CBA cut interest rates by as much as 0.30% across its savings accounts yesterday, exemplifying the tactics many banks are using to help recoup the costs incurred from reducing home loan rates by the full 0.25% March cash rate reduction. Via Australian Broker.

Two weeks before the major’s home loan

reductions come into effect, the ongoing bonus rates on its Goal Saver

account have been reduced by 0.25%, its pensioner security account by up

to 0.25% and its Youth Saver account by 0.30%; the NetBank Saver

account was unchanged, with an ongoing rate of just 0.10%

“CBA is one of six banks so far to cut

deposit rates since last week’s cash rate cut, with dozens more expected

to follow,” said RateCity.com.au research director Sally Tindall.

“It’ll be interesting to see how far

Westpac, NAB and ANZ shave their rates, seeing as they’ve already taken

the knife to some of their savings rates this year.

“In this low rate environment, finding a

savings rates above inflation can feel like finding a needle in a

haystack, but they are out there.”

The highest rate currently on offer is 2.25%, which can be found at neobanks 86 400 and Xinja Bank.

However, they’re “unlikely to stick around”, according to Tindall.

Last week, Xinja announced no new Stash

savings accounts will be able to be opened for an indefinite period, in

order to take care of existing customers.

For now, the neobank will maintain its

2.25% rate, with no strings attached and interest paid from the first

dollar up to $245,000, calculated daily and paid monthly.

“When faced with higher than expected deposit flows, and an RBA

rate cut, most banks would just drop deposit interest rates, hurting

existing customers while chasing new ones. That’s not what Xinja is

about,” said CEO and founder, Eric Wilson.

“Xinja offers a different way of banking, and that extends beyond technology to how we treat our customers.”

However, Wilson did reiterate the Stash account has a variable rate which may go up or down in the future.

“Right now, in what are turbulent times, we want to stand by the rate we have offered,” he said.

“But there are three things we have to

balance: the RBA rate cut makes it more expensive for Xinja to hold

deposits at the same rate before the launch of our lending program;

there has been an unprecedented uptake of Xinja Bank by Australians; and

now, how we – as a new bank – manage the costs of those deposits. “

Steve Weston, fresh back from 4 years with Barclays in the UK

was listening to the May 2017 budget speech, and his world changed. The budget

contained a plethora of banking reforms, including Open Banking, big bank

levies, the BEAR (cultural reform) and the potential to allow new Fintech bank

start-ups an on-ramp in terms of regulation and capital to foster innovation

and competition in the banking sector.

The announcements opened the door on the potential to create a digital bank and platform business, akin to Starling Bank in the UK. Starling was founded in 2014 by industry-leading banker Anne Boden, who not only recognised how technology could transform the way people manage their money and serve customers in a way that traditional banks hadn’t, but also how a platform business can accelerate scale. They have since surpassed one million accounts, raised £263 million in backing and were voted Best British Bank two years running. Their customers also rate them Excellent on Trustpilot.

Throughout 2017 Steve developed the concept, built a team and by January 2019, Volt Bank was Australia’s first neobank to receive an unrestricted ADI licence. It has now begun on-boarding sections of its 40,000-strong waitlist and is announcing a ‘no catches’ ongoing base interest rate of 2.15 per cent on savings, ahead of a public launch planned for early 2020. Volt’s ‘no catches’ interest rate is not subject to an introductory period, or conditions that lead to many consumers not actually receiving a higher rate, like minimum monthly deposits or a minimum number of transactions.

Volt’s unique digital solution was designed to help consumers

‘save often’ and ‘spend wisely’ after CEO & Co-Founder, Steve Weston, noted

a distinct absence of personal finance products that actually help to make

Australian consumers better off.

Steve Weston, Volt Bank’s CEO and Co-Founder

“What I find troubling is banks saying they are putting

customers at the heart of what they do but that isn’t reflected in actual

practice. As an example, banks should say what percentage of their savings

account customers get the higher advertised interest rates rather than the

often very low base rates. The same applies to home loan interest rates. Why is

it that new customers get a better deal than loyal customers?

“Banking needs to be done in a better way. Volt’s first

product, our savings account, offers a highly competitive rate without any

conditions. I challenge other banks to do the same.

“We are taking our

time to build every product and feature in a prudent fashion, including by

seeking feedback through our co-creation app, Volt Labs. When we launch to the

public in 2020, Volt will be a viable, well-understood, and trusted option for

everyday Australians,” concluded Mr. Weston.

So, what’s under the hood?

Well first there are no branches, but it has also been built

digital first. and at the heart of the concept is the desire to truly assist

customers reach the outcomes they’re seeking and is aiming to help shift

behaviours. For example, the Volt app will

also support savings discipline, helping to create a savings habit. This is

decidedly NOT a product push.

