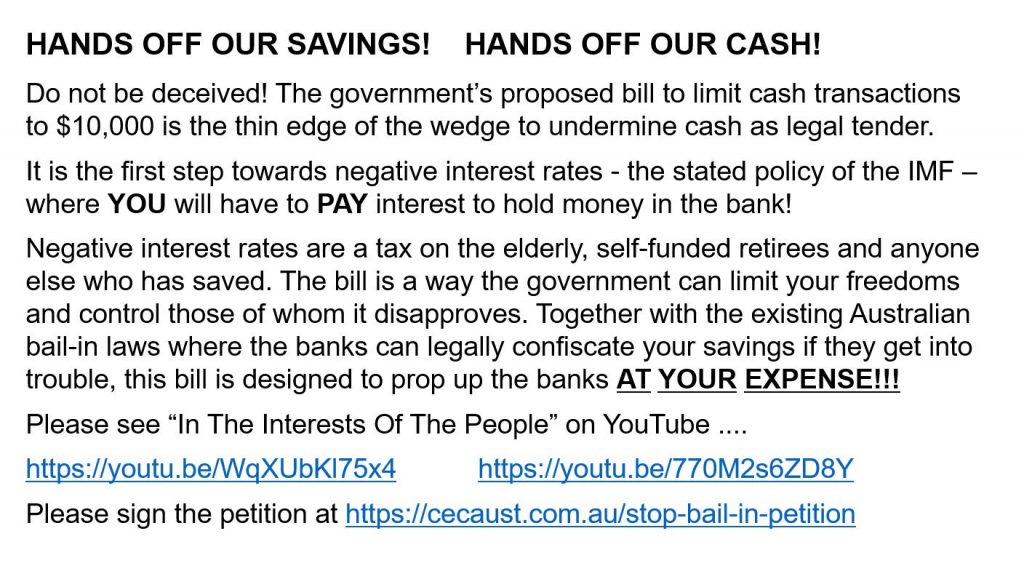

A quick reminder that the draft legislation relating to the restrictions on cash transactions which the Treasury released for comment recently, and was the subject of our recent shows, has a deadline of Monday 12th August.

Email: blackeconomy@treasury.gov.au with the subject line:

Submission: Exposure Draft—Currency (Restrictions on the Use of Cash) Bill 2019

This bill proves the necessary preparations for negative interest rates in Australia, meaning money in the bank could cost savers!

There is a clear link between the restrictions on cash holding and cash transactions and negative interest rates. Indeed, the IMF, and other organizations admit that without such cash restrictions, negative interest rates, (perhaps as low as 4%!) will not be effective.

One of our viewers prepared a brief flier which he hopes may be useful to help raise awareness of this critical issue. Its available here. Share as widely as you can. Remember the deadline is 12th August!

Screen shot of flier – note click on image to access live linked document which you can view or download

Last Friday the Treasury released a draft bill which would ban cash transactions above $10,000. But I discuss the real story, with the CEC‘s Robbie Barwick. It has more to do with negative interest rates than may first appear.

Deposit Bail-In is something which we have been discussing in recent times, not least because of the overt example now active in New Zealand under the Open Banking Resolution, the mandate from the G20 and the Financial Stability board and the implementation in several other countries in response to this.

In Australia, the situation has been unclear, since the 2018 bill was passed on the voice.

Treasury and politicians keep denying there is any intent to bail-in deposits to rescue a failing bank, but then divert to a discussion of the $250k deposit insurance scheme which first would need to be activated by the Government, and second only once a bank has failed. It is irrelevant to bail-in.

Bail-in is where certain instruments could be converted to shares in a bank to buttress its capital in times of pressure to attempt to stop a bank failing, and so would reduce the risk of a Government bail-out using tax payer funds. They will use private funds (potentially including deposits, which are unsecured loans to a bank), instead.

So, today we release an opinion from Robert H. Butler, Solicitor. This was addressed to the Citizens Electoral Council of Australia, and is published with their permission. The key finding is simply that:

Whilst not beyond doubt, it is my opinion that the provisions of the Act do provide for a power of bail-in of bank deposits which did not exist prior to the passing of the Act.

This means that unless the law is changed to specifically exclude deposits (any side of politics going to volunteer to drive this?), bank deposits are not unquestionably free from the risk of bail-in. And we have the view that the vagueness is quite deliberate, and shameful.

Time to pressure our members of Parliament, and raise this issue during the expected election ahead.

Here is the full opinion:

I have been asked to provide an opinion as to whether the Financial

Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Act

2018 (“the Act”) creates a power of bail-in by Australia’s banks of

customers’ deposits.

At a minimum, the Act empowers APRA to bail in so-called

Hybrid Securities – special high-interest bonds evidenced by instruments which

by their terms can be written off or converted into potentially worthless

shares in a crisis.

However, the Act also includes write-off and conversion

powers in respect of “any other

instrument”. The Government has contended that these words do not extend to

deposits, on the basis that the power only applies to instruments that have

conversion or write-off provisions in their terms, which deposit accounts do

not. However, the reference to “any other

instrument” would be unnecessary if the power only applied to instruments

with conversion or write-off provisions; moreover, banks are able to change the

terms and conditions of deposit accounts at any time and for any reason,

including on directions from APRA to insert conversion or write-off provisions,

which would thereby bring them within the specific terms of the write-off or

conversion provisions of the Act.

The issue could now be simply resolved by Government

passing a simple amendment to the Act to explicitly exclude deposits from being

bailed in.

Bail-in is one of the 3 alternative actions which can be

taken in respect of a distressed bank.

The alternatives are:-

Bankruptcy and liquidation of the bank;

Bail-out, which is the injection into the bank

of the necessary capital to meet the bank’s liabilities. This is the action

which was undertaken after the 2008 GFC by governments through their Treasuries

and Central Banks bailing out the banks with taxpayers’ funds;

Bail-in, which is the injection into the bank of

the necessary capital to meet the bank’s liabilities either by the bank writing

off its liabilities to creditors or depositors or converting creditors’ loans

or deposits into shares whereby creditors and depositors take a loss on their

holdings. A bail-in is the opposite of a bail-out which involves the rescue of

a financial institution by external parties, typically governments that use

taxpayers’ money.

Liability

limited by a scheme, approved under Professional Standards Legislation

The provisions of the Act as they affect bail-in require a consideration

of the issue in 3 different sets of circumstances, and the provisions of the

Act need to be considered separately in relation to each such set of

circumstances.

Those 3 sets of circumstances are:-

Hybrid Securities issued by banks;

Customer deposit accounts with banks;

Bank documentation implementing deposit

accounts.

(i) Hybrid securities

The ASX describes Hybrid Securities as “a generic term used to describe a security

that combines elements of debt securities and equity securities.” Whilst there

are a variety of such securities, in short they are securities issued by banks

which permit the amounts secured by the security to be converted into shares or

written off at the option of the bank in certain circumstances.

The Act provides specifically for Hybrid Securities.

Section 31 adds “Subdivision

B-Conversion and write off provisions” to the Banking Act 1959 and inserts

a definition Section 11CAA which provides that “conversion and write off

provisions means the provisions

of the prudential standards that relate to the conversion or writing off of:

Additional

Tier 1 and Tier 2 capital; or

any

other instrument.”

The Act also inserts Section 11CAB which provides:

“(1)

This section applies in relation to an instrument that contains terms that are

for the purposes of the conversion and write off provisions and that is issued

by, or to which any of the following is a party:

(a) an ADI;

……

The

instrument may be converted in accordance with the terms of the instrument despite:

any

Australian law or any law of a foreign country or a part of a foreign country,

other than a specified law; and

…..

The

instrument may be written off in accordance with the terms of the instrument

despite:

any

Australian law or any law of a foreign country or a part of a foreign country;

…..

