ASIC’s decision to update RG 209 followed a

number of developments since the guidance was last updated in late

2014. These developments have included:

ASIC regulatory and enforcement actions, including court decisions

ASIC thematic reviews on various parts of the industry such as interest-only loans

the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

recent and upcoming initiatives such as comprehensive credit reporting and open banking, and

changes in technology.

Following an extensive consultation, ASIC

has updated Regulatory Guide 209 (RG 209) to provide greater clarity and

support to lenders and brokers in meeting their obligations.

Importantly, ASIC has maintained principles-based guidance that supports

flexibility for licensees.

The changes include:

A stronger focus on the legislative purpose of the obligations—to reduce the incidence of consumers being encouraged to take on unsuitable levels of credit, and ensure licensees obtain sufficient reliable and up-to-date information about the consumer’s financial situation, requirements and objectives to enable them to assess whether a particular loan is unsuitable for the particular consumer.

More guidance to illustrate where a licensee might undertake more, or less, detailed inquiries and verification steps based on different consumer circumstances and the type of credit that is being sought. The updated guidance includes new examples about a range of different credit products including large and longer-term loans, credit cards and personal loans, small amount loans and consumer leases and different kind of consumer circumstances – such as first home buyers, existing customers, strata corporations, high net worth and financially experienced consumers.

More detailed guidance about how spending reductions may be considered as part of the licensee’s consideration of the consumer’s financial situation, requirements and objectives.

More detailed guidance about the use of benchmarks as a way to check the plausibility of expenses, as well as additional guidance about the HEM benchmark.

Clarity about more complex situations for some consumers – for example the different situations of consumers such as income from small business, casual employees, new employees, the gig economy, as well as joint and split liabilities and expenses.

ASIC has also included a section on the

scope of responsible lending, explaining the areas that are not subject

to responsible lending obligations – such as small business lending

irrespective of the nature of the security used for the loan.

The National Credit Laws provide consumers

with important protections when seeking credit directly from a lender

or through a broker. ASIC’s revised guidance is intended to assist

lenders and brokers to comply with their responsible lending obligations

and ensure that they do not recommend or provide credit that is

unsuitable.

ASIC Commissioner Sean Hughes said “ASIC

conducted extensive consultation on this important issue. The public

hearings and submissions highlighted the areas where industry sought

clarification from ASIC. We have listened carefully to all stakeholders

and addressed areas where we consider updated guidance would help. We

hope that today’s guidance will assist industry to more confidently make

responsible lending decisions and to facilitate good lending outcomes

for consumers.”

The guidance has also been updated to

reflect technological developments including open banking and digital

data capture services. RG 209 notes the cost and ease of access to

transaction information will be improved over time, which should improve

lenders’ overall view of a consumer’s financial situation.

ASIC has also published its response to

submissions made to Consultation Paper 309 and a tool to assist users of

RG 209 to navigate the updated structure of the document.

Today I would like to address some of the issues that have been

raised in relation to responsible lending and demonstrate two facts.

First, that the concerns are misplaced. Second, the principles

underpinning these provisions remain sound, even in the changed economic

environment since 2010.

At the outset I want to emphasise that our guidance is just and only that,

guidance. It does not have the force of law. The fact that we are

updating our guidelines, does not change the law, which has been in

place since 2010. However, what has been made abundantly clear to us in

the course of our consultations, is that industry would welcome more

assistance in interpreting how to meet responsible lending obligations.

Put simply, this is what we are endeavouring to achieve. We are not, and

never have sought to impede the flow of credit to the real economy.

I want to take this opportunity to reflect upon three broad questions

that keep recurring in the work we are doing to update our guidance:

Why does responsible lending matter?

Why is ASIC updating its guidance, and why now?

What does an update to the guidance mean in practice for lenders and what will it achieve?

And importantly, along the way I will respond to some misconceptions

about responsible lending. There are some myths that need busting to

address exaggerated and inaccurate criticisms about our consultation on

revising this guidance.

Why does responsible lending matter?

Responsible lending is fundamentally about the credit industry’s

commitment to dealing fairly with its customers. Ensuring robust and

balanced standards of responsible lending to consumers has been, and

will continue to be, a key priority for ASIC.

Consumer credit is part of the life blood of our society and economy. A report by Equifax Australia in July 2019 estimated that 4.4million applications for consumer credit were expected to be made in the 6 months to the end of the year[1].

Inappropriate lending can have devastating consequences for

individuals and families, and on a broader scale, can undermine

confidence in financial markets.

Australia introduced a national consumer credit regime in 2009 to

avoid excesses in lending and predatory lending to consumers. In the

preceding period, the impact of the financial crisis had revealed a

number of shortcomings in policies and practices at financial

institutions abroad. Some of these practices were clearly aimed at

taking advantage of vulnerable borrowers.

Although lending standards in Australia were not as lax as other

countries, during the pre-crisis period the share of ‘low doc’ loans

written in Australia had grown strongly in the lead up to the crisis[2].