Customers can onboard in less than 3 minutes and Volt will

deliver a customer experience not provided by incumbent banks.

But Volt is also a platform, where providers of digital finance services can connect. Indeed, Volt already has an agreement with PayPal (after Citi, Barclays etc). Via their API they plan to offer best in class digital services on their platform.

They plan to grow via what Steve called Viral Advocacy and the 40,000 wait-list is part of that plan.

And Volt is a fully fledged ADI (in APRA speak) and so can

offer deposit and savings accounts protected by the Government’s Financial

Claims Scheme up to $250k, just like other Australian licenced banks.

They have a road map already laid out ahead, tackling other

customer needs, and whilst initial funding for the venture has come mainly from

high-net worth investors, they will be tapping a broader investor base to raise

the capital they will need to commence lending quite soon.

So, I see this as more than just another upstart Fintech.

Volt has the pedigree, the vision and the capability to become a significantly

disruptive player in the Australian market. And frankly, as their Deposit rate

is no holds barred higher than others in the field, it will be interesting to

see how the incumbents respond. But this could just be the start of the long

awaited and needed banking revolution here. Perhaps like Aussie Home Loans disrupted

mortgage lending a generation ago?

Things could get very interesting indeed!

Note: DFA has no commercial relationship with Volt Bank. This article is one in our series on digital banking disruption – Fintech Spotlight.

We review recent changes in central bank policies which will involve another bout of quantitative easing, and the impact on the saver community – a sector which silently are being taken to the cleaners. Why no fuss?

One of the critical issues which is hardly discussed in the media is that fact that many savers have funds in accounts which are paying very low rates of interest, when in fact there are better deals available. This little guilty secret allows banks to pump up their margins, offer highly attractive rates to capture new customers then milk them down stream.

Paying lower interest rates to longstanding customers is a long-running pricing strategy used by firms around the world, and gets almost NO coverage. Its a blatant example of “price discrimination” which occurs when providers offer different prices to different customers that have the same costs to serve but different willingness to pay.

But now the UK’s Financial Conduct Authority has released a discussion paper on the problem, which we also see here in Australia. They believe this is unlikely to change without further intervention. They propose a solution which we think might be worth looking at here too. So today I am going to look through their report, and discuss the issue in depth.