Under the Basel Accord, a bank’s capital consists of Tier 1

capital and Tier 2 capital which includes Hybrid Securities.

The Section 11CAB provisions mean that any law which would

otherwise prevent the conversion or write-off of Hybrid Securities does not apply

unless a particular legislative provision specifically provides that it does

apply. One of the principle types of legislation that this provision would be

directed towards is consumer legislation, particularly those provisions which

allow a Court to set aside or vary agreements if a party has been guilty of

false or misleading conduct – this is precisely the sort of argument which

could be raised in the circumstances referred to by outgoing Australian

Securities and Investments Commission (ASIC) Chairman Greg Medcraft in an

exchange with Senator Peter Whish-Wilson in the hearings of the Senate

Economics Legislation Committee on 26 October 2017: Mr Medcraft said: “There are two reasons we believe a lot of

the retail investors buy these securities. One is they don’t understand the

risks that are in over 100-page prospectuses and, secondly – and this is

probably for a lot of investors – they do not believe that the government would

allow APRA to exercise the option to wipe them out in the event that APRA did

choose to wipe them out.“

When Senator Whish-Wilson raised the spectre of

“bail-in”, Mr Medcraft confirmed: “Yes, they’ll be bailed in. The big issue with these securities is the

idiosyncratic risk. Basically, they can be wiped out – there’s no default; just

through the stroke of a pen they can be written off. For retail investors in

the tier 1 securities – they’re principally retail investors, some investing as

little as $50,000 – these are very worrying. They are banned in the United

Kingdom for sale to retail. I am very concerned that people don’t understand,

when you get paid 400 basis points over the benchmark [4 per cent more than

normal rates], that is extremely high

risk. And I think that, because they are issued by banks, people feel that they

are as safe as banks. Well, you are not paid 400 basis points for not taking

risks…” He emphasised: “I

do think this is, frankly, a ticking time bomb.“

The over-riding intention behind Sections 11CAB(2) and

11CAB(3) is to deal with issues arising from the examples in the comments of

Graeme Thompson of APRA in an address on 10 May 1999 when he said: “… APRA will have powers under proposed

Commonwealth legislation to mandate a transfer of assets and liabilities from a

weak institution to a healthier one. This is a prudential supervision tool that

the State supervisory authorities have had in the past, and it has proved very

useful for resolving difficult situations quickly. We expect the law will

require APRA to take into account relevant provisions of the Trade Practices

Act before exercising this power, and to consult with the ACCC whenever it

might have an interest in the implications of a transfer of business.”

The new Sections 11CAB(2) & (3) mean that APRA does not need to consider

those issues (or any other) in relation to conversion and write-off of Hybrid

Securities.

(ii) Deposits

Whether or not bail-in of other than Hybrid Securities is

implemented by the Act has been the subject of debate and concern since the

Bill which led to the Act became public. The principal area of concern is

whether or not the bail-in regime was extended by the Act to deposits made by

customers with banks.

The central issue is the wording of the definition in

Section 11CAA quoted above and what “any

other instrument” means. “Instrument”

is not defined in the Act but a “financial

instrument” is defined by Australian Accounting Standard AASB132 as “any contract that gives rise to a

financial asset of one entity and a financial liability or equity instrument of

another entity.” As confirmed by the Reserve Bank, a deposit with an

ADI bank comes under such a definition – it is a contract with terms and

conditions as to the deposit being set by a bank, accepted by a depositor on

making a deposit and creating a financial asset (a right of repayment) and a

financial liability in the bank (the obligation to repay).

Deposits are created by “instruments” and are governed by the terms and conditions of

those instruments.

The intent of the reference to “any other instrument” in Section 11CAAAA is assisted by the

Explanatory memorandum which accompanied the Exposure Draft and which states:

“5.14

Presently, the provisions in the prudential standards that set these

requirements are referred to as the ‘loss absorption requirements’ and

requirements for ‘loss absorption at the point of non-viability’. The concept

of ‘conversion and write-off provisions’ is intended to refer to these, while

also leaving room for future changes to APRA’s prudential standards, including

changes that might refer to instruments that are not currently considered

capital under the prudential standards.”

Section 11AF of the Banking Act provides that APRA can

determine Prudential Standards which are binding on all ADIs. These standards

are in effect regulations which have the force of legislation by virtue of the

authorisation in the Banking Act. That Section provides, inter alia:

“(1)

APRA may, in writing, determine standards in relation to prudential matters to

be complied with by: (a) all ADIs; …..”

Banks are ADIs.

The various Prudential Standards issued by APRA are

accordingly headed with the phrase: “This

Prudential Standard is made under section 11AF of the Banking Act 1959 (the

Banking Act).”

That power then leads into the issue of APRA using this

authority to expand the meaning of “capital”

the subject of conversion or write-off, to encompass deposits if deposits are

not already covered by the reference to “any

other instrument”.

That these provisions as to conversion and write-off are

not limited to Hybrid Securities is confirmed in Section 11CAA itself as quoted

above. The provisions extend to “any

other instrument” by sub-section (b) of that Section and must relate

to instruments other than those referred to in sub-section (a), i.e. other than

“Additional Tier 1 and Tier 2 capital”

(being instruments which themselves contain an explicit provision for

conversion or write-off). All instruments that the Act refers to as to being

able to be converted or written off “in

accordance with the terms of the instruments” come under the

definition of “Additional Tier 1 and Tier

2 capital” – “any other

instruments” is not only an entirely unnecessary addition if the Act

is intended to apply only to instruments with conversion or write-off terms,

its very broad language must be intended to encompass some other instruments (“which are not currently considered capital”

as stated in the Explanatory memorandum) and that could extend to instruments

relating to deposits.

If Section 11CAA thus extends to instruments relating to deposits then APRA

can as the Prudential Regulator issue a Prudential Requirement Regulation or a

Prudential Standard for the writing-off

or conversion of deposits.

APRA already has a power to prohibit the repayment of

deposits by ADIs, a power which already verges on the writing off of those

deposits. The Banking Act Section 11CA provides:

“(1)

… APRA may give a body corporate that is an ADI … a direction of a kind

specified in subsection (2) if APRA has reason to believe that:

…..

the body

corporate has contravened a prudential requirement regulation or a prudential

standard; or

the

body corporate is likely to contravene this Act, a prudential requirement

regulation, a prudential standard or the Financial Sector (Collection of Data)

Act 2001, and such a contravention is likely to give rise to a prudential risk;

or

the

body corporate has contravened a condition or direction under this Act or the

Financial Sector (Collection of Data) Act 2001 ; or

….

(h)

there has been, or there might be, a material deterioration in the body

corporate’s financial condition; or

….

(k)

the body corporate is conducting its affairs in a way that may cause or promote

instability in the Australian financial system.

…..

(2)

The kinds of direction that the body corporate may be given are directions to

do, or to cause a body corporate that is its subsidiary to do, any one or more

of the following:

….

not to repay any money on deposit or

advance;

not to

pay or transfer any amount or asset to any person, or create an obligation

(contingent or otherwise) to do so;

…..”

This provision was inserted into the Banking Act in 2003 by

the Financial Sector Legislation Amendment Act (No 1).

It is not known whether this power has been exercised by

APRA. Relevantly Graeme Thompson in the address referred to above said: ”

… Particularly in the case of banks and

other deposit-takers that are vulnerable to a loss of public confidence, APRA

may prefer to work behind the scenes with the institution to resolve its

difficulties. (Such action can include arranging a merger with a stronger

party, otherwise securing an injection of capital or limiting its activities

for a time.)“

It is a relatively small step to then convert or write-off

what the ADI has been prohibited from repaying or paying out.

