Between 2001 and 2010 roughly 1.7 million Australians dropped out of home ownership and shifted back to renting. More than one-third did not return by 2010. These statistics, from the Household, Income and Labour Dynamics in Australia (HILDA) survey, reflect increasingly insecure jobs, the prevalence of marital breakdown and lone person households, widening income inequalities and the high levels of debt accompanying spiralling real house prices.

Rather than climbing a ladder of housing opportunity that heads in an upward direction only, a growing number of Australians are precariously positioned on the edges of home ownership. We can think of the edges of ownership as a permeable, contested border zone between owning and renting, where households juggle their savings, spending and debt as they attempt to retain a foothold on the housing ladder.

And according to new research comparing Australia with the UK, policy settings play an important role in determining who can and can’t manage to stay in the home ownership game.

The research used three panel surveys – the HILDA survey, the British Household Panel Survey (BHPS) and its successor Understanding Society. We tracked the ownership experience of 1,907 Australian and 674 British individuals that began periods of home ownership between 2002 and 2010 (a period that covers the enormous disruption caused by the global financial crisis). In each year we have recorded their tenure status.

The figure below shows the proportion of people exiting ownership year on year as a spell of ownership lengthens (the maximum spell length in this study being 8 years). For example, 8% of those Australians that had managed to sustain three consecutive years of ownership shifted into the rental sector in the following year. In contrast, 6% of British home owners transitioned into rental housing after three successive years of ownership.

Despite the turbulent British housing market conditions, and a more serious economic recession following the global financial crisis, Australians’ experiences of home ownership appear more precarious. In fact, in all but one year the exit rate is higher in Australia. For a randomly selected Australian moving into home ownership between 2002 and 2010 the chances of “surviving” as a home owner beyond seven years are only 59%. The chances of “survival” are somewhat higher at 68% in the UK. The edges of ownership appear more permeable in Australia.

Exit rate Australia and UK, 2002–2010

Authors’ own calculations from the 2002–10 HILDA Survey, 2001–08 BHPS and Understanding Society wave 2.

For a minority of individuals in the surveys, labour market mobility might be a factor encouraging a temporary shift out of ownership, as people relocate to take advantage of job opportunities. However, it is clear from the data that the majority of moves out of home ownership are related to financial stress. For example, 15% of those Australians leaving home ownership reported difficulties in paying utility bills in one or more years before exit, while only 7% of those with enduring ownership spells reported such difficulties. 9% of departing Australians fell behind on their mortgages, but only 2% of those with enduring ownership spells testified to such difficulties. Similar patterns are revealed in the British data.

This is no surprise. What is striking is that financial stress is more likely to cause a loss of home ownership status in Australia than it is in Britain – a puzzling feature of the findings which cannot be explained by differences in the personal characteristics of Australian and British members of the panels. If, for instance, ownership reached further down the Australian income distribution we might expect more insecure housing experiences among Australian home buyers. But controlling for these possible differences does not explain our results.

Why is Australia different?

There are instead signals in the data which suggest institutional differences across the two countries are at play. There are two factors that could disproportionately draw marginal Australian owners into the rented sector, while propping up the ownership ideals of their British counterparts.

First, and most obviously, the rental sectors of the two countries are quite different, and appear to have a different function at the edges of ownership. The higher likelihood of exit from ownership in Australia may reflect the role of the larger unregulated Australian private rental sector in “oiling the wheels” between renting and ownership. The size, geography and diversity of the Australian private rented sector make it relatively easy for households to adjust housing costs to income by moving before mortgage stress becomes excessive.

Arguably, therefore, renting performs a risk management role, offering temporary, relatively easily accessible, refuge for those on the edges of home ownership. From this perspective, the earlier exit of Australian households who experience financial stress may be seen as the product, in part, of a well-functioning housing system in which the rented sector offers a general safety net. This does occur in the UK, but to a much more limited extent, via a small social rented sector which offers a ‘soft landing’ for households with some very specific (largely health-related) housing needs.

Second, however, there are differences in the two countries’ social security systems. Historically, British home owners with particular financial needs (such as the loss of all earned income) have been eligible for what is now known as support for mortgage interest (SMI). This may postpone or prevent the need to sell up. There is no such safety net for mortgagors in Australia.

Whether, in the long run, either institutional “solution”(growing the rental sector or subsidising mortgagors at risk of arrears) is satisfactory is a topic for policy makers to discuss.

Other options include shared ownership and equity share, which, if provided at scale could offer an escape valve for financially stretched home owners, perhaps improving on the diversity offered by the Australian private rental sector.

On the other hand, if households in either country have the need or appetite to swap the costs of owning for those of renting or shared ownership regularly or routinely, then it must be time to consider the financial instruments that might enable them to do so without incurring the massive transactions costs, and domestic upheaval, of selling up and moving into a rental property.

Authors: Gavin Wood, Professor of Housing at RMIT University, Melek Cigdem-Bayra, Research Fellow at RMIT University, Rachel On, Principal Research Fellow, Bankwest Curtin Economics Centre at Curtin University, Susan Smit, Honorary Professor of Geography at University of Cambridge.

Agreement on the controversial Trans-Pacific Partnership could come as early as this week, with negotiations now focused on “the last few issues,” according to Trade Minister Andrew Robb.

Movement towards finalising the TPP comes as unions step up a campaign supported by Opposition Leader Bill Shorten against what is seen as anti-labour provisions in the China-Australia Free Trade Agreement, taking political debate over free trade to a new level.

“Dry” economists on the right don’t like “trade distorting” bilateral agreements (they don’t even like calling them “free trade” agreements), while many on the left are concerned about trade agreements going too far, beyond reducing tariffs and quotas, and getting involved in social policy, labour standards and the provision of public goods.

But even beyond the political debate, there is the question of what Australian businesses want from public policy as they engage themselves in global markets.

The DHL Export Barometer gives us a pretty good handle on what exporters think. It surveys 600 Australian exporters annually, and has done since 2003.

For the most part, trade agreements have traditionally played a small part in impediments to exporting. Most businesses worry about the exchange rate – when it is too high their goods and services become expensive, when it’s too low their input costs soar (as 80% of exporters also import). They also worry about border regulations and business culture differences. For the most part they didn’t think about FTAs and certainly not the GATT or the WTO.

But in the DHL Export Barometer for 2015, there’s good news about free trade agreements, which will be music to the ears of Andrew Robb.

In surveying existing and new agreements there is evidence that exporters like Australia’s FTAs and that they actually work in a practical business sense despite the recent controversy.