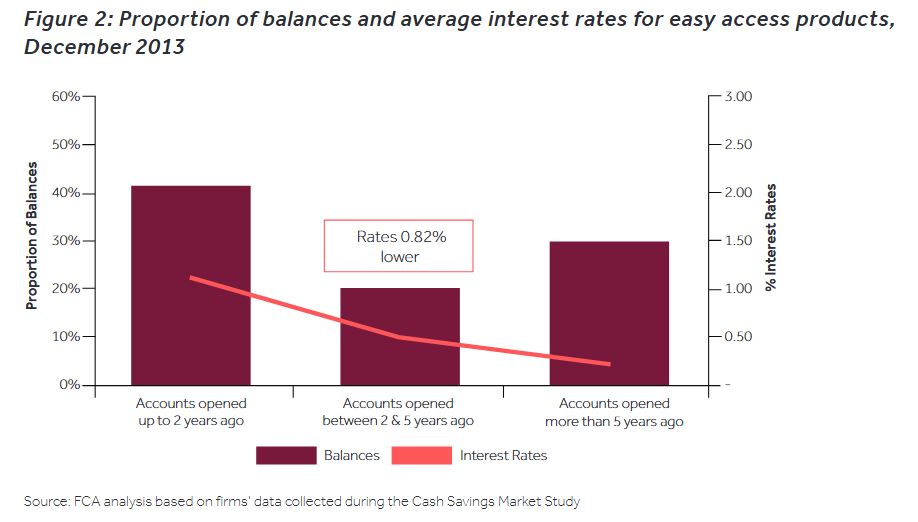

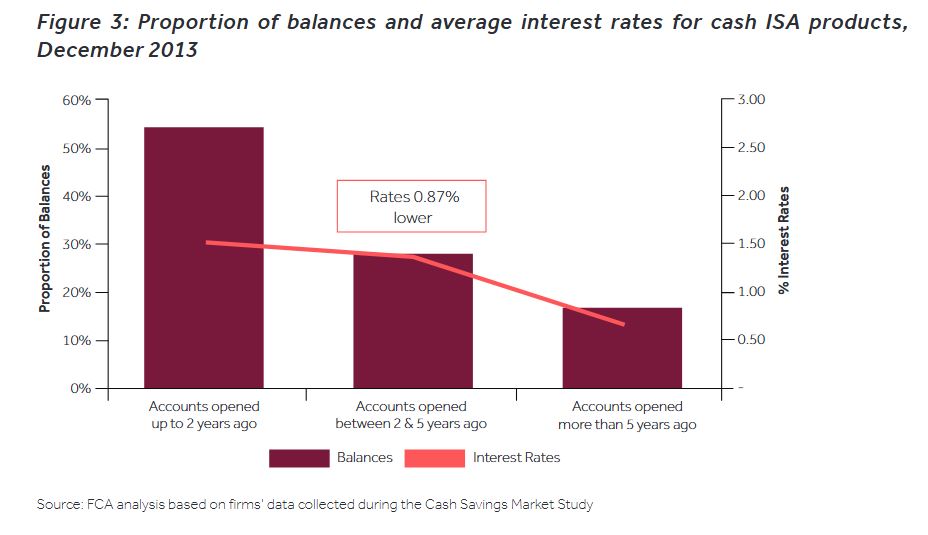

Many savers (yes there are still some with money in the bank despite the debt bomb), have their hard earned funds sitting in low interest paying accounts. Their research shows that 33% of the £354bn easy access savings account balances in savings accounts in the UK have been in accounts for more than 5 years, and that on average longstanding customers received on average 0.82% less than accounts opened more recently. A similar trend is also reported in the £108bn investment savings account, where again longstanding customers received on average 0.87% lower.

They call out the high level of consumer inertia in the cash savings market, with only 9% of consumers switching in the last 3 years. Their research also highlights that providers have multiple easy access products, leading to confusion for consumers, and large personal account providers have a competitive advantage over smaller providers.

So they has initiated a discussion about what should be done in the UK to improve outcomes for customers.

They say that consumers are put off switching by the expected hassle; large, well-established personal current account providers are able to attract most savings balances despite offering lower rates; and there is a lack of product transparency.

In fact this is the latest in a series of interventions which the FCA has been look at since 2015. They initially trialed

A switching box: provided to customers periodically, setting out the potential financial gains from switching. This would prompt customers to consider their choice of account and provider.

RSF: a simple ‘tear-off’ form and pre-paid envelope which would enable a customer to switch to a better paying account offered by their existing provider more easily (internal switching).

Neither worked that well, though the second, a simple tear-off form was a little more effective.

They also tried what they called a sunlight remedy for 18 months in 2015-16. In this trial, they asked firms to provide data on the lowest possible rate that customers could earn across all their easy access savings accounts and easy access cash ISAs. This was split into on-sale and off-sale accounts and branch and non-branch accounts. They released the data over 12 months, via publications. However, they found that the trial did not have a clear, measurable impact on providers’ rate setting strategies. There may be several reasons for this, including that the rates published did not always accurately reflect the rate being paid to most customers.

In the current paper they describe some of the other options they considered, including a complete price discrimination ban on easy access cash savings products. This would involve firms being required to offer single interest rates for all easy access cash savings accounts and easy access cash ISAs, irrespective of the length of time the account has been open.

Banning price discrimination would address the harm against longstanding customers. Under this approach, providers would be unable to offer different interest rates based on age of account. Longstanding customers would have the most to gain from this approach as they are likely to see an increase to their interest rates. Furthermore, customers would not have to take any action to be put on to the same rate as new customers.

It would also increase transparency as providers would be unable to obfuscate prices by making interest rates for all customers clear. This would make it easier for customers to understand and compare their interest rate. It would therefore be beneficial for competition as it would make it easier for customers to shop around for a potentially better value product with an alternative provider.

It may be beneficial for smaller providers with smaller back-books as it would not affect them as much as providers with larger back-books. Smaller providers would therefore be able to continue to offer higher rates than large providers, attracting customers.

This would make it easier for small firms to attract new balances and thus expand. The increased transparency adds to this effect as customers would be able to compare rates more easily and understand how different providers treat their customers.

However, the FCA says that although they have not performed any detailed modelling of this potential remedy, they believe that the unintended consequences of this approach could be significant and may outweigh the intended benefits. First, retail deposits make up a vital part of providers’ funding strategies, with 87% of funding generated by customer deposits (either current accounts or savings accounts).

This approach is, therefore, likely to have an adverse impact on funding models. It would significantly decrease flexibility and reduce providers’ ability to alter their pricing strategies to manage their funding requirements, ie by either shedding or attracting deposits. They

consider that this could lead to significant unintended consequences. They, therefore, believe that a less restrictive option would be more proportionate relative to the harm. Secondly, the impacts may be offset by significantly reducing front-book interest rates across the board, particularly for larger providers. This is because providers may find it too costly to increase interest rates on all back-book accounts. This may reduce the benefits of shopping around for more active customers who wish to remain with a larger provider.If the customer knows they are getting the best internal rate, there may be less of an incentive to shop around at all. If fewer customers shopped around, this may have the effect of further entrenching the power of the incumbents.

