On “Black Monday” October 19, 1987, the US stock market crashed, losing over 500 points and 22% of its value in a single day. At around the same time, R.E.M. had just broken through as a major act, and their song “It’s the End of the World as We Know It (And I Feel Fine)“ was playing everywhere, getting an extra boost from the events of the day.

In the US, it seemed the ostensible “Reagan era” was coming to an end. The still-evolving neoliberal economic order – based on valuing financial returns over wage increases as a source of demand – had been shown up. Asset bubbles were not to be trusted as a stable basis for an economic policy order.

However, a short-run solution would soon be found. Almost immediately, an untested, newly installed Federal Reserve chairman, Alan Greenspan, would flood the streets with money. The stock market would recover its lost ground over the next year, and resume its ascent – standing today at 15,871.

Since then, over the past 28 years, the global economy has run on bubbles. Since 1987, these have spanned the Mexican peso crisis, the Asian financial crisis, the “tech wreck” or “dot-com” bust, and the global financial crisis itself.

Most recently, just this past Monday, August 24, we have seen history repeat. On “Black Monday 2015″, China’s stock market lost 8.5% of its value. In turn, the People’s Bank of China has taken a page from the Greenspan playbook and flooded markets with money. One can expect the Federal Reserve and US government to approve – as they should. Now is not the time to follow the Euro playbook or worry about export competitiveness. As followed on each of the above crises, lending freely is the route to recovery.

However, one could be excused for wondering how we got here – addicted to bubbles and bail-outs. In this light, one can view the current market situation through three lenses, to get a successively broader take on where we stand today.

How we got from there to here

First, in the short run, a Chinese slowdown has been apparent for some years –- as has been an American recovery. In this light, some flight from Chinese markets and assets was to be expected –- leaving monetary policymakers facing the difficult challenge of engineering a global “soft landing.”

This dilemma echoes the Asian crises of the 1990s: when US growth increased in the mid-1990s, the Greenspan Fed raised interest rates. In response, investors shifted money from Asia to the US –- with early Asian declines over 1997-1998 assuming a self-reinforcing momentum. In recent months, the Yellen Federal Reserve has been aware of the danger of history repeating itself. In this light, Black Monday 2015 will likely see the Yellen Fed back away from its plans to begin raising interest rates next month. This should help revive global markets.

Secondly, in the middle run, China has itself faced over the past decade the challenge of overcoming what former World Bank President Robert Zoellick termed a “middle income trap” –- in which investment-led growth hits an upper bound. To move beyond that limit, China faces the challenge of promoting domestic demand as a new basis for sustained growth. However, measures that would enable such shifts might entail the strengthening labor unions and raising wages and prices – sparking the sort of inflation that Chinese leaders fear may undermine their legitimacy. In this light, we may know how to recover – but reform poses a bigger challenge.

Thirdly, over the long run, we can view this second “Black Monday” as demonstrating the extent to which asset-price bubbles are not a “bug,” but rather a “feature” of the current system.

Eat, drink, trade, repeat.Justin Lane/EPA/AAP

Over the post-World War II Keynesian decades, wage and price growth provided the foundation for sustained demand and growth –- at the ongoing cost of accelerating wage-price inflation. By the early 1980s, governments around the world sought to crack the back of inflation by breaking labour’s market power. For example, in the US and UK, Reagan and Thatcher employed recessionary policies and legal assaults to break unions. In Australia, the Hawke-Keating Prices and Incomes Accord sought a more negotiated route to wage-price stability. Yet, it ultimately took Paul Keating’s “recession we had to have” of the early 1990s to dampen wage pressures.

In this light, one might finally note that Paul Kelly-styled praise for 1980s-1990s market reform in Australia or similar claims for the alleged free market reforms of the Reagan-Thatcher years are more than a little misleading.

We do not live in an era of self-regulating markets. There is no substantive difference between the fiscal accommodation of the wage-price spirals of the 1960-1970s and the monetary accommodation of the asset-price bubbles of the 2000-2010s. In this light, just as Black Monday 1987 may have demonstrated the weakness of relying on asset-price increases to sustain growth, Black Monday 2015 –- coming seven years after the global financial crisis –- demonstrates the difficulty of constructing an alternative order, one that might enable stable growth.

Author: Wesley Widmaier, Australian Research Council Future Fellow at Griffith University

Stock markets all over the world followed China’s lead, plunging into the red and wiping hundreds of billions of dollars off of share values. But, while it’s tempting to lay the blame entirely at China’s door, a look at the global economy and markets shows Western markets have been overvalued and were due a correction.

Equities are risky assets and do not go up forever in straight lines, so corrections can be fast and furious at times. This acts as a useful reminder to investors that stocks are risky assets.

Stock markets in recent years have benefited from market-friendly monetary policies. There have been three rounds of quantitative easing from the Federal Reserve, the Bank of Japan and more recently the European Central Bank. There have for some time been concerns about the outrageous valuation of shares of certain US companies, including Facebook, Twitter, Tesla, GoPro, Netflix and Amazon. Both short-term and long-term interest rates globally have been artificially low for record periods. This unusual era of money printing and low interest rates has boosted asset prices – not just stocks, but also property prices in major towns and cities around the globe.