According to the DHL Export Barometer, the USA FTA (AUSFTA) is at last helpful after a decade of implementation. Other agreements deemed helpful include those with New Zealand, Singapore and ASEAN. The survey finds AUSFTA is benefiting exporters, with increased sales and a larger proportion of exporters claiming the agreement has had a positive impact on their business (55%).

This occurred despite the USA hitting the sub-prime crisis just three years after the deal was forged in 2005. The US unemployment rate has now returned to pre-GFC levels, notwithstanding the commentators who predicted that the AUSFTA would “kill a country” (I assume they meant Australia).

The support for AUSFTA was followed by that for New Zealand (47%), AANZFTA – the agreement between Australia, New Zealand and ASEAN on 41% and Singapore on 38%.

The new “trifecta” of FTAs – Japan, South Korea and China – has got the endorsement of the Australian exporter community. In fact, Japan is more beneficial than expected and all FTAs to North East Asia are enticing new exporters. Some 61% of exporters think the China FTA will have a positive effect, 36% think South Korea will and 35% think Japan will deliver.

In terms of the Japan FTA, 59% thought the trade pact would increase exports to that destination, and 38% thought they would start exporting to Japan as a result of the FTA. Many also thought the FTA would help enhance an online presence and help develop new products and services for that destination.

In terms of future FTA destinations, exporters think that India, Indonesia, the Gulf Co-operation Council and Latin America should now be on Andrew Robb’s dance card. But of all the future pacts, India drew the most negative ratings, consistent with the view about increased competition from India.

Perceptions matter

But what about the controversial TPP? It received a positive response among exporters, with 69% saying they’d increase exports to TPP countries and 25% saying they’d start exporting to TPP countries as a result of the TPP.

But the TPP has some complications not always apparent in up and down trade deals, including the investor provisions that have been controversial in other jurisdictions. As Princeton economist Dani Rodrik pointed out in his book “Has Globalisation Gone too Far?”, when trade agreements stray onto the turf of the provision of public goods, or legislation like plain packaging for tobacco, they are likely to lose public support.

Even in the China FTA the labour market provisions have overshadowed the benefits the overall agreement would bring. And it is important to remember Rodrik’s finding that economies that are open to trade have well developed labour market institutions and social insurance.

This is reflected in my own research that showed that exporters, on average, paid 60% higher wages than non-exporters, provided better levels of occupational health and safety, more education and training, equal opportunity provisions and were more likely to be unionised.

The research has shown free trade can grow side by side with union support. An open economy is bolstered by improvements in productivity, efficiency and fairness in the labour market. These are important lessons to heed as we strive to benefit from the next round of FTAs.

Author: Tim Harcourt, J.W. Nevile Fellow in Economics at UNSW Australia

The ostensible purpose of the 2015 Intergenerational Report is to ensure Australia’s future prosperity in the face of demographic ageing over the next 40 years. Its real purpose is different.

The Coalition won the 2013 election as the party of economic management, a party that would balance the books after years of Labor profligacy, hence the 2014-15 budget cuts. The report uses the alleged ageing crisis to legitimate these budget cuts, as well as a high rate of immigration-fuelled population growth.

Thus it focuses on the costs of ageing. But our new research shows it makes three claims which are overstated to the point of being deliberately misleading. This is important as the IGR is being used as a basis for far-reaching policy decisions.

First, on page 1, the IGR says labour force participation will fall because the number of people aged 15-64 for every person 65 plus will drop from 4.5 today to just 2.7 in 2055. This fall will reduce per capita economic growth.

Second, the cost of providing health care, pensions and aged care for an older population will balloon.

Third, because migrants tend to be young, Australia must maintain high immigration. The authors project annual net overseas migration (NOM) of 215,000 from 2018-19 to 2054-55. This is a large number; from 1990-91 to 2005-06 the annual average was 95,000.

Together with natural increase, it will inflate the population from 23.8 million today to 39.7 million, an increase of 15.9 million, or 66.8%.

Claim 1: ageing and Australians’ future prosperity

Per capita economic growth is the product of the population, participation and productivity. The report’s calculations of their respective contribution are set out in in Figure 1. The main driver is productivity, projected to contribute 1.5 percentage points each year.

Source: ABS cat. no. 5206.0, 6202.0 and Treasury projections

The chart shows a slight fall in per capita economic growth from declining labour force participation of 0.1 percentage points a year. This is a big surprise. Despite the up-front assertion about ageing’s negative impact on participation, the effect turns out to be minimal.

An even bigger surprise is that the chart shows a 0.1 percentage point annual increase in per capita economic growth from population. This is because the proportion who are children will fall relative to all those aged 15 plus.

This positive effect is astonishing. Treasury’s own modelling shows that the ‘population’ effect cancels out the small labour-force participation effect.

Claim 2: budget costs

The report projects a substantial increase in health expenditure. But most of this is due to rising costs in providing health care for everyone. The online chart data for chart 2.11 makes this clear; only 16% of the projected increase is due to ageing.

Scares about pension costs and aged-care funding are similarly exaggerated. Pension payments currently equal 2.9% of GDP. Depending on policies, this percentage may fall to 2.7 by 2054-55 or rise to 3.6 (p. 69). And government expenditure on aged care may rise from 0.9% of GDP in 2014-15 to just 1.7% in 2054-55 (p. 71).

These two sets of figures are hardly startling. Indeed Australia spends a much lower proportion of GDP on age pensions than most OECD countries; in 2007 the OECD average was 7% of GDP.

Claim 3: the economic gains from high net migration

The report asserts that high migration results in a younger population than would be the case without it (p. 11). To bolster this claim it presents an arresting bar chart.

Source: ABS cat. no. 3101.0 and 3412.0.

But oddly the authors don’t quantify the difference and its long-term effects.

To fill this gap we used two ABS projections (with slightly different assumptions to those of the report) and estimated the difference that a NOM of 200,000 p.a. makes to the median age in 2055. We found that it produces a median age of 41.4. By comparison, no net migration over the next 40 years results in a median age of 46.1.

(The two projection series used here are series 38 (NOM 200,000 p.a, TFR 2.0, high life expectancy) and series 56 (Nom 0, TFR 2.0, high life expectancy). See data published online with Population Projections, Australia, 2012.

This minor “younging” effect is assumed to increase participation (page 20). But our research (p. 6) shows the report’s own data shows that this has a negligible impact on per capita economic growth. For example, an extra 70,000 net migrants per year until 2055 adds four million people but only increases per capita economic growth by 0.06%.