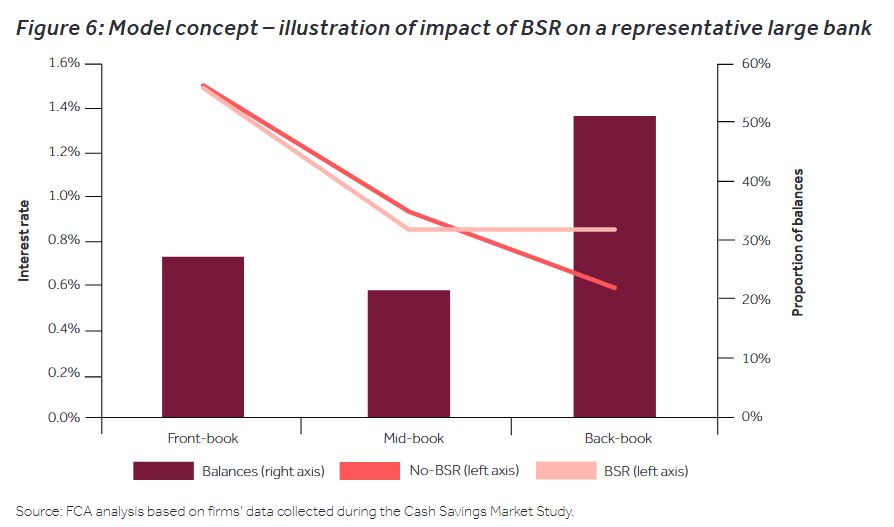

So, instead, they suggesting the introduction of a basic-savings-rate (BSR).

The BSR would involve providers applying single interest rates (BSRs), respectively, to all easy access cash savings accounts and to all easy access cash ISAs which have been open for a set period of time (for example, 12 months). Individual providers could decide the level of their BSR, and would be able to vary it. Providers would remain able to offer different interest rates to customers in the period before the BSR applies (the front-book).

The BSR option that they have modelled is based on providers having broadly 3 groups of customers:

front-book customers who opened their accounts less than 1 year earlier

mid-book customers who opened their accounts between 1 and 2.5 years earlier

back-book customers who opened their accounts over 2.5 years earlier

They suggest that consumers could gain £300m per year – (actually a range of £150m – £480m)

This is a net transfer from firms to customers, taking into account the ‘waterbed effect’ between the different customer groups. They envisage that a BSR could apply to an account after it has been open for a specified length of time. Providers would retain the freedom to offer a full range of easy access products to front-book customers (ie on accounts before the BSR applies) and would also be free to offer the BSR to front-book customers.

They envisage that a BSR could apply to all banks and building societies that offer easy access cash savings accounts and easy access cash ISAs. Credit unions were excluded from the scope of the CSMS as most products they offer could not be substituted for others. Most credit unions offer a dividend rather than an advertised interest rate on their savings. This dividend can depend on how much profit the credit union has made in the year.

They say it would be important for the BSR to be communicated effectively to consumers. This would ensure that consumers are aware of the changes to their interest rate on their savings account and prompt them to consider their choice of savings account and firm; in doing so, they may increase competitive pressure. In addition to providers’ current obligations on the communication of interest rate changes, to provide clarity to consumers before they open their account, providers could:

display their BSR prominently on their webpage, clearly stating that this is their ‘Basic Savings Rate’ and that it is comparable

include the BSR in summary boxes for easy access accounts; they could make the interest rate that would apply after 12 months clear and include a projection of the balance of the account when the BSR applies based on a £1,000 account balance.If a BSR were to be proposed, the FCA’s current view is that providers should communicate the change to existing customers when they first implement the BSR. Sunlight remedy linked to a BSRAs a development of the sunlight remedy trialled in 2015-16, they could introduce a sunlight remedy linked to the BSR. They could ask providers to report their BSRs to the FCA to be published on the FCA website biannually. The aim of this would be to bring to light firms’ strategies towards their longstanding customers. They would expect this to:

be reported by the media as an indicator of how firms treat longstanding customers, exerting reputational pressure on firms to change their behaviour

increase back-book rate transparency, removing a switching barrier by making it easier for customers to understand if they are getting a good dealThey believe that publishing BSRs on the FCA webpage would be more successful than the sunlight trial, given that the BSRs would be directly comparable across firms. they, therefore, believe this would be more likely to have an effect on providers’ rate-setting strategy.

I think its time we had a debate in Australia about the same issue, because data from my surveys highlights that many savers are not getting the best returns they could. So far as I can see ASIC has not even looked at the problem, more shame on them. Another case where regulators here are asleep, and customers are being ripped off as a result – does that sound familiar?

Australian banks are borrowing money at record-low rates from their term-deposit customers, despite needing their cash more than ever.

