The NZ Reserve Bank today reduced the Official Cash Rate (OCR) by 25 basis points to 2.25 percent.

The outlook for global growth has deteriorated since the December Monetary Policy Statement, due to weaker growth in China and other emerging markets, and slower growth in Europe. This is despite extraordinary monetary accommodation, and further declines in interest rates in several countries. Financial market volatility has increased, reflected in higher credit spreads. Commodity prices remain low.

Domestically, the dairy sector faces difficult challenges, but domestic growth is expected to be supported by strong inward migration, tourism, a pipeline of construction activity and accommodative monetary policy.

The trade-weighted exchange rate is more than 4 percent higher than projected in December, and a decline would be appropriate given the weakness in export prices.

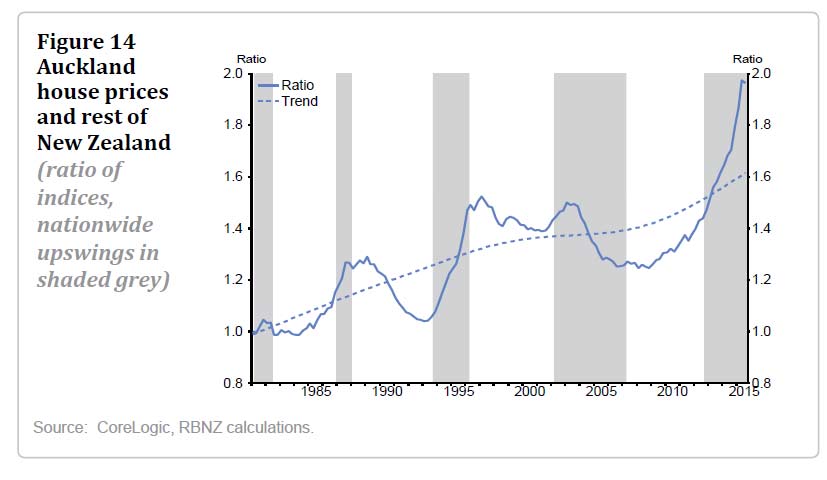

House price inflation in Auckland has moderated in recent months, but house prices remain at high levels and additional housing supply is needed. Housing market pressures have been building in some other regions.

There are many risks to the outlook. Internationally, these are to the downside and relate to the prospects for global growth, particularly around China, and the outlook for global financial markets. The main domestic risks relate to weakness in the dairy sector, the decline in inflation expectations, the possibility of continued high net immigration, and pressures in the housing market.

Headline inflation remains low, mostly due to continued falls in prices for fuel and other imports. Annual core inflation, which excludes the effects of transitory price movements, is higher, at 1.6 percent.

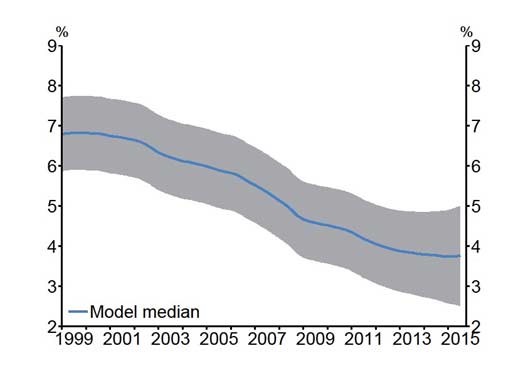

While long-run inflation expectations are well-anchored at 2 percent, there has been a material decline in a range of inflation expectations measures. This is a concern because it increases the risk that the decline in expectations becomes self-fulfilling and subdues future inflation outcomes.

Headline inflation is expected to move higher over 2016, but take longer to reach the target range. Monetary policy will continue to be accommodative. Further policy easing may be required to ensure that future average inflation settles near the middle of the target range. We will continue to watch closely the emerging flow of economic data