The Federal government has today announced that it will be commissioning an independent review of the retirement income system, via InvestorDaily.

This

review was recommended by the Productivity Commission in their report

Superannuation: Assessing Efficiency and Competitiveness and comes 27

years after the establishment of compulsory superannuation.

The

review will look at the three pillars of the existing retirement income

system, being the Age Pension, compulsory superannuation and voluntary

savings.

In doing so, the review will cover the current state of

the system and how it will perform in the future as Australians live

longer and the population ages.

Through its work, the review will

establish a fact base of the current retirement income system that will

improve understanding of its operation and the outcomes it is delivering

for Australians.

The review will be conducted by an independent three person panel.

Mr

Michael Callaghan AM PSM, a former Executive Director of the

International Monetary Fund and a former senior Treasury official will

chair the review, together with fellow panellists Ms Carolyn Kay, who

has more than 30 years’ experience in the finance sector across roles

both in Australia and overseas, including as a member of the Future Fund

Board of Guardians, and Dr Deborah Ralston, who is a Professorial

Fellow in Banking and Finance at Monash University, a member of the

RBA’s Payments System Board and most recently chair of the Alliance for a

Fairer Retirement.

A consultation paper will be released in November 2019 and the final report provided to Government by June 2020.

The

Review will establish a fact base of the current retirement income

system that will improve understanding of its operation and the outcomes

it is delivering for Australians. It aims to identify how the

retirement income system supports Australians in retirement, the role of

each pillar in supporting Australians through

retirement, distributional impacts across the population and over time

and the impact of current policy settings on public finances.

FSC

CEO Sally Loane said the FSC will work closely with the review to ensure

continuing improvements to Australia’s retirement income system,

particularly through the superannuation system.

“Superannuation

consumers receive significant benefits from competition and choice, and

this will be an important focus of the FSC’s approach to the Review,” Ms

Loane said.

“However, this review should not delay important

reforms that the Government has already committed to that will

significantly improve consumer outcomes in superannuation.

“These

include the introduction of a ‘default once’ framework to prevent

unintended multiple accounts, as recommended by both Commissioner

Kenneth Hayne and the recent Productivity Commission review of

superannuation, and legislating an obligation for trustees to consider

the retirement needs of their members.”

The FSC will also suggest

to the review that the government should retain its policy of increasing

the Superannuation Guarantee to 12 per cent. The FSC also suggests that

superannuation laws should be simplified and red tape in the sector

should be removed including barriers to rationalising legacy products.

“The

FSC looks forward to advocating strongly for these positions during the

Review process over the coming year,” Ms Loane said.

AMP welcomed

the review and said a strong retirement system is essential to

supporting the wellbeing of Australians now and into the future.

“This

is a once-in-a-generation opportunity to improve our current retirement

system to make sure it adequately serves everyone’s needs. Now is the

time to have the debate on this issue,” an AMP spokesperson said.

Latest on the cash ban, which was presented in Parliament today, with Robbie Barwick from the CEC.

On 19 September 2019, the Senate referred the provisions of

the Currency (Restrictions on the Use of Cash) Bill 2019 [Provisions] to the Economics Legislation Committee for inquiry and report by 7 February 2020.

If you’d like to be part of a delegation to visit your local MP, call the CEC on 1-800 636 432 to be put in touch with others in your area.

Use and share these links for finding MPs and Senators. Click the link, and find the heading State/Territory in the box titled Refine Search on the right hand side of the page. Click on your state and call as many MPs and Senators as you can, on their Parliament House numbers, starting with 02-6.

More on the Cash Restriction Bill with Robbie Barwick from the CEC.

The Liberal/Nationals joint party room agreed to support the bill, despite the 4,000 or so public submissions not posted by Treasury, and the details of the bill yet to be released. Democracy at work?

Use and share these links for finding MPs and Senators.

Click the link, and find the heading State/Territory in the box titled Refine Search on the right hand side of the page. Click on your state and call as many MPs and Senators as you can, on their Parliament House numbers, starting with 02-6.

British health-care conglomerate Bupa runs more nursing homes in Australia than anyone else. We now know its record in meeting basic standards of care is also worse than any other provider. Via The Conversation.

This is more than a now familiar story of a corporation putting

shareholders before customers. It is also about another abysmal design

failure in regulation.

Health care is meant to be one of our most regulated sectors. In this

case, Bupa’s facilities were inspected and certified by the Aged Care

Quality and Safety Commission.

The regulator’s inspectors found 45 of Bupa’s 72 nursing homes

failed health and safety standards. In 22 homes the health and safety

of residents was deemed at “serious risk”. Thirteen homes were

“sanctioned” – with government funding being withheld and the homes

banned from taking new residents.

Yet none of this appears to have spurred Bupa’s management into action, according to media reports.