Dozens of institutions have cut the interest rates they pay on locked-away savings, even though the Reserve Bank hasn’t touched the official cash rate since August last year.

The RBA reported in recent days that rates on three-month and six-month term deposits have fallen to record lows.

Martin North, finance expert at Digital Finance Analytics, said savers are “trapped” and “copping it”.

“The banks have quietly been eroding the returns on deposits at the same time as they’ve been lifting the interest rates on their mortgages,” he told The New Daily.

“It frustrates me that everybody is fixated on mortgage rates, but we’ve got this other segment of the population that is intrinsically trapped by these lower interest rates.”

Average rates on three-month term deposits peaked at 6.55 per cent in 2008, just after the global financial crisis, and have plunged ever since. In July, the latest figures available, the average rate fell below 2 per cent for the first time since records began in 1982.

Back in 2008, a saver with $10,000 could have earned $163 for locking away their cash for three months. Now, with the average rate at just 1.95 per cent, they’d be lucky to get $48 for their trouble.

Since the RBA cut rates last year, 59 institutions have slashed their three-month term rates (compared to four increases); 47 have cut one-year rates (with only 17 increases); and 24 have cut five-year rates (compared to just six increases), according to comparison website Canstar.

“My suspicion is we’re not going to see term deposit rates go up until we see the Reserve Bank go up,” said Steve Mickenbecker, chief financial spokesperson at Canstar.

“The banks have not felt any need to compete harder.”

More galling for borrowers is the fact, revealed by the RBA, that banks need term depositors more than ever.

RBA assistant governor Christopher Kent told an event in Sydney on Wednesday that banks are increasingly borrowing from everyday Australians the money they use to fuel their profits, rather than from expensive overseas bond markets like New York.

Deposits now account for 60 per cent of bank funding, Mr Kent said, up from lows of 35 per cent before the financial crisis – a shift he described as “quite stark”.

This is because the market and regulators have pressured the banks to rely more on term deposits, as this source of funding is considered more resilient to economic shocks.

Here’s how to make the banks pay more for the money they need.

Term is better than nothing

Finance analyst Martin North said many Australians have their money in online savings accounts, without realising they could be getting a better deal from a term deposit.

“There are many people holding their money at call, rather than in term. They will probably not be aware how much their interest rates have dropped in recent times because a lot of people set and forget,” he said.

In July, online savings accounts were paying a miserable 1.65 per cent on average – compared to 1.95 per cent for three and six-month terms, 2.25pc for a year, and 2.5pc for three years.

“If you can afford to tie your money up for a bit longer, it’s probably worth it because you’ll get better rates.”

Never break a contract

Mr North said it is “almost always” a bad idea to pull money out of a term deposit before it reaches maturity in order to take up a better offer elsewhere, as you will often be charged a hefty penalty.

“If you’ve got money in a term deposit, you’ll be locked into a specific term. It’ll be a contract,” he said.

“So be very careful about breaking contract to chase higher rates, as you’ll be charged an arm and a leg to do that.”

Look beyond the big banks

Term deposits are not just offered by the big four banks. They are available at smaller banks, community banks, credit unions and building societies across Australia, so it could be a good idea to compare widely before choosing an account.

“Don’t just automatically assume that the bank you’re with gives you the best rate, because they may not. There’s no guarantee they are,” Mr North said.

“So shop around.”

Never auto-renew

Steve Mickenbecker at Canstar said one of the biggest mistakes made by term depositors was rolling over at the same institution, without comparison shopping.

“If you go into term deposits, be prepared to be a little bit active. Maybe that means going for your six or 12-month term, but be prepared to shift when you get to the end of that term,” he said.

“Never do an auto renew. Look at the rates on offer every time you approach maturity.”

Be wary of super-long terms

Banks may be keen for long-term customers, but the market expects the RBA to lift rates relatively soon.

Mr North said locking away your money for too long could mean you miss out when rates eventually rise.

“Bear in mind that the likelihood in the medium term is that rates will go higher still, so you probably don’t want to go out too far because effectively you might be sitting on a rate that in two years time looks rather cheap.”

Consider an annuity

An alternative to the term deposits sold by banks are short-term annuities offered by life insurance companies, with terms of one year or more.

Justin McMillan, financial planner at Perth-based Smart Wealth, said annuities have better rates because providers are “aggressively” chasing new customers.

“Annuities are basically like extended term deposits, but the rate, because it’s from a life insurance company rather than from a bank, is normally better,” Mr McMillan said.

“They are a growing product, so it’s really a market share play.”

Anyone is eligible, and two of the biggest providers are Challenger and CommInsure. But remember: unlike term deposits, they are not guaranteed by the government.

Editors note. DFA changed the wording in the fourth paragraph as the original article as written confused borrowers with savers!

