Bitcoin enthusiasts have recently been roiled by claims that an Australian named Craig Wright and his deceased partner are the mysterious founders behind the cryptocurrency.

Of course, we’ve been down this path before. The New York Times, Fast Company, The New Yorker and Newsweek have all made similar claims about different people, only to be proved wrong. And last month, Wired – the magazine behind the most recent claim – said there are reasons to believe Wright is actually a hoaxer and not “Satoshi Nakamoto,” as the currency’s creator is known.

Regardless of whether the new claims are correct, it has resurrected a worry that has long plagued bitcoin users. Around one million bitcoins were mined early in the currency’s history and have never been transferred. Were they to be sold en masse, bitcoin’s value could drop precipitously, wiping out a lot of wealth and threatening its status as a reliable alternate currency, independent of banks and governments.

However, the reporting about Wright and the bitcoin businesses and trusts he has established – presumably for tax and secrecy purposes – reveals an even bigger threat to bitcoin users and other supporters of virtual currency: how will such currencies be treated for tax purposes?

This is a question I have been exploring for the last decade, both with regard to virtual currencies designed to be used solely online, such as for World of Warcraft, and those designed for use in the real world, such as bitcoin.

Australian tax authorities searched the home of Craig Wright shortly after Wired magazine fingered him as the founder of bitcoin. Coincidence?Reuters

Currency or investment?

Bitcoins are created by a computer algorithm and are initially allocated through a process colloquially referred to as “mining.” Miners collect bitcoins by solving complex mathematical equations used to authenticate transfers and in so doing both bring more of the currency into the world and maintain the system.

Bitcoin users have a public key and a private key associated with the bitcoins they own. To effect a transfer, one must use the private key. However, transfers are recorded on a public “block chain,” which uses the associated public key.

This secure public record-keeping obviates the need for third-party intermediaries, like banks. While the world can see the public key and how many bitcoins are associated with it, the owner of the bitcoin can remain anonymous if he keeps his association with that key secret.

Approximately 15 million bitcoins have been issued to date, and they are currently valued at about US$430 each, for a total of approximately $6.5 billion. The algorithm is designed to generate 21 million bitcoins, and experts anticipate that the last bitcoin will be issued sometime between 2110 and 2140.

Bitcoin is designed to be used as a currency, though some hold it as an investment. The difficulty is that governments have taken a variety of positions on the nature of bitcoin for tax purposes.

For instance, some countries, including those in Europe, have classified bitcoin as a currency for consumption tax purposes, meaning that the various value-added taxes do not apply to bitcoin exchanges, while others, such as Australia, have not. Similarly, the U.K. treats bitcoin as foreign currency for income tax purposes, while the U.S. regards it as property.

Those who “mine” bitcoins will likely be subject to income tax on the value they receive under the theory that they are being compensated for validating bitcoin transactions and maintaining the block chain that records all transfers. But this is true regardless of whether bitcoin is recognized as a currency. In other words, they are not really mining and not subject to the complex rules governing mining operations. Instead, they are being compensated for services.

The difficulty arises when people try to spend their bitcoins, however acquired.

Another man said to be the mysterious Satoshi Nakamoto was Dorian Nakamoto.Reuters

How cash transactions are taxed

Those who spend local currency, such as dollars (U.S. or Australian) or euros, do not report a gain or loss when they do so. For instance, if I buy a hamburger, I don’t have a gain or loss on the currency used, regardless of whether it has changed value relative to other currencies.

As the baseline currency, a dollar is worth a dollar, even though it may fluctuate against other currencies or be affected by inflation.

Foreign currency is different. If I buy a euro for $1 and spend it later, when it is worth $1.10, theoretically I have a $0.10 gain that I should be taxed on. Different countries have different rules, but in the U.S., taxpayers need not pay taxes on such gains if they are under $200 in a given year.

By refusing to classify bitcoin as a currency for income tax purposes (local or otherwise), tax authorities effectively treat bitcoins as any other property, meaning that those who buy items with bitcoins must report any gain on the transaction associated with a change in its value. That is, it is treated like an investment, regardless of how the owner actually uses it.

It is as if they sold their bitcoins for cash and then used that cash to make a purchase. Worse yet, if the bitcoin has gone down in value, taxpayers might not be able to deduct the losses, because they could be considered personal. Thus, anyone using bitcoin as a currency has to keep track of each bitcoin’s cost so that he can accurately calculate gain or loss.

This administrative task, combined with the potential need to pay income taxes, could make bitcoin too difficult to use as an alternate currency.

While bitcoins are a virtual currency, some enthusiasts have minted physical versions.Reuters

Wright’s woes

Wright’s tale of woe with the Australia Tax Authority (ATA) (revealed in a transcript made public as part of the effort to prove that he is Satoshi Nakamoto) shows how the decision not to classify bitcoin as a currency creates problems with a tax on goods and services (GST).

Among other things, Wright sought to create an exchange to buy and sell bitcoin. If bitcoin were considered a currency, such exchanges would be exempt from the GST, and the exchange could operate economically. However, if the GST applied to such transactions, as the ATA claimed, the exchange would be forced to purchase $1 of bitcoin for $1.10 (assuming a 10% rate).

In other words, if you use normal currency, it would cost you $1, but if you use bitcoin, it would cost $1.10. Bitcoin becomes a lot less attractive under those conditions.

To avoid this result, Wright and his lawyers established a number of offshore trusts and argued that, for many of the transactions the ATA was investigating, no bitcoin was actually transferred. Instead, the beneficial interests in the trusts, which were not subject to the GST, were transferred. The bitcoin itself was purportedly held offshore, and any transfer of the bitcoin or rights to it were outside the reach of the ATA.