But the report’s goal is an extra 15.9 million, not four million. What about the infrastructure costs? Here it makes the bizarre claim that infrastructure costs “are not linked explicitly to demographic factors” (page 57).

Two hidden agendas

Demographic ageing does not impose heavy costs. Rather, the phony scare campaign has been used to justify the Coalition’s budget cuts, while the high NOM assumptions help justify its current immigration policy.

The government is desperate to find a short-term solution to the problem of lower economic activity post the resources boom. Population growth boosts the housing and city-building industries and this may help, not with per capita economic growth but with aggregate economic growth.

The latter is the key driver of tax revenue and, in the case of business, of growth in sales. The report does not say much about it, except to provide the results of its modelling. Here aggregate GDP is projected to grow by 2.8% per annum to 2054-55. (Page 27.) The IGR’s data shows that, while gains in productivity will make a substantial contribution to this, crude population growth accounts for nearly half.

Why worry?

The IGR does devote a few pages (See page 38) to the environmental implications of its population growth, conceding that careful management will be required. But it finds no serious costs for the Commonwealth as the “level of Commonwealth Government spending on the environment is not directly linked with demographic factors” (page 40).

So Treasury is off the hook. But all Australians will suffer from the impact of massive population growth on the environment and the alienation of agricultural land. (See contributions from Rhondda Dickson, Michael Jeffrey and Gary Jones in Sustainable Futures: Linking population, resources and the environment].

The other pressing concern for voters is jobs and the economy. What are the newly arrived migrants going to do, apart from build houses for each other?

The supposed economic ill-effects of ageing are trivial. They should be easily managed by future generations themselves, provided they are not overwhelmed by the costs of bloated cities and environmental decay.

Authors: Katharine Bett, Adjunct Associate Professor of Sociology at Swinburne University of Technology; Bob Birrel, Researcher, Centre for Population and Urban Research at Monash University

Discussion of an increased GST at this week’s leaders’ retreat is based on two motivations.

Firstly, state governments expect future structural budget deficits if they are to meet growing outlays for expenditure on health, education and the national disability support scheme.

Second, as argued in the 2010 Henry Review and the current Re:think review, tax reform including an adjusted GST would contribute to a more productive and larger economy. A larger economy directly means more taxation revenue. Also, a larger economy is required to support entrenched community aspirations for more and better government services as well as more private expenditure.

There are pros and cons to a larger GST. On the positive side, relative to income tax and state stamp duties, a broad based consumption tax is a less distorting and costly tax to raise government revenue. On the negative side, a GST is a regressive tax which is passed forward to households as higher prices.

Balancing the pros and cons of a larger GST requires a package of tax changes, as was the case with the introduction of the GST in 2000.

The package would include:

a larger GST, involving a broader base, a higher rate or both

the replacement of existing high distorting state indirect taxes, including stamp duties

the recycling of some of the increased GST revenue as higher social security rates and a lower and more progressive personal income tax rate.

The latter would offset the regressive distribution effects of the GST. Specific details of the reform package should be topics for detailed assessment and then community discussion.

Manage the fairness issue

GST funds collected by the Commonwealth, net of administration costs, are currently distributed as general purpose, or non-tied, grants to the states (and territories). The allocation formulae is designed to meet an equity objective so that if each state applied a similar tax system it could provide a similar level of services to its citizens, referred to as horizontal fiscal equalisation (HFE).

The base of the current GST represents just under a half of a comprehensive measure of consumption expenditure. New Zealand’s GST is more comprehensive.

In Australia the main exemptions are fresh food, education, health, child care, water and sewage, and imports valued at less than A$1000. While these exemptions provide an element of progressivity to the GST, the effect is relatively small. Lower income households in general allocate a larger share of their expenditure to the exempt items. But, higher income households spend many more dollars on the exempt items.

The progressive income tax system and the means tested social security system are better targeted and more effective ways to redistribute income to meet social equity objectives.

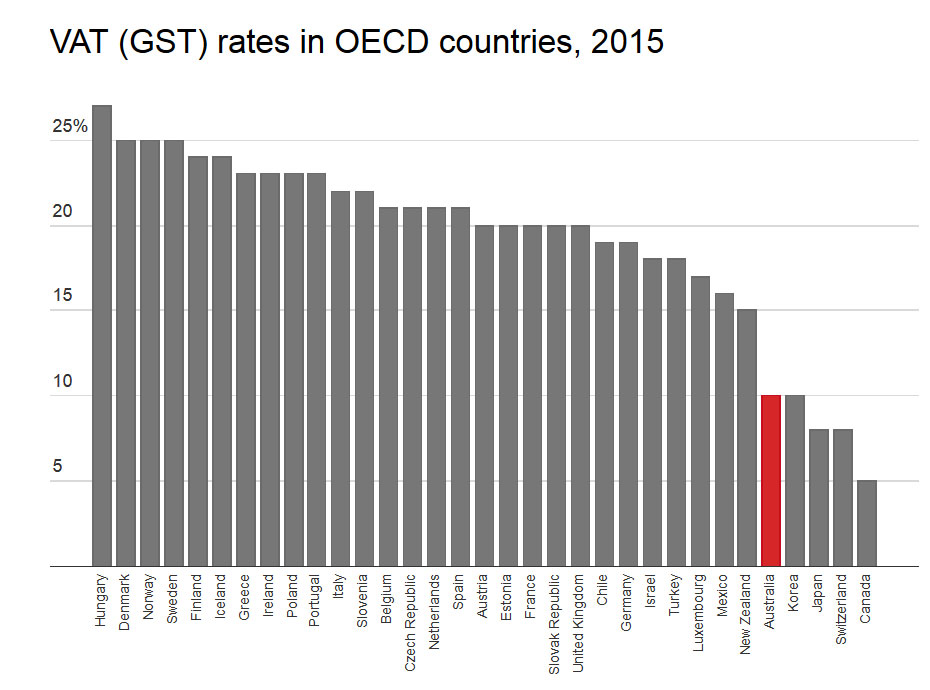

Australia’s 10% GST rate compares with 15% for New Zealand, and above 20% for many European countries.