More interestingly, until this correction, the current bull market has been extremely unusual in that it has been one of the longest ever periods recorded (48 months) without a 10% correction in the S&P 500 index. The green candles in the chart below show the index being up for the month red candles represent it down for the month. The previous longest periods were October 1990-October 1997 (84 months) and March 2003-October 2007 (54 months). The large red candle at the end represents the most recent drop.

Monthly movements in the S&P 500 index from February 2009.XXXX

Another sign that US stocks had become overvalued was the fact that the price-to-earnings ratio, which measures a company’s current share price relative to its earnings per share, was approaching 19 to 20 times earnings – historically it averages 16.

Price to earnings ratio on the S&P 50.XXXX

If we were to use Robert Shiller’s ten-year cyclically adjusted ratio, the market is even more overvalued at 24 times ten-year average earnings, typically the long term average is 15. By giving a long-term average of earnings, the Shiller ratio better reflects a firm’s long-term earning power.

Prospective ten-year annual returns were likely to be in the region of just 1-3%, which is too low to compensate investors for holding risky assets. The recent fall in US and other stock markets will help improve future prospective US stock returns to a low, but more healthy, 3-5% range.

Ten-year average price earnings ratio on the S&P 500.XXXX

What about China?

The current sell-off is probably related to events in China – there, the stock market clearly entered bubble territory some months ago. Chinese stocks were rising despite the economy clearly slowing and it was selling at price-to-earning ratios that made no economic sense even if you believed in a 7% growth story.

The Chinese economy is in much greater difficulty than the Chinese government has been prepared to admit to date. That is why recent devaluations of the renminbi have been a catalyst for the recent global stock market correction. It is an admission by the Chinese that their economy is in serious trouble, and represents an attempt to boost the economy through an increase in exports at the expense of some of their competitors.

The Chinese economy is the second-biggest economy in the world after the US, so trouble there also spells trouble for the global economy. The attempts by the Chinese government to prop up their stockmarket were doomed to fail and in recent days this has become very clear.

Closer to home

Another reason for the global stock market sell-off is that the US Federal Reserve has been getting closer to raising interest rates from their artificially low target range of 0 to 0.25%. Some market participants are clearly trying to get out of the market before any rise, which is now unlikely to happen in September.

The low interest rates have led to US companies issuing record amounts of debt, not so much to finance future growth but to buy back their own shares to artificially raise their earnings per share. This can work in the short-run, but not in the long run. Raising the leverage (debt-to-equity ratio) of US stocks increases their riskiness and therefore their potential for volatility. This is precisely what we are now witnessing.

Three-month US treasury bill interest rates.XXXX

The obvious question is what the recent turbulence implies for investors and companies. Should they stay put, or be worried that we are facing a similar crisis to the 2007-08 crash? The good news is that US stocks are nowhere near as overvalued as in the 2001 and 2007 although they should be wary of some of the most obscenely overvalued stocks mentioned earlier.

The Chinese stock market remains overvalued (still some 60 times their earning value) and the economy is in deep trouble. Even US stocks are still highly valued using the Shiller measure. This means global stocks will remain under pressure.

The turbulence we have witnessed is likely to continue, but rallies both ways tend to happen very quickly. Interest rates remain extremely low and will act as a future drag on the market as and when they rise. Companies should also be concerned about a wider slowdown in the global economy hitting their earnings, as China is now the world’s second largest importer of commodities, goods and services.

Author: Keith Pilbeam, Professor of Economics at City University London

This week’s global sell down in stocks has been pegged to fears about the slowdown in China, but looks more like the effects of contagion.

In China, the Shanghai Composite fell by more than 8%, to levels below that which have previously triggered government intervention. The S&P/ASX 200 Index closed down 4.1% on Monday, and the Australian dollar hit a fresh six-year low at 72.69 US cents. The Tokyo Stock Exchange slumped 4.61% to its lowest level in six months, and markets in Taiwan and Hong Kong were also significantly lower.

Talk of a currency war has continued, with the suggestion that China is devaluing its currency against other Asian currencies in order to maintain its all-important export competitiveness. This implies some form of deliberate policy action, and in the modern era of Asian central banks I do not see that this is what is happening. Modern central banks, of which there are many in Asia, do not typically engage in this type of behaviour. Instead, what we seem to be seeing is evidence of reassessment and contagion.

Contagion is not transmitted by fundamental economic relationships. For example, if there is a fall in the oil price, we could realistically expect the value of the Japanese yen to fall (as an oil importer) and the value of the Norwegian kroner to rise (as an oil producer). Contagion, instead reflects deviations from these fundamental expected relationships.

When a market, “over-reacts” (or under-reacts) to a shock generated elsewhere, then this may represent the effects of contagion.

But commentators are sometimes a bit loose in their use of the term. Sometimes, they mean that the drop in the value of a currency will have real effects on another economy. For example, a drop in the value of the renminbi means competitive pressure on other economies in the region, resulting in some potential reduction in their expected future growth, and hence some fall in value of their currencies. This is what is known as a spillover.

The fact that we can articulate a channel for this effect makes it something we can anticipate, and we could perhaps even have bought a hedge against this risk in the financial markets. Contagion proper is not expected and as a result cannot be priced in the markets. Contagion may be based on investor behaviour – often spooked by fear.

The current currency uncertainty in Asia is a good case in point. To date, there is no real evidence of the currency war that had been feared by some commentators. Instead, lowered expectations for future growth, and to some extent concerns of portfolio holders have created falls in the value of other Asian currencies. That which is based on underlying fundamental linkages and is well-founded will remain, but where fundamentals are stronger than current market fears suggest, then we might well expect corrections.

