At a speech given at Bloomberg in London, Ian McCafferty, external member of the Monetary Policy Committee, argued that the tight credit conditions which followed the financial crisis have now “diminished markedly” for firms – a fact which has important implications for monetary policy.

McCafferty’s analysis indicates that both large and small firms have been broadening their sources of finance away from banks. While large firms have turned increasingly to capital markets, with growing bond and equity issuance, SMEs have been drawing on new alternative sources of lending, including ‘crowdfunding’ and peer-to-peer lending platforms.

McCafferty warned that it was important to recognise that this form of finance is still small compared to bank lending, on which SMEs remain heavily reliant, but added: “alternative finance is growing, and is likely to be a developing feature of the market in future years.”

McCafferty noted that the UK economy continues to face headwinds – notably fiscal consolidation and sub-par growth in the world economy. However, he argued that the reduction the headwinds in business finance is now supporting the normalisation of the economy. With that, he said: “it is reasonable to expect the neutral interest rate – the level of interest rates consistent with full employment and inflation at target – to also move towards more normal levels”.

He concluded: “If we on the MPC are to achieve our ambition of raising rates only gradually, so as to minimise the disruption to households and businesses of a normalisation of policy after a long period in which interest rates have been at historic lows, we need to avoid getting ‘behind the curve’ with respect to the neutral rate. And for me, that provides an additional justification not to leave the start date for lift off too late.”

Labour party leader Jeremy Corbyn this week unveiled his new team of economic advisers. He hopes they will help build a set of policies capable of countering the narrative of belt-tightening austerity which delivered David Cameron and George Osborne into Downing Street back in May.

Corbyn and shadow chancellor John McDonnell are scheduled to meet four times a year with the seven-strong group which includes people like Thomas Piketty and Mariana Mazzucato. Also on the panel is City University professor Anastasia Nesvetailova, an expert on the international financial sector and its role in the global financial crisis of 2007-09. We asked her to give her thoughts on four policy areas reportedly under consideration by Corbyn and his team:

Q: The new Labour leadership has indicated support for a financial transaction tax, but why does support for this ebb and flow so much?

The idea for the Tobin tax, so called after the economist James Tobin suggested it in the late 1960s to early 1970s, has been long debated. This concept of applying a relatively tiny tax to every financial transaction tends to be evoked in the midst of financial crises and instability, or whenever the costs of finance to society appear to outweigh the benefits of deregulated finance.

Forex fight.REUTERS/Damir Sagolj

It may be comparatively mature as a concept then, but the Tobin tax has been difficult to implement in real policies. During its early life, the idea was eclipsed by the paradigm of monetarism and free markets of the 1970s and 1980s. And throughout there have remained unresolved technical issues about its implementation.

One major divisive issue has been the scope of a possible tax: should it be universal and global (to minimise regulatory arbitrage), or can it be implemented on a different scale by individual nation states? The Tobin tax was originally proposed to target the foreign exchange market – a segment of financial volatility, speculation and bubbles. Today though, we know that the foreign exchange market is only one part of the financial system – albeit a very large part at about a US$5 trillion daily trading volume.

Many other financial transactions today are multi-layered and multi-jurisdictional – very often they involve complex credit contracts. And so a tax designed when the realities of financial markets were quite different and less advanced may not be applicable to all financial transactions today uniformly.

Another issue is how to tailor such a measure to the complexity of today’s financial structures and not harm the needs of businesses and consumers who rely on the foreign exchange market for their daily business needs. Finance is famously prone to speculation and bubbles, but it is an organic and very central sphere of economic activity in advanced, highly financialised capitalism; we need to be cautious about tinkering with the inner workings.

Q: Is there a future for Britain free of the dominance of the financial sector?

This is a tricky question, because it presumes that the financial sector is counterpoised to the rest of economic activity. In reality, we are all part of finance today, and that includes the shadow banking system – a complex set of non-bank financial intermediaries, transactions and entities. Overall, the City of London financial sector plays a crucial role in providing market and funding opportunities for the economy. A better question would be to ask: how can the financial sector today work for society?