The problem for tax authorities

It’s not clear whether such arguments would actually succeed, but they illustrate a real problem that intangible assets raise for both consumption and income taxes, especially for countries that use a territorial tax system (that is, one that doesn’t tax foreign income).

If assets are considered to be outside a given country, they will not be subject to that country’s GST or equivalent tax. Moreover, if the asset can be “wrapped” in a trust or other entity whose ownership interests are exempt from the GST, it can potentially escape tax even if it is held locally.

Similarly, if such assets generate income, for instance when they are bought or sold, under a territorial system, that income will be taxed in the country where the sale occurred.

It is not surprising that Wright established at least some of his trusts in known tax havens, such as the Seychelles. Even if his efforts to shield bitcoin from tax through these efforts succeed, they are far too complicated for the average user and will likely further impede bitcoin’s adoption as an alternate currency.

Bitcoin’s challenge

Much of the recent focus has been on whether Wright really created bitcoin and whether he is sitting on a hoard worth close to a half billion dollars, which could potentially destabilize the market.

However, the real threat to bitcoin and other similar products may come from a far more mundane source: the world’s tax authorities. Absent favorable rulings, every bitcoin transaction could generate both income and consumption tax liability, rendering bitcoin impractical as an alternate currency.

Sophisticated tax planning to avoid such outcomes might succeed but would make bitcoin harder to use.

Thus, while bitcoin was developed as a means to free individuals from the need to interact with third parties, including the government, it nonetheless needs governmental cooperation if it is to move from the fringes to the mainstream.

Author: Adam Chodorow, Professor of Law, Arizona State University

The recent somewhat rapid demise of Dick Smith Holdings, resulting in its entry into voluntary receivership, is a stark reminder of the risks of investing in companies listed by private equity firms without doing careful research. Another example from the recent past is Myer, which has also never recovered anywhere near its original listing price.

Some commentators have blamed the demise on poor strategy, circumstances in the retail sector, or poor inventory management. But while investors in Dick Smith Holdings shares could end up with nothing, the private equity firm that acquired Dick Smith from Woolworths in 2012 has already recouped its cash investment several times.

How is this possible?

How did Anchorage Capital Partners manage to acquire Dick Smith from Woolworths in 2012 in a deal worth A$115 million and list it in the market for an equivalent total market value of A$520 million?

Private equity 101

Private equity firms typically represent informed investors such as high net worth individuals, or fund managers looking for higher returns through leveraged investments.

Typically a private equity firm will undertake a portfolio of highly leveraged investments in different sectors achieving a level of diversity but at a high risk the longer they stay in.

The firms have a very clear objective: identify businesses with potential for high returns based on their balance sheet, operating potential or capacity for leverage and for tax benefits but to exit as soon as objectives are achieved.

The objective is not to acquire a business with the objective of investing for the longer term, but purely with a view to exiting at a point where the return for risk relation is maximised.

Window dressing

This means that an exit is planned from day one to the extent return is not compromised. The long term prospects for the business are only of interest to the private equity firm to the extent that it helps dress the business for the market to help with the private equity firm’s exit. In the case of exit by listing this will typically involve changing and packaging the business so it is perceived as a more valuable investment by future investors. The packaging will typically involve all essential market positive aspects of the business, the balance sheet, capital structure and management.

If an acquired business is already listed, often they will de-list the firm, restructure and repackage it and then place in on the market through a stock exchange or sell it as going concern in part or whole in a sale. Often they will acquire divisions or segments of businesses within larger enterprises as was the case for Dick Smith.

Typically private equity deals are highly leveraged, namely there is much more debt than equity used to fund the acquisition, but once interest and debt is covered all returns go to shareholders, and initially this is the private equity firm. When a business is acquired by a private equity company, it is done through an entity or holding company (newco). Newco under private equity control, typically buys itself, in the sense that newco will own the acquired business but private equity controls newco.

Private equity will fund the acquisition of the business by a majority of debt within newco and not the private equity firm. The private equity firm and management will contribute the minimum equity required; this will depend on the financing arrangements which will be governed by newco’s balance sheet, the reputation of the private equity firm and management, and the appetite of the financial institutions for newco debt. Tax benefits will also be maximised to the extent that interest is tax deductible, a huge benefit given the degree of debt. Furthermore the tax paid on such gains is capital gain, taxed at a lower rate. Private equity firms will use very smart tax lawyers and accountants to structure the deal so that taxes paid will be well minimised.

The private equity firm and management will hold all the equity in newco, but with restrictions on managers in terms of selling their equity. Private equity firms will only accept restrictions on their selling down shares to the extent that it is a condition precedent for debt financing and they believe it maximises the price they can receive on exit so it doesn’t create the wrong impression.

Private equity firms will also earn returns by charging the acquired firm sometimes exorbitant management fees as well as by extracting returns from sale of the business in part or whole, and may even extract dividends, depending on financial covenants from lenders that are put in place at time of acquisition.

Private equity may plan to maintain a stake in the longer term, past their initial exit, to the extent it helps maximise the value received for their sold down stake and will be prepared to write off that continuing stake having already achieved their desired return.

This is what I suggest has already happened in the case of Dick Smith. Anchorage received a price of more than A$2 a share, liquidating the majority of its holding and in the process is also likely to have raised new equity to retire some of the debt, depending on the convenants in place. Regardless Anchorage will have made many times its intial investment at the listing of Dick Smith Holdings even after paying the upside to Woolworths if any requirement as part of the deal.