Rebalancing in action

The reaction of global currency markets to the Chinese renminbi devaluation is mainly newsworthy because it was unexpected. In a manner rather reminiscent of the disbelief that Russia would defer payments on its debt in 1998 (because a nuclear power had never before done so), there was no expectation that the Chinese currency would change in such a ground-breaking manner. It then takes markets a little while to sort out their reaction. As it does, this will set up a new set of expectations around how transmissions work.

It is the changes in the network of the relationships between different currencies and countries that represent the contagion effect. Previously existing links between currencies, may be weakened in the longer term, perhaps as markets recognise the greater separability of some of the other Asian economies from the driving force of China. At the same time other links may form or strengthen, perhaps in the direct assessment of individual Asian economies by non-Asian investment markets.

This changing landscape of the transmissions between currencies represents the changing nature of the underlying economies, and our preferences in incorporating them into our portfolio decisions. The existence of contagion represents the stress that ensues when we recognise that our existing map of the linkages between economies is fundamentally questioned by new events. It is part of a transition arrangement as information is rearranged by the markets.

While the above sounds very sound, the problem with contagion is that it is often abrupt, costly and falls disproportionately.

My recent research shows how contagion transmits internationally, and identifies a number of different channels. More importantly, it illustrates the costs associated with contagion in the form of ensuing banking crises. We show that if there is contagion which has both systematic effects (affecting the common drivers of the currencies in the Asian region for example), and idiosyncratic effects (where the source of the shock causes a disproportionate reaction in a particular asset, such as perhaps the effect of the Chinese devaluation on the Indonesian rupiah) these channels are likely to lead to high fiscal costs of subsequent banking crises.

Indonesia has itself paid a high cost in the past for these crises – during 1997-98 it arguably had stronger fundamentals than those of other Asian economies, but it suffered extraordinary economic hardship in the period of recovery.

The question is what is to be done about contagion. The experts find this a very difficult issue. In some ways nothing can be done, markets must realign their expectations. But if there is significant volatility as a result of this, or a retraction of credit, there will be very real effects for the economy in reducing investor confidence. Detecting, preventing and managing contagion is an important component of the management of systemic risk for any economy.

Author: Mardi Dungey, Professor of Economics and Finance, Associate Dean of Research, Tasmanian School of Business and Economics at University of Tasmania

As another corporate reporting season in Australia draws to a close, the broad trend has been moderately underwhelming earnings results, combined with a rise in the earnings repaid to shareholders in the form of a dividend.

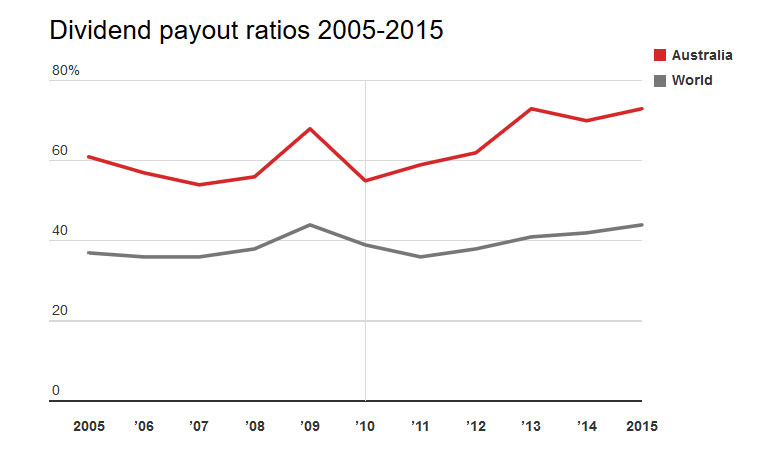

During this recent reporting period Australian firms returned, on average, 73% of their profits to shareholders as a dividend. This leaves only 27% of profits available to be retained in the firm to fund future growth.

As shown in the chart below, the ratio of profits paid out as dividends has increased in Australia from approximately 60% in 2005 to the current value of 73%. This result mirrors a recent international trend, however Australian firms continue to have high dividend payout ratios by international standards. The average firm around the world currently only returns 44% of profits to shareholders.

While many retail investors enjoy the regular revenue stream provided by the high yielding Australian equity market, this increasing trend in dividend payout ratios implies that dividends have consistently been growing at a faster rate than earnings; a phenomena that is not sustainable in the long-run and comes at the cost of economic growth.

A taxing issue

The large proportion of profits paid by Australian firms can largely be attributed to the imputation tax system, which was introduced in 1987 as a means of removing the double taxation of dividends. It allows companies to provide investors with a rebate for company tax that has been paid in the form of a franking credit attached to dividends.

Dividend imputation has achieved its intended aim of reducing the leverage of Australian firms. It’s an incentive for the use of equity rather than debt finance. Under the previous tax system, debt was more attractive than equity finance, resulting in the Australian economy having a large exposure to financial risk given the highly levered nature of many firms.

However, this reduction in financial risk has come at the cost of significant under-investment in the non-mining sectors of the Australian economy. The increased demand for dividends within an imputation tax system restricts firms’ access to their preferred source of financing: retained earnings.

