New Zealand’s financial system remains sound and the risks facing the system have reduced in the past six months, Reserve Bank Governor Graeme Wheeler said today when releasing the Bank’s May Financial Stability Report.

“The outlook for the global economy has been improving but global political and policy uncertainty remains elevated and debt burdens are high in a number of countries. A sharp reversal in risk sentiment could lead to higher funding costs for New Zealand banks and an increase in domestic borrowing costs. New Zealand’s banks are vulnerable to these risks because of their increasing reliance on offshore funding for credit growth,” Mr Wheeler said.

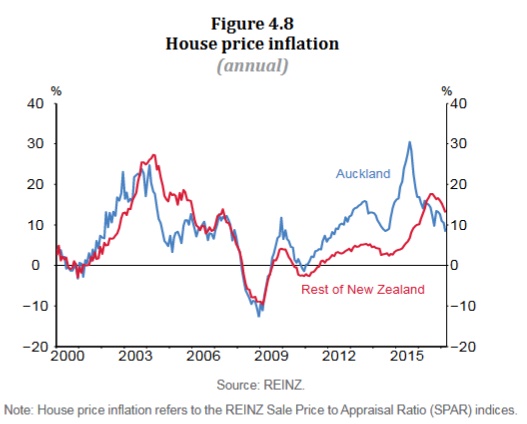

“House price growth has slowed in the past eight months, in response to tighter loan-to-value ratio (LVR) restrictions, and a more general tightening in credit and affordability pressures in parts of the country.

While residential building activity has continued to increase, the rate of house building remains insufficient to meet rapid population growth and the existing housing shortage. House prices remain elevated relative to incomes and rents, and any resurgence would be of concern.

“Dairy prices have recovered significantly in the past 12 months, and the majority of dairy farms are likely to have returned to profitability in the 2016/17 season. However, parts of the dairy sector are carrying excessive debt burdens, and remain vulnerable to a fall in income or an increase in costs. Banks should continue to closely monitor and maintain full provisioning against lending to high risk farms,” he said.

Deputy Governor Grant Spencer said “The banking system maintains strong capital and funding buffers, and profitability remains robust. The banking system appears to be operating efficiently when compared with other OECD countries, based on metrics such as cost-to-income ratios, non-performing loans and interest rate spreads.

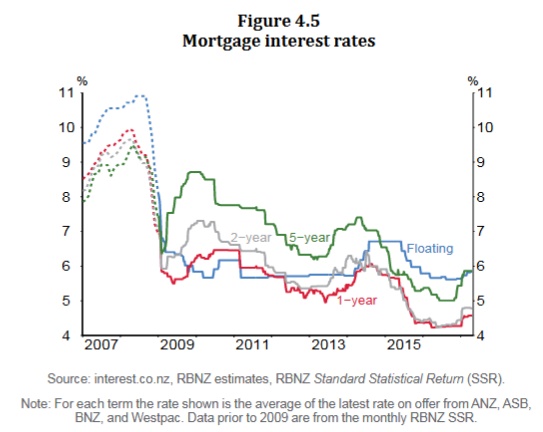

“Banks have generally tightened credit conditions in light of funding constraints and the increasing risks around housing. Banks are seeking to reduce their reliance on offshore funding and have raised deposit rates.

The Reserve Bank supports a cautious approach to managing foreign debt, in light of lessons learned in the GFC.

“While the LVR restrictions have increased the banks’ resilience to any fall in house prices, a significant share of housing loans are being made at high debt-to-income (DTI) ratios.

Such borrowers tend to be more vulnerable to any increase in interest rates or declines in income. There is evidence that borrowers with high DTI ratios are the most vulnerable to rising mortgage rates. At a mortgage rate of 7 percent, around half of existing borrowers with DTI ratios above 5 are expected to face severe stress. However, this represents just 3 percent of borrowers.

Overall, this analysis suggests that a significant proportion of New Zealand borrowers are vulnerable to a material increase in mortgage rates. A sharp and unexpected rise in mortgage rates could see the most vulnerable households default, sell their houses or reduce consumption to repay debt. Recent borrowers in Auckland and borrowers with high DTI ratios appear most vulnerable, signalling that a continued high share of lending at high DTI ratios is concerning and may present a risk to the housing market and financial stability.

The Reserve Bank will soon release a consultation paper proposing the addition of DTI restrictions to our macro-prudential toolkit.

“The Reserve Bank is making progress on a number of other initiatives. A review of bank capital requirements is underway and we recently released an issues paper on the intended scope of the review. We recently concluded a review of the outsourcing policy for registered banks, and the Bank and other agencies are assessing the recommendations from the International Monetary Fund’s recent (FSAP) review of New Zealand’s financial system.”