The responsible lending law reforms were introduced to Parliament to

curb undesirable market practices that many were concerned about at the

time, including[3]:

providing or recommending inappropriate, high cost and potentially unaffordable credit;

upselling of loans to higher amounts than were necessary to fulfil the consumer’s needs;

unscrupulous lenders providing consumers with unaffordable loans

that will default – thus facilitating the recovery of the equity in the

consumer’s home; and

inadequate financial disclosure, poor responses to financial difficulty and unsolicited credit limit increases.

The core principle behind this regime is simple and has not changed

since 2010 – despite what many critics and commentators have been

saying. A licensee must not enter into, or suggest or assist a customer

to enter into, a contract that is unsuitable. None of this is new. To

ensure this outcome the licensee must:

First – gather reliable information that will inform the licensee

about what the consumer wants and their financial situation. This

involves making reasonable inquiries about the consumer’s requirements

and objectives in relation to the credit product, and the consumer’s

financial situation, and taking reasonable steps to verify the

consumer’s financial situation.

And then, second – assess whether the contract will be ‘not unsuitable’ for the consumer.

Why is ASIC updating its guidance on responsible lending and why are we doing it now?

Since the introduction of the responsible lending laws, ASIC has

regularly reviewed industry practices and identified a range of

compliance issues. Some examples of our work include:

In 2015 we reviewed industry’s approach to providing interest-only

home loans. We identified practices that could result in borrowers being

unable to afford their loan repayments down the track, and we suggested

to lenders that they needed more robust processes to improve the

accuracy of their assessments regarding capacity to repay.

This was followed in 2016 by our review of large mortgage broker

businesses. This review resulted in ASIC setting out further actions

which credit licensees could take to reduce the risk of being unable to

demonstrate compliance with their obligations.

Alongside our industry reviews, we’ve undertaken a number of

enforcement actions to improve compliance. Our actions against The Cash

Store, Bank of Queensland, BMW Finance, Channic, Motor Finance Wizard,

ANZ (Esanda), and Thorn Australia send a clear message to industry and

consumers that ASIC will take action to stamp out irresponsible and

predatory lending, and deter breaches of the law.

More recently, the Royal Commission into the financial services

sector found some major shortcomings in the way in which responsible

lending laws were being applied by lenders.

At this point, I should say something briefly about the decision in

the proceedings that ASIC took against Westpac in 2017 – the so-called

‘Wagyu and Shiraz’ case. This preceded the Royal Commission, and

Commissioner Hayne did not directly address ASIC’s case against Westpac.

ASIC was unsuccessful in this matter and while we respect the judgment,

we have lodged an appeal.[4]

Almost every commentator has criticised this decision and suggested

that ASIC’s appeal creates avoidable uncertainty. Our objective in

appealing this decision is, in fact, to clarify the application of the

law. And we believe that doing so is in the best interests of both

consumers and lenders. It is an important part of ASIC’s mandate to

clarify the law where there is uncertainty, and thereby support and

guide industry to understand their obligations.

We decided to appeal because we consider that the decision creates

uncertainty about what a lender is required to do to comply with its

obligation to make an assessment of whether a loan is not unsuitable for

the borrower. And, if the judgment is to be understood as standing for

the proposition that a lender may do what it wants in the assessment

process (as His Honour found), then we consider that to be inconsistent

with the legislative intention of the responsible lending regime. The

Westpac case relates to the period between December 2011 and March 2015,

and although in the years since we have seen some improvements in

responsible lending standards amongst the industry, there is a real risk

that uncertainty in the approach required by lenders to comply with the

law could result in slippage by some lenders.

Put simply, we believe that the judgment left it too unclear what

steps are required of a lender. We are seeking clarity by appealing.

The proper forum to debate this is now the Full Federal Court. Like any

other litigant, we are availing ourselves of access to an appellate

body. We should not be criticised for accessing the Courts to resolve a

dispute, as all regulators do from time to time.

Notwithstanding our appeal in the Westpac case, we consider that ASIC

should still provide updated guidance mindful that the appeal has not

yet been heard. All of the ingredients necessary are there – judicial

decisions, ASIC enforcement action, thematic reviews, the Royal

Commission, changes to technology. The updated RG209 looks to build on

the existing guidance, which we believe is fundamentally sound, and to

bring those developments together in a single, instructive guide and to

clarify and provide more certainty to industry in key areas where we

can.

Some misconceptions about responsible lending

There are a number of myths and exaggerated claims about the supposed

effects of the responsible lending laws that need to be addressed.

These claimed effects are either not supported by the facts or data, or,

if they are real, they are the result of a fundamental misunderstanding

and misapplication of the law.

Let me address a few of the most significant.

The first is the suggestion that small business lending is negatively affected by the responsible lending obligations.

There has been a lot of misinformation published recently in the

media and in the current corporate reporting season about the effect of

the responsible lending requirements on small business lending.

The responsible lending obligations administered by ASIC apply to credit provided to individuals for:

personal, domestic and household purposes (this includes buying/improving a home); and

residential investment purposes (this includes buying/improving/refinancing residential property for investment purposes).

They apply also to loans to strata corporations for these same

purposes. This is the one, very niche, area of application of the

responsible lending obligations to an entity rather than an

individual.

Otherwise, a loan to a company (including small proprietary companies) for any purpose is not subject to the responsible lending obligations.