Savers are seeing deposit rates falling according to our household surveys. This short video explains why, and which households in particular are most impacted.

There is bad news for those households with bank deposits. We have already seem a range of deposit repricing initiates by the banks, as they trim their deposit rates. But it is likely to get worst, as international sources of funding get cheaper, and changes to capital requirements are likely to translate to further rate cuts for savers down the track.

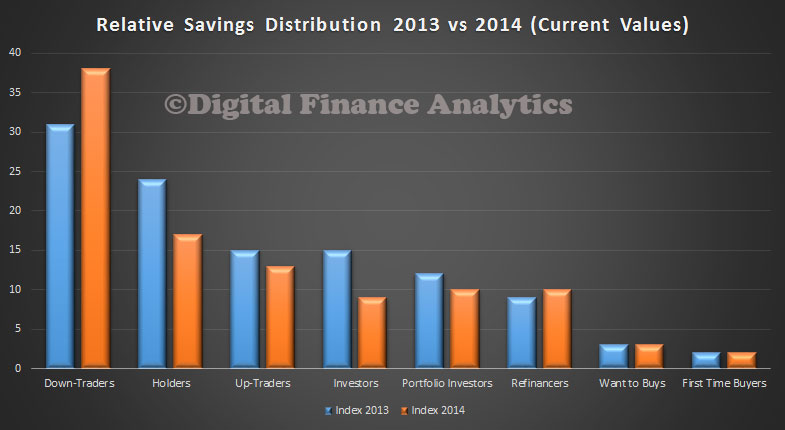

We see that Down-Traders hold the largest relative share of savings, up from 32% last year to 38% this year. All other segments are at the same relative values as last year, or at lower levels. This highlights that people looking to sell and move to smaller properties are hold the most significant savings.

In this analysis, savings includes balances in current accounts, call and term deposit accounts, and other liquid savings vehicles, but excludes property, shares are superannuation.

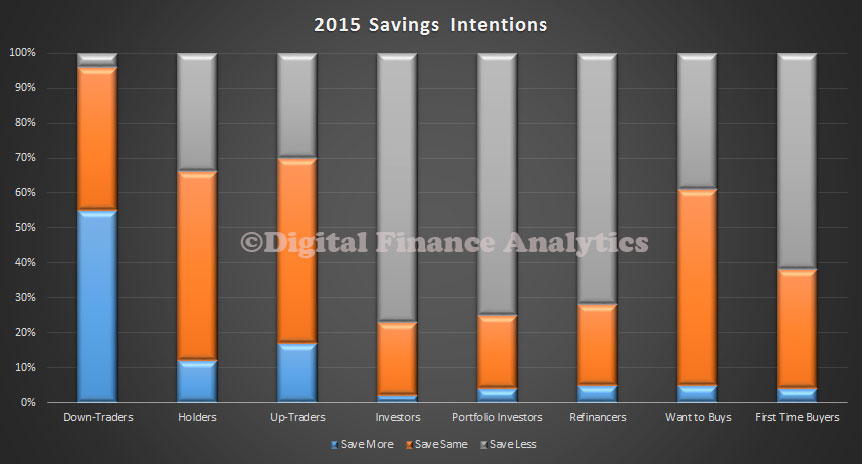

Looking at savings intentions, we see that Down-Traders are expecting to save more next year (55%), and only 5% are expecting to be savings smaller amounts. Investors, Portfolio Investors and Refinancers are more likely to be saving less next year. Want to Buys and First Time Buyers are also quite likely to do the same next year.

Our survey suggests that households who are in savings mode will continue to save, and actually lower interest may well encourage even greater saving. Low interest rates are not a path to stimulate spending in the current environment for many.

Finally, I think we see significant inter-generational issues in play. Some say it has always been this way, but the relative wealth distribution seems more skewed in 2014, thanks to rising property values, significant savings by some, and significant borrowing by others.

We see that Down-Traders hold the largest relative share of savings, up from 32% last year to 38% this year. All other segments are at the same relative values as last year, or at lower levels. This highlights that people looking to sell and move to smaller properties are hold the most significant savings.

In this analysis, savings includes balances in current accounts, call and term deposit accounts, and other liquid savings vehicles, but excludes property, shares are superannuation.

Looking at savings intentions, we see that Down-Traders are expecting to save more next year (55%), and only 5% are expecting to be savings smaller amounts. Investors, Portfolio Investors and Refinancers are more likely to be saving less next year. Want to Buys and First Time Buyers are also quite likely to do the same next year.