It is true that competition and financial innovation can and does spur economic growth and makes our daily lives much easier: it is convenient to rely on credit cards when you travel or to be able to take a mortgage. But financial innovation is also inherently very risky. Hyman Minsky, the theorist of financial fragility who did not live to see many of his predictions come true, said that in advanced capitalism there is always a trade-off between financial innovation and economic stability. Looking back at the unresolved legacy of the 2007-09 crisis, it is clear that the question about who should assume the risks incurred by the financial industry during the “good times”, has not been addressed by policy-makers fully.

Taxpayer funded. RBS.REUTERS/Luke MacGregor

Instead, society and the state, were made to work for finance: in 2007-08, the risks from financial innovation were socialised and austerity measures followed. This happened against the big gains from financial innovation that had been privatised by the finance industry. As a result, despite the progress on the financial reforms since 2008, we are ill-prepared for the next financial crisis, which according to Minsky, is certain to come.

Q: What should a new Bank of England mandate look like?

The Bank of England should remain independent, but it should have the power and the tools to continue to act as a stabiliser of the economy and be able to intervene with a diverse and flexible range of tools during a period of financial crisis or instability. It is important to understand that uncertainty about central banks’ mission and mandate today is not a unique problem of the UK.

During the crisis of 2007-09, the central banks on both sides of the Atlantic stepped in and played a role that they were not meant to. We are lucky that they did so. Against many economic dogmas, they were not simply lenders of last resort, they made the markets, as my colleague Perry Mehrling argues in his book New Lombard Street. They made the markets when liquidity vanished and when private participants, buyers and sellers, simply would not pick up the phone.

In the wake of Lehman, along with the governments, central banks saved the payment system from a collapse. And although it was meant as a temporary solution, there was no exit strategy from that role. Up to this day, central banks are de facto in charge of much more than simply price stability.

Notes and queries. How can the BoE be better put to use?natalie, CC BY-NC

The problem is that the formal mandate of the Bank of England is too narrow for what is required of the central bank in the advanced financialised context. The risk is that during the next financial crisis they may not have the tools to intervene. Central banks are major actors in financially advanced economies and in any plans for a major recovery they are likely to remain so. They will need new tools to deal with what will be an unavoidably a complex crisis.

Q: Is there a feasible place for public ownership in the banking sector?

Again, an interesting question because somehow it assumes that public ownership is alien to the banking system. In reality, public ownership is already present in finance: as a policy measure when banks are nationalised and a potential measure when a bank is identified as a systemically important institution and its failure threatens the economic stability.

One of the major triggers of the great transformation of banking in late 20th century was the move (in the US) to put investment banks into the hands of markets and the ownership of shareholders. The major consequence of that decision was that the risks that previously were theoretically containable in closed partnerships arrangement, were potentially socialised. Simply put, large bank holding companies trading in the markets have systemic consequences for the economy – and a collapse may trigger systemic risks beyond this particular institution.

This is exactly what happened in 2007-09, when the UK government had to nationalise several banks in order to save them from a collapse. Since banks are crucial systemic institutions in our economy, and since they perform many utility-like functions (payments, clearing) critical for the economic security of the country, it can be argued that public ownership is best suited to guard the public interest in utility banking. And in fact, given our experience in the financial crisis, it can be argued that they were, in effect already nationalised.

I can anticipate a counterpoint from the banking industry: public ownership is wasteful, it stifles innovation and competition. But while the benefits of privately-owned banking groups are difficult to quantify, data suggests that bank executives and managers were rewarded handsomely even as their institutions were making losses and were on a public liquidity drip and, further, that in finance, innovation takes the form of regulatory arbitrage and avoidance, rather than the benign pursuit of the public good.

Author: Anastasia Nesvetailova, Professor of International Politics, Director of the Global Political Economy MA, City University London

Released by the Bank of England, “Don’t just do something, stand there”… (and think) was David Miles final speech as an external MPC member reflects on the past six years of low interest rates, the lessons we can take from the financial crisis and where monetary policy might go from here. In particular he discusses the value of using macro-prudential tools versus interest rates in tackling financial instability.