The reinvestment of retained earnings creates multiplier effects that have a greater positive impact on the economy compared with dividends in the hands of individual shareholders. By retaining less of their earnings and under-investing compared with international counterparts, Australian firms run the risk of lagging behind.

Time for a policy fix?

Given the Australian government is currently focused on driving investment and growth in the non-mining sectors as the key mechanism for improving the current fiscal imbalance, consideration may have to be given to the future efficacy of the imputation tax system and the incentives it creates for large dividend payouts.

The imputation tax system is less relevant today than it was in 1987, given the increased integration between global markets and the growing reliance on international funding. As the tax benefits of the imputation tax system can only be accessed by Australian taxpayers, it creates a bias in favour of domestic investors.

For domestic superannuation funds with a marginal tax rate close to zero, the imputation tax system means they pay little, if any, tax on dividends, creating a big incentive for over-exposure to domestic equities. Given the structural changes that have occurred since 1987, the recent Financial System Inquiry noted that “the case for retaining dividend imputation is less clear than in the past”.

An alternative tax system that does not impose double taxation on investors while potentially reducing the current handbrake on economic growth is Singapore’s one-tier tax system. Under this system, profits are only taxed once at the corporate level. In Singapore dividends and capital gains are tax exempt. This simplified tax system reduces compliance costs and would ease the domestic investors’ current demand for dividends, and their associated franking credits, to be paid out.

Regardless of any taxation reform, investors need to be mindful that they can’t have their cake and eat it too with respect to dividends. The current trend of increasing the proportion of profits paid as dividends is not sustainable and has the potential to impede Australia’s long-run economic growth.

Author: Paul Docherty, Senior Lecturer, Newcastle Business School at University of Newcastle

Every now and then, I see an article in the media that is skeptical about the future of mobile advertising – the kind of ad you see when you open an app on your smartphone and there’s either a discount coupon at the center of the screen or a display ad at the bottom.

Many critics have asserted that mobile advertising does not work, that mobile marketing is all but dead and that people worry too much about their data privacy to accept these techniques on their devices and will not do so in the future.

Facebook’s latest quarterly earnings report may show that the social media network now earns a whopping 75% of its US$12.5 billion in annual revenue from mobile advertising, but even that does not seem to calm the naysayers.

Now the skeptics may start changing their minds, however, thanks to a number of recent rigorous studies that have systematically analyzed the effectiveness of different kinds of mobile advertising and marketing over the past few years in a wide variety of countries.

Using carefully designed field experiments, my colleagues, fellow scholars and I have consistently found irrefutable evidence that mobile advertising works.

More importantly, we have seen that 85% of users have willingly embraced the idea that marketers will reach them with an offer for the right product at the right time at the right place on the right device (smartphone). In fact, 49% of users are receptive to it and willingly sacrifice data privacy in exchange.

The question isn’t whether mobile advertising is effective, as I’ll show; it’s what factors make it more or less effective and make it more likely that a consumer will engage.

It turns out that various factors – such as location, time, weather and crowdedness – influence the effectiveness of mobile advertising, especially when done in the form of coupons.

A complex infrastructure

At the outset, it is useful to distinguish between mobile push advertising (a coupon sent in a text message) and pull advertising (an offer or message in an app such as Yelp).

From a functional perspective, pull advertising is similar to search engine advertising by presenting consumers with a list of coupons that are sorted by relevance in terms of location, prices or store ratings, allowing them to actively search for preferred options.

Conversely, the concept of mobile push advertising is more closely related to display advertising, in which users are either being targeted depending on their browsing behavior (behavioral targeting) or by the context of the website (contextual targeting).

Mobile ads work

A number of studies have demonstrated the effectiveness of mobile advertising in different contexts.

For example, Professor Yakov Bart and colleagues have shown that mobile display ad campaigns significantly increased consumers’ favorable attitudes and purchase intentions when they promoted products that were utilitarian (ie, need-based goods used for practical purposes) versus hedonic (ie, desirable goods that are used for luxury purposes). Similarly, Professor Sam Hui and colleagues have shown that targeted mobile promotions that incentivize people to travel more within a store can increase unplanned spending by as much as $21 per visit.

Studies by mobile app analytics companies like Flurry have shown that people are more than willing to tolerate ads and accept various forms of mobile marketing in exchange for cool apps. While consumers may not be in love with in-app advertising, their behavior makes it clear that they are willing to accept it in exchange for free content, just as we have on the internet for years.

The impact of geography, time, weather and context

Lets start with geography. In today’s location services-enabled smartphones, it is intuitive to expect that geographical targeting can increase product sales or at least brand affinity.

Research I conducted with my coauthors (Avi Goldfarb and Sangpil Han) in 2013 demonstrated that even when users interact with brands on social media platforms like Twitter, they tend to engage much more strongly with brands whose stores are in close proximity to where they are physically located at any given point in time.

In another separate study, my coauthors (Dominik Molitor, Martin Spann and Philipp Reichart) and I showed that the farther away from a store a user is when receiving a coupon, the less likely it will be redeemed. Increasing the distance to a store by one kilometer (0.62 miles) decreases mobile coupon response rates by between 2% and 4.7%.

It is also intuitive to expect that temporal targeting – the time a user is sent a certain type of ad – matters.

For example, sending a mobile coupon for a 50% discount on a beer on a Tuesday afternoon at 2 pm has a much lower probability of being redeemed than a 50% offer on a cappuccino at the same time and same location, after controlling for price.