The losers will be those who are committed, management, shareholders, particularly those who held on since the Dick Smith Holdings listing and unsecured creditors with skin in the game vs Achorage which is simply involved. It’s like bacon and eggs, the hen is involved but the pig’s committed.

Author: John Vaz, Director of Education, Department of Banking and Finance, Monash University

Four years in the making, the European Union’s new data protection rules have finally been agreed by the European Council and await the approval of the European Parliament. But a last-minute addition has sparked a debate about responsibility and consent, by proposing to raise to 16 the “age of consent” under which it is illegal for organisations to handle the individual’s data. This would force younger teenagers to gain parental permission to access social networking sites such as Facebook, Snapchat, WhatsApp or Instagram.

While raising this digital age of consent from 13 as it is in the US to 16 would strengthen the protections they receive, there are doubts about whether it would be enforceable. How would the firms behind social networks be able to verify their users’ ages, for example, or whether they had their parents’ permission? There are already Facebook and Instagram users below the age of 16, so that would entail potentially closing those accounts – how would this be policed?

Could parents or social network providers be prosecuted for allowing the under-16s to access a social network? The proposed new EU rules, the General Data Protection Regulation, would impose heavy fines (4% of annual turnover) for those organisations or firms that breach data protection laws, which means the likes of Facebook would have a great incentive to ensure they complied. But there are few obvious ways to do this.

Additionally, any ban may lead some teenagers to lie about their age in order to create or maintain an account, potentially putting them in more danger by pretending to be older than they are. Janice Richardson, former Co-ordinator of the European Safer Internet Network, said that denying the under-16s access to social media would “deprive young people of educational and social opportunities in a number of ways, yet would provide no more (and likely even less) protection”.

Sophisticated age verification software would be needed, such as scanning machine-readable documents such as passports. But would this be sufficient to satisfy the legal threshold? This would also introduce further problems with the need to acquire and store this sensitive data.

So many social networks to choose from.Twin Design/shutterstock.com

Informed consent

One of the chief concerns during the consultation process for the General Data Protection Regulation was the growth of social networking sites such as Facebook and how data protection rules applied to them. In November 2011, the then EU Justice Commissioner Viviane Reding said she was concerned about the growth of digital advertising and the lack of understanding of how it involved harvesting and analysis of personal information. These concerns led to the decision to update the Data Protection Directive to reflect the many changes in how we use the internet since it was passed in 1995.

While the preamble to the General Data Protection Regulation states that young people deserve protection as they may be less aware of risks and their rights in relation to their personal data, this appears to be a paternalistic view adopted by the European Commission.

For example, the Swedish Data Protection Board (similar to the UK Information Commissioner’s Office) conducted a study of 522 participants aged between 15-18 and found that the majority had experienced unkind words written about them, around a quarter were sexually harassed online, and half of those on Facebook had had their account hijacked. But it also found that the young people had a generally good understanding of privacy issues.

On the other hand, a study from Ofcom, the communications watchdog in the UK, found that teenagers couldn’t tell the difference between search results and adverts placed around them, demonstrating that young people’s understanding of how the web works, and the role of their personal data, is not always sufficient – and perhaps insufficient to represent real, informed consent.

Negotiations ultimately allowed member states to opt-out from the requirement to raise the digital age of consent, but issues remain. With an opt-out agreed, member state governments may lower the age to 13, which would cause confusion due to the way the internet functions across borders. Would a 15-year-old in one country find that his use of social media became illegal as he crossed the border into another?

Facebook, which started among US universities, was originally aimed at the over-17s before dropping its minimum age to 13, hugely expanding its number of users. But this move was not without difficulties, and an estimated 7.5m Facebook users are under the minimum age. Facebook founder Mark Zuckerberg wants the 13-year-old minimum removed altogether.

The question is, can such young teenagers or children take responsibility for holding social network accounts? While concerns around protecting teenagers from the potential dangers of social networking are well-intentioned, it seems rather that the genie is out of the bottle. Parental guidance and education is perhaps a better approach than applying the long arm of the law.

Author: Rebecca Wong, Senior Lecturer in Intellectual Property and Cyberlaw, Nottingham Trent University

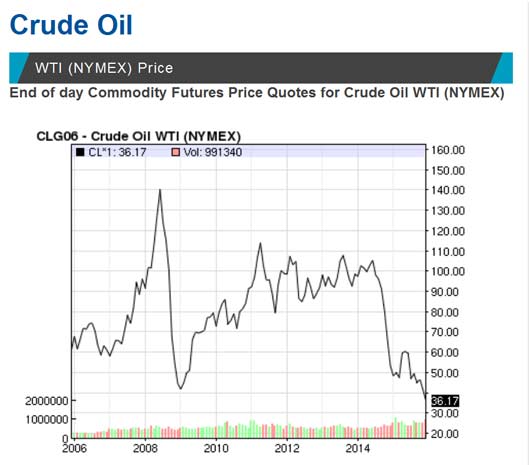

It has been a turbulent year for oil. Prices were strong in summer 2014, before plummeting in the second half of that year. After a modest stabilisation in early 2015, they dropped even further and are now more than two thirds lower than in summer 2014 – as the graph below shows. It’s bad news for oil producers but is forcing some, at least, to reform their economies as a result.

Russia is losing an estimated US$2 billion in revenues for every dollar fall in the oil price. Its economy is heavily dependent on energy revenues, which account for 50% of its federal budget revenues. Even a dramatic interest rate hike to 17% has not helped the steep devaluation of the ruble, the stock-market drop or the amount of money leaving the country.