Broaden the base

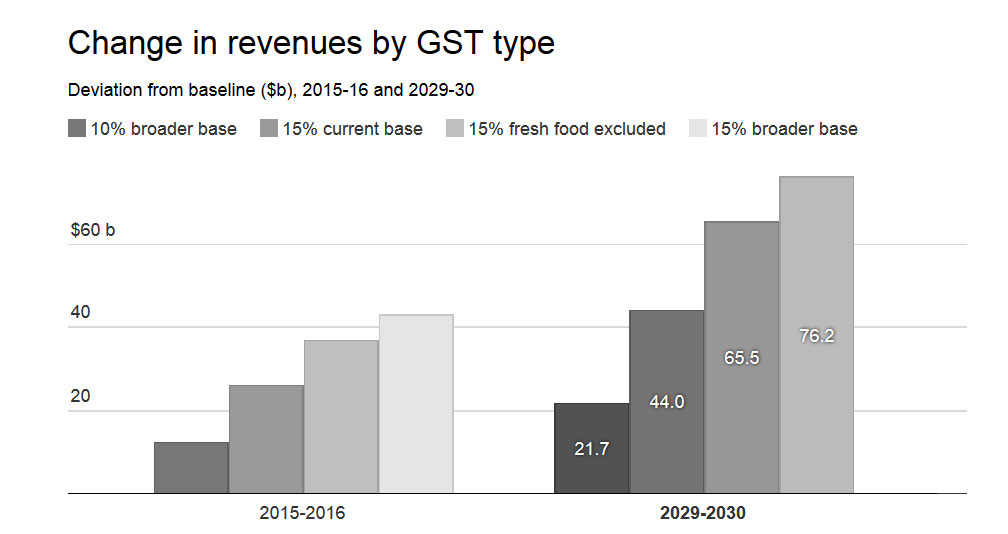

Additional GST revenue could be collected if the base was broadened by removing some to all of the current exemptions, by raising the rate, or both. Either option could generate a similar additional revenue stream. For example, removing all exemptions would double the revenue stream, as would a doubling of the rate to 20%.

In terms of efficiency and simplicity, the base broadening option has the advantage.

On an equity basis, there is little difference between an approximate revenue neutral larger GST tax base and a larger GST tax rate. Why treat a necessity food now exempt different to a necessity clothing now taxed, or a utility electricity now taxed but not water now exempt?

While the current exemptions from the GST base add an element of progressivity to the GST when compared with a comprehensive base, the redistribution effect is small.

The main categories of GST exempt spending are fresh food, health, education, rent, and financial supplies.Re:think discussion paper – Treasury estimates using ABS 2011, Household Expenditure Survey 2009-10, cat. no. 6530.0, ABS, Canberra

More importantly, appropriate increases in social security rates and reductions in lower income tax rates as a part of a tax reform policy package are more direct and better ways to achieve distributional equity with a broader tax reform package.

Scrap inefficient state taxes

The revenue gained from a larger GST could be used to replace more distorting and inefficient state indirect taxes. A revenue neutral package would generate large productivity gains and some simplicity gains with minimal changes in equity and distribution of the aggregate tax burden.

State taxes that should be replaced include stamp duties on insurance, and perhaps a component of a wider reform package to replace conveyance duty on the transfer of property with a broad base and higher tax rate on property. Both the ACT and SA have begun a reform package to replace conveyance duty.

A GST reform package would change Commonwealth-state financial relations. Government leaders would have to resolve both the split of aggregate revenue from the reform package between the commonwealth and the states, and then the distribution of the aggregate revenue gain to the states between the different states. Clearly, there would be very different views about the plausible options to do this.

Author: John Freebairn, Professor, Department of Economics at University of Melbourne

Even before the government’s options paper on tax reform is released later this year, many reforms have been taken off the table, at least before the next election. Here’s the expert view on six.

Broadening or increasing the GST

Some experts say expanding the GST, which is a regressive tax, would unfairly hit middle-income earners and women. Others say a broader base, not higher rate, would be the best approach.

If done as part of a package of tax reforms, John Freebairn argues increasing the GST could actually boost our standard of living.

Fixing the asymmetry between negative gearing and capital gains tax

As Helen Hodgson has explained, negative gearing would be less attractive if the capital gain on the sale of an investment was taxed in full.

The Henry Review recommended reducing the benefit of negative gearing by allowing only a 40% capital gains discount, but this was rejected by then Prime Minister Kevin Rudd.

Antony Ting says negative gearing is not a fair tax policy – particularly when considering the way investment properties are treated.

Dale Boccabella says the best solution would be to quarantine negative gearing so that losses on investment properties couldn’t be used as deductions against other income. But he also thinks abolishing it is preferable.

Prime Minister Tony Abbott has ruled out any changes to negative gearing, arguing to do so would be akin to increasing taxes.

Adopting global measures to prevent tax avoidance by multinationals

When Australia hosted the G20 leaders summit in November last year, it agreed to a number of actions to ensure fairness in the international tax system. The OECD is leading global reforms, arguing unilateral action could harm the global agreement that is required to stop multinationals shifting profits to reduce their tax burden.

Since then, Treasurer Joe Hockey has announced new measures specifically designed to target multinationals using complex schemes to escape paying tax. Experts say the measures lack teeth since they only apply to foreign and not Australian multinationals.

The next set of OECD-led measures to address global tax avoidance are due to be released at this year’s G20 summit in Turkey. The OECD recommendations will be finalised by December.

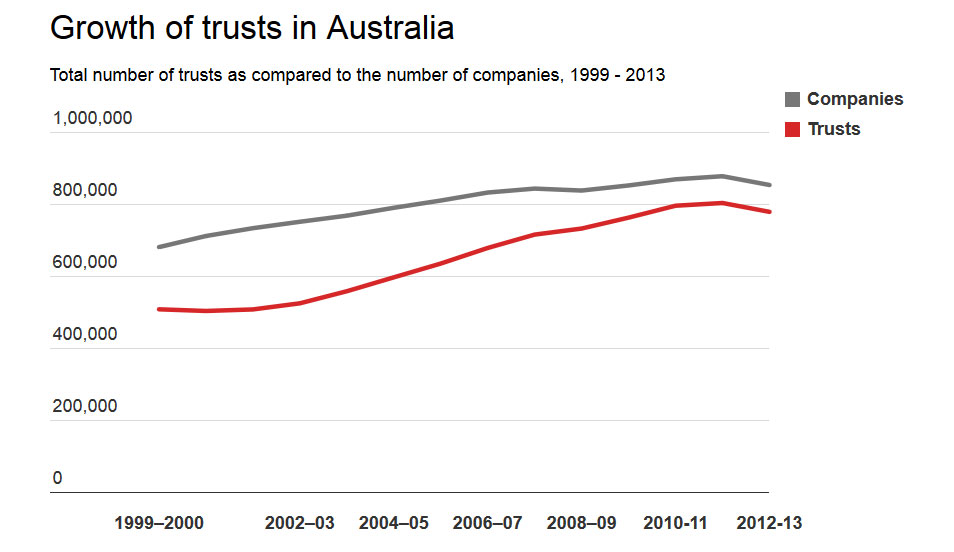

Taxing trusts as if they were companies

In 1999 the Ralph Review of Business Taxation recommended that trusts be taxed as companies, a move that originally got the support of Treasurer Peter Costello. Political pressure soon saw the government back away from this plan, and despite Joe Hockey showing support for the idea back in 2011, it is not one that has the support of the government.

