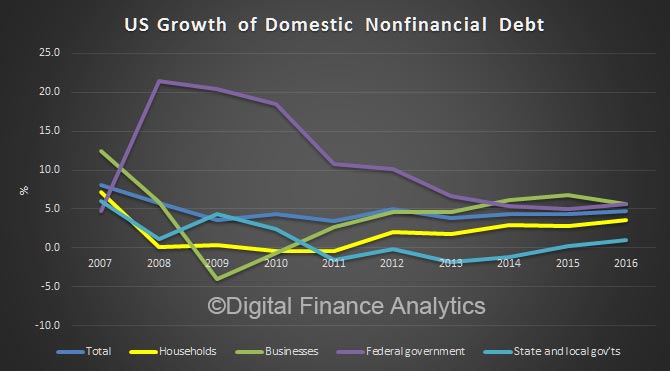

The Fed released the US Accounts to Dec 2016. It shows growth in household debt, but a lowering of business investment and government debt down from the 2008 highs.

Domestic nonfinancial debt outstanding was $47.3 trillion at the end of the fourth quarter of 2016, of which household debt was $14.8 trillion, nonfinancial business debt was $13.5 trillion, and total government

debt was $19.1 trillion.

Domestic nonfinancial debt growth was 2.9 percent at a seasonally adjusted annual rate in the fourth quarter of 2016, down from an annual rate of 5.8 percent in the previous quarter.

Household debt increased at an annual rate of 3.8 percent in the fourth quarter of 2016. Consumer credit grew 6.2 percent, while mortgage debt (excluding charge-offs) grew 3.