectors. The People’s Bank of China injected massive liquidity into Chinese markets.

In Australia, the RBA slashed interest rates, with deep successive cuts in 2008–09. Looser monetary policy was matched by the Rudd government’s significant fiscal expansion to prevent the collapse of consumer spending.

The reason behind this fiscal pump priming, combined with the dramatic monetary measures, was clear: in late 2008, credit markets froze. Admittedly, there is much debate about how long and to what extent this occurred. However, the fear of contagion was so palpable that the interbank lending market experienced systemic dysfunction and, at the very least, credit rationing took place.

The problem for central banks is that they have relatively few monetary tools available to them. The traditional lever to prevent overheating is to exert monetary discipline by raising interest rates, thus increasing the cost of credit.

Conversely, under the crisis conditions of the GFC, the central banks slashed interest rates to encourage consumption. However, the US Federal Reserve, the Bank of Japan, the Bank of England and the European Central Bank reached their lower limits faster than the RBA, which never adopted ZIRP.

But that may be about to change. The RBA’s cash rate is at a historic low of 1.75%, and the bank may cut further as the Australian economy plateaus, combined with the uncertainty wrought by Brexit.

The new normal

Make no mistake: ZIRP and even perhaps NIRP are the new normal. Just ask Janet Yellen. When the Federal Reserve chairman increased US interest rates by 0.25% in December 2015, the markets reacted savagely. It was the first Federal Reserve (Fed) rate rise since 2006.

US Federal Reserve chair Janet Yellen.JIM LO SCALZO/AAP

Fourteen months earlier, Yellen had tapered off the US’s third quantitative easing program (QE3), ending it on schedule in October 2014. Between 2008 and 2014, the Fed had purchased over US$4.5 trillion in government bonds and mortgage-backed securities in three rounds of QE, plus a fourth program, Operation Twist (2011–12).

The outcome was an avalanche of “free” money. Why “free”? Because, in the long run, the real cost of the capital for commercial banks was zero, or less than zero.

The Fed was effectively printing money (although it’s more complex than that). The effects were clear: the US central bank was reflating the American economy, and by extension the global economy, by injecting massive amounts of liquidity into the system in an attempt to ameliorate the worst effects of the 2008–09 financial crisis.

US Fed moves this year

No one on the markets was surprised by the central bank’s December 2015 rate rise. The clear objective was to return some semblance of normality to global interest rates.

The problem is it didn’t work. The tapering-off of QE in late 2014 meant that the last sugar hits of stimulus were wearing off in 2015.

The Yellen rate rise, plus the clear intention of the Fed to incrementally drive rates higher, spooked the markets. In May this year, undeterred by gloomy US jobs figures, Yellen indicated that she would seek to raise US interest rates “gradually” and “over time” as US growth continued to improve. Her concern was that adherence to ZIRP would ultimately bite in the form of inflation.

Not anymore. Brexit has seen to that. It was one of the factors behind the Fed committee’s decision to keep interest rates on hold in mid-June.

ZIRP – or something approximating it – is becoming the “new normal” because cheap money has become structural; the global financial system is now structured around the persistence of low-cost credit. NIRP is thus the logical continuum of this downward interest rate spiral.

Negative interest zates

Until recently, most macroeconomic textbooks argued that zero was rock bottom for interest rates. The GFC shifted the goalposts.

This is where NIRP enters the picture: negative interest rates. How do they work? Typically, commercial banks will park their money in their accounts with the central bank, or in private markets, such as the London Interbank Offered Rate (LIBOR). Thus, their money never sleeps and earns interest 24/7, even when bank doors are shut.

But NIRP is different. Negative rates mean depositors pay for the privilege of a bank to hold their money. Which means depositors are better off holding the cash than placing the funds on deposit. Japan has experienced the results of a NIRP first-hand.

Bank of Japan (BOJ) Governor Haruhiko Kuroda decided to adopt negative interest rates.FRANCK ROBICHON/AAP

There is a method in this madness: the G7 central banks want commercial banks to lend, not to accumulate piles of cash. Consequently, the policy effect of both ZIRP and NIRP is to stimulate business and consumer lending in order to drive real economic activity. With piles of cash looking for investment placements, the shadow banking system of financial intermediaries may also drive enterprise investment.