Dale Boccabella says the taxing of trusts is another anomaly in Australia’s tax system that is unfair. Trusts are commonly used by families with a high income to distribute funds to low-earning family members in order to minimise tax.

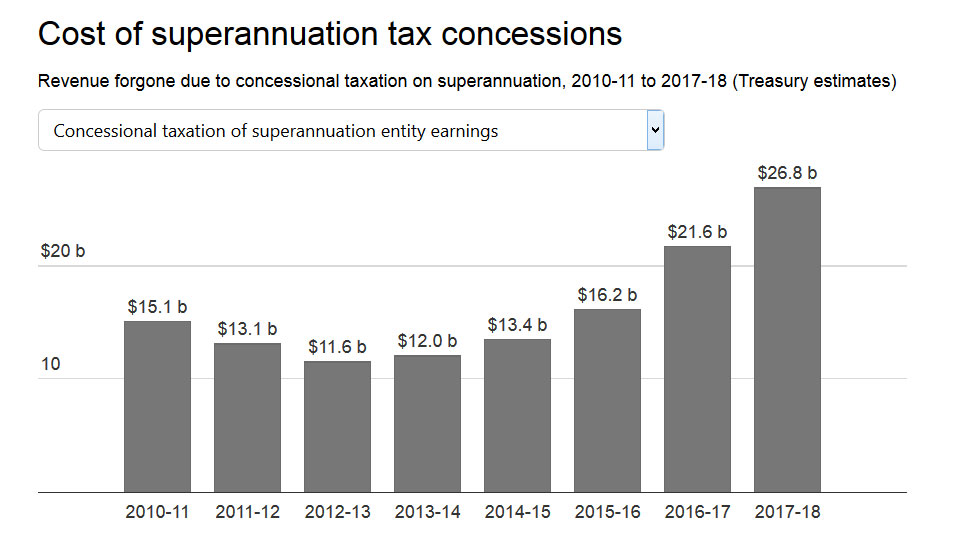

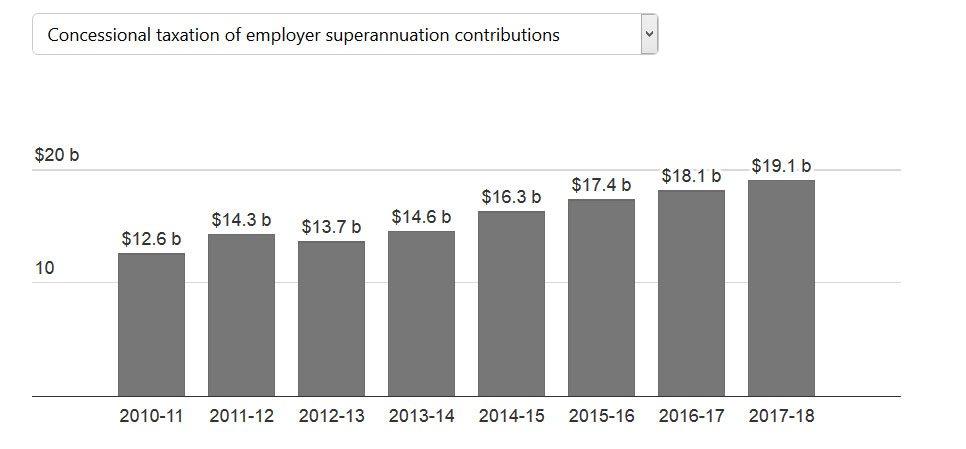

Removing concessions on the taxation of super

Most experts agree superannuation tax concessions are unevenly distributed and are in need of reform.

The Labor Party wants to remove the tax-free concession available to people with annual superannuation incomes from earnings of more than A$75,000, a move it says would raise more than $14 billion over 10 years.

Prime Minister Tony Abbott has ruled out any “adverse changes” to superannuation, including changes to super tax concessions.

Expanding land tax over stamp duty

The Henry tax review argued stamp duties are a highly inefficient tax on land, and that land tax could provide an alternative and more stable source of revenue for the states.

Miranda Stewart says stamp duty is volatile, feeds into house prices (contributing to lack of affordability) and taxes more heavily those people who purchase new housing more often, than those people who don’t.

It wasn’t that long ago that we lived in an entirely analogue world. From telephones to televisions and books to binders, digital technology was largely relegated to the laboratory.

But during the 1960s, computing had started to make its way into the back offices of larger organisations, performing functions like accounting, payroll and stock management. Yet, the vast majority of systems at that time (such as the healthcare system, electricity grids or transport networks) and the technology we interacted with were still analogue.

Roll forward a generation, and today our world is highly digital. Ones and zeroes pervade our lives. Computing has invaded almost every aspect of human endeavour, from health care and manufacturing, to telecommunications, sport, entertainment and the media.

Take smartphones, which have been around for less than a decade, and consider how many separate analogue things they have replaced: a street directory, cassette player, notebook, address book, newspaper, camera, video camera, postcards, compass, diary, dictaphone, pager, phone and even a spirit level!

Underpinning this, of course, has been the explosion of the internet. In addition to the use of the internet by humans, we are seeing an even more pervasive use for connecting all manner of devices, machines and systems together – the so-called Internet of Things (or the “Industrial Internet” or “Internet-of-Everything”).

Complex systems

We now live in an era where most systems have been instrumented and produce very large volumes of digital data. The analysis of this data can provide insights into these systems in ways that were never possible in an analogue world.

Data science is bringing together fields such as statistics, machine learning, analytics and visualisation to provide a rigorous foundation for this field. And it is doing this in the same way that computer science emerged in the 1950s to underpin computing.

In the past, we have successfully developed complex mathematical models to explain and predict physical phenomena. For example, we can accurately predict the strength of a bridge, or the interaction of chemical molecules.

Then there’s the weather, which is notoriously difficult to forecast. Yet, based on numerical weather prediction models and large volumes of observational data along with powerful computers, we have improved forecast accuracy to the point where a five-day forecast today is as reliable as a two-day forecast was 20 years ago.

But there are many problems where the underlying models are not easy to define. There isn’t a set of mathematical equations that characterise the health care system or patterns of cybercrime.

