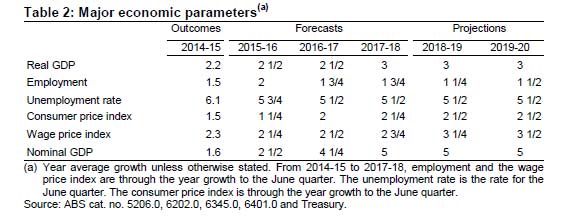

In essence, the Budget forecasts indicate that the Australian economy continues to transition from mining investment-led growth to broader-based growth. But real GDP growth is forecast to be below potential over the next two years at 2½ per cent in 2015-16 and 2016-17 and then strengthen to 3 per cent in 2017-18 as the detraction from falling mining investment eases. Over the following two years, real GDP is projected (not forecast) to increase by 3 per cent per annum.

The economy is already benefiting from rapidly rising mining export volumes and this is set to continue as more LNG export capacity comes on line. Mining export volumes are expected to increase by more than 20 per cent over the forecast period.

In the midst of this transition and as noted at our most recent Hearing, the labour market has been remarkably resilient. The labour market has performed better than expected at 2015‑16 MYEFO. Employment growth has been supported by moderate wage growth and the transition to more labour-intensive sectors of the economy.

Inflation outcomes so far appear to have been weaker than forecast in the 2015‑16 MYEFO. Consumer price inflation in the March 2016 quarter showed broad‑based weakness that was reflected in the very weak underlying inflation outcome. In that context, the Reserve Bank Board decided to reduce the cash rate by 25 basis points to 1.75 per cent, the lowest setting on record.

Reports from across Australia indicate that activity in New South Wales and Victoria remain strongest, while activity in Tasmania has also picked up. The Northern Territory and the Australian Capital Territory are performing reasonably well and Queensland is performing better than expected a year ago supported by a pick-up in construction activity around Brisbane. South Australia continues to remain soft, and there are clear signs that activity in Western Australia is weaker than expected.

Globally, growth is forecast to be weaker than 2015-16 MYEFO. The United States has had a slow start to the year but there are tentative signs of a pick-up in Europe. China’s growth continues to moderate, but remains relatively strong compared with most other major economies.

I want to focus my comments today on the risks to the global outlook.

Risks to the global growth outlook are present in both advanced and emerging market economies as global uncertainties increase. This message was made clear at the latest meeting of the G20 Finance Ministers and Central Bank Governors in April where the outlook for growth was assessed to remain modest and uneven.

As also noted previously, significantly for Australia are the uncertainties around the implications of the transition in the Chinese economy from investment-led to consumption and services-led growth given the exposure of Australia and its major trading partners to China. And while China’s economic transition is expected to contribute to more sustainable growth over the longer term, Chinese domestic consumption and a growing service sector is unlikely to fully offset the decline in investment and a slowing industrial sector in the near and medium term.

There will be opportunities for Australia in this transition. Our past trade has predominantly been focused on demand for our commodities. Trade with China as it transitions to a consumer-led economy will be more focused on demand for our services. We also expect a growing investment relationship with China, building off a strong base and further boosted by the China-Australia Free Trade Agreement.

A sharper than expected slowdown in Chinese growth, however, would have significant implications for our economy and the region. This is because China is Australia’s number one export market and import supplier. Globally, China is one of the main trading partners for more than 100 economies which account for about 80 per cent of world GDP; so a slowing China will have far reaching effects around the world.

There are risks of renewed volatility in financial markets, which we saw earlier this year. That volatility can reflect concerns in equity and credit markets as to whether the outlook for current global growth will be strong enough to drive corporate earnings and maintain low default rates in order to sustain current valuations. Such bouts of volatility have adversely impacted the financial conditions faced by businesses and households in key global economies.

Banks globally also continue to hold more capital than they did prior to the global financial crisis. However, a number of major economies continue to face financial challenges, particularly the euro area, Japan and a range of emerging market economies. Significant debt has been raised in recent years, particularly in emerging markets, which could also create challenges for both borrowers and lenders in a continued low global growth environment.

Inflation remains low globally reflecting, in part, the impact of low energy costs. I expect inflation in major advanced economies to remain below policy targets for at least in the near term and monetary policy in major advanced economies to remain accommodative for some time yet. Significantly, expectations for further US Federal Reserve rate rises have been pushed out a little.

There is also the risk that low inflation, coupled with low wages growth and low productivity growth experienced in many advanced economies, could become embedded in lower potential growth over time.

Estimates for long-run potential global growth are also being reconsidered by official forecasters. This partly reflects the ongoing legacy of the global financial crisis which has had long lived effects on investment in productive capital and on labour markets. In advanced economies, potential growth was slowing even before the global financial crisis.

Contributing to low productivity growth and declining potential growth is the significant transition underway in global demographic conditions. The global population is growing more slowly, and as fertility rates fall and people live for longer, populations are growing older. A number of countries — including Japan, China and Germany — are confronting declining working age populations.

There is also uncertainty about the effect of oil prices on global growth. This is because the response to lower oil and energy prices in 2015 has not been as strong as might be expected based on historical experience. Factors likely to have muted the positive net impact of lower oil prices on global growth include lower global energy investment and a smaller than expected increase in global private consumption, perhaps as consumers save part of the windfall from lower oil prices.

In summary, it is all uncertain. The Budget shows that the Australian economy continues to transition from mining investment-led growth to broader-based growth. As a still relatively small, open economy, global economic conditions are very important to Australia’s economic outlook. The fact is that global economic conditions continue to be challenging.

On another matter, Treasury standard practice is not to release costings beyond the forward estimates or for the medium term. On this occasion, the Treasurer has authorised me to provide to the Committee the medium-term estimate of the cost to the budget of lifting the small business entity threshold and reducing the company tax rate to 25 per cent by 2026-27. The cost of these measures to 2026-27 is $48.2 billion in cash terms. These estimates have been incorporated into the budget’s medium-term projections for tax receipts. I note that, as with all tax projections over 10 years, these costings have considerable uncertainty. I also note that the medium term economic projections in the Budget assume significant ongoing economic reforms. Finally, I note that Treasury has estimated that the Government’s tax package is estimated to increase the level of GDP by a little over 1 per cent in the long term.

The 2016 PEFO uses the same projection methodology that has been used in budgets and budget updates since the 2014-15 Budget.

The 2016 PEFO uses the same projection methodology that has been used in budgets and budget updates since the 2014-15 Budget.