Surprisingly, the sales impact of employing these two strategies (location and time) simultaneously is not straightforward.

A paper by Temple University scholar Xueming Luo and others draws on contextual marketing theory to show that when targeting proximal mobile users – those located near an event or store – the odds of a sale are higher by 76% for a same-day promotion compared with sending a promotion two days in advance.

By contrast, with non-proximal mobile users, they found that a little advance notice helped, but not too much. When a mobile coupon is sent out one day ahead of an event, the odds of a consumer purchase jumps 950% compared with a same-day text message and 71% compared with one sent two days ahead of time.

Basically, consumers who received marketing messages close to the time and location of an event formed more concrete mental construals – a term in social psychology referring to how individuals perceive, comprehend and interpret the world around them. That in turn increased their involvement and purchase intent, while more spatial and temporal distance had the opposite effect.

Even weather can impact the effectiveness of mobile advertising.

A 2015 study revealed how mobile purchases prompted by marketing were significantly higher on days with more sunshine and lower when it was cloudy or rained. Theories from psychology have argued better weather, both actual and perceived, induces better moods and causes an increase in risk tolerance or the willingness to part with cash. On the other hand, exposure to bad weather leads to poor moods and more risk aversion.

Finally, it turns out that our propensity to respond to mobile advertising is also affected by how crowded our environment is.

In a 2014 paper my coauthors (Michelle Andrews, Xueming Luo and Zheng Fang) and I showed that people are more likely to redeem mobile coupons when they are being physically squeezed in crowded contexts.

Based on a follow-up user survey that we carried out, this behavior can be explained by the phenomenon of ”mobile immersion”: to psychologically cope with the loss of personal space in crowded contexts, users can escape into their personal mobile space. Once there, they become more involved with the targeted mobile messages they receive, and, consequently, are more likely to make a purchase in crowded contexts.

For marketers, the high-level finding is that consumers may be more receptive to targeted mobile ads when they are in crowded spaces with strangers, whether in a subway car or even in a busy tourist area such as New York City’s Times Square.

Lip service to privacy

Here is the bottom line: we think we care about data privacy, but when it comes to redeeming offers on our smartphones, we actually pay it only lip service.

Put differently, an increasing proportion of people (especially millennials) understand that a give-and-take relationship is becoming more common as we interact with brands trying to sell us stuff.

We give our data to marketers (both willingly and inadvertently), and in return we expect to receive highly curated and personalized offers on our smartphones. Many consumers have even become resigned to the idea that they have little control over their data, and that this is the future of the world we will inhabit.

Does every form of mobile advertising work well? Of course not.

A banner ad that pops up and covers the already scarce real estate on our screen is not going to be nearly as well-received by users as an offer distributed via text message and triggered by a location-sensing beacon when we are up and about in a shopping mall.

For example, as you walk past Zara, your smartphone buzzes with an offer of 15% off any purchase from Zara and a 20% off any purchase from American Apparel. In our most recent paper, my coauthors (Beibei Li and Siyuan Liu) and I showed that consumers have a growing preference for these kinds of offline trajectory-based mobile advertising: they are yielding extraordinary high redemption rates and customer satisfaction rates.

There is a simple message for mobile marketers in all of this: consumers appreciate relevancy and context. So make that ad count. Work on your targeting. Don’t overwhelm us with too many notifications. Don’t abuse our trust.

The evidence clearly shows mobile ads are not going anywhere. As such, the future of mobile advertising looks incredibly bright to me.

Author: Anindya Ghose, Professor of Information Technology and Professor of Marketing at New York University

When the men and women of the committee which sets UK interest rates get together these days, they are dealing with a deceptively simple question. Rates will go up, but how far and how fast? Their answer will decide the fate of a fragile recovery.

You might well argue that the financial crisis was unnecessary; that the imposition of austerity meant that recovery was slower than it needed to be and that the burden of adjustment was unfairly shared. But notwithstanding this, the economy is recovering.

This means that interest rates also have to get back to normal. The most recent meeting of the Bank of England’s Monetary Policy Committee left things as they were – at a historic low of 0.5%, where it has remained since February 2008. It is both the lowest rate ever and the longest period without a change in rates. This cannot go on for much longer. We will get another rate decision on September 10 and even members of the committee who usually argue for lower rates, such as David Miles, are openly discussing the moment when the rate will start to rise.

Spent force?

But why do interest rates have to rise? Well, consider the choice between spending now or delaying expenditure into the future. In an economic downturn, the benefits of increasing spending in the present outweigh the costs of reducing it in the future. This is why low interest rates, which encourage spending right now, were a useful policy response to the financial crisis.

But in more normal times, low interest rates encourage levels of expenditure which may exceed the productive capacity of the economy and so cause rising inflation. They may also lead to excessive borrowing and so risk another financial crisis. Higher interest rates, which encourage saving that can be channelled into productive investment, are then more appropriate.

So, if interest rates have to go up in order to manage the transition to another kind of economy, how quickly will they rise? Here, policymakers face two major risks. The first is within the banking system.

Risk factors

Banks are holding more than £300 billion in reserves at the Bank of England. This has been a useful cushion in turbulent times (reserves increased recently during the latest Greek crisis) but going forward, the economy needs banks to make loans rather than accumulate cash.