The situation is even worse for the world’s largest exporter of oil, Saudi Arabia, which is expected to end the year with a deficit of $150 billion – about 20% of its GDP and the largest in its history. It has already started cutting project budgets and military acquisitions as a result. It is even introducing VAT for the first time.

The severity of falling oil prices on Saudi Arabia’s economy can also be seen in its decision to open its stock market to foreigners in June 2015. It has also relaxed rules to allow qualified investors direct access to stocks to reduce the economy’s dependence on crude.

In Venezuela, the economy was already in a shambles when oil was at $120 a barrel. And in Malaysia the government is realigning its budget by removing gasoline and diesel subsidies. Similar steps were taken by governments across the world to remove oil subsidies – Indonesia abandoned a four-decade-old policy of subsidising gasoline while India also stopped subsidising diesel and raised fuel taxes.

Of course, falling oil prices are not bad for all. They increase households’ scope for consumption and at the same time decrease companies’ production and transportation costs, which normally leads to higher profits and increased investments. Rapidly developing economies such as China and India, which are net importers of oil, are experiencing the most obvious immediate benefits. They are able to use savings on oil imports to reduce their trade deficit, improve government budgets, reduce inflation and redistribute money to infrastructure projects.

Out of pocket: drivers in India will no longer benefit from government diesel subsidies.Steve/flickr, CC BY-NC-ND

Nations that are dependent on oil revenues will therefore require immediate economic and financial reforms in 2016 to balance their budgets. One method being adopted by many Islamic states is the issuing of sharia law-approved bonds, known as sukuk. These bonds can be used to finance big projects such as the building of important infrastructure, including airports, and developing other natural resources.

Malaysia has been leading the way on this, banking on its burgeoning Islamic finance industry to reduce its oil earnings shortfall. It is planning to sell $1 billion to $1.5 billion of sovereign credit in 2016 on top of global Islamic bonds this year.

The Saudi Arabian government is similarly depending on both conventional sovereign bonds and sukuk to finance its budget deficit. In 2015, the kingdom issued sovereign bonds worth around 100 billion riyals ($26.5 billion) to ease the shortfall. It’s all part of a $130 billion spending plan to diversify its economy away from oil. But to increase its share of the Islamic finance market, it will need to follow Malaysia’s lead in making the regulations clear for trading sukuk.

Many more oil exporters are turning to sukuk bonds to cover their deficits, including Bahrain, Oman, Qatar and Nigeria, Africa’s largest oil producer. The sukuk bond market is forecast to grow by 15% in 2016 as a result.

The emergence of sukuk has been a significant development in Islamic capital markets for many oil rich nations in the Middle East and South East Asia. Funds raised through sukuk can be allocated in an efficient and transparent way. Sukuk issuance has proven its resilience during recent periods of turbulence in global capital markets and it is showing its potential to act as a cushion for falling oil prices for oil rich countries.

Author: Nafis Alam, Associate Professor of Finance, Director- Centre for Islamic Business and Finance Research (CIBFR), University of Nottingham

Potentially trailblazing plans for state-assisted financing of affordable housing are emerging in New South Wales. In what looks to be a landmark policy announcement with possible national ramifications, the NSW government last week outlined the first phase of Premier Mike Baird’s March 2015 election commitment to establish a A$1 billion fund for social and affordable housing.

But for the short-lived GFC housing stimulus, this is the first significant rental housing supply subsidy in Australia since the 2008 National Rental Affordability Scheme (NRAS).

While full details are yet to be disclosed, it appears the Social and Affordable Housing Fund (SAHF) will be something like a “future fund” or endowment scheme. Government will invest a capital sum in revenue-generating assets. The resulting returns will underpin annual payments to approved consortia over 25-year terms.

This ongoing subsidy will help community housing providers bridge the gap between rental revenue and operating costs. Most importantly, it includes repayment of construction debt raised from private financial institutions such as banks and super funds. Perhaps in awareness of research evidence on ways to minimise the cost to taxpayers of private finance for affordable housing, officials acknowledged the possibility of a government guarantee or other credit support on loans to consortia.

In principle this is quite a big deal. The more familiar policymaking style involves one-off or pilot initiatives. The SAHF is presented as an ongoing budget commitment to state-supported social and affordable housing growth, with phases two, three and four of the program signalled at the launch.

Second, as the name implies, SAHF is centred on “social” housing: it has a 70% minimum social housing requirement. Unlike schemes such as the NRAS, most of the homes will be financed to allow rents set at levels manageable for very low-income groups rather than affordable only to moderate-income earners.

In the post-GFC world this is highly unusual. For example, only in Scotland does a significant UK social housing investment program remain intact.

Third, and most important, the fund’s creation reflects a long-overdue official recognition that, left to itself, the market does not and cannot provide decent housing that low-income groups can afford.

Big plans, but starting small

Having promised voters a $1 billion housing fund, the Baird government has announced phase one plans for 3,000 homes – a fraction of what’s needed.AAP/Nikki Short

While potentially important in principle, the SAHF is decidedly modest in practice, at least in its initial phase. The statewide target – implicitly to be achieved over several years – is for just 3,000 homes. This will barely scratch, let alone seriously dent, the backlog of 60,000 applicants marooned on the NSW public housing waiting list.

And that’s before you even consider the tens of thousands of unregistered low-income private tenants pushed into poverty by high rents across the state. In Sydney alone, 94,000 families and single people were in this position in 2011. Many if not most will be additional to those on the public housing list.

Nevertheless, there’s a lot to like in the NSW government’s approach. It puts non-profit community housing providers (CHPs), which have a strong track record of high-quality tenancy management, front and centre. Registered CHPs will manage all SAHF housing.