It might be argued that APRA’s powers in existing Sections

of the Act are not absolute and are subject to various qualifications and

limitations arising out of their context within the Act or the balance of the

Section or Sections of the Act in which they appear. To avoid such an

interpretation, Section 38 of the Act inserts 2 new sub-sections to Section

11CA in the Banking Act:

“(2AAA)

The kinds of direction that may be given as mentioned in subsection (2) are not

limited by any other provision in this Part (apart from subsection (2AA)).

(2AAB)

The kinds of direction that may be given as mentioned in a particular paragraph

of subsection (2) are not limited by any other paragraph of that subsection.”

APRA has already adopted the need for certain capital to be

capable of conversion or write-off, regardless of laws, constitutions or

contracts which may affect such decisions, the Explanatory Statement for

Banking (Prudential Standard) Determination No. 1 of 2014 stating:

“The Basel Committee on

Banking Supervision (BCBS) has developed a series of frameworks for measuring

the capital adequacy of internationally active banks. Following the financial

crisis of 2007-2009, the BCBS amended its capital framework so that banks hold

more and higher quality capital (Basel III). For this purpose, the BCBS

established in Basel III more detailed criteria for the forms of eligible

capital, Common Equity Tier 1 (CET1), Additional Tier 1(AT1) and Tier 2 (T2),

which banks would need to hold in order to meet required minimum capital

holdings.

Basel III provides that

AT1 and T2 capital instruments must be written-off or converted to ordinary

shares if relevant loss absorption or non-viability provisions are triggered.

Banking (prudential

standard) determination No. 4 of 2012 incorporated the Basel III developments

into APS 111 with effect from 1 January 2013. …”

(iii) Bank documentation implementing deposit accounts

Even if the words “any

other instrument” in Section 11CAA do not encompass deposits, there is a

further issue in relation to the implementation of bail-in of deposits

revolving around the issue of the documents/instruments issued by banks in opening

accounts and accepting deposits from customers.

The documentation issued by each Australian bank when

opening such an account, has a provision which enables the Bank to change the

terms and conditions from time to time without the consent of the customer. The

specifics of the power vary from bank to bank but each fundamentally contain

such a power. Some examples of various clauses are set out in Appendix 1.

If APRA as the Prudential Regulator issued a Prudential

Requirement Regulation or a Prudential Standard requiring a bank to insert a

provision into its documentation/instruments relating to deposit-taking

accounts providing for the bail-in of those deposits – their write-off or

conversion – then those provisions would then clearly come within the specific

provisions of conversion or write-off within the Act and the deposit the

subject of the account could be bailed-in immediately.

Such a directive could be issued by APRA in accordance with

the secrecy provisions in the Australian Prudential Regulation Authority

Act1998 and be implemented with little or no notice to the account holder.

Whilst not directly relevant to an interpretation of the provisions of the Act, there are a number of unusual and concerning aspects to its introduction, passing and intentions.

As noted above, the issue could now be simply resolved by

Government passing a simple amendment to the Act to explicitly exclude deposits

from being bailed in i.e. written off or converted into shares.

Whilst not beyond doubt, it is my opinion that the provisions of the Act do provide for a power of bail-in of bank deposits which did not exist prior to the passing of the Act.

Philip Gaetjens, Secretary to the Treasury addressed the Senate Estimates today on the budget. We are being helped by super-high iron ore prices, but downside risk sits in the household sector, and especially, the falls in property and household consumption.

Fiscal outlook

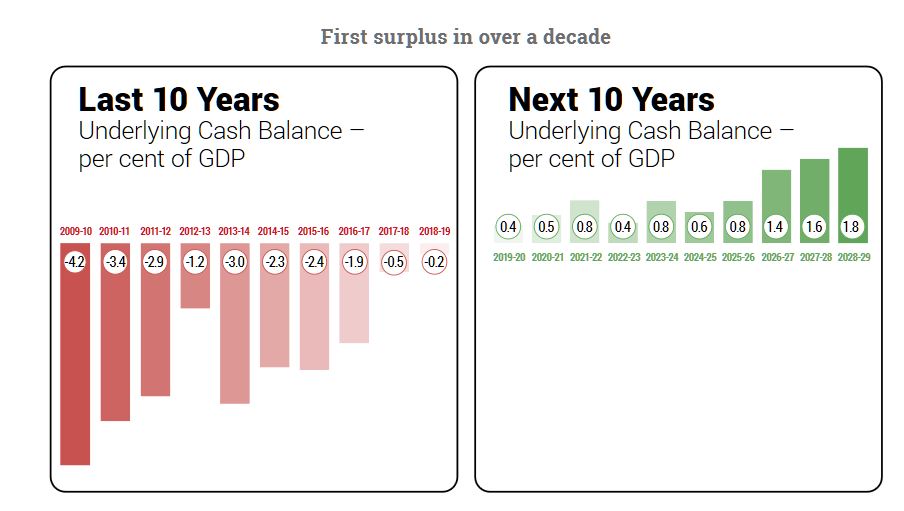

The Budget forecasts an underlying cash surplus in the 2019-20

financial year of $7.1 billion, the first surplus since 2007-08. It is

then forecast to increase to a surplus of $11 billion in 2020-21, with

sustained surpluses projected into the medium term. The fiscal outlook

continues to benefit in particular from commodity prices that have

remained at elevated levels, coupled with continued growth in resource

exports, which both support further expected improvement in company tax

collections in 2018‑19 and 2019-20.

Ongoing strength in iron ore and metallurgical coal prices since the

MYEFO and a consequent delay in the assumed phase down in these prices

have contributed to a higher terms of trade in 2018‑19. The Budget

prudently assumes a return to more sustainable levels over the next four

quarters. Nominal GDP growth is expected to be 3¼ per cent in 2019-20, ¼

of a percentage point lower than at the MYEFO, and 3¾ per cent in

2020-21. In contrast to the upgrade in the terms of trade, growth in

real GDP and domestic prices have been revised down, reflecting data

since MYEFO, including the weaker‑than‑expected December quarter 2018

National Accounts released on 6 March.

As I noted in my last statement to the committee, the path to

returning the budget to surplus has been a long one and reflects the

long lasting fiscal impacts of financial shocks and economic transitions

that occur as an economy rebalances. The long run of deficits has also

left Australia with substantially higher public debt levels. The

improved fiscal outlook now enables a greater focus on public debt

reduction to improve Australia’s position to meet future domestic and

international challenges.

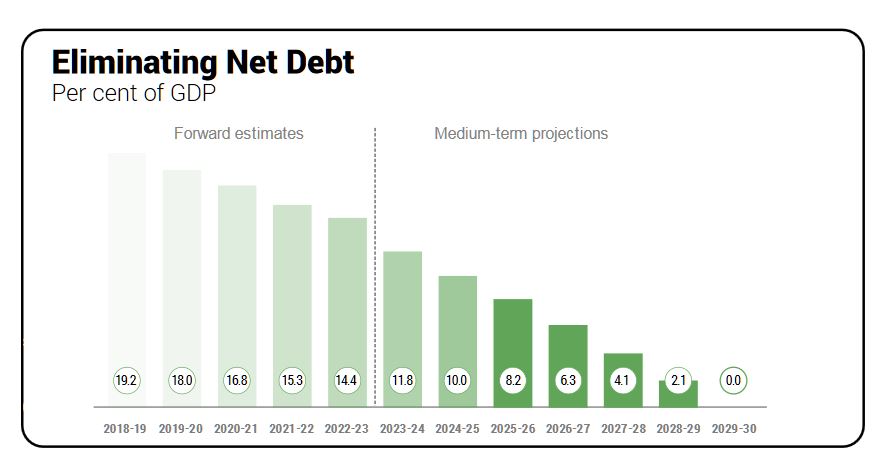

In the Budget, gross debt is expected to be 27.9 per cent of GDP in

2019-20, falling to 25 per cent of GDP at the end of the forward

estimates and further to 12.8 per cent of GDP by the end of the medium

term. Net debt is also expected to decline in each year of the forward

estimates and the medium term, falling from 18 per cent of GDP in

2019-20 to a projected zero per cent by 2029-30.