Where there is a loan to an individual, the purpose of the loan

determines whether the loan is subject to the responsible lending

obligations. The nature of any security for the loan does not affect

this test, nor does the source of income to pay the loan back. In other

words, it is not an asset test but a predominant purpose test.

A loan to an individual predominantly for a business purpose is not

subject to responsible lending obligations. ‘Predominant’ simply means

‘more than half’.

So, if someone borrows $500,000 of which $300,000 is to be used to

establish a small business, and the remainder for making home

improvements, the loan is not subject to the responsible lending

obligations.

Similarly, if a small business operator obtains a loan to purchase a

motor vehicle which is to be used 60% of the time for work purposes but

will also be available for personal use, the loan is not subject to the

responsible lending obligations.

A loan to an individual for business purposes secured over a borrower’s home is not subject to the responsible lending obligations.

Of course, a lender may choose to apply its responsible lending

processes to business loans for its own commercial reasons to manage its

credit risk portfolio or to meet its prudential obligations.

AFCA in its role as the dispute resolution scheme for the credit

industry deals with both small business loans and consumer loans. There

has been some confusion in industry about whether the responsible

lending obligations are going to be applied by AFCA in relation to small

business loans. In evidence at ASIC’s public hearings in August this

year, AFCA undertook to clarify this misunderstanding in its forthcoming

guidance to its members.

There has also been a suggestion that ASIC’s guidance and

consultation has caused increases to credit application processing times

or rejection rates.

Contrary to some anecdotal statements, the evidence and data do not

point to ASIC’s guidance in RG 209 or our consultation to revise this

guidance, as having caused increases in credit application processing

times or rejection rates.

We do accept that, following the commencement of the Royal

Commission, lenders began to review their approach to responsible

lending and to tighten standards. And that these reviews, prompted by

the Royal Commission and not by ASIC’s guidance (which,

remember, has been unchanged since November 2014), have resulted in

them seeking more detailed information from borrowers and necessitated

some systems upgrades and staff training.

To the extent this had any effect on processing times, it was only at

the margins. In coming to that conclusion, we have actively sought

information about processing times.

The Australian Banking Association (ABA) recently disclosed

information to ASIC that shows, on average, approvals for mortgage loans

for ABA members in late 2018 took 4 days longer than they had in early

2018, but that by mid-2019 this had decreased to be just 2 days longer.

During ASIC’s recent public hearings in August, we asked some of the

major banks and other lenders about changes to loan application times

and rejection rates:

one bank confirmed it has not experienced material changes and approved between 80-85% of applications; and

two banks attributed any changes they have experienced to changes in demand for credit and changes in the bank’s own processes.

And, illustrative of the fact that adherence to responsible lending

laws does not have to spell lengthy processing times, Tic:Toc (a smaller

on-line lender) told us that their fastest time from a consumer

starting an application to being fully approved is 58 minutes. And that

includes full digital financial validation of the consumer’s financial

position.

The ABA has not indicated any direct impact by ASIC on ABA members’

processing times. The reasons given for an increase in approval times

instead included:

a new APRA reporting framework (inspection of record keeping);

an APRA review leading to internal changes to processes and procedures;

satisfying new risk limits imposed on certain lending by APRA;

AFCA decisions influencing interpretation of regulatory requirements; and

reinterpretation by the ABA members of responsible lending requirements.

Anecdotally, we have also heard of instances where front-line lending

officers are seeking to escalate loan approval decisions to their

managers, which may also have added to perceived delays.

Finally, there has been a suggestion that responsible lending has had a negative effect on economic growth.

We do not accept this. The evidence and data available to ASIC do not

suggest that the decision to update our guidance has contributed to the

current state of the economy by limiting access to credit.

Indeed, lending trend reports published by the ABA show that banks

are still lending – approval rates remain between 85-90% for home

lending and 90-95% for business lending (the latter of course should not

be captured by our guidance on the responsible lending obligations).

Instead, the main reason for slower credit growth has been a decline

in the demand for credit. Statements made during ASIC’s public hearings,

other information we have collected from industry, and recently

published economic statistics all support this view.

And, in fact, there are signs that this may be turning around.

The Australian Bureau of Statistics reported that (in seasonally

adjusted terms) lending commitments to households rose 3.2% in August

2019, following a 4.3% rise in July. Earlier this week, CBA announced a

3.5% increase in home lending and 2.8% in business lending for the 3

months to October.

This pick-up in recent approvals lends further support to the view

that it is not responsible lending obligations that have been dampening

credit availability. So too do the following sources:

The Reserve Bank of Australia (RBA) continues to comment on the

impact on credit of the construction cycle and of reduced demand for new

housing. The RBA found that housing turnover had declined to

historically low levels (below 4%) and has only just begun to rise.

The ABA lending trend report states that a significant shift in

market sentiment within the housing sector – following the election

outcome, RBA cash rate cut, and lowering of APRA’s serviceability floor –

is likely to be a key driver of a boost in investor loan applications.

In addition, the RBA’s recent Financial Stability Review explained

that uncertainty about the outlook for global economic growth has

increased in the last 6 months, with a greater chance of weak growth.