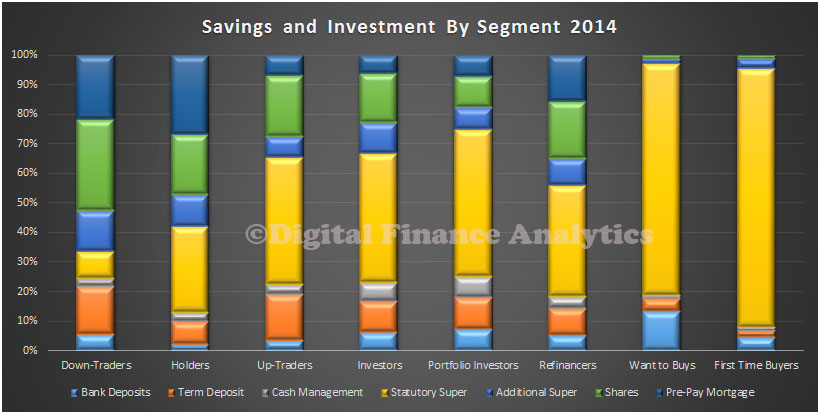

We can also look at the relative distribution of saving and investment vehicles by type. For some, the main vehicle is statutory superannuation, whereas for some other groups, bank deposits and cash management accounts are more significant. We also highlight the importance of pre-paying the mortgage for some segments.

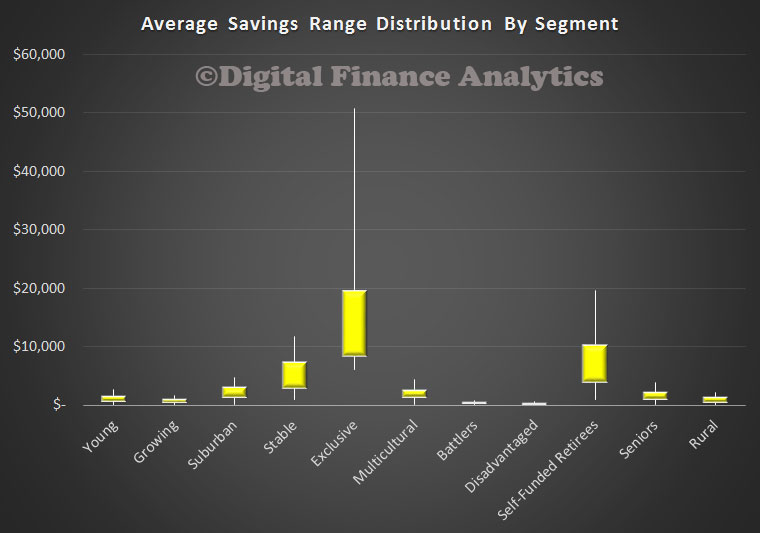

At this point, we introduce our master household segments, and show the relative savings distribution across these segments. By far the largest balances are held by the Exclusive segment, followed by Self-Funded Retirees. The chart shows the relative distribution, with the yellow box showing the 50% distribution bounding.

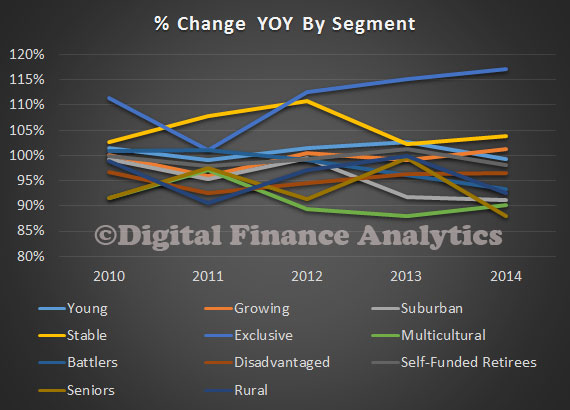

We also see some trends by looking across segments over time. Exclusive and Stables household segments are seeing balances increasing, whereas Seniors and Self-Funded Retirees are seeing balances falling. In our analysis we saw that these older groups are especially feeling the impact of lower savings rates.

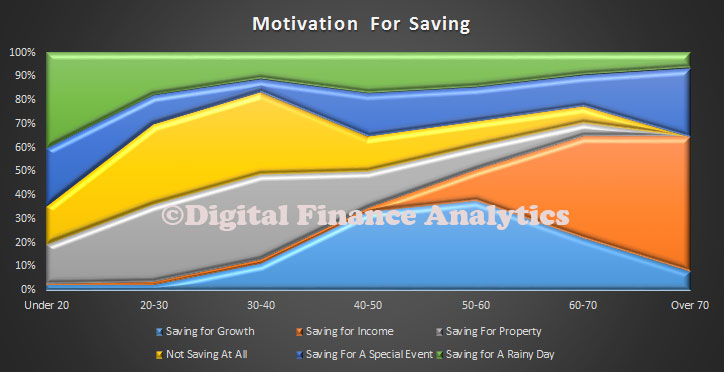

Another way to look at the savings scene, is to examine the motivations for savings. The chart below shows the relative distribution by age bands. Significantly, many households in the 20-30 and 30-40 age ranges are not saving at all. Older households are more likely to be saving for growth, whereas the oldest households are most likely to be saving for income.