Domestic economic outlook

The economic data released since MYEFO were a bit weaker than had

been expected, which I highlighted in my address to the committee in

February. The December quarter 2018 National Accounts data confirmed the

slowing in momentum in the real economy in the second half of 2018,

although this followed two quarters of strong growth earlier in the

year.

Spending by the household sector, on both consumption goods and

housing, has moderated. We also know that housing prices have been

declining over the past year and a half. Falls in residential building

approvals since late 2017 are expected to flow through to lower dwelling

investment over the coming years. Consumption of discretionary items

has been particularly soft, including for those components that relate

to housing market conditions, such as household furnishings and motor

vehicles. While the pick‑up in growth in retail sales in February was

welcome, it followed a number of weak outcomes.

In contrast, non-mining investment has continued to grow at a solid

pace and spending by the public sector, including on services, such as

health and education, as well as on infrastructure, has been growing

above its long-run average rate. Mining investment is expected to grow

in 2019-20 for the first time in around seven years.

Despite some weakness in the real economy, there has been continued

strength in the labour market. Employment growth was above its long-run

average over the year to February, and the unemployment rate is now

4.9 per cent, a rate last recorded in June 2011. The participation rate

is close to its record high.

Growth in real GDP is forecast to be 2¾ per cent in 2019-20 and

2020-21. This is around Australia’s estimated potential growth rate.

Growth overall is expected to be supported by accommodative monetary

policy settings and the Australian dollar, which is one-third lower than

its 2011 peak against the US dollar.

Household consumption, business investment, and public final demand

are expected to contribute to growth over the forecast period. Dwelling

investment is expected to detract from growth over the forecast period,

particularly in 2019-20.

Solid economic growth is expected to continue to support employment

growth, which is forecast to be 1¾ per cent through the year to the June

quarter 2020 and the June quarter 2021. Consistent with positive

employment prospects, the participation rate is forecast to be 65½ per

cent and the unemployment rate is expected to be 5 per cent across the

forecast period. As economic growth strengthens and spare capacity in

the labour market continues to be absorbed, wage growth is expected to

pick up.

Before moving onto the global economic outlook, I would like to take a

moment to emphasise the importance of business liaison in formulating

Treasury’s economic forecasts. In the lead-up to the Budget, Treasury

conducted business liaison with a range of stakeholders, including

banks, mining companies, industry bodies, economists, state and

territory governments, representative organisations and small

businesses. These consultations provide detailed forward-looking

insights on the economic outlook, which directly inform our

deliberations on the economic forecasts. Our business liaison activity

also substantially benefits from Treasury’s state office presence in

Sydney, Melbourne and Perth.

Global economic outlook

Moving now to the global economic outlook, since MYEFO there has been

some deterioration in the outlook for global growth, particularly in

the euro area and economies outside of Australia’s major trading

partners. Reflecting this, forecasts for global growth have been

downgraded. Nonetheless, growth in Australia’s major trading partners is

forecast to continue to be robust, at 4 per cent in each of the

forecast years. Labour market conditions continue to be strong and

inflation remains relatively contained in most major advanced economies

compared with historical experience.

The United States economy continues to grow solidly. Wage growth has

picked up and inflation has increased slightly, closer to the target

rate. Growth in China is moderating, reflecting weaker domestic demand

as authorities address risks in the financial system and trade pressures

weighing on business confidence. With help from targeted macroeconomic

policies, China is expected to achieve the authorities’ target of 6.0 to

6.5 per cent growth this year. ASEAN-5 economies continue to perform

solidly, with domestic demand and favourable demographics supporting

growth.

As outlined in the Budget, there is a high degree of global

uncertainty, which appears to be weighing on measures of global

confidence amid a range of economic and geopolitical risks. These risks

include continued concerns about trade protectionist sentiment, high

levels of debt in a range of countries, including in Europe, and Brexit

risks, although Australia’s trade is oriented more towards Asia than

Europe. In the near term, there is also uncertainty about how quickly

activity in some countries will bounce back from temporary factors that

weighed on growth in the second half of 2018.

The federal government has announced a $600 million fighting fund to support the recommendations of the financial services royal commission, via InvestorDaily.

Buried

on page 167 of the hefty 2019 Federal Budget are the Hayne-related

expenses to be incurred by Treasury over the next five years.

The

government will provide $606.7 million over five years from 2018-19 to

facilitate its response to the Royal Commission into Misconduct in the

Banking, Superannuation and Financial Services Industry.

The

package comprises a suite of measures that fulfil the government’s

commitment to take action on all 76 of the recommendations of the Royal

Commission’s Final Report, including:

•

Designing and implementing an industry funded compensation scheme of

last resort for consumers and small business ($2.6 million over two

years from 2019-20);

•

Providing the Australian Financial Complaints Authority with additional

funding to help establish a historical redress scheme to consider

eligible financial complaints dating back to 1 January 2008 ($2.8

million in 2018-19);

•

Paying compensation owed to consumers and small businesses from legacy

unpaid external dispute resolution determinations ($30.7 million in

2019-20);

•

Resourcing the Australian Securities and Investments Commission (ASIC)

to implement its new enforcement strategy and expand its capabilities

and roles in accordance with the recommendations of the Royal Commission

($404.8 million over four years from 2019-20).

• Resourcing

the Australian Prudential Regulation Authority (APRA) to strengthen its

supervisory and enforcement activities which will support its response

to key areas of concern raised by the Royal Commission, including with

respect to governance, culture and remuneration ($145.0 million over

four years from 2019-20);

•

Establishing an independent financial regulator oversight authority, to

assess and report on the effectiveness of ASIC and APRA in discharging

their functions and meeting their statutory objectives ($7.7 million

over three years from 2020-21);

•

Undertaking a capability review of APRA, which will examine its

effectiveness and efficiency in delivering its statutory mandate, as

well as its capability to respond to the Royal Commission ($1.0 million

in 2018-19);

•

Establishing a Financial Services Reform Implementation Taskforce

within the Treasury to implement the Government’s response to the royal

commission, and co-ordinate reform efforts with APRA, ASIC and other

agencies through an implementation steering committee ($11.2 million in

2019-20); and

•

Providing the Office of Parliamentary Counsel with additional funding

for the volume of legislative drafting that will be required to

implement the Government’s response to the Royal Commission ($0.9

million in 2019-20).

The

cost of this measure will be partially offset by revenue received

through ASIC’s industry funding model and increases in the APRA

Financial Institutions Supervisory Levies and from funding already

provisioned in the Budget.

Lower taxes

Handing

down the Federal Budget 2019-2020 in parliament last night, Mr

Frydenberg said that the budget would restore the nation’s finances

without raising taxes.

“The

budget is back in the black and Australia is back on track,” the

treasurer said, announcing that the coalition delivered a $7.1 billion

surplus.

“Over

the last year the interest bill on national debt was $18 billion,” he

said. “We are reducing the debt and this interest bill, not by higher

taxes, but by good financial management and growing the economy.”

The government has announced immediate tax relief for low- and middle‑income earnersof up to $1,080 for singles or up to $2,160 for dual income families to ease the cost of living.

The coalition will also be lowering the 32.5 per cent rate to 30 per cent in 2024-25,

increasing the reward for effort by ensuring a projected 94 per cent of

taxpayers will face a marginal tax rate of no more than 30 per cent.

“The

Australian Government is lowering taxes for working Australians and

backing small and medium‑sized business, while ensuring all taxpayers,

including big business and multinationals, pay their fair share,” the

treasurer said.