What we do have, though, is increasing volumes of data collected from myriad sources. The challenge is that this data is often in many forms, from many sources, at different scales and contains errors and uncertainty.

So rather than trying to develop deterministic models, as we did for bridges or chemical interactions, we can develop data-driven models. These models integrate data from all the various sources and can take into account the errors and uncertainty in the data. We can test these models against specific hypothesis and refine them.

It is also critical that we look at these models and the data that underpins them.

360 degree data

At my university, we have built a Data Arena to enable the exploration and visualisation of data. The facility leverages open-source software, high-performance computing and techniques from movie visual effects to map streams of data into a fully immersive 3D stereo video system that projects 24 million pixels onto a four metre high and ten metre diameter cylindrical screen.

Inside the Data Arena.

Standing in the middle of this facility and interacting with data in real-time is a powerful experience. Already we have built pipelines to ingest data from high-resolution optical microscopes and helped our researchers gain insight into how bacteria travel across surfaces.

We read 22 million points of data collected by a CSIRO Zebedee which had scanned the Wombeyan Caves, and ten minutes later we were flying though the cave in 3D and exploring underground.

No matter what sort of data we have been exploring, we have inevitably discovered something interesting.

In a couple of cases, it has been immediately obvious we have errors in the data. In an astronomical dataset, we discovered we had a massive number of duplicate data points. In other situations, we have observed patterns that hadn’t been evident to domain experts who had been analysing the data.

This phenomenon is the classic “unknown unknown” (made famous in 2002 by US Secretary of Defence Donald Rumsfeld) and highlights the power of the human visual system to spot patterns or anomalies.

Today’s world is drenched in data. It is opening up new possibilities and new avenues of research and understanding. But we need tools that can manage such staggering volumes of data if we’re to put it all to good use. Our eyes are one such tool, but even they need help from spaces such as that provided by Data Arena.

Author: Glenn Wightwick,DVC Research at University of Technology, Sydney

In 2013 alone, more than 500 houses were demolished in Nashville, Tennessee, a sharp increase from previous years. And hundreds of additional teardowns are expected in a city that’s projected to add a million residents over the next two decades.

Nashville is hardly the only North American city to experience a recent wave of teardowns. In Vancouver, a housing and real estate expert reports that the city issued more than 1,000 demolition permits in 2013. She points out that most of the demolitions are of single-family homes, and each sends “more than 50 tonnes of waste to landfills.”

While preservationists have long decried the loss of historic fabric and cultural capital through teardowns, the environmental costs of demolition are increasingly coming to the fore.

A waste of energy and a waste of space

The negative environmental consequences of teardowns are manifest. According to the Chicago Metropolitan Agency for Planning (CMAP), demolition and construction now account for 25% of the solid waste that ends up in US landfills each year. Further, when a building comes down and its materials are hauled off to the dump, all the energy embedded in them is also lost. This consists of all that was expended in the original production and transportation of the materials, as well as the manpower used to assemble the building.

As CMAP explains, “examining embodied energy helps to get at the true costs of teardowns and links it to issues of air pollution and climate change (from the transport of materials and labor), natural resource depletion (forests, metals, gravel) and the environmental consequences of extracting materials.”

Often, a more environmentally friendly, quaint home is “replaced by a very expensive, much larger house, which is frequently left vacant.” Meanwhile, in the most desirable cities, in their tony suburbs, and in popular resorts, investors park their assets in “McMansions” that are sporadically occupied.

Additionally, bigger houses necessarily encroach upon open space. Not only does expansion entail the uprooting of mature plantings – which benefit air quality – but it also eliminates trees that can provide shade and minimize energy required to cool buildings in warmer months.

Urban facelifts erase more than crumbling buildings

In city neighborhoods, opponents of demolition will often cite the loss of historic character.

Advocates for development, on the other hand, frequently argue that demolition rids cities of decrepit, obsolete houses, paving the way for multi-unit developments. In this sense, cities can become more efficient with their limited space, avoiding suburban sprawl while alleviating the long, traffic-snarled commutes of those who travel to the city.

In many cities, however, new construction on the sites of torn-down houses is aimed at attracting relatively affluent young or middle-aged professionals – the demographic that appreciates urban amenities like shops, restaurants and museums.

Time was that a “walking world” – that is, an environment in which services and amenities are available within walking distance of one’s home – was possible for all city-dwellers, regardless of class. Today, in many urban areas, housing in the dense central core is the purview of the rich, and the less affluent are pushed to the outskirts.

As a result, formerly diverse neighborhoods become economically monolithic. Longtime residents scatter as home values – and taxes – are driven up by new construction.

Withering cultural capital

Teardowns also have negative cultural implications.

All houses tell a story: they’re evidence of how earlier generations thought about domestic life and designed spaces to reflect their daily needs. When we demolish them, we lose those crucial traces of the past.

Of course, older houses often cannot satisfy contemporary demands for amenities, and were frequently built on a smaller scale. Modestly scaled houses from the 19th and early 20th centuries – which represent a wide range of architectural styles – are sometimes built out or renovated. But often developers and homeowners opt to (as a “For Sale” sign in my neighborhood recently put it) “scrape the lot.”

For whatever reason, high square footage has become a prerequisite for new homes in the United States, where the average size of a house built since 2003 is more than double that in England. The United States Census Bureau reports that between 1973 and 2008 the average square footage of new houses soared from 1,660 to 2,519, only dipping after the Great Recession.

Small houses aren’t alone in falling victim to the wrecking ball. The Los Angeles Times recently reported on the demolition of mansions in desirable LA neighborhoods that had sold for as much as US$35 million.

Actress Jennifer Aniston has taken a stand against her mega mansion-inhabiting peers, arguing that “The very idea that a building of 90,000 square feet can be called a home seems at the least a significant distortion of building code.”

Even in less supercharged real estate markets, large and well-built homes fall victim to rising land prices that make them more valuable as dirt.

One example is Georgia’s Glenridge Hall, an historic Tudor Revival mansion, which The Georgia Trust, a statewide historic preservation organization, designated a “place in peril” earlier this year.

Featured in films and providing some of the setting for the first season of The Vampire Diaries, Glenridge Hall had been preserved, until recently, by descendants of the original owner. But the architecture and planning firm Duany Plater-Zyberk & Company – darlings of the New Urbanism movement, which advocates for the revival of traditional town planning and walkable mixed-use developments – demolished the building to make way for a new mixed residential and commercial “English Village.”

As I pointed out in my recent book, the builders of Tudor mansions like Glenridge Hall in the 1920s and 1930s attached a great deal of significance to the historic feel of their homes: in famous Tudors like the Virginia House and Agecroft Hall, they went so far as to import materials from actual English Tudors.