The Review refers to regulatory measures introduced in December 2014 and

in early 2017 (being the prudential measures put in place) as a ‘speed

bump’ for investment lending and interest-only lending. The Review also

refers to ‘tighter standards’ implemented by lenders, relating to their

own credit risk appetite and policies – these are adopted by banks to

manage their own credit risk exposure, rather than for the purpose of

complying with responsible lending obligations. And, finally, the Review

points to an increase of credit approvals in recent months which the

RBA expects to flow through to higher lending.

What does an update to the guidance mean and what will it achieve?

Our Regulatory Guides are intended to be useful and informative

documents and there has been a great deal of anticipation about the

upcoming revision. There are a few key points I would like to make about

what an update to our guidance means and will achieve.

First – our regulatory guidance was last updated in November 2014,

and the responsible lending obligations themselves have not materially

changed since 2010. For a topic like responsible lending, where the

application of the law continues to be clarified through court

decisions, and where the industry’s technologies and systems evolve and

change, it is appropriate to conduct periodic reviews and updates of our

guidance.

Second – the consultation process has involved multiple steps. We

allowed three months to receive submissions, in order to get thoughtful

and broad feedback. We exercised our power to conduct public hearings –

for the first time in more than 15 years. This proved to be a very

useful and respectful forum to talk to industry participants about their

views. We have also recently concluded a group of round-table sessions

with stakeholders including ADIs, non-bank lenders, brokers, providers

of small amount credit contracts and consumer leases, and consumer

representative groups. This enabled us to test and distil the

conclusions we were drawing on necessary changes.

Third – it is critical everyone is clear that our guidance does not,

and the revised guidance will not, create new obligations. Simply

because it cannot do that. Our regulatory guides are just that – guidance – about approaches that licensees can adopt to reduce the risk that they fail to comply with the responsible lending laws.

Fourth – The submissions were wide ranging, but many made the point

that they were looking for more guidance not less, albeit while

retaining flexibility to exercise judgments in implementing responsible

lending practices.

We made it very clear in the consultation paper that we wanted to update and clarify our existing guidance and provide additional guidance.

When we release the updated regulatory guide in a few weeks, I urge

licensees to take the guidance on board and to compete with each other

on the quality of products and services to consumers. Not focus on

processes which merely seek to achieve a minimum level of compliance.

Conclusion

In conclusion, I hope that I have given context for what we are doing

and why, and busted some myths about the practical effects of

responsible lending.

We all have a role to play to ensure that both consumers and

investors can continue to have confidence in the efficient and fair

operation of our credit markets. As the leaders and responsible managers

of our credit institutions, it falls to you to implement processes that

ensure consumers are provided with products that are affordable for

them and suit their needs.

We intend for our update to Regulatory Guide 209 to provide greater

clarity to industry. All the same, there is little doubt that we will

continue to be engaged in conversation with industry about responsible

lending.

A former Macquarie banker says hazy guidelines around lending will cause problems for the next six months following the Westpac case, predicting the big four banks will corner ASIC and demand clearer standards, according to an exclusive in InvestorDaily today.

During

a panel discussion at The REAL Future of Advice Conference in Vietnam

this week, former Macquarie head of sales and distribution for

mortgages, Tim Brown, noted the recent Federal Court decision ruling in

the favour of Westpac.

ASIC

had taken Westpac to court over allegations it breached lending laws

between 2011 and 2015 by using the household expenditure measure to

estimate potential borrowers’ living expenses.

ASIC had argued the benchmark was too frugal and that customers’ expenses were higher.

Mr

Brown, who is currently the chief executive of Ezifin Financial

Services, called the current lending landscape a “minefield” where

lenders “can’t get clarification from ASIC” over standards for

evaluating consumers’ eligibility for mortgages.

“I

think the problem with this whole expense discussion, as I was pointed

out earlier on is that a lot of the assessors put their own personal

assessment on what someone else spends money on, which is where the

problem lies,” Mr Brown said.

“It needs to be much more factual.

“I

think it is going to be a problem for at least another six months until

some of the banks get together with ASIC and say look we need to get

some clear guidelines around this. Because they’re basically saying HEM

isn’t acceptable anymore.”

Mr

Brown noted when he first started lending, brokers would sit with

clients, go through their expenses and make sure they had enough

capacity to meet any future increases and interest rates, by using HEM

and allowing up to two and a half per cent above the current rate.

Reflecting on his expenses when buying his first house, said he did not think he would have passed current standards.

“But

within the first six months of buying a home, and we know this

factually and we’ve recently seen ASIC having these discussions, that

most people will reduce their discretionary spending by 20 per cent.

“Now,

most assessors in the past could make that decision without any

concern. But in the current environment, they are afraid to make those

decisions now because there’s a way around it and ASIC might review

that. And this comes back to this personal assessment of someone else’s

opinion on what someone should have a discretionary not a discretion.

“Because

ASIC just goes ‘well you know best endeavors, you know, whatever you

think is reasonable.’ And then they’ll charge you if they don’t think

it’s reasonable.”

‘We want some direction’

Talking

about missing clarity from ASIC, Mr Brown said: “The banks are sick of

this game that they’re playing with ASIC at the moment and eventually

the four of them will get together and say look, you need to give us

some clear guidelines.”