As a first step, the Bank of England has to stop paying interest on these reserves. This will encourage banks to run down reserves and increase lending. But reducing bank reserves by, say, £200 billion will increase lending by roughly £2 trillion (economists call this the “money multiplier”: historically the multiplier has been around 10). Doing this too quickly risks destabilising the economy. So this suggests we will see a modest and gradual increase in interest rates.

The second risk lies with households and firms. Low interest rates have enabled some individuals to stave off bankruptcy by managing to keep up loan repayments. This will no longer be possible once interest rates start to rise. These are the so-called “zombie loans” that stalk the economy, and no one knows how many of these are out there, or at which point in the interest rate cycle they will become a serious danger. Caution again suggest a modest and gradual increase until the scale of the problem becomes clearer.

Level up

Finally, let’s consider how high interest rates will eventually rise.

Policymakers have suggested that the pre-crisis average of 5% may be too high. Why? First, it is not clear how much of the damage caused by the financial crisis is permanent. If the economy has sustained serious damage to its productive capacity, interest rates will need to stay low for a protracted period, until investment has rebuilt capacity.

Second, it has been argued that there are now fewer investment opportunities than there were before the crisis, as the wave of productive investments opened up by the rapid spread of globalisation and new technology has ebbed away, robbing us of opportunities to generate growth and support a robust recovery. This “secular stagnation” hypothesis argues for lower interest rates into the future.

Of course, these arguments are all about successfully managing the recovery of the domestic economy – and we know only too well that external factors, such as US sub-prime mortgages, can have devastating effects across the world. It will be a useful by-product of the expected modest and gradual rate rises from the Bank of England that if and when the next crisis strikes from out of the blue, then there remains the room to bring rates straight back down again.

Author: Chris Martin, Professor of Economics at University of Bath

Data is a new currency of sorts: we all generate a lot of it, and many companies already use it to serve their ends or ours. But, for many very good reasons, it’s not easy to persuade people that they should give their data away. There are more than enough surveillance scandals or data breaches to make an open approach seem like a bad idea.

A study commissioned by the Digital Catapult, a working group bringing together academics and industry – and conducted by a credit checking firm – concludes that consumers want new services that will allow them to collect and manage personal data, and that paying people to share their personal data creates new business opportunities.

The report suggests that people are eager to use their own personal data as a means to earn money: a majority of respondents (62%) said that they would be willing to receive £30 per month to share their data. But respondents could only choose between £2 and £30 per month – there was no option to opt-out and share nothing at all. Of course, if you’re facing a choice where you can earn something or nothing for your data that will be hoovered up anyway whether you like it or not, it’s hardly surprising that people choose the maximum available. It feels as if the rest who answered otherwise just didn’t understand the question.

So, it doesn’t mean personal data is worth £30 per month, and nor does it stand up the report’s claims of “£15 billion of untapped wealth for UK consumers”. This value is arbitrary, plucked out of the air and relative only to the limited choices people were offered. No doubt they’d not turn down £100 or £1,000 either.

The value of data, and to whom

The research I’ve carried out suggests that it’s hard to put a monetary value on personal data sharing – in some circumstances it is possible to estimate how much people are willing to pay to keep the data secure. The difficulty with assessing how much data is worth is because one person’s data tends only to gain value when it is aggregated with other people’s data. This makes it hard, if not impossible, to decide what a single person’s data is really worth – even if some attempts have been made to find a market price.

We carry more information with us than we realise.ter-burg, CC BY

In fact many people don’t really understand what their personal data is, how it is stored and used – and this is something the report backs up. Considering these difficulties, then, is it ethical to use cash incentives to persuade people to hand over their personal data? Do those doing so understand the potential implications, and should those offering the cash be required to explain?

Some stand to profit more than others

Let’s not ignore the fact that the study was carried out by a credit checking firm. The firms’ business is based on gathering considerable amounts of personal information from various sources and then selling it on to others, including the same organisations from which they drew the data in the first place and those people who have become records in their systems. They have access to many data sources that describe our lives, such as banking records, our home address, bills with various utility companies and the like. However, there are many other digital pieces of information about us which yet are not shared with credit checking companies.

Perhaps it’s no surprise that this report justifies the introduction of services that will allow third parties to collect and manage more of personal data that we produce. For example, a firm might launch a personal data management app that collates mobile phone use, GPS records, loyalty card data, health data from fitness apps and your NHS records, alongside charitable donations, social network data and productivity apps. Then it could offer the opportunity to share some or all of that data with them for a fee, paying you, for example, £30 a month, at which point almost everything about you, from work, physical health, habits and social groups, could be discovered and triangulated, and used by them for their financial benefit.

Risk vs benefits

While the report suggests such services might benefit the public good, the question is of who holds the reins: government, business, or the third sector? Having your data will directly benefit those in control of it, and those they sell or share it with – but would it benefit you?

Time will show whether this degree of data integration is beneficial at all. But given that people understand so little about how their personal data is created, gathered and shared – and the implications of all this – it seems simplistic to offer cash incentives for people to share the information that describes their lives in detail. That’s without even considering the many risks posed by collating so much information on individuals and storing it together – as tales of massive data breaches, losses, and abuses continue to remind us.

Author: Anya Skatova, Research Fellow, Horizon Digital Economy Research Institute at University of Nottingham

In an opinion piece in The Australian on Monday, Treasurer Hockey suggested that Australia collects too large a proportion of its public revenue through income tax.