However, ZIRP and NIRP are blunt instruments; the perverse outcomes of the stimulus programs of the US Fed, the Bank of Japan and the European Central Bank were artificially inflated stockmarkets and various sector bubbles (such as real estate, classic cars).

The combination of ZIRP and QE may have also created a “liquidity trap”. This means that central banks’ QE injections caused only a sugar rush and did not inflate prices, as one would normally expect from a significant expansion of the monetary base.

Instead, many developed countries have experienced multiple recessions and a prolonged period of deflation. In April this year, the Australian economy experienced deflation for the first time since the GFC, which compelled the RBA to make its most recent 0.25% cut in May 2016.

Yellen knows the global economy cannot retain ZIRP indefinitely. But, ironically, all of the central banks are caught in their own liquidity trap: unable to relinquish ZIRP for fear of market catastrophe; unwilling to abandon QE entirely as “the new normal” demands fresh injections of virtually cost-free credit.

A lack of interest

The Australian economy has done quite well by having interest rates above the OECD average, particularly since the GFC. This has encouraged significant foreign investment flows into Australia as global investors seek somewhere – anywhere – to park their cash as other safe-haven government bonds, such as the US, Japan and Germany, are in ZIRP or NIRP territory. It also doesn’t hurt that Australia’s major banks and government bonds are blue-chip-rated. And Australian sovereign bonds have excellent yields too.

If ZIRP is the new normal, that matters to the Reserve Bank of Australia. It also matters to all Australian home buyers, businesses, banks, pensioners, investors, students and credit card holders. Everyone, in other words.

ZIRP has created hordes of winners: mortgage interest rates are at historic lows. Property buyers who borrowed when rates were relatively high (at, say, 6-7%) are now paying less than 4%. Credit card rates are still astronomically high (20–21% or more), but balance transfer rates are zero. New credit issues in terms of consumer debt represented by unsecured loans (which is what a credit card is) have a real capital cost of zero. This is virtually unprecedented.

But ZIRP or near-ZIRP produces many losers as well. There is no incentive to save because rates are so low. Hoarding cash makes no sense.

Global surplus capacity reinforces deflation as both goods and commoditised services are cheap. Wages are terminal. Pension funds’ margins are smaller, thus expanding future liabilities and reducing the value of current superannuation yields.

In a world of ZIRP, is it any wonder that all of this cheap or (effectively) free cash has been stuffed into the global stock exchange and real estate markets, creating not only a double bubble, but double trouble?

The best things in life are free

QE is like heroin: the first hit is always free. The commercial banks got their first hit in 2008 and the prospect of going cold turkey sends them into paroxysms of fear.

The problem is that the dealers – the central banks – have started using their own product and are just as hopelessly addicted to both ZIRP and QE. To rudely cut off supply would destroy their own markets.

The RBA is not immune to the elixir of ZIRP. No central bank wants to assume responsibility for a recessionary economy; the RBA took enough heat for its monetary policy mismanagement of 1989-90, which induced the 1990s recession.

Unlike the Fed, the RBA is not about to fire up the printing presses and engage in rounds of QE, if it runs out of tools and is compelled to adopt ZIRP. The RBA is too conservative to engage in such policy in any case.

But this conservatism has a direct impact upon federal government fiscal policy, irrespective of whether the LNP or the ALP is in power. From Rudd to Turnbull, Treasury has been forced to increase its borrowing time and time again, blowing out the forward fiscal projections year after year.

No government has delivered a surplus because it is no longer possible. The RBA is partly responsible for this because, rather than expanding its balance sheet via QE, it has forced Canberra to accumulate government debt of more than $AU400 billion, which the overburdened Australian taxpayer will pay for.

Like most drug deals, this will not end well.

Author: Remy Davison, Jean Monnet Chair in Politics and Economics, Monash University

Lots has been written about how the banks are not passing the full rate on, but much of the discussion is ill informed. So we wanted to bring some perspective to the scene.

Lots has been written about how the banks are not passing the full rate on, but much of the discussion is ill informed. So we wanted to bring some perspective to the scene.