Speaking at the Resolution Foundation, David explains that when he joined the MPC in June 2009, interest rates had already been cut to the record low of 0.5% and the Bank bought £75 billion of government assets via its quantitative easing programme. At the time no one on the Committee would have predicted that more than six years later Bank Rate would still be 0.5%; that the Bank would have made a further £300 billion of assets purchases and none would have been sold; that inflation would be 0% and that the market implied Bank Rate three years ahead (mid 2018) would be only around 1.6%.

“All this is a sign of the enormous and lasting disruption that came after the financial crisis of late 2008.”

Conditions, however, have started to change and now “the case for beginning a gradual normalisation in the stance of monetary policy is stronger than at any time since I joined the committee over 6 years ago.” Having been called an “arch-dove” in the past some might think it “bizarre” for David to say this. But, he says, “they should not; the ‘hawk – dove’ labels are pretty silly because they suggest some unchanging genetic tendency towards favouring one type of policy; anyone who was like that would be very ill suited to be on the MPC.”

Dealing with the aftermath of the financial crisis has proved exceptionally hard, but there are lessons we can take from it for both financial stability and monetary policy. First, “the best way to handle the risks of incurring huge costs from another financial crisis is to control leverage in the financial sector”. Since the crisis, policy makers have debated the value of using macro-prudential tools versus interest rates in tackling financial instability. David argues that the UK is going down the right route by increasing capital requirements and reducing leverage in the banking sector rather than “skewing monetary policy towards trying to stop financial instability problems”.

Second, we have learnt more about the dynamics of the effective lower bound (ELB) and the efficacy of QE. When central banks the world over cut interest rates to their ELB many believed that the risks of self- reinforcing deflation and protracted slumps had increased sharply and that asset purchases were not likely to help much. In the end, only a few OECD countries experienced outright deflation and falls in short term inflation expectations were temporary.

Turning to the likely future path of monetary policy, given the current outlook David finds that though “it is not all good news” we are in “a much better place than we have been: unemployment is down to just under 5.5%; annualised GDP growth has been near 3% for several quarters; consumer and business confidence has risen sharply over the past year or so; the household saving rate is low and suggests that spending is not being held back by expectations of low near term inflation; wages are rising; the availability of finance has risen and its cost fallen; corporate profitability looks solid.”

So where might Bank Rate be heading? “That question could be couched in terms of so called r* (the appropriate interest rate to keep inflation on track and demand in line with productive capacity)”. A number of factors might mean that this rate will be “significantly lower than in the past”, four important ones are: increased credit spreads, fiscal headwinds, secular stagnation and demographics. David concludes that the combination of these factors, and their various weights, could lead to a rough estimate of r* three years or so down the road of around 2.5 – 3%, relative to the 4.5 – 5% prior to the crisis. This lower range is “some way north of the conditioning assumption used at the time of the May Inflation report of just under 1.5%.”

“Given that, and given that many of the after effects of the mess of 2008 do seem to have faded (e.g. the drying up of bank credit) then I think a first move up in Bank Rate soon is likely to be right. I do not attach great weight to the idea that starting this process will create great risks of dropping back into very weak growth, falling into negative inflation and engendering a splurge in risk avoiding behaviour. I attach more weight to the risks of waiting too long and then not being able to take a gradual path to a more normal stance for monetary policy.” David adds, “one thing the MPC will not do (and never has) is just follow another big central bank; it is a daft idea that we cannot raise rates in the UK before the US and also cannot be long behind them.

“As conditions change you change your view on what is right; and things have changed a lot in the UK in the past year or so and very largely for the better. Now is closer to the right time to start a gentle amble back towards a more normal setting for monetary policy…”

The implementation of bank ring-fencing in the UK continues a trend of dilution and flexibility by granting additional, albeit minor, concessions to the banks and remaining silent on the important subject of intra-group limits, says Fitch Ratings. The Prudential Regulation Authority’s (PRA) concessions in their end-May statement follow earlier watering-down of proposed rules for ring-fenced banks (RFB) by the UK government, which allowed more activities to be included within the ring-fence.

Fitch believes that only six of the largest UK retail banks will be subject to the ring-fencing rules, and of these only HSBC and Barclays are likely to have significant operations outside the ring-fence. Ultimately, the strength of the ring-fence will have rating implications for the entities within UK banking groups.