Flurries of inspection reports and written warnings over months and

years only underlined that the regulatory tiger, even if it had teeth,

had a very soft bite.

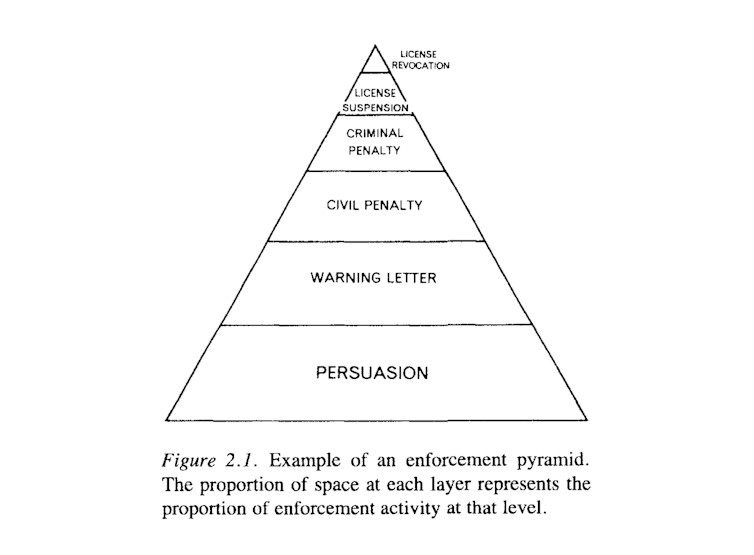

Responsive regulation

We have seen examples of equally insipid regulation in other areas.

In the building sector, for example, a range of regulatory flaws

including outsourced building certification have led to shoddily built and dangerous apartment construction.

In the financial sector, the banking royal commission castigated the

industry regulators – the Australian Securities and Investments

Commission and the Australian Prudential Regulatory Authority – for

their unwillingness to enforce rules.

“The conduct regulator, ASIC, rarely went to court to seek public denunciation of and punishment for misconduct,” noted royal commissioner Ken Hayne. “The prudential regulator, APRA, never went to court.”

This failure is due to more than individual agency shortcomings. It’s

an unintended consequence of the design of “responsive regulation” –

the system that has superseded command-and-control regulation over the

past three decades.

Responsive regulation was popularised by Australian sociologist John

Braithwaite and American law professor Ian Ayres in the early 1990s. It

was intended to overcome the pitfalls of the command-and-control model,

which involved regulators employing large numbers of inspectors to look

for non-compliance.

From about the 1970s it had become increasingly evident this model

wasn’t working. It was also very expensive. Consider, for example, the

cost of having fire and health and safety inspectors visit every single

building site, particularly when most builders were doing the right

thing. The cost and intrusiveness of the system fuelled calls to do away

with regulation .

Too big to fail

Ayers and Braithwaite saw their model as a way forward.

“Responsive regulation is not a clearly defined program or a set of prescriptions

concerning the best way to regulate,” they explained. “On the contrary, the best strategy is shown to depend on context, regulatory culture and history.”

Responsive regulation assumes that in most cases the enterprises

being regulated are interested in compliance and will respond to

light-touch directives. It assumes that often compliance failures are

due to ignorance or inadequate procedures. Its approach is to give

parties a chance to amend their ways.

But there’s a potentially huge flaw in the responsive regulation

model. What happens when an organisation is so large it is deemed too

big to fail, or deems itself so?

This seems to have been the case with a number of financial companies

whose misdeeds were exposed by the banking royal commission. It seems

it might have been the case with Bupa.

In such cases, because of the timidity of the regulator or the

confidence of the enterprise, the warnings might just go on and on. The

company continues to book its profits – which may well eclipse any

penalty it might have to pay if crunch time does ever come.

Markets have their limits

This design flaw highlights a more fundamental problem with

governments positioning themselves as rule makers and leaving the rest

to the “market”.

Markets are designed to facilitate exchange on the basis of profits.

The profit motive means market participants look for the lowest-cost

option. In aged care this means paying the lowest possible wages,

possibly to unqualified staff, and cutting corners to cut costs.

Markets are very useful for increasing individual choices and

efficiently allocating resources, but they are not suited to every task.

They fail when factors other than profit ought to be considered.

We therefore need to think about the design of regulatory systems more holistically, as part of a broader social process.

The pioneers of responsive regulation certainly understood this. They

emphasised flexibility, taking into account context, culture and

history.

What those three things now tell us, given widespread regulatory failure across industries, is that government should not resist stepping in to provide important public services where the private sector cannot or will not do so at an acceptable level. Nor should it be afraid to act through empowered regulators, with ressources and powers to fulfil their mandates.

Author: Author: Benedict Sheehy, Associate professor, University of Canberra