He wrote: “The problem is we have an over-reliance on personal income tax to support our revenue base. Our largest source of tax revenue is personal income tax.”

And he went on to say: “When personal income tax is calculated as a proportion of total tax revenue, Australia’s taxation level is the second highest among OECD countries.”

At first sight, his assertion certainly checks out. Initial analysis of the OECD statistical database reveals that of the OECD countries, only Denmark collects more of its revenue through taxes on individuals. On average personal income tax comprises about a quarter of public revenue in OECD countries, while in Australia it is closer to 40%. A comparison across OECD countries is shown in Figure 1 below.

http://stats.oecd.org/

But this finding needs to be seen in context. While there is a widespread public perception that Australia is a high-taxation country, the reality is that Australia is one of the more lightly taxed of all developed countries. In 2013 (the latest year for which comparative data is available), Australian taxes across all tiers of government were 27% of GDP, compared with the OECD average of 34%. Of the tax we do collect a large proportion is in the form of personal income tax, but because our total collection is low, income tax forms a large proportion of that amount.

When we re-analyse the same data to consider income taxes as a proportion of GDP a different picture emerges, as shown in Figure 2. At 11% of GDP, our dependence on income tax is above the OECD average of 9%, but it is significantly lower than in many other OECD countries.

http://stats.oecd.org/

What is notable from Figure 2 is that more prosperous countries in general tend to be reliant on income taxes. While the OECD is traditionally seen as a “rich countries’ club”, expansions of its membership over recent years have brought that generalisation into question. It now includes Chile and Mexico, many eastern European countries re-establishing their economic bases after decades of central planning, and the struggling Mediterranean countries.

When analysis is restricted to a high-income OECD countries – those countries with per-capita incomes above $US36,000 – a different picture emerges, as is shown in Table 1. At 10.7% of GDP, Australia’s income tax revenue is about on the average of these countries (10.5% of GDP).

It is understandable that prosperous developed countries rely comparatively heavily on personal income taxes. They generally have a significant middle class, they have taxation authorities with the capacity to ensure a high degree of compliance, and their wealthier citizens aren’t about to emigrate to find better places to live.

This brief analysis is a reminder that we need to be wary of politicians’ broad statements on taxes. There is a political temptation to set the scene for income tax cuts in a pre-election budget, but, given Australia’s general low level of taxes and high fiscal deficit, the more compelling question should be about improving our public revenue.

Author: Ian McAuley, Lecturer, Public Sector Finance at University of Canberra

Fintech firms are infiltrating all areas of financial services, from payments platforms, lending, capital raising, investment, advice, insurance to capital markets.

Fintech firms, which are essentially disruptive digital finance models, can help lower barriers to entry in financial services. They are also reducing transaction costs, addressing issues of information asymmetry, empowering consumers and facilitating international linkages. All these contribute to the regulatory goals of efficiency and fairness.

Around the world governments have responded positively to the new models, recognising the benefits of driving competition, and increasing access to markets, especially in areas such as small business finance. Models such as peer-to-peer lending and Crowd Sourced Equity Funding (CSEF) have been welcomed in the US, Europe and the UK.

Governments in the UK, Canada and New Zealand have either implemented or are finalising the implementation of regulatory regimes to support CSEF. In the US, the enactment of the Jumpstart our Business Start ups (JOBS) Act, which referenced the importance of online funding for start-ups and other companies to raise capital, was pivotal for CSEF globally.

But facilitating the practical move to market of new digital finance companies is a challenge for both the fintech firms and regulators.

Compliance challenge

Young fintech companies with limited resources face a significant hurdle navigating the maze of regulatory licensing and compliance requirements. Much of this has been developed for far more mature and larger organisations.

On the other hand, regulators struggle to balance openness to innovation and disruptive technologies with protecting the interests of consumers, investors and the privacy of individuals.

The United Kingdom has led the way in many respects. The Financial Conduct Authority has established a network called Project Innovate which supports industry innovation to improve consumer outcomes. The UK fintech industry also has its own industry body, Innovate Finance, to support technology-led financial services innovators.

In Australia, it’s the Australian Securities and Investments Commission that’s tasked with licensing and monitoring fintechs. This needs to be done with a keen eye also on the need to enhance competition in the system and build confidence in the new models to ensure participation by both investors and consumers.

To assist in this process ASIC has developed an “innovation hub”. This is a single point of entry to the system for innovators seeking to gain regulatory approval and thereby make it easier for them to navigate the regulatory system.

Collaborative approach

The innovation hub can be linked to a growing realisation that collaboration is required between financial sector innovators, consumer groups, academics, relevant government agencies and regulators to deal with complexity and examine opportunities from a system-wide perspective.

Accordingly ASIC has also announced the establishment of a Digital Finance Advisory Committee, with representation from the fintech community, consumers and academics. The focus is on streamlining ASIC’s approach to facilitating new business models with common application processes, including applying for or varying a licence and in granting waivers from the law.

These initiatives represent a significant departure for Australian regulators for two key reasons. First, our regulatory agencies have tended to retain a low-risk, conservative approach to regulation. On an international basis, this stood us in good stead throughout the global financial crisis, when our regulatory agencies were recognised internationally for their prudent approach. But this had increasingly become a barrier to innovation.