“At

the moment, I think the industry bodies are trying to come together

with something they can take to ASIC both from a vendor’s perspective

and also from a MFAA (Mortgage and Finance Association of Australia) and

FBAA (Finance Brokers Association of Australia).”

Mr Brown noted every time he had been on a panel, he had been asked about the Westpac decision.

“There’s obviously a real concern among the number of people at the moment,” he said.

ASIC has commenced proceedings in the Federal Court against National Australia Bank (NAB) for breaches of the law arising from failures with its Introducer Program.

ASIC alleges that between 3 September 2013 and 29 July 2016, NAB

accepted information and documents in support of consumer loan

applications from third party introducers who were not licensed to

engage in credit activity.

As a result, ASIC alleges NAB breached s31(1) of the National Consumer Credit Protection Act 2009 (National Credit Act)

which prohibits credit licensees from conducting business with parties

engaging in credit activity without an Australian credit licence (ACL).

ASIC also alleges that NAB breached its obligations under s47 of the

National Credit Act requiring it to engage in credit activities

efficiently, honestly and fairly and to comply with the Act.

The proceedings relate to the conduct of 16 bankers accepting loan

information and documentation from 25 unlicensed introducers in relation

to 297 loans.

One of the key objectives of the National Credit Act’s licensing

regime is consumer protection. The imposition of a licensing regime was

intended to address concerns that third-party referrers (including

brokers and introducers) may misrepresent consumers’ financial details

to ensure loans are approved, and their commissions are paid, in

circumstances where the consumers’ true financial position means that

the loan should not be made.

ASIC is asking the Court to find that NAB breached the National

Credit Act and to impose a civil penalty on NAB for doing so. The

maximum penalty for one breach of s31(1) of the National Credit Act,

during the time of contravention, was 10,000 penalty units, or $1.7 to

$1.8 million.

The proceeding will be listed for directions on a date to be determined by the Court.

Background

Since at least 2000, NAB operated the credit industry’s largest

referral program, known as the ‘Introducer Program’, whereby a

third-party introducer could ‘spot and refer’ a potential customer to

NAB in exchange for commission if the customer entered into a loan with

NAB. Between 2013 to 2016, NAB’s Introducer Program generated $24

billion dollars’ worth of loans.

Introducers referring customers through the Introducer Program were

only to provide NAB with the potential customer’s name and contact

details. In order for an introducer to provide NAB with further

information or documents, the law required that the introducer be

authorised under an ACL.

ASIC’s investigation uncovered that NAB bankers overstepped the ‘spot

and refer’ requirement by accepting information and documentation from

the 25 unlicensed introducers, including completed home loan

applications, payslips, copies of customer identification documents and

more. This behaviour can pose a serious risk to consumers, as ASIC also

identified that in some instances the documents provided to NAB by the

unlicensed introducers were false.

During the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry, NAB identified that

misconduct in their Introducer Program went undetected until 2015 for

reasons including:

no head of the Introducer Program, with a General Manager only being appointed in October 2016

a lack of systems to monitor or review introducers, and

controls over the Introducer Program relied heavily on bankers.

the misconduct identified in the present proceedings

the misconduct that was the subject of ASIC’s administrative action

against former NAB Branch Manager Rabih Awad; and the misconduct that

was the subject of ASIC’s administrative action against former NAB

Branch Manager Rabih Awad (18-211MR), and

the misconduct identified in ASIC’s criminal prosecution and

administration action against former NAB Branch Manager Mathew Alwan (19-216MR).

In July 2018, ASIC banned Mr Awad (who is one of the 16 bankers

identified in the present proceedings) from engaging in credit

activities and providing financial services for a period of seven years.

Mr Awad was found to have given NAB false payslips, letters of

employment, and entered false referee contact details in NAB’s lending

systems in multiple home loan applications. A majority of the false

documentation submitted to NAB by Mr Awad was provided to him by a real

estate agent who was previously registered as a NAB Introducer.

On 20 August 2019, Mr Alwan (who is not one of the 16 bankers

identified in these proceedings) pleaded guilty to one count of

‘intention to defraud by false or misleading statement’, an offence

under the NSW Crimes Act. The charge relates to Mr Alwan’s conduct in

relation to 24 home loan applications which he falsely told NAB were

referred by his uncle’s business ‘Suit Club’, a registered NAB

Introducer. This resulted in NAB paying Suit Club $56,955 worth of

commission. In October 2018, ASIC permanently banned Mr Alwan from

engaging in credit activities and providing financial services for the

same misconduct.

On 25 March 2019, NAB announced that it will be terminating the Introducer Program on 1 October 2019.

Last week the Judge delivered his verdict in the ASIC-Westpac HEM case, essentially because of the ~260,000 loans examined in the case less than 5,000 would have potentially had their loans tweaked lower if the HEM was not used, whereas the bulk of the loans would have been bigger if HEM was not utilised in the decisioning.