65% of younger households are most likely saving for a specific event (e.g. holiday, car, wedding) or for a rainy day. We see that saving for property purchase peaks in the 30-40 years age group.

We believe that households will continue to be cautious in 2015, and that will savings rates continuing to fall, we will see many saving more, not less. The RBA remains keen to encourage households to spend more, but the research shows that saving remains important for those with the largest balances, and many are stress by costs of living rising, savings rates falling, and therefore are expecting to save less.

This is the last post for 2014. Thanks to all those who follow, read and comment on the DFA Blog. We will be back early in 2015, with fresh insight and updated surveys. Meantime happy holidays.

There is bad news for those households with bank deposits. We have already seem a range of deposit repricing initiates by the banks, as they trim their deposit rates. But it is likely to get worst, as international sources of funding get cheaper, and changes to capital requirements are likely to translate to further rate cuts for savers down the track.

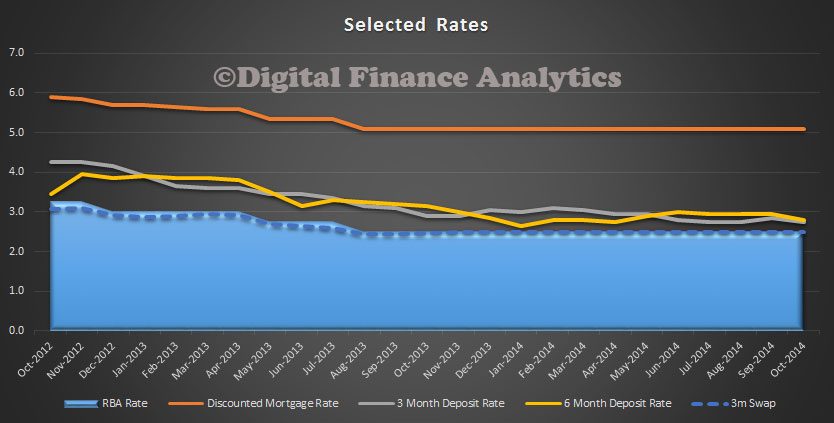

Rates have been coming down for those with bank deposits in recent months, and the rate of fall has accelerated recently. The chart below shows the movements of discounted mortgages, 3 month and 6 month deposits, and also the 3m swap rate, using RBA datsets.

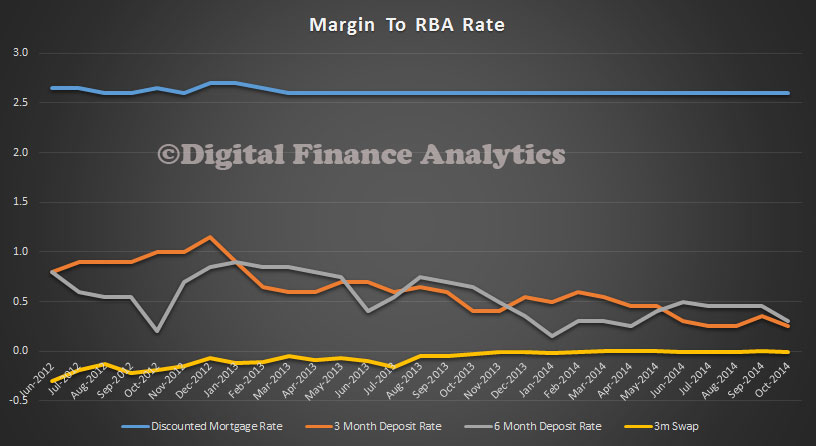

Whilst there is selective deeper discounting on the mortgage side, for some, savers are finding their returns falling. This is show most clearly by comparing the margins between the RBA rate, and loans and deposits. Despite the static RBA rate, deposit rates are falling.

Looking ahead, with banks likely to have their wings clipped by the FSI report, due soon, and changes to capital following on which are likely to lift the costs of lending, the net result will be further pressure on saving rates, and more households looking for higher risk alternatives, as the RBA often mentions in their monthly statements. This continued fall of deposit returns hits older household segments the hardest, especially those banking on deposits to fund their retirements. Returns will be below inflation, so capital is effectively being eroded.

As a comparison, in the UK they have had 6 years of low deposits, and recently savers have found their rates being cut further. Many households are in financial stress as a result. In Australia, savers will either wear the losses, seek higher risk alternatives, or spend the money. Perhaps this latter course may assist an otherwise sluggish consumer sector. But it is not looking pretty.

Blog")