Unfortunately, for today’s wealthy builders and buyers, the past carries little cachet. For many, older homes are considered an obstacle rather than a badge of distinction. And when these radical presentists are given free rein to tear down the remains of the past, we all lose.

Author: Kevin D Murphy, Andrew W Mellon Chair in the Humanities and Professor and Chair of History of Art at Vanderbilt University

Australian companies will soon be publishing financial results, as well as information about sustainability efforts.

Corporate social responsibility of the big four banks – Australia and New Zealand Banking Group (ANZ), Commonwealth Bank of Australia (CBA), National Australia Bank (NAB) and Westpac is a continuing topic of debate following recent scandals and reports of unsustainable activities.

Yet according to ANZ chairman, David Gonski, Australians ought to “stop bashing the banks” for being large and profitable.

This comment should put civil society on guard.

A recent study by the Centre for Corporate Governance at the University of Technology Sydney, part of the UNEP Inquiry into the Design of a Sustainable Financial System, examined self-regulatory and voluntary sustainability efforts of the world’s largest banks, in partnership with Catalyst Australia which scrutinised the efforts of the big four Australian banks.

Sustainable finance

The “four pillars” of the Australian banking system are a dominant part of the Australian economy: the four banks are featured in the top five of the ASX 200 and hold A$522 billion of Australian household deposits, equal to one-third of Australia’s gross domestic product.

In the words of David Murray, former CBA boss and chair of the Financial System Inquiry: “banks fund most of the assets in the economy – whether it’s businesses, governments themselves, homes or projects, whatever else.”

This market dominance results in great power and great responsibility. As banks provide the majority of external finance to companies and governments, they can influence practices: bank lending potentially has more impact on sustainable enterprise than investment and divestment on the stock market.

Banks can thus wield their enormous market power to support sustainable activities, while their actions can likewise contribute to detrimental behaviour.

Conflicting images

The examination of the sustainability efforts of Australian and international banks reveals a schism between symbolic and substantive sustainability efforts.

At the 2014 World Economic Forum, Westpac was named the most sustainable company in the world. ANZ has been named as a leader in the global banking sector by the Dow Jones Sustainability Index, a major reference point for sustainable investors, six times in the last seven years, while NAB and the CBA have likewise been recognised for their sustainability performance.

As a result, public confidence in banks is low: according to a national survey, part of the research by Catalyst Australia, 76% of respondents believe that banks put profits before their social and environmental responsibilities.

Regulation and Supervision

In 2005, the Government launched an Inquiry into Corporate Responsibility and Triple Bottom Line reporting. It examined the extent to which the Australian legal framework encourages or discourages company directors from considering interests of stakeholders other than shareholders, the suitability of voluntary sustainability measures, and the appropriateness of reporting requirements.

Furthermore, the Committee recommended that sustainability reporting should remain voluntary, fearing that “mandatory reporting would lead to a ‘tick-the-box’ culture of compliance”.

In the aftermath of the global financial crisis, financial sector regulators were pushed to exercise more supervision and be less trusting of self-regulatory efforts. Consequently, in 2013 the Government launched the Financial System Inquiry. Regrettably, the terms of reference did not address social and environmental sustainability and risks in the financial sector.

The readiness to increase supervision to avoid financial risks is not matched by a similar willingness to supervise and regulate the social and environmental risks caused by the financial sector. This emphasis on voluntary efforts is problematic, as the study by Catalyst Australia shows that only 26% of the Australian public believe banks will behave ethically and responsibly if they self-regulate.

Bridging the governance gap

While many Australian and overseas banks have successfully shaped sustainable corporate imagery, the research by the Centre for Corporate Governance and Catalyst Australia finds that self-regulation permits facts to be obscured and leaves social and environmental matters peripheral to business strategies.

The assurance that banking activities are based on sustainable principles requires public monitoring of compliance and performance – as US litigater Louis D. Brandeis famously said:

“Publicity is justly commended as a remedy for social and industrial diseases. Sunlight is said to be the best of disinfectants; electric light the most efficient policeman.”

In order to accomplish this, directors’ duties ought to be reformulated to include social and environmental responsibilities, sustainability reporting requirements should be redefined and further embedded in corporate governance systems, and social and environmental risk assessments should apply the precautionary principle, shifting the burden of proof to actors that potentially cause harm.

Robust governance, regulation and supervision should not be seen as measures that restrain innovation or entrepreneurship, but rather as instruments that can help to restore trust, and ensure that banking activities are conducted openly, fairly and sustainably.

Author: Martijn Boersma, Researcher in Corporate Governance at University of Technology, Sydney

Greece has just experienced a nasty reality check. For Europe, the reckoning might simply lie a little further down the road. The Syriza party and prime minister Alexis Tsipras secured a triumph in the elections of January 2015 based on promises to “tear up” the bailout agreements and put an end to austerity. Until a week ago, when the notorious referendum took place, the party and its leader seemed to stick by their conviction that an aggressive stance towards EU partners should and could broker a better deal for Greece, away from half-hearted compromises. This morning it became obvious that this was not possible.

The Greek government had to sign an agreement not too different from those to which previous governments agreed and which were opposed by Syriza – in fact, some of the measures the Greek parliament is being asked to pass were part of previous agreements but were never implemented. Was Syriza naïve? Were they populists? Probably a combination of the two.

Grexit not dead yet

At least for now, Tsipras seems like a leader who found the courage to assume responsibility and came to realise – the hard way – that the EU is all about compromise. Tsipras has now two choices: either follow the steps of previous Greek governments, equivocate and eventually fail taking the country with him or truly support the plan and try making a positive change out of a very difficult deal. Despite the deal, a Greek exit from the euro is closer than ever, particularly if he chooses the former.

Something that could help Tsipras choose the latter is that his government is the first to enjoy very wide political support, at least for the moment. Because of the high stakes and high tension of the last few weeks, all political parties with a clear European orientation have backed Tsipras in the negotiations and seem to support the agreement. This is a weapon that no other government had before in promoting reforms. A Syriza-led government is also the best option for stability in Greece, given the popularity that Syriza and Tsipras enjoy and which should be respected.

But this does not mean that Tsipras would not face opposition or that anti-austerity or populism in Greece has ended. In fact, it is quite the opposite.

Eurosceptics

A sizeable proportion of Syriza MPs, including some of the party’s ministers, have made clear they do not support the agreement. The next few days will show whether this group will take control over the anti-austerity camp. At the same time, others, like members of the government coalition partner Independent Greeks or even far-right party Golden Dawn, remain opposed to the agreement. What happened this weekend would probably only fuel their euroscepticism.