I have now had the chance to speak to a number of industry

players, and most have fallen into expected camps. Lenders in the main welcome

the decision, suggesting that common sense has prevailed, and that ASIC was not

reasonable in its interpretation of responsible lending guidelines. On the

other side, consumer advocates are calling for tighter controls and suggesting

that the HEM benchmarks, even in their revised form are too low – meaning that

households are committed to servicing loans they cannot afford. And ASIC has

commenced a review of responsible lending by years end.

But among my conversations on this topic, I found a sensible and balance view expressed by Fintech CEO Mark Jones from SocietyOne. They of course are on the cutting edge of technological innovation through their lending processes in Australia.

Mark made the point that recently lenders have been raising

their standards, but the question becomes whether a lender has to try and

uncover untruthful declarations from prospective borrowers. In Australia there

is no clear-cut legal obligation of borrowers to be honest and transparent in

their declarations, whereas in the USA there is such a legal obligation, and in

New Zealand a Code of Conduct.

He cited examples where applicants had clearly lied on loan

application forms.

What is the right balance between asking in painful detail

for information from applicants, some of which are unsure of their specific

spending patterns, and the fact that in any case if they take a loan, they may

be capable of “life-style modification”?

So, he sees HEM in the context of the broader loan

assessment processes, with data from applications tested again HEM, and

additional dialogue around other unusual commitments which might include school

fees, alimony, and other elements. This

is all around knowing your customer. And

there needs to be a focus on both discretionary and non-discretionary categories

to give a complete picture.

The systems which Fintech’s like SocietyOne use are more sophisticated and can handle the complex algorithms which reflect real life. Positive credit and now Open Banking, both of which are arriving, are helpful in uncovering critical information. As a result, there are better outcomes for customers. No lenders want to make a loan which is designed to fail! And it opens the door to more sophistication around risk-based pricing

So, in summary, the trick is to get the right balance between getting every scrap of potential data from a customer, thus getting bogged down in the detail but missing the big picture; and applying simplistic ratios which do not provide sufficient precision to spot good and bad business. And it is this balance which needs to be defined in responsible lending, to a level which passes both community expectations and the operational requirements of lenders. To that end, the debate should not really be about HEM at all!

The big four bank has told ASIC to consider the utility of the broker channel before proposing bespoke responsible lending obligations, adding that it has not identified a notable difference in the quality of loans originated by the channel. Via The Adviser.

In

February, the Australian Securities and Investments Commission (ASIC)

launched a review to update its responsible lending guidance (RG 209),

which has been in place since 2010.

ASIC opened consultation by

inviting submissions from stakeholders within the financial services

sector and has since commenced a second round of consultation in the

form of public hearings, in which stakeholders that provided submissions

have been called to provide further guidance.

Appearing before

ASIC during its first round of public hearings, Westpac’s general

manager of home ownership, Will Ranken, was asked to provide an

assessment of the quality of mortgages originated through the broker

channel.

Mr Ranken noted that the bank’s verification requirements

for loans originated via the proprietary channel are the same for those

originated by brokers but acknowledged that broker-originated loans

require an “extra layer of oversight and governance”.

“When a

customer chooses to go to a broker, we’re one step removed, so there’s

another layer of oversight and governance on the broker channel,” he

said.

However, the Westpac representative stated that the bank has

not observed substantive differences in the quality and characteristics

of home loans originated by the third-party channel.

“If

you look at performance, particularly the metric around 90-day

delinquencies, they’re largely the same with our proprietary channel –

there’s no meaningful difference between those channels,” Mr Ranken

said.

“In terms of the tenure of loans, I think on average it’s

measured in months rather than quarters. In terms of the difference [in

the average tenure of the loans], it’s one or two [months].

“In terms of the size of a loan, if you look at averages, and averages can be a bit misleading, the average size of a loan through the broker channel is a little bit larger. That’s probably more for smaller loan sizes, customers are happier to deal with a branch, but for larger complex lending requirements, there’s a greater propensity for customers to go to a broker.”

Mr

Ranken was then asked if Westpac would support a move by ASIC to

prescribe different responsible lending obligations depending on how a

loan is originated.

In response, Mr Ranken warned that ASIC should

consider the effect of such changes on the value proposition of the

broker channel.

“I would say on providing additional guidance on

one particular channel over another, it would be important to take into

account the very valuable contribution that brokers do make to the

overall market,” he said.

“Specifically, I talk to the level of

competition that they facilitate in the market, either through providing

independence and access to a multitude of lenders, as well as the

service they give to customers in terms of assisting them with complex

needs.

“To the extent that guidance may require additional steps

either on the lender or the broker themselves, we just want to balance

that with ensuring that it maintains a viable and dynamic broker

channel.”

When pressed on the question, Mr Ranken added: “We’re comfortable with the policies and procedures that we’ve got in place around the broker channel, so it’s hard to comment on guidance… The devil’s in the detail. It really depends on what the detail of the guidance would be.”

Other stakeholders, however, including consumer group CHOICE, have called on ASIC to enshrine specific broker obligations in its RG 209 guidance.

CHOICE

pointed to research from ASIC’s review of interest-only home loans in

2016, which reported that mortgage broking record-keeping from

verification enquiries was “inconsistent” and, in some

cases, “fragmented and incomplete”.