Superannuation

The

Government will allow voluntary superannuation contributions (both

concessional and non-concessional) to be made by those aged 65 and 66

without meeting the work test from 1 July 2020. People aged 65 and 66

will also be able to make up to three years of non-concessional

contributions under the bring-forward rule.

Those

up to and including age 74 will be able to receive spouse

contributions, with those 65 and 66 no longer needing to meet a work

test.

“This measure is estimated to reduce revenue by $75.0 million over the forward estimates period,” the treasurer said.

“Currently,

people aged 65 to 74 can only make voluntary superannuation

contributions if they self-report as working a minimum of 40 hours over a

30 day period in the relevant financial year. Those aged 65 and over

cannot access bring-forward arrangements and those aged 70 and over

cannot receive spouse contributions.”

The

government will make permanent the current tax relief for merging

superannuation funds that is due to expire on 1 July 2020.

“This

measure is estimated to have an unquantifiable reduction in revenue

over the forward estimates period,” Mr Frydenberg said.

Since

December 2008, tax relief has been available for superannuation funds

to transfer revenue and capital losses to a new merged fund, and to

defer taxation consequences on gains and losses from revenue and capital

assets.

The

tax relief will be made permanent from 1 July 2020, ensuring

superannuation fund member balances are not affected by tax when funds

merge. It will remove tax as an impediment to mergers and facilitate

industry consolidation, consistent with the recommendation of the

Productivity Commission’s final report into the superannuation industry.

The

treasurer said consolidation would help address inefficiencies by

reducing costs, managing risks and increasing scale, leading to improved

retirement outcomes for members.

The government will also

reduce costs and simplify reporting for superannuation funds by

streamlining some administrative requirements for the calculation of

exempt current pension income (ECPI).

The

Government will allow superannuation fund trustees with interests in

both the accumulation and retirement phases during an income year to

choose their preferred method of calculating ECPI.

The

Government will also remove a redundant requirement for superannuation

funds to obtain an actuarial certificate when calculating ECPI using the

proportionate method, where all members of the fund are fully in the

retirement phase for all of the income year.

This measure will start on 1 July 2020 and is estimated to have no revenue impact over the forward estimates period.

FSC has mixed feelings

The

Financial Services Council (FSC) welcomed the government’s

superannuation changes to reduce red tape and improve access to

voluntary contributions.

“The

expansion of the work test exemption, spouse contributions and

bring-forward arrangements will provide workers nearing retirement

greater flexibility to make additional super contributions if they are

able. The electronic requests for release of super and simplification of

exempt current pension income calculations are sensible and welcome,”

FSC chief executive Sally Loane said.

“The

FSC also supports the tax relief for merging super funds, as this will

help the superannuation industry consolidate to reduce costs and improve

member outcomes.”

However,

the FSC is disappointed this is not part of a comprehensive product

rationalisation scheme, despite this being a longstanding government

commitment.

“A lack of reform in this area means consumers are locked into older, more expensive products,” Ms Loane said.

The FSC is pleased to note the Budget has largely kept the superannuation settings unchanged. However, Ms Loane said the council

is disappointed the government has failed to reform non-resident

withholding tax for managed funds in the Asia Region Funds Passport.

“This

means Australia will remain uncompetitive in our region, and Australia

will not be competing with Asian funds on a level playing field.

“The

withholding tax on managed funds raises little money, but harms our

competitiveness within Asia, putting Australia’s fund managers at a

major competitive disadvantage in the region.”

Treasurer Josh Frydenberg has said that the government will look at reviewing the impacts of removing trail in three years’ time rather than abolishing it next year as originally announced, following concerns regarding competition, via The Adviser.

In

an announcement on Tuesday (12 March), Treasurer Josh Frydenberg said

that “following consultation with the mortgage broking industry and

smaller lenders, the Coalition government has decided to not prohibit

trail commissions on new loans but rather review their operation in

three years’ time”.

The review, to be undertaken by the Council of

Financial Regulators and the Australian Competition and Consumer

Commission (ACCC) will therefore look at both the impacts of removing

trail as well as the feasibility of continuing upfront commission

payments.

Both the abolition of trail and upfront commissions were recommended by commissioner Hayne in his final report for the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

While the government had initially said in its official response to the final report

that it would ban trail commission payments for new mortgages from 1

July 2020, the Treasurer has now said that the removal on trail will

instead be reviewed in three years’ time.

“Mortgage

brokers are critically important for competition and delivering better

consumer outcomes in the mortgage market. Almost 60 per cent of all

residential mortgages are settled by mortgage brokers,” Mr Frydenberg

said on Tuesday.

“There are 16,000 mortgage brokers across

Australia – many of which are small businesses – employing more than

27,000 people. The government wants to see more mortgage brokers, not

less,” he said.

The Treasurer added that ASIC’s 2017 review of

broker remuneration “did not identify trail commissions as directly

leading to poor consumer outcomes and did not recommend the removal of

trail commissions”.

“Only the government can be trusted to protect

the mortgage broking sector and ensure that competition is strengthened

so consumers get a better deal,” he said.

Mr Frydenberg added that the government was “taking action on all 76 recommendations contained in the final report” of the banking royal commission and had already announced a number of new measures that will be brought in, including:

a best interests duty that will legally obligate mortgage brokers to act in the best interests of consumers;

a new requirement that the value of upfront commissions be linked to the amount drawn down by consumers;

a ban on campaign and volume-based commissions; and

a two-year limit on commission clawbacks.

“These

changes will address conflicts of interest in the industry by better

aligning the interests of consumers and mortgage brokers,” Treasurer Frydenberg said.

But the numbers in MYEFO show it has failed to hit many of its own targets.

Target 1: Surpluses on average over the cycle

The government’s overarching fiscal objective is to deliver budget

surpluses: not just in one year but on average over the economic cycle.

MYEFO indicates the government is expecting a $5.2 billion deficit in 2018-19 (0.3% of GDP).

It will be the 11th consecutive deficit for the Commonwealth budget.

Deficits have averaged $33.2 billion (2.1% of GDP) over those 11 years.

Yes, a $4.1 billion surplus is forecast for next year, with surpluses projected to reach $19 billion (0.9% of GDP) by 2021-22.

But so big have the recent deficits been, that even if everything

goes well and the fiscal position continues to improve, the budget would

need to be in surplus for decades to produce a surplus on average over

each year, far longer than what most economists consider a typical

economic cycle.

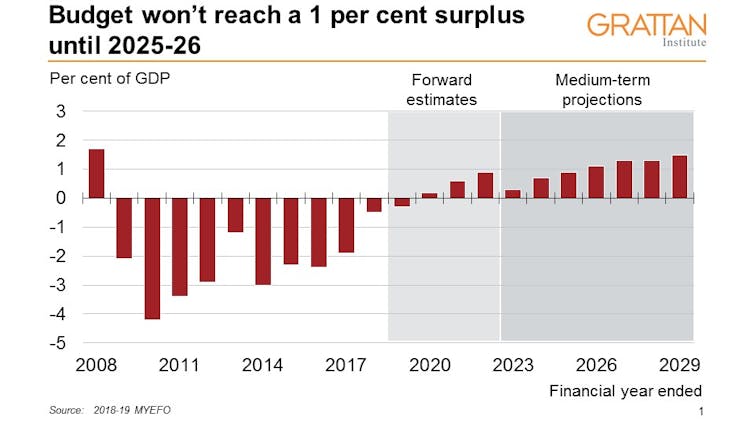

A related fiscal target is that budget surpluses will build to at least 1% of GDP as soon as possible.

Despite revenue windfalls from income and company taxes (discussed

below), the government is still forecasting it won’t reach that 1% of

GDP surplus target until 2025-26.

Policy decisions in this year’s budget and MYEFO – including income

and company tax cuts, additional funding for independent and Catholic

schools, and changes to the GST formula to placate Western Australia –

have weakened the bottom line in 2021-22 by $10.5 billion.