The scheme offers a long-term (up to 25 years) operating subsidy that can be matched to a private financing deal. This gives private investors like super funds the certainty they need. “We’ve listened and we’ve read the reports on that,” officials said.

And it recognises the cost to social landlords of co-ordinating services for tenants who have support needs: the operating subsidy will include a component for this. The 2010 Henry review of taxation recommended this.

Limits to affordable land must be overcome

Having access to land at an affordable price is fundamental to successful affordable housing strategies. Phase one of the SAHF relies on unlocking land to develop social housing owned by churches, NGOs and other philanthropic sources. This is a finite strategy and we query whether well-located sites for 3,000 dwellings will be forthcoming? What then?

The state government has the two-part answer in its power. First, it must require all medium- and large-scale residential projects to include a reasonable component of affordable housing. For Sydney, we suggest a city-wide target in the region of 15-25%.

There is a once-in-a-generation opportunity right now in Sydney to do this as large-scale redevelopment plans unfold along transport corridors, in precincts and renewal areas. Once developers have bought up that land it will be too late. They need to be able to factor into their feasibility plans the cost of providing the affordable housing, and thereby reduce the price they offer for sites.

Second, state and local government-owned land made available for affordable housing (for example, public housing estates slated for renewal, surplus government sites and air spaces above public sites) must be priced at a level that affordable housing developers can afford to pay to keep their costs (and therefore the government operating subsidy exposure) to a minimum.

Only by linking its financing strategy with favourable pricing of state land offers and planning policy changes will the SAHF be scalable and durable – offering potential to reduce the unacceptably high levels of unmet housing need.

Premier Baird is expected to announce further details of the fund early in the new year. With worsening affordable housing shortages around the country, it must be hoped that the prime minister, his treasurer and his cities minister, as well as premiers and treasurers across Australia, will tune in to learn more on this constructive initiative.

Authors: Hal Pawson, Associate Director – City Futures – Urban Policy and Strategy, City Futures Research Centre, Housing Policy and Practice, UNSW Australia; Vivienne Milliga, Associate Professor – City Futures Research Centre, Housing Policy and Practice, UNSW Australia.

When a central bank lifts interest rate targets by 0.5% it expects households and firms to respond. In a crisis, the official target may fall by 3% in order to shock the economy into a positive response. These movements of interest rates by the central bank are an important tool of macroeconomic adjustment

They are also relative to the longer term, or normal rate of interest in the economy. What is interesting now is that rates have been low for quite a long time suggesting the natural rate of interest in the economy has fallen permanently.

A recent research paper from the Bank of England suggests that the global neutral interest rate may settle at or below 1%. To put this in context, the paper suggests that rate was around 5.5% in the 1980s (yes, that is real, so adjusted for inflation).

Central banks will get into a tizz about this because it gives them less room to cut rates to stimulate the economy. It gives the bankers much less room to cut interest rates in a crisis.

The reasons for the fall are broadly that saving has tended to increase and investment to fall; more money is available but fewer people want to borrow, thus driving down rates. The authors of the Bank of England paper argue the trends will not change abruptly so we can expect low rates for a long time.

They suggest savings have tended to increase in part for demographic reasons, because of rising inequality, and from a desire by Asian governments to maintain a financial buffer. The main demographic reason has not been ageing, but a decline in the dependency ratio: as birth rates have fallen, the proportion of people who were not of working age has fallen from 50% to 42% over the last 30 years. With fewer children people have been able to save more.

Piketty and others have pointed out the increase in within-country inequality over the last few decades, and since richer people save more than poor people, this too has tended to boost savings.

At the same time the authors argue that investment has fallen for three main reasons. The most important is the fall in the price of capital equipment which has meant that a given increase in output can now be obtained more cheaply (with a lower investment spend).

Investment by government has also fallen slowly but surely over recent decades, albeit with some uptick in response to the global financial crisis. It is less clear why this has happened but I suspect it is because government revenue growth is limited by sensitivity around taxes, and government expenditure is increasingly directed towards transfer payments. Investment also seems to have fallen because it appears to have become relatively riskier – the return on capital has fallen but not nearly as much as the risk free rate – reducing the inclination of firms to invest.

What does it mean for you and I? Broadly we face a world which advantages investors and disadvantages savers. The returns on our investments in safe assets will be low and investors are likely to take on additional risks in order to boost returns. This makes it hard for Australian investors since banks and miners dominate our exchange: the low interest rate environment is not good for banks, and there is no clear end in sight to the commodity price downturn.

As voters we should be less concerned about public debt than we were. The case for policy changes which stimulate growth has increased, and increased government investment in productive assets is strengthened.

Author: Rodney Maddock, Vice Chancellor’s Fellow at Victoria University and Adjunct Professor of Economics, Monash University

All eyes are on the US Federal Reserve which is expected to raise interest rates for the first time in nearly a decade. Since the financial crisis in 2008, the US, along with the eurozone, UK and Japan have held their interest rates close to zero and used quantitative easing to flood financial institutions with capital.

This two-pronged approach to reviving economic growth has led to a colossal amount of money being injected into the global financial system, offered at next to nothing. While the aim has been to revitalise the consumer spending needed to boost the economies of advanced economies, developing countries are poised to be the victims of these policies.

More than US$12 trillion has been injected into the global financial system since 2008 all in the name of stabilising the global economy. The injection of hot money at this pace and quantity is nothing more than a false economy, and could sooner rather than later trigger massive economic challenges in emerging economies.

Investors have been able to borrow significant sums for very little and direct the proceeds into high-yielding assets in developing countries. A fire hose of cash has poured into investments, financing infrastructure and other projects. But the massive surge in the supply of cheap credit has created unstable bubbles.