Despite recent reforms from the Combined Industry Forum, which restricted the payment of commission to the loan amount drawn down by a borrower, the consumer group alleged that the supposed lack of record-keeping was “particularly harmful for consumers” because “brokers are currently incentivised to sell loans that will provide them with the largest commission”.

ASIC’s first

round of public hearings concluded, with the second round of hearings to

commence in Melbourne on Monday, 19 August.

The regulator is expected to publish its new guidance before the end of the calendar year.

In a keynote address by ASIC Chair, James Shipton at Committee for Economic Development of Australia (CEDA) event in Melbourne yesterday, it appears the regulator will hold public hearings about responsible lending practices.

He said that ASIC was updating its responsible lending guidance, and as part of its consultation, public hearings would be held to “robustly test some of the issues and views that have been raised in submissions”.

This is a follow-up to ASIC’s consultation paper on updating its guidance on responsible lending, which was issued in mid-February 2019.

Interestingly, ASIC has discretion as to whether such hearings would take place privately or publicly. However the regulator is required to have regard to whether it is in the public interest for a hearing to take place in public.

In addition, ASIC also has power to summon witnesses and require the production of documents for the purposes of a public hearing. It may also refer to a court any questions of law arising at a hearing.

To date ASIC has hardly used it hearings powers but is does appear they intend to utilise these as an aspect of its renewed approach to enforcement in the wake of the Hayne Royal Commission.

We are embedding and expanding new supervisory approaches and promoting best practice and innovation in regulation – particularly through our Close & Continuous Monitoring program (or CCM) and our corporate governance review that is aimed at improving governance practices at the board level.

We are also implementing new and existing reforms and working towards our new obligations and responsibilities in response to the Royal Commission. This includes an expanded role for ASIC to become the primary conduct regulator in superannuation.

ASIC is appealing last year’s landmark Federal Court decision, determinedto prove two Westpac subsidiaries provided personal financial advice despite not being licensed to do so, via Financial Standard.

In

December 2018, Justice Jacqueline Gleeson determined Westpac Securities

Administration Limited (WSAL) and BT Funds Management (BTFM) had

breached the Corporations Act in 2014, during two telephone campaigns in

which staff recommended the rollover of superannuation accounts to

Westpac/BT super products.

However,

the judge said ASIC failed to prove the phone calls constituted

personal financial advice. Under their respective AFSLs, WSAL and BTFM

are only licensed to provide general advice.

ASIC has now filed an

appeal of the decision, seeking greater clarity and certainty as to the

difference between general and personal advice for consumers and

financial services providers.

“The

dividing line between personal and general advice is one of the most

important provisions within the financial services laws. It directly

impacts the standard of advice received by consumers,” ASIC deputy chair

Daniel Crennan said.

“This is why ASIC brought this test case and

ASIC believes further consideration by the full court of the Federal

Court is necessary to better inform consumers and industry.”

The

case concerned 15 phone calls which the judge determined to be general

advice “because the callers did not consider one or more of the

objectives, financial situation and needs of the customers to whom the

advice was given.”

However, in 14 of the 15 calls, the law was

breached by the implication that the rollover of super funds into a BT

account was recommended. While not dishonest, the product advice was not

provided efficiently, honestly and fairly, the judge deemed.

The changes appear mainly clarifications and tweaks to language rather than substantive changes. But it does underscore the lenders obligations to make reasonable inquiries when making a loan. Nothing here that would open the credit taps, that I can see.

They are asking questions about credit which currently falls outside the guidelines, such as SACC and Business loans.

They do address HEM benchmarks saying that ” A benchmark figure does not provide any positive confirmation of what a particular consumer’s income and expenses actually are”. Its a plausibility test.

We propose to clarify our guidance in RG 209 on the use of benchmarks as follows:

(a) A benchmark figure does not provide any positive confirmation of what a particular consumer’s income and expenses actually are. However, we consider that benchmarks can be a useful tool to help determine whether information provided by the consumer is plausible (i.e. whether it is more or less likely to be true and able to be relied upon).

(b) If a benchmark figure is used to test expense information, licensees should generally take the following kinds of steps: (i) ensure that the benchmark figure that is being used is a realistic figure, that is adjusted for variables such as different income ranges, dependants and geographic location, and that is not merely reflective of ‘low budget’ spending; (ii) if the benchmark figure being referred to is more reflective of ‘low budget’ spending (such as the Household Expenditure Measure), apply a reasonable buffer amount that reflects the likelihood that many consumers would have a higher level of expenses; and (iii)periodically review the expense figures being relied upon across the licensee’s portfolio—if there is a high proportion of consumers recorded as having expenses that are at or near the benchmark figure, rather than demonstrating the kind of spread in expenses that is predicted by the methodology underlying the benchmark calculation, this may be an indication that the licensee’s inquiries are not being effective to elicit accurate information about the consumer’s expenses

This is the ASIC announcement:

ASIC’s guidance has been in place since 2010 when the responsible

lending laws were first introduced. Although the laws have not changed

since 2010, ASIC considers it timely to review and update the guidance

in light of its regulatory and enforcement work since 2011, changes in

technology, and the recent Final Report of the Royal Commission into

Misconduct in the Banking, Superannuation and Financial Services

Industry.