The PRA’s statement and near-final rules show that it is staying with the overall approach outlined in the October 2014 consultation. However, by clarifying that certain key aspects will be reviewed on a case-by-case basis and reminding the banks that it is possible to request waivers and modifications, the PRA has introduced additional flexibility. Banks may still have some room for manoeuvre because final rules will not be published until 3Q15 and banks will have until 2019 to comply.

Core issues such as the ‘large exposures limit’ on intra-group exposures between an RFB and the rest of its group and intra-group dividends are still open. UK banks argue that they need clarity to plan for future group treasury management and capital allocation. Under EU rules, the PRA could elect to limit large exposures to 10% of a RFB’s capital. We believe this tight limit would strengthen the ring-fencing and protect RFBs from riskier group activities.

Banks requested clarification about what types of subsidiaries can and cannot be owned by an RFB. A prescriptive list of permitted activities will not be published by the PRA, rather banks will have the opportunity to discuss subsidiary business lines with it on a case-specific basis. This could result in a broader range of permitted activities for RFBs, helping to diversify revenues and simplify operational functions, but also widen the net to include higher-risk business lines.

HSBC indicated recently that it intends to widen the scope of activities included in its RFB. The over-riding guideline is that a subsidiary should not expose the RFB to any risk affecting its ability to provide core activities in the UK. The relative size of subsidiaries will also be considered by the PRA under its ‘proportional’ approach, especially if these are undertaking activities largely unrelated to the RFB’s line of business.

RFBs must be able to take decisions independently and guidelines for board membership, risk management and internal audit arrangements aim to achieve this. Banks queried some of the board cross-membership restrictions and the PRA clarified that board membership rules do not apply to RFB sub-groups. This will make it easier for RFBs to fill the boards of their ring-fenced subsidiaries and affiliates.

Under its proportionality approach, the PRA can consider further waivers to governance arrangements, especially if compliance with the rules proves to be overly burdensome. Lloyds Banking Group is seeking a waiver on the requirement for its RFB, which will make up around 90% of the group, to have a different board of directors to that of its group. The PRA also clarified that RFBs are not prevented from relying on group services from other group entities, which is important if RFBs are to contain costs.

In our view, RFBs will still face some governance conflicts. The rules allow for some board members to be group employees, hold director positions in other group companies and independents can have occupied group positions subject to some restrictions. All board members can receive part of their remuneration in the form of listed shares in a group company. The practical implementation of governance rules will be important to ensure that the right balance is struck between achieving synergies between the RFB and the rest of its group and limiting the direct exposure, both financial and otherwise, to improve the resolvability of the group.

The UK’s financial system is not “entirely safe” according to former Bank of England governor Lord Mervyn King, speaking on BBC Radio 4’s Today programme. He questioned the banking system’s ability to withstand another crisis and argued the core problems that led to the meltdown have not yet been dealt with.

“I don’t think we’re yet at the point where we can be confident that the banking system would be entirely safe. I don’t think we’ve really yet got to the heart of what went wrong.”

King, went on to say that imbalances between global economies have not yet been resolved. He added keeping base rate at the low of 0.5 per cent cannot go on .

“The idea that we can go on indefinitely with very low interest rates doesn’t make much sense.” However raising interest rates now “would probably lead to another downturn”.

He was at the helm of the Bank of England during the GFC.

His comments mirror some of the concerns highlighted in the recent Murray report.

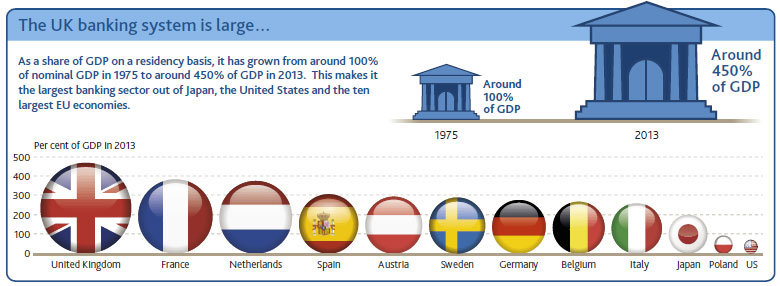

In the light of the FSI report, and the emphasis on the need to secure the Australian economy from potential risks relating to banks which may be too big to fail (TBTF), there is a timely article in 2014 Q4 Quarterly Bulletin from the Bank of England on the consequences of the UK’s large banking sector, which is estimated to be about 450% of GDP. Why is the UK banking system so big and is that a problem?