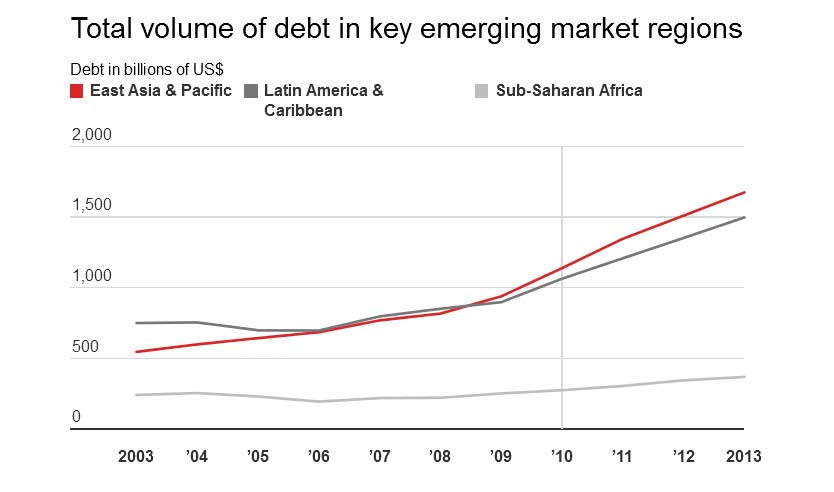

As the following graph shows, key emerging economies such as Ghana, Nigeria, Argentina, Brazil, Thailand and Vietnam have seen dramatic increases in their debt stock. And they are not alone. World Bank data shows they are among 80 emerging markets whose debt has increased significantly since the financial crisis.

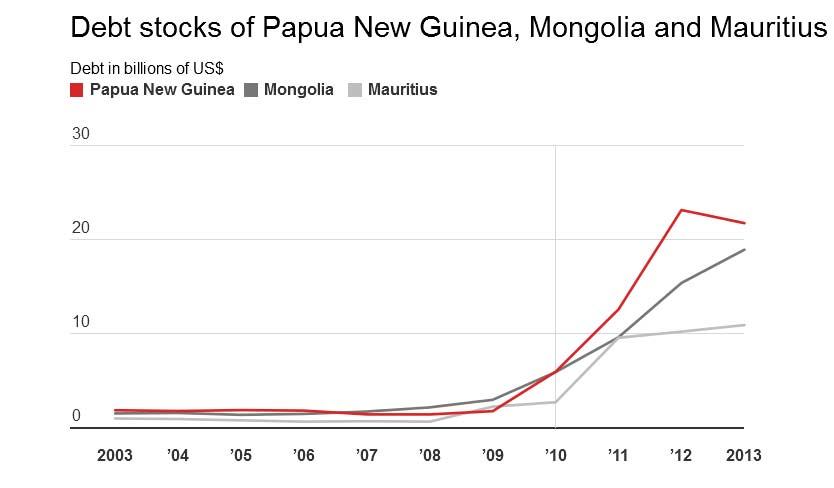

A number of others such as Mongolia, Mauritius and Papua New Guinea saw their debt stock increase by close to 1,000% in the five years following the 2008 financial crisis. These are all low income economies and so their ability to absorb economic shocks is minimal. If (and when) foreign investment is pulled out, they will suffer.

Bubble bursting

If investment is withdrawn – as is likely when interest rates rise – this will leave a gaping hole in the financial system of the recipient countries. Investment in everything from infrastructure to health, education and manufacturing in these countries would be left chronically underfunded, as a colossal amount of money would need to be channelled towards debt-servicing for many years to come.

Not only this, an increase in interest rates could trigger a massive capital outflow from developing countries to where the return on investments has suddenly increased. This is likely to cause a massive shortfall in market capitalisation and burble-busting in the developing countries affected.

To fill the sudden shortfall in capital, the developing countries affected could turn to public or private lenders for urgent financial assistance. But this will increase their debt burden even further.

Most of the debt stocks owed by these developing countries are denominated in foreign currencies, with approximately 80% in US dollars. As the US raises interest rates, the US dollar will strengthen, which will significantly heighten the debt-servicing cost for countries paying back their debts in that currency. Given the nature of their fragile economies, developing countries including Nigeria, Vietnam, Ethiopia and Ghana are most likely to be vulnerable and may have to resort to further borrowing and a fire sale of valuable assets in order to meet their debt obligations.

Exchange rate uncertainty could also trigger a series of credit events, which are capable of hurting the countries’ credit rating. This could lead to margin calls and a review of the existing terms and conditions of lending. And this will only exacerbate the debt burden of the countries concerned even further.

Even a small percentage increase in interest rates is likely to cause shock waves across developing countries. It is a challenging time for emerging markets right now, with commodities in a prolonged slump, and with both China and the eurozone (other key investors) facing economic slowdown.

With an interest rate hike marking the end of cheap credit, this will cause a gaping hole in developing economies’ capital markets. The outflow of capital from their markets will in turn cause their currencies to depreciate further, while the US dollar will strengthen as money flows in. This could lead to even more serious and prolonged debt-servicing problems.

Author: Ola Sholarin, Senior Lecturer, Quantitative and Financial Economics, University of Westminster

With the US Federal Reserve seemingly set on raising interest rates, it’s time to take stock of what low rates have done for the world. And what the prospects are when this era of low interest rates comes to an end.