Hardly the actions of a government in a hurry to deliver a sizeable surplus.

Verdict: Fail.

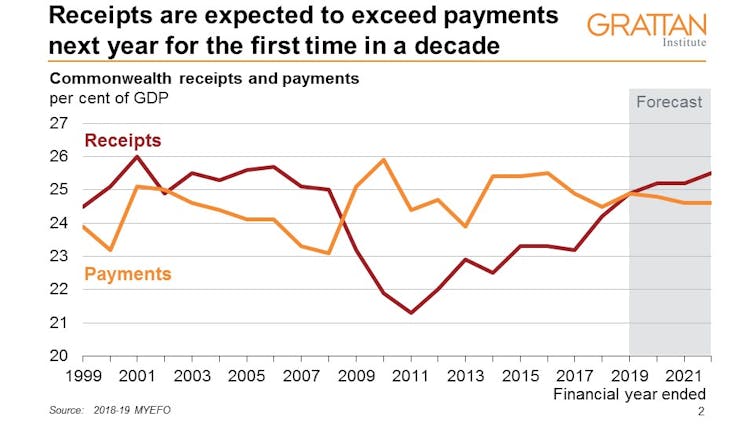

Target 2: Reduce the payments-to-GDP ratio

The government’s policy is also to maintain strong fiscal discipline

by controlling expenditure, with a falling payments-to-GDP ratio its

measure of success.

Whether it has met the target depends on the starting year.

Governments payments are forecast to reach 24.9% of GDP in 2018-19, up

from 23.9% in 2012-13 before the Coalition took office.

The government prefers the starting point of its first year in office 2013-14 where payments were 25.5% of GDP.

Either way, payments in 2018-19 remain above the 30-year historical average of 24.7% of GDP.

While the government projects that spending will fall slightly

further to 24.6% of GDP by 2021-22, this relies on spending growth

across the government’s major programs falling substantially compared to the previous four years – without major policy changes to help facilitate the fall.

Verdict: Debateable pass.

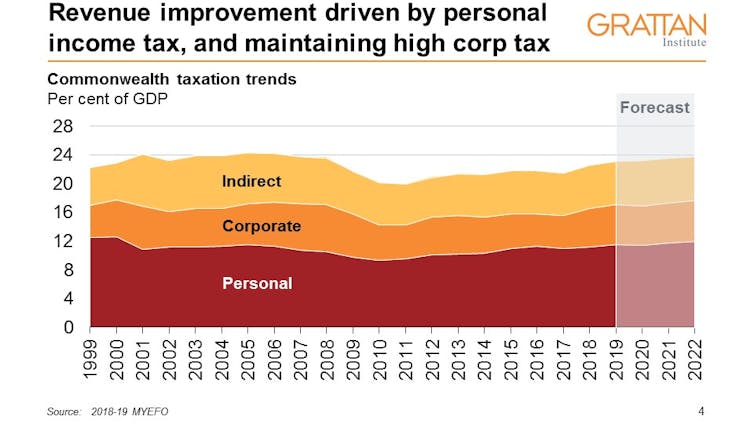

Target 3: Tax-to-GDP ratio below 23.9% of GDP

In last year’s budget, the government introduced a new target of capping tax collections at 23.9% of GDP.

Why 23.9%? That was the average level of tax during the final two terms of the Howard/Costello government.

While the Coalition is understandably keen to follow the lead of one

of its most electorally successful governments, that was also a period

where tax collections were historically high.

Tax collections are projected to reach 23.8% of GDP in 2022, on the

back of stronger than forecast personal income tax and company tax

receipts.

Verdict: Pass.

MYEFO Chart.

Target 4: New spending measures more than offset by reductions in spending elsewhere

Since becoming prime minister, Scott Morrison has sent mixed signals

about whether his government will adhere to the longstanding budget rule

that all new spending proposals be matched with budget savings.

At the MYEFO press conference, Finance Minister Matthias Cormann said it was a “matter of balancing competition priorities”.

Here’s the straight answer – the net effect of policy changes

announced in MYEFO are an additional $12.2 billion in spending over four

years.

In other words, the government has not offset new spending with cuts

to other spending programs. The Turnbull government similarly failed to

offset its new spending in 2017-18 (although it succeeded in prior

years).

There have been some reductions in spending because of improvements

in the economy. The government claims these reductions offset its recent

spending announcements. But genuine offsets come from policy changes,

not economic good luck.

Verdict: Fail.

Target 5: Shifts due to changes in the economy banked as an improvement in budget bottom line

This objective is key to the government’s fiscal conservative credentials.

If it has some economic good luck, it commits to use the proceeds for budget repair rather than new spending or tax cuts.

This rule has been irrelevant for most of the past decade, because

almost every budget had revenue collections falling short of forecast.

But the Morrison government is in the middle of a mini revenue boom –

revenue collections were higher than forecast in both the 2018-19

budget and MYEFO.

Company tax collections are higher largely due to strong commodity

prices. Income tax collections are up and government spending is down

because of improvements in the economy.

So has the government used this chance to show off its fiscal prudence?

Not exactly. It will spend around $11.8 billion of this windfall,

give away another $19.3 billion in tax cuts and bank just over half of

it ($35.2 billion) to the bottom line.

And in the shadow of an election, we can almost certainly expect

further spending. The $9 billion in decisions taken but not announced –

potentially a pre-election warchest – suggests that more tax cuts could

also be on the way.

Verdict: Fail.

Our final verdict

The challenge in assessing budget management is separating good luck

from good management. Governments will always seek to take credit for

economic upswings that boost the bottom line.

Fiscal targets are there to keep them on the straight and narrow.

An objective assessment of the government’s performance against its

own key targets suggests its good news budget is more mirage than

magnificent management.

Authors: Danielle Wood, Program Director, Budget Policy and Institutional Reform, Grattan Institute; Kate Griffiths Senior Associate, Grattan Institute

A welcome move, the shadowy Council Of Financial Regulators has started publishing minutes of its quarterly meetings. However, group think, and self-interest is all over it. Specifically the comments about tighter credit, and the need to continue to lend (to keep the debt bomb ticking a bit longer! Also how does independence of the RBA work in this context?

They noted that non-ADI lending for housing has been growing significantly faster than ADI housing lending and there is some evidence that non-ADI lending for property development is also increasing quickly.

As part of its commitment to transparency, the Council of Financial Regulators (the Council) has decided to publish a statement following each of its regular quarterly meetings. This is the first such statement.

The statement will outline the main issues discussed at each meeting. From time to time the

Council discusses confidential issues that relate to an individual entity or to policies still

in formulation. These issues will only be included in the statement where it is appropriate to

do so.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s

main financial regulatory agencies. There are four members: the Australian Prudential

Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC),

the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor

chairs the Council and the RBA provides secretariat support. It is a non-statutory body,

without regulatory or policy decision-making powers. Those powers reside with its members.

The Council’s objectives are to contribute to the efficiency and effectiveness of financial

regulation, and to promote stability of the Australian financial system. The Council

operates as a forum for cooperation and coordination among member agencies. It meets each

quarter, or more often if required.

At each meeting, the Council discusses the main sources of systemic risk facing the

Australian financial system, as well as regulatory issues and developments relevant to its

members. Topics discussed at its meeting on 10 December 2018 included the following:

Financing conditions. Members discussed the tightening of credit conditions for households

and

small businesses. A tightening of lending standards over recent years has been appropriate

and

has strengthened the resilience of the system. At the same time, members agreed on the

importance of lenders continuing to supply credit to the economy while they adjust their

lending

practices, including in response to the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry. Members discussed how an overly cautious

approach by some lenders to incorporating relevant laws and standards into loan approval

processes may be affecting lending decisions.