The UK banking sector is big by any standard measure and, should global financial markets expand, it could become much bigger. Against that backdrop, this article has examined a number of issues related to the size and resilience of the UK banking system, including why it is so big and the relationship between banking system size and financial stability.

There are a number of potential reasons why the UK banking system has become so big. These include: benefits to clustering in financial hubs; having a comparative advantage in international banking services; and historical factors. It may also reflect past implicit government subsidies. Evidence from the recent global financial crisis suggests that bigger banking systems are not associated with lower output growth and that banking system size was not a good predictor of the crisis (after controlling for other factors). On the other hand, larger banking systems may impose higher direct fiscal costs on governments in crises. That said, there are aspects of banking sector size that were not considered in this paper but that might have a bearing on financial stability, such as the possibility that the banking system becomes more opaque and interconnected as it grows in size and the link between banking system size and the rest of the financial system.

Moreover, further work is needed to improve our understanding of the drivers of the n-shaped relationship between the ratio of credit to GDP and economic growth and on the quantitative importance of agglomeration externalities in banking. The importance of the resilience, rather than the size, of a banking system for financial stability is more clear-cut. For example, evidence from regressions and case studies suggests that less resilient banking systems are more likely to suffer a financial crisis. This is, in part, why the Bank of England, in conjunction with other organisations including the FSB, is pursuing a wide-ranging agenda to improve the resilience of the banking system. These policy initiatives will also mitigate some of the undesirable reasons why the UK banking system might be so big, for example, by eliminating banks’ TBTF status and implicit subsidy.

The Prudential Regulation Authority (PRA) is today fining Royal Bank of Scotland Plc (RBS), National Westminster Bank Plc (Natwest) and Ulster Bank Ltd (Ulster Bank) £14 million for inadequate systems and controls which led to a serious IT incident in 2012. This is the first financial penalty the PRA has imposed since it came into being in April 2013. The Financial Conduct Authority (FCA) has separately fined the banks for the same incident.

In April 2013, the PRA and FCA announced that they would investigate the RBS, Natwest and Ulster Bank IT incident which led to widespread disruption to customers and the financial system. A joint investigation was considered necessary because the incident impacted upon the objectives of both the PRA and the FCA.

The IT incident, which began on 18 June 2012, directly affected at least 6.5 million customers in the United Kingdom, 92% of whom were retail customers. The IT incident had the potential to have an adverse effect on the safety and soundness of RBS, Natwest and Ulster Bank as it impacted upon:

the ability of the banks’ retail customers to access their accounts;

the ability of the banks’ commercial customers to access their internet banking service, preventing them from accessing their accounts or making payments;

customers of other institutions who were unable to receive payments from the banks’ affected customers; and

the ability of the banks to fully participate in clearing. An efficient clearing system is fundamental to the efficient operation of the financial markets.

Disruption to the majority of RBS and Natwest systems lasted until 26 June 2012, and Ulster Bank systems until 10 July 2012. Disruptions to other systems continued into July 2012. The cause of the IT incident was the failure of the banks to have the proper controls in place to identify and manage exposure to the IT risks within their business.

Properly functioning IT risk management systems and controls are an integral part of a firm’s safety and soundness. The PRA considers that the IT incident could have threatened the safety and soundness of the banks and could have, in extremis, had adverse effects on the stability of the financial system in that it interfered with the provision of the banks’ core banking functions, impacted third parties and risked disrupting the clearing system.

Andrew Bailey, Deputy Governor, Prudential Regulation, Bank of England and CEO of the PRA said:

“The severe disruption experienced by RBS, Natwest and Ulster Bank in June and July 2012 revealed a very poor legacy of IT resilience and inadequate management of IT risks. It is crucial that RBS, Natwest and Ulster Bank fix the underlying problems that have been identified to avoid threatening the safety and soundness of the banks.”

The banks agreed to settle at an early stage and were therefore entitled to a 30% discount, without which they would have been fined £20 million.