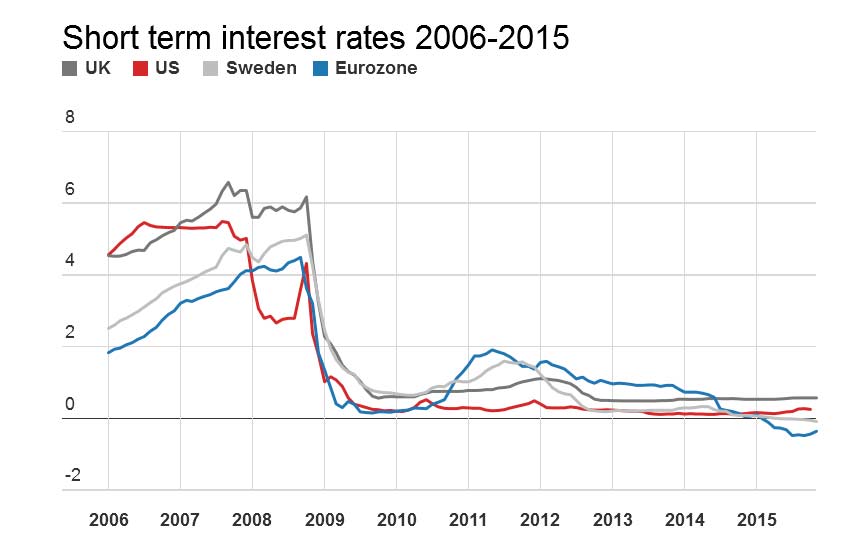

Since the financial crisis, short-term interest rates have been close to zero in most major economies. The US Federal Reserve has held interests around 0.25% for the last seven years. Meanwhile, the UK’s bank rate remains at 0.5% and in Sweden the central bank has set a negative nominal rate.

The reasons are straightforward. Interest rates reflect the cost of borrowing so low rates make it cheaper to borrow to invest. This investment should increase growth, create jobs and ease the economy out of recession. Here’s what seven years of rock bottom interest rates have done in reality.

Investment

So low interest rates should have been great for investment. This has not exactly been the case, however. Investment as a share of GDP fell after the financial crash in the US, UK and eurozone, but has taken a long time to recover, and hasn’t yet regained pre-crash levels.

This is because the fall in real wages after the financial crash means labour has been relatively cheap, decreasing the incentive for firms to undertake capital investment. Plus there are ongoing concerns about weak demand both in the UK, the eurozone and the wider global economy, which also inhibit investment despite low interest rates. Fears of this weak demand may explain why rate rises in the relatively open economies of the UK and the eurozone have been delayed compared to the US, which has experienced buoyant domestic demand in recent months.

Consumption

One effect that may come back to bite us is the effect of low interest rates on consumption. Some commentators fear that the UK’s recent recovery, for example, is fuelled by consumption based on household debt. Any rise in interest rates may choke off that channel of recovery, and may mean some borrowers cannot repay their loans.

Laden with shopping … and debt?EPA/Andy Rain

Global economy

Capital flows between nations are affected by differences in their interest rates. As interest rates fell after the financial crisis, it freed up huge amounts of capital, which was then invested in countries where returns were more favourable. These capital outflows worsen the balance of payments deficit. In turn this leads to depreciation of exchange rates making imports relatively more expensive and thus improving the trade balance.

As rates rise we therefore expect to see exchange rate appreciation – a “strengthening” of the dollar is expected to follow on the back of the Fed’s rate rise – and a deteriorating trade account. Great news for cheap holidays in far flung lands, but bad news for exporting firms, and financial distress for emerging economies with dollar denominated debt.

Housing

A further sting in the tail is the potential effect on the housing market. British homeowners in particular have enjoyed many years of cheap variable-rate mortgages and perhaps haven’t realised how even very small rises in interest rates can have quite dramatic effects on monthly repayments.

This could have dire consequences for people’s ability to afford their mortgage repayments if rates rise. Some would say that such rises would help correct an overheated housing market. But, while this may be true in some regions (such as the UK’s south-east), it is not true everywhere. Interest rate rises may therefore increase regional inequality.

So, we’ve seen that low interest rates have “good” effects in promoting investment and increasing household consumption, though there may be a cold turkey effect when cheap borrowing comes to an end.

Savings and pensions

Low interest rates and low inflation have reduced the reward for saving to pitiful levels. Households have effectively been encouraged not to save, but to spend. This means many do not have contingency plans for a “rainy day”. And more importantly many people have woefully inadequate pension provision for their old age.

Low interest rates also feed through to annuity rates which convert pension pots on retirement into a stream of income throughout retirement years. Annuity rates have collapsed, and so pensions are not as generous as people had anticipated. In turn this discourages people from making pension contributions, which is exactly what is not needed as the population lives longer.

Author: W David McCausland, Professor of Economics, University of Aberdeen

On December 12, 2015 in Paris, the United Nations Framework Convention on Climate Change finally came to a landmark agreement.

Signed by 196 nations, the Paris Agreement is the first comprehensive global treaty to combat climate change, and will follow on from the Kyoto Protocol when it ends in 2020. It will enter into force once it is ratified by at least 55 countries, covering at least 55% of global greenhouse gas emissions.

No, not Donald Trump trying to savage it any time he comes within three feet of a microphone. It’s that enormous social shifts in recent years – like the forcible relocation of 250 million people from rural areas to urban environments – have transformed the country, in the words of its Academy of Social Sciences, from “a society of acquaintances into a society of strangers.”

And these strangers, it turns out, don’t think much of each other. Social trust is at miserable levels, leading to a shaky business environment in which half of all written contracts are blatantly breached.