Our review of RG 209 will consider whether the guidance remains

effective and identify changes and additions to the guidance that may

help holders of an Australian credit licence to understand ASIC’s

expectations for complying with the responsible lending obligations.

ASIC welcomes submissions on the update of our guidance on

responsible lending from any interested party. In the consultation paper

we have asked a series of questions about specific matters. We are also

keen to hear from stakeholders about any other issues considered

important that are not dealt with in the consultation paper.

ASIC is also considering whether to provide an opportunity for key

stakeholders to speak to the Commission at public hearings in addition

to making written submissions.

Further information about the consultation and its progress will be available on the ASIC website.

“The responsible lending obligations are an integral part of the

regulatory framework for all consumer loans” said ASIC Commissioner Sean

Hughes. “ASIC wants to ensure its guidance provides industry with

certainty, including as a result of emerging technology and initiatives

such as open banking and comprehensive credit reporting. We encourage

everybody to participate in this extensive consultation process”.

The consultation is open for a period of three months, with comments due by Monday 20 May 2019.

Background

Regulatory Guide 209 Credit licensing: Responsible lending conduct

(RG 209) contains ASIC’s guidance on responsible lending for consumer

credit. RG 209 was issued in 2010 and last revised in November 2014.

Since then there have been many matters that now mean it is timely for ASIC to update its guidance.

ASIC regulatory and enforcement actions, including court decisions,

ASIC thematic reviews on various parts of the industry such as interest-only loans,

the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry,

Recent and upcoming initiatives such as comprehensive credit reporting and open banking, and

Changes in technology.

ASIC has also received anecdotal feedback that licensees may be

applying the responsible lending obligations where the law does not

require them to be applied (e.g. in small business lending). We are

seeking feedback on whether there is a need to include some additional

guidance in RG 209 which sets out particular examples where the law does

not require responsible lending or related obligations to apply.

“Reserve Bank governor Philip Lowe is understood to have met with the big bank chiefs in recent weeks to caution them against an overzealous tightening of credit supply in response to lending rules and the Hayne royal commission”.

The RBA is of the view that lenders are turning good business away, and need to take risk on.

Some SME’s are getting caught in the cross fire, and its clear that business is finding it harder to get funding. This was covered in the RBA’s minutes, released yesterday.

Of course the responsible lending obligations have not changed, but now the meaning and obligations are front of mind. Thus banks need to examine income and expenses etc and cannot necessarily rely on HEM or mortgage brokers. So all this is in direct opposition to the RBA’s wishes, and we suspect the risk of legal action, or worse will continue to limit bank lending.

The ASIC Westpac case will be back before the courts in the new year, though as yet is not clear whether HEM will be tested in court, or whether its more about reaching a settlement. And the royal commission recommendations will be out in February

Is the RBA really condoning the bad behaviour and law breaking exposed in the past year?

And remember that currently mortgage lending is still running at more than 5% on an annualised basis, according to RBA data.

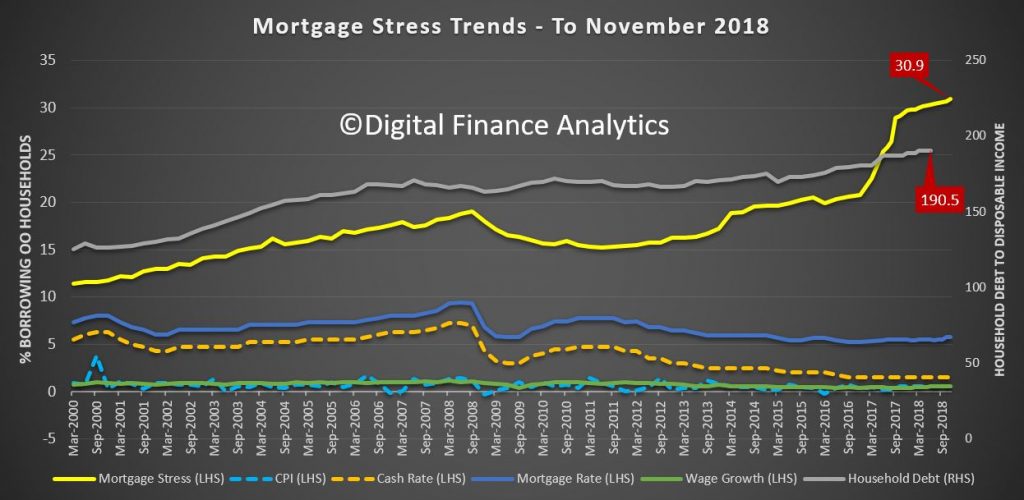

The fundamental problem is the RBA has been responsible for the growth of credit to the point where households in Australia are some of the most leveraged in the world, home prices have exploded and bank balance sheets have inflated. But all this “growth” is illusory. Mortgage stress continues to build and the wealth effect is reversing as home prices slide.

Thus, as we anticipated, we will see a number of “unnatural acts” by the RBA and the Government to try and stop the debt bomb from exploding, by trying to get credit to expand. But this is irresponsible behaviour, in the light of rising global interest rates, high market volatility and building systemic risks.