But the way this deal was struck could have implications far beyond Greece. The nature of discussions between eurozone elites uncovered once more the huge distance between what goes on in Brussels and the European citizens. While discussions among the finance ministers of the eurogroup and at the Eurosummit were taking place, social media was filled with frustration over the apparently rather aggressive form of negotiations. International media, meanwhile, were keen to underline the lack of solidarity shown by eurozone countries, especially Germany.

European leaders seem oblivious to that and the impact that this whole process could have had on euroscepticism across Europe. The leader of Britain’s anti-EU UK Independence Party, Nigel Farage, was quick to comment that if he was a Greek politician he would vote against this deal, and if he was a Greek who voted No in the referendum he would be protesting in the streets. Just a year after the European elections in 2014, there is a risk of a new wave of euroscepticism which the EU will have to address in the long term.

Crisis management

Jean Monnet, the French political economist, said in 1976:

Europe will be forged in crises, and will be the sum of the solutions adopted for those crises.

Indeed, the EU is the child of World War II and, after that, has evolved through many other crises. One could imagine a similar social media frenzy had the means existed during the failed European constitution of 2005 or even the so-called “empty chair” crisis of the mid-1960s when France withdrew its representatives from the European Commission.

Let’s hope this crisis improves the EU and allows it to progress; however much this latest crisis has been an important one for the public debate, it is by no means the first – and it probably contains the seeds of the next.

Author: George Kyris, Lecturer in International and European Politics at University of Birmingham

The Chinese stock markets have experienced significant turmoil in recent weeks, with the Shanghai Composite Index – the country’s major reference – falling by 32% since June 12. But this fall was preceded by an equally sharp rise of 150% over the previous nine months. In the 20 years since I have been working in finance, I’ve never seen anything like this. So what is going on with the Chinese stock market?

There are several reasons for this unusual behaviour: firstly, when I teach stock market investment to my Chinese students, I always remind them that the Shanghai stock exchange should be thought of more as a casino, rather than as a proper stock market. In normal stock markets, share prices are – or, at least, should be – linked to the economic performance of the underlying companies. Not so in China, where the popularity of the stock market directly correlated with the fall in casino popularity.

Stocks and casinos

In China, given the low credibility of the financial statements published by listed companies, investors need to rely on other tools to predict share price performance. These tools include a heavy reliance on technical analysis and charts – a method that tends to predict future share price based purely on the company’s past performance, with no regards to its fundamentals. Even the name of the company is often neglected; all that matters is the historic price performance.

While this technique is also used in Western markets, my experience in China is that it is the predominant method for investment. Hence the disconnect between a share’s price movements and economic fundamentals.

There has been, however, a strong correlation between the stock market’s performance and the revenues of the casinos in Macau. While gambling revenues were growing at a fast pace in Macau, people largely ignored the stock market – whose performance was, largely, uninteresting for a number of years. But since China’s president, Xi Jinping, launched a campaign against corruption, gambling activity has started to decline. This was when the stock market started to move up. Coincidence?

Real estate

The other reason why the stock market experienced a sharp increase between September 2014 and June 2015 relates to the Chinese real estate market. In recent years, investment in real estate has been the only way for ordinary citizens to get returns higher than the paltry 3% offered by bank deposits (yes, 3% is paltry in an economy that grows at more than 10% a year in nominal terms). But high capital requirements and growing regulations on the purchase of real estate has meant that benefiting from this growing market has been increasingly difficult for ordinary citizens.

Macau: the traditional home of Chinese gambling.Shutterstock

Commercial banks therefore – in an effort to mimic real-estate returns – started to offer so-called “wealth management products”, which are basically funds that invest in the real estate market. These funds were then repackaged and resold in the retail market. Chinese individuals would take their savings out of current accounts and placed them into these wealth management products and achieve returns similar to those available to buyers of real estate.

This was the modus operandi until the beginning of 2014, at which point the economy and the real estate markets started to show signs of weakness. The once-easy money coming from the property market started to disappear and people with wealth management products started to get into financial trouble and some of them even defaulted on their payments (the government bailed them out, so no individual was at a loss).

Monetary policy

From November 2014 the Chinese central bank, worried about the slowing economy, decided to institute an aggressive monetary policy to rapidly lower interest rates with the aim of stimulating the economy, which also caused current account rates to decline. This created a perverse scenario where individuals who were already seeking returns higher than those offered by current accounts were then denied the opportunity to get them through real estate because of the falling market. As a result, deposit rates were cut further and the return on current accounts became even more dissatisfying. Commercial banks found themselves in a quandary.

The Shanghai Composite Index’s growth and decline in recent months.Yahoo finance

With the casino route closed and real estate off the table, what was left? The Shanghai and Shenzhen stock markets: the two main stock markets that had remained dormant for years.

Banks then turned the old real estate wealth management products into investment vehicles to purchase shares directly on the stock markets. A large portion of customer deposits were then directly invested in the stock market, which then surged on the back of that demand.

An empty bubble?

Meanwhile, however, nothing happened to the earnings forecasts of the underlying companies. In fact, if anything, they should have been revised down because of the deteriorating macroeconomic condition of the Chinese domestic economy. But of course, as we said before, no one really looks at earnings and price ratios.

Due to the desire to maximise returns, many individuals then used leverage so that the inflow of money in the stock market was even higher. For example, if someone wishes to purchase shares for a total value of 100RMB, but only has available cash in his deposit account of, say, 60RMB, he could borrow the remaining 40RMB from the brokerage house. By doing this, the original source of 60RMB was turned into an upward push of the stock price equivalent to the full 100RMB. This drove strong share price growth between September 2014 and June 12 2015.

What happened on June 12 2015? Nothing. Just some smarter investors (generally large institutional investors, which represent 20% of all market volumes) started to sell and the rest of the market followed suit. Fear got hold of small investors (who represent 80% of the market) and selling accelerated, with margin calls making those selling do so even faster, and here we are today – a 32% drop and counting since the peak of mid-June.

In the past few days, the Chinese government has adopted a number of measures to try to mitigate this crash. The market finally reacted positively to a relaxation of restrictions on margin requirements. But this measure simply transfers the risks from investors to brokerage houses – it does not change the fact that the market has increased by 70% over the last year. The bubble, if it is a bubble, still has a long way to go.

Author: Michele Geraci, Head of China Economic Policy Programme, Assistant Professor in Finance at University of Nottingham