Second, this is a highly collaborative approach, something that is generally not a hallmark of Australian business. The lack of collaboration has been a weakness of our system in generating interaction between researchers, innovators, corporates and regulators and we have been amongst the least collaborative of all OECD countries, to our cost. Bringing together these parties through the Digital Finance Advisory Committee, and fintech hubs such as Stone and Chalk, could lay a foundation for more sustainable financial services innovation.

Opening the way to greater financial innovation is especially important in an economy with such a highly concentrated financial sector.

Ultimately the ability of key agencies to adapt and adjust risk levels to accommodate disruptive technologies will impact on both the domestic and international competitiveness of Australian finance sector, to the benefit of Australian consumers and businesses.

Author: Deborah Ralston, Professor of Finance and Director at Monash University

The 14-year sentence handed to Tom Hayes, the Yen trader at the centre of the Libor-fixing scandal in the UK, is the longest sentence yet in a scandal that has cost his former employer UBS, and others, US$17 billion in fines.

Apart from his obvious guilt, Hayes went out of his way to antagonise the Court, and the Judge.

Hayes, described as the “Machiavelli of Libor”, will not be the last to suffer the consequences of this fraud. Unfortunately, however, it appears bank executives will not be among those punished. And this is curious. UBS either knew, turned a blind eye, or had such weak internal controls that Hayes was able to perpetrate this fraud for three some years.

UBS was no doubt motivated, in part, by the US$260 million Hayes made for it. All the while he was being courted by the usual suspects: Lehman Brothers and Goldman Sachs.

He then fell out with UBS, over pay, and joined Citibank. Within a year Citibank had discovered his fraud. What at UBS we were led to believe remained undiscovered for in excess of three years, Citi sacked him for.

Along with Libor fixing went the obligatory “Bollinger by the case” lifestyle, amply supported by a perverse incentive structure. Hayes claimed in testimony that his managers were well aware of what he was doing. Indeed one trader remarked “mom Teresa would have rigged Libor had she been trading it!”.

Tactically, Hayes was no genius. He gave 80 hours of sworn testimony to the Serious Fraud Office (SFO) as part of a plea deal. He then decided to renege on that deal, and plead not guilty. But he failed to make the admissibility of the testimony contingent upon the plea deal. So he was left pleading not guilty, facing 80 hours of his own testimony.

ASIC’s role

In Australia the Australian Securities and Investments Commission (ASIC) is investigating rigging of the bank bill swap rate, as well as misconduct in the forex rate. True to form, ASIC is again taking a “light-touch” approach, appealing to bankers’ better nature, despite the gathering storm in the community and the rage sweeping the Senate select committee.

ASIC obviously cannot read the writing on the wall, or seems unable to understand its remit: to enforce the law, with prosecutions if necessary, not gentle cajoling. The result is systemic fraud taking root within the financial system. Individual investors lose. As does every trader and banker who is honest and doing the right thing.

ASIC Chairman Greg Medcraft has expressed his frustration that banks are adopting an overly legalistic approach. But he neglects to mention the very substantial power that ASIC possesses. This includes the power to search, to seize, to eavesdrop, to enter, to inspect, to compel disclosure. Nor does he mention that ASIC has substantial resources, and could quite easily target one bank, or one trader, to make the point that rigging interest rates will not go unpunished.

This comes on top of a litany of failures from ASIC to enforce the law: the financial advice scandals at CBA, NAB and Macquarie, front-running and insider trading at IOOF, and now interest rates. As my colleague Pat McConnell wrote recently in The Conversation, most of the compliance being compelled in the financial industry is not thanks to ASIC, but the result of investigative journalism from “one-woman regulator” Adele Ferguson.

Josh Frydenberg, assistant Treasurer, has announced a review of ASIC. But the review will not accept submissions, so is hardly consultative.

Having worked for ASIC’s sister organisation and bank regulator APRA, I can attest to cultural impediments within government that do not take kindly to criticism, and are deeply resistant to anything that challenges the prevailing orthodoxy. Disappointingly, these were exactly some of the criticisms levelled against APRA after the collapse of HIH. On that occasion the Royal Commission called for changes to APRA that would reform the culture of the bank regulator. For a time APRA seemed genuinely engaged in this project. But it has long since fallen back into old habits: civil service mandarins more concerned with building personal empires than building resilience in the financial system.

It’s time for the creation of a Financial Regulator Assessment Board, in line with a recommendation (27) from the Financial System Inquiry. Nothing short of an ongoing, independent review of the corporate cop will stop Australia’s slide into systemic corruption. A board, comprised of wise women and men, not connected to government (Treasury, the RBA, APRA or ASIC), and who have no skin in the game, are more likely to provide the kind of over the horizon views of financial system challenges, than are hand-picked bureaucrats, picked by the assistant Treasurer.

Some might view the establishment of such a board as duplication. Which in some ways is exactly what it is.

But in aircraft engineering duplication is called “double-redundancy”. In other words, when one system fails, a second, back-up system picks up where the first, failed system left off. This is exactly what a Financial Regulator Assessment Board could do for the financial system.

Must we wait for a financial crisis before this idea is implemented?

Author: Andrew Schmulow, Senior Research Associate, Melbourne Law School. Visiting Researcher, Oliver Schreiner School of Law, University of the Witwatersrand, Johannesburg. at University of Melbourne