There are some amazing mortgage refinance deals out in the market at the moment as lenders seek out lower risk mortgage borrowers, so it is worth considering whether a refinance is appropriate for your financial situation.

There are both benefits and risks, as this guest post from NSW Mortgage Corp highlights.

There are both benefits and risks, as this guest post from NSW Mortgage Corp highlights.

First let’s be clear what a refinance is. Essentially it means transferring your current mortgage to another lender, (or a different loan with the same lender), and it may be for the same amount, or if there is sufficient equity, you might be able to get a bigger loan. But there might be fees to do this, and not all lenders have the same deals, so it is important to shop around.

There are a range of scenarios where a refinance makes sense.

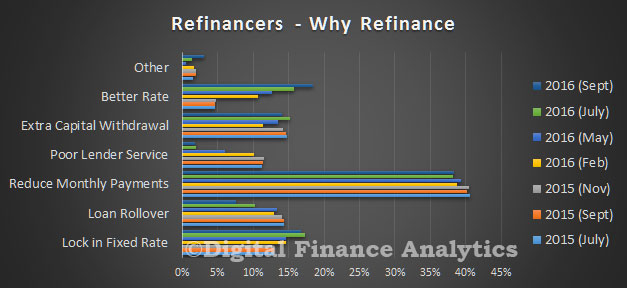

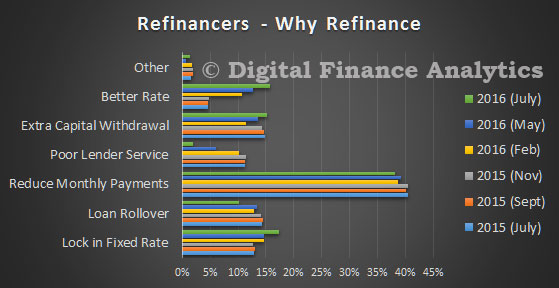

Reducing Monthly Payments and Avoiding Default

Many households are finding their monthly mortgage repayments a strain, yet they are not necessarily on the lowest available rate. Depending on your current rate it might be possible to reduce the real monthly payments. In some cases, this make the difference between keeping the mortgage up to date and missing payments, which might lead to default.

Helping with Home Renovations

With home prices on the slide in some areas, more home owners are looking towards home renovations as a way to increase the equity in their home. But, home renovation is costly. Renewing or restoring your home to its former conditions may require expensive materials and skilled labor. You need money to finance house renovations like fixing of old walls and ceilings, repainting and plumbing works. Things could get more costly if you would include roof repair or replacement, fixing of sewer line problems, and fixing pest problems.

But if there is sufficient equity in your property (value of the property less current mortgage) it is feasible to refinance and drawn down money for renovation. Often this is a more cost effective route than looking to fund renovations on a credit card, or even a personal loan, because secured interest rates tend to be significantly lower.

Invest in Education

Some households use equity from their property to pay for or to complete a college education, but this is getting more costly with time. For those thinking of going back to school while working, taking a break to complete the course funded from equity might work for you (provided the mortgage repayments can still be met from the household budget). Applying for refinance mortgage could spell the difference between a good and stable career and failure. Sometimes, you just have to make the decision and move forward with your career goals. In the same way, parents who are willing to send their children to a good school can take advantage of mortgage refinance. They can use the money to pay off the old mortgage and get some extra cash for their child’s education. This way, you don’t have to get another short-term loan or charge your credit card with a high interest date for your child’s tuition fees.

Pay outstanding bills

This is more tricky, but in some cases a refinance can be used to pay outstanding bills and so avoiding missing payments, save money on late fees and avoid getting a bad credit score. Think of this as a one-time opportunity to revamp your finances, as it’s not something which can be repeated often, the equity in the property is not an ATM.

Also, some loans have pre-payment penalties, while others don’t. So before you make any advanced payment, clear this up with your creditor. You can also pay overdue bills and save yourself from collectors and court suits.

The Small Print

But, you have to face one big truth – not all refinance mortgages are the same. There are lenders who have lenient standards and those that are very strict especially in terms of your income requirement. Others have strict credit score requirements and financial documents. So, before you sign up for the next refinance mortgage, ask everything you need to know about the requirement and the loan agreement.

While there are many benefits to mortgage and home refinance loans, there are risks to keep in mind as well.

Before choosing a refinance product:

- Shop around and ensure you choose a refinance product best suited to your needs. Criteria includes what your loan to value ratio (LVR) is, and which home loan features you need or which features you no longer want

- Make sure that the new mortgage is cheaper than your original mortgage

- Be aware there may be high exit fees for leaving your fixed rate home loan early, and upfront fees from your new lender. Ask about additional costs such as private mortgage insurance, application of valuation fees, and the possibility of getting a third mortgage

- Know the modes of payment. Some lenders offer interest only payment, which may sound so good because of low monthly dues, but it can actually draw more money from you because you are simply paying the interest and not the principal. Make sure that the payment terms allow you to pay the principal, plus the interest each month

- Consider the housing market. Don’t get refinancing when the market is not doing well. You may end up paying very high fees in exchange of a loan. Why don’t you wait till it gets better? Or, you can opt for a more practical solution. Look for a lender that gives you an interest rate and loan costs which is similar to loan terms when the market is favorable. Remember that volatility has a high impact in the pricing of the real estate properties and the mortgage fees as well

- Check whether making multiple refinance applications are damaging your credit file. Only make soft enquiries which do not affect your credit score

There are many reasons to get a mortgage refinance, but it ultimately depends on your situation. Always shop around and take your time to do research before making a decision. While shopping around, avoid making hard inquiries as this will lower your credit score which will result in getting higher interest rates. By considering all the advice given in this article, you will be able to determine which refinance product is best for you.