Since part of the problem is the lack of a credit reporting system, the government has decided to establish one. But instead of only considering people’s ability to repay loans, this system will rank people based on their trustworthiness using all sorts of data.

This might sound exactly like the kind of thing you’d expect from an authoritarian regime. And as someone who has pondered the ways in which privacy is squeezed by an ever-expanding surveillance state, I was intrigued by this unholy alliance between Big Data and Big Brother.

But what really surprised me was not just the outlandish lengths to which the Chinese government will go to evaluate its citizens. It was that its tactics were surprisingly close to what is already happening here, as banks look for ways to lend money to – and collect fees from – people with no traditional credit history.

But first let’s look at what the Chinese are doing.

The glories of trust-keeping

Using an enormous range of information, from traffic violations to consumer patterns to social networks, China intends to give every one of its 1.3 billion citizens a “social credit” score by 2020.

A recently translated summary of the plan explains that the goal is nothing less than raising “the sincerity and quality of the entire nation.” That, it says, should help address everything from workplace accidents to food safety failures to tax evasion and production of counterfeit goods (putting Canal Street, every New York woman’s go-to source for knockoff Chanel handbags, rather under a cloud).

The plan includes recommendations for establishing “civil servant sincerity dossiers,” something I’d like to see applied to my local DMV, lots of talk about “professional ethics, household virtue and individual morality” and encouraging companies to conduct “client sincerity evaluations.”

I’m not sure what that means, but it conjures visions of online retailers diligently making entries like, “Disappointing customer. Returned item saying ‘It didn’t fit.’ Strongly suspect she’s lying about being a size 6.”

There’s also a large public relations component, with the use of news media to “forge a public opinion that trust-keeping is glorious” and a raft of proposed holidays, including “Sincere Trading Propaganda Week” and “Quality Month.”

Alibaba’s Jack Ma wants to read your mind.Reuters

The pains of trust-breaking

Before you start worrying about the caliber of the other 11 months of the year, you’ll be glad to hear that there’s also a strategy for enforcement. This includes informants, blacklists and the rather chilling promise that “those breaking trust will meet with difficulty at every step.”

Interestingly, the government is letting private companies, like Alibaba, the e-commerce giant that made US$1 billion in eight minutes the other day, take the lead in a series of pilot projects.

Alibaba’s finance arm, Sesame Credit, has been issuing customers with social credit scores based in part on their purchases and hobbies.

As Sesame’s technology director explained, someone who played hours of video games “would be considered an idle person,” so less creditworthy, while someone “who frequently buys diapers” is probably a parent, so “more likely to have a sense of responsibility.”

Suddenly that puts Nicolas Cage in Raising Arizona, running from the cops with a stocking mask over his head and a package of Huggies under his arm, in a whole new light.

Sesame has even launched a mobile phone game in which users can guess whether they have higher or lower scores than their friends. What could be more fun than seeing whether your friends are – literally – worth hanging out with?

This may all seem crazy, in ways both scary and silly. But before we get too smug about how it would be unthinkable here, consider the recent news about credit agencies “exploring new ways of assessing consumers’ ability to handle loans,” right here in the United States.

These include scouring “phone and utility bills, change-of-address records and information drawn from DVD clubs and suppliers of rent-to-own furniture.” And that’s just the well-known companies like TransUnion and FICO.

Start-up credit agencies and banks, reports The Economist, go even further, “piecing together scores by analyzing applicants’ online social networks,” monitoring their Facebook messages and determining whether they are spending prudently.

(Here we pause as I put down my phone, from which I was just about to order a gravy separator from Williams-Sonoma, in case I needed to separate gravy sometime. Suddenly, it just didn’t seem – what’s the word? – prudent.)

The credit agencies say that they are responding to a demand by their customers – the banks, which are looking for new sources of revenue and hoping to find it in people who previously had no credit score.

In China, diapers apparently means trustworthy. She deserves a loan.ReutersThese guys would have a tougher time getting credit.Reuters

Building a better citizen

So while we’re not subjected to a government effort to “build a better citizen,” as the Chinese are, we’re not doing much to prevent the private sector from conducting not-entirely-dissimilar data-mining investigations into millions of people too young, too poor or too new to the country to have traditional credit scores.

Ever since Target started using data-mining to predict whether female customers were pregnant (which explains why I received a can of formula, seemingly out of the blue, right before I had my first child), scholars have warned us about the many ways the private sector can use predictive analytics to figure out who we are and what they can sell us.

But even if it’s good business, there’s something odd about collecting all these disparate pieces of information – traffic violations, bills paid and unpaid, staying friends with your ne’er-do-well elementary school classmate, having children, playing Call of Duty: Black Ops III – and assigning the whole mess a single numerical score.

Reducing all aspects of social and consumer life to a single unit of value seems to fundamentally misunderstand the complexity of human experience. Maybe remaining friends with a childhood buddy with a poor loan history does reflect on your own financial creditworthiness. But that friendship might also point to other things about you – your past, your loyalty or your willingness to help those in need – that cannot be assigned a numeric value along the same spectrum as whether you paid your gas bill.

Maybe an authoritarian single-party state can’t be that concerned with the dignity and autonomy (let alone the privacy) of its citizens. But at least the Chinese plan has been publicly circulated. Its “you will be trustworthy – or else” message might be a little alarming, but it’s not like it keeps you guessing.

We can’t really say the same for our own shadowy system of credit ratings. And if the market requires it, how long will it be before we all get evaluated based on whether our purchases are of the “responsible adult” or “idle slacker” kind?

Better start stocking up on the Huggies.

Author: Caren Morrison, Associate Professor of Law, Georgia State University