Members observed that housing credit growth has moderated since mid-2017, with both demand

and supply factors playing a role. The demand for credit by investors has slowed noticeably,

largely reflecting the change in the dynamics of the housing market. In an environment of

tighter lending standards, the decline in average interest rates for owner-occupier and

principal and interest loans suggests that there is relatively strong competition for

borrowers of low credit risk. Credit to owner-occupiers is continuing to grow at 5 to 6 per

cent.

Non-ADI lending. The Council undertook its annual review of non-bank financial

intermediation. Overall, lending by non-ADIs remains a small share of all lending. However,

non-ADI lending for housing has been growing significantly faster than ADI housing lending

and there is some evidence that non-ADI lending for property development is also increasing

quickly. The Council supported efforts to expand the coverage of data on non-ADI lenders,

drawing on new data collection powers recently granted to APRA.

Housing market. Members discussed recent developments in the housing market.

Conditions have eased, but this follows a period of considerable strength in the market.

Housing prices have been declining in Sydney, Melbourne and Perth, but are stable or rising

in most other locations. The easing in the housing market is occurring in a period of

favourable economic conditions, with low domestic unemployment and interest rates and a

supportive global economy. The Council will continue to closely monitor developments.

Prudential measures. APRA briefed the Council on its latest review of the countercyclical

capital buffer, the results of which will be published in the new year. It also provided an

update on its residential mortgage measures, including the investor lending and

interest-only lending benchmarks. In line with APRA’s announcement in April 2018 that it

would remove the investor lending benchmark subject to assurances of the strength of lending

standards, the benchmark has now been removed for the majority of ADIs. The interest-only

lending benchmark, introduced in 2017, has resulted in a reduction in the share of new

interest-only lending, along with the share of interest-only lending that occurs at high

loan-to-valuation ratios.

Financial sector competition. The Council discussed work by its member agencies in response

to the Productivity Commission’s Final Report of its Inquiry into Competition in the

Australian Financial System. The Council strongly supports improved transparency of mortgage

interest rates and a working group is examining a number of options. The Council also

discussed the Productivity Commission’s recommendations relating to lenders mortgage

insurance and remuneration of mortgage brokers.

Both the Productivity Commission and the Financial System Inquiry recommended a review of the

regulation of payments providers that hold stored value – referred to in legislation as

purchased payment facilities (PPFs). The Council released an issues paper in September and held

an industry roundtable in November. Members considered the feedback received from these

processes and received an update on progress with the review.

Limited recourse borrowing by superannuation funds. Members discussed a report to Government

on leverage and risk in the superannuation system, as requested in the Government’s response to

the Financial System Inquiry. The use of limited recourse borrowing arrangements remains

relatively small, but has risen over time. Leverage by superannuation funds can increase

vulnerabilities in the financial system, though near-term risks have reduced with the shift in

dynamics in the housing market.

International Monetary Fund’s Financial Sector Assessment Program (FSAP). The FSAP review of

Australia was conducted during the course of 2018; preliminary findings were presented to the

Australian authorities in November. The Council held an initial discussion of the main FSAP

recommendations and how they could be addressed. The FSAP will be finalised in early 2019, at

which time summary documents will be published. (Further information on the FSAP review was

published in the Reserve Bank’s October 2018

Financial Stability Review.)

Representatives of the Australian Competition and Consumer Commission and the Australian

Taxation Office attended the meeting for discussions relevant to their responsibilities.

In a statement issued today, Treasurer Scott Morrison said the reform will represent the “most significant increases in maximum civil penalties in twenty years”.

These increases are right, as before the financial impact of poor behaviour was very low However, do not be misled, changing penalties will not address the fundamental cultural, structural and economic issues which have combined to deliver a finance sector which is simply not fit for purpose.

We need a removal of incentives from the advice sector (mortgage brokers included). Actually we need unified regulation across credit and wealth sectors (the current two regimes are an accident of history).

We need structural separate and disaggregation of our financial conglomerates. We need a realignment of interests to focus on the customer – which by the way is not at odds with shareholder returns, as customer focus builds franchise value and returns in the long term.

We need cultural reform and new values from our finance sector leaders. (Executive Pay should come under the spot light).

We need a reform of the regulatory structure in Australia, because they are captured at the moment at least by group think, and their interests are aligned too closely to the finance sector. This must include ASIC, APRA, RBA and ACCC. All have bits of the finance puzzle, but no one is seriously accountable.

But there is a more fundamental issue. We have relied on overblown credit, and superannuation sectors, as a proxy for high quality economic growth. This inflated housing and lifted household debt.

We need a fundamental economic reset, because reforming financial services alone won’t solve our underlying issues.

Here are the changes:

The government will increase penalties under the Corporations Act to:

“For individuals: (i) 10 years’ imprisonment; and/or (ii) the larger of $945,000 OR three times the benefits;

For corporations: (i) the larger of $9.45 million OR (ii) three times benefits OR 10% of annual turnover.

“The Government will expand the range of contraventions subject to civil penalties, and also increase the maximum civil penalty amounts that can be imposed by courts, to the maximum of:

the greater of $1.05 million (for individuals, from $200,000) and $10.5 million (for corporations, from $1 million); or

three times the benefit gained or loss avoided; or

10% of the annual turnover (for corporations).

“In addition, ASIC will be able to seek additional remedies to strip wrongdoers of profits illegally obtained, or losses avoided from contraventions resulting in civil penalty proceedings.”

The Treasury released a request for submission relating to the thorny issue of digital exclusion, and specifically the fact that some companies, in a drive to digital first, are starting to charge consumers to continue to receive paper bills, for services such as utilities. There is already legislation in some other countries to protect consumers from this.

The Treasury suggest a range of options:

Option 1 — the status quo, with an industry led consumer education campaign;

Option 2 — prohibition (ban) on paper billing fees;

Option 3 — prohibiting essential service providers from charging consumers to receive paper bills;

Option 4 — limiting paper billing fees to a cost recovery basis;

Option 5 – promoting exemptions through behavioural approaches.

As we discussed last week, they suggest 1.2 million households are digitally excluded by not having access to the internet.

The Keep Me Posted Lobby Group (who contacted me after last week’s post) advocates there should a ban on paper billing fees.

“We clearly stated Keep Me Posted’s position to support a total ban on all billing fees, which is option 2 of the consultation paper,” said Kellie Northwood, Executive Director, Keep Me Posted.

To add weight to be debate we wanted to make two points.

FIRST – the Treasury estimate understates the number of households who are digitally excluded and so more would be potentially hit by excess bill charges.

SECOND – we believe option 2 – ban fees is the right option.

How Many Households Are Digitally Excluded?

We use data from out rolling 52,000 household surveys across Australia.

The result suggests that it is not just access to the internet which is an issue, but there are some households who just are unwilling or unable to use the internet. In fact the Treasury’s estimate of the number of households impacted is understated.

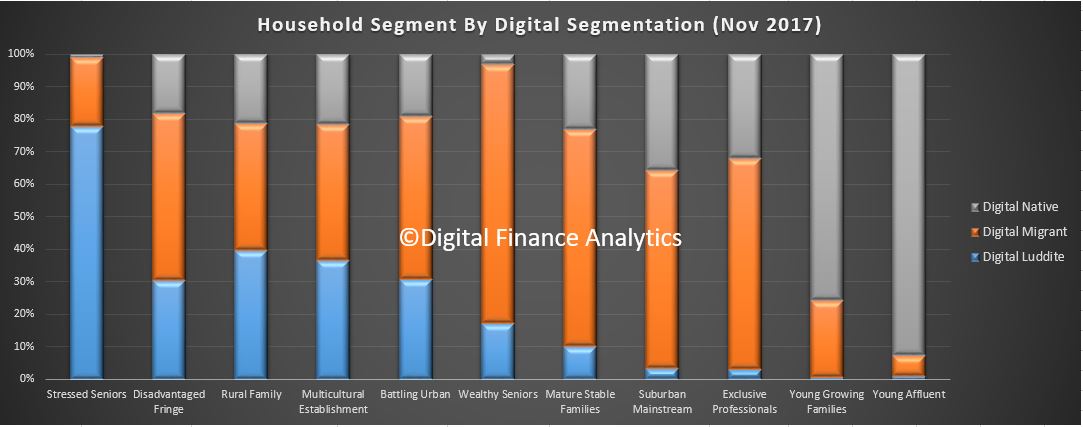

We segment households, digitally speaking into three group.

DIGITAL NATIVES: Households who are naturally digital, using mobile devices, constantly online and using social media, often using multiple devices including tablets and smart phones.

DIGITAL MIGRANTS: Households who are moving from terrestrial services to digital, taking up smart devices and learning to access social media and other online services.

DIGITAL LUDDITES: Households who prefer terrestrial services, but who are now starting to migrate online and are reluctantly adopting the new paradigm. In many cases they are unwilling or unable to migrate.

We also use our master household segmentation, which is based on multi-factorial geo-demographic and behaviourial analysis, though based on our rolling 52,000 household survey.

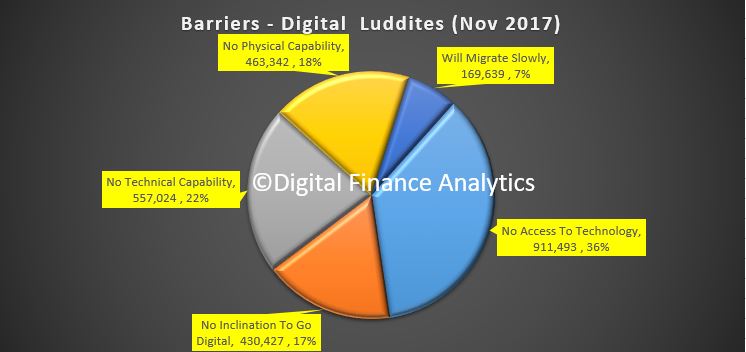

The results show that Digital Luddites are predominately in the older and less wealthy households, including Stressed Seniors, those living in the disadvantaged fringe areas around our major cities, those in a rural setting, and those from non-English speaking ethnic backgrounds. Count up all the Digital Luddites and it comes to 27% or 2.6 million households.

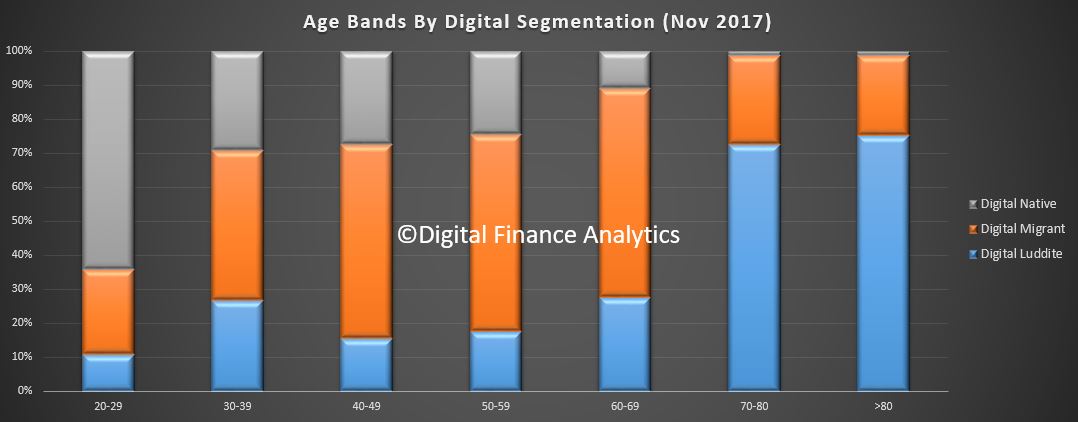

We can examine the splits by age bands, and confirm that older households are more likely to be in this group.

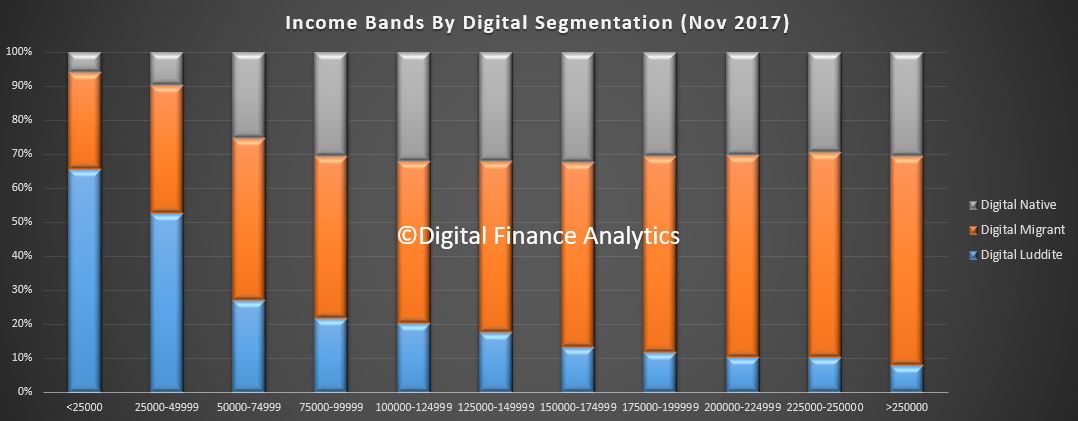

Analysis by income band highlights that significantly more are in the lowest income range, including many on pensions and Government support.

We were able to examine the barriers which were driving households into the Luddite group. We found that whilst 7% (around 170,000) are likely to migrate to digital channels, if slowly; 36% (around 911,000) households did not have access to the internet, or usable device; 17% (around 430,000) had no inclination to go digital, even if they could; 22% did not have the technical capability – could not operate a smart phone, did not know how to get to connect to the internet – (around 557,000); and 18% (around 463,000) did not have the physical capability (thanks to disability or other factors).

Stripping back the analysis to a financial capability (did they have the funds to purchase a device, internet access etc), then we estimate 54% of Luddites were impacted by these economic factors, or 1.36 million households.

We believe therefore the Treasury estimate of the number of households impacted by digital exclusion is understated. This adds more weight for intervention.

The Right Choice Is: Option 2 – Fees Should Be Banned

Companies are clearly able to save money if they can stop sending out paper versions of statements, and rely on customers to receive online notification and then retrieve their statements. This economic driver is understood, though most often the initiate will be dressed up as “environmentally friendly”, or “more convenient”. It appears though that savings are not passed back to consumers directly, but flow into general funds.

Our research suggests that a considerable number of households are unable to go digital. Thus they risk having additional fees and charges imposed on them, with no mitigating option. This is in effect a price rise. Whilst education, and communication to households may assist some, many are not able to migrate. These are the least wealthy, older and more exposed households. This is not equitable.

In some cases it appears charges for bills are significantly higher than the incremental charge based on an estimate of what the incremental cost should be, and in any case, experience from the banking sector highlights suggests it is difficult to get a definitive incremental estimate of the cost of a bill. We think restricting the acceptable charge to cost to recovery, is complex, cannot be audited, and offers too much wriggle room.

We cannot support the differentiation between essential and non-essential services, not least because the threshold would potentially vary by household circumstance, and we cannot see a justification for charging for paper billing in some circumstances, but not others.

Therefore charges for paper billing should be banned.

Companies would be welcome to offer discounts to those receiving electronic delivery (although the ACCC may have to ensure that overall costs of service are not lifted to facilitate the subsequent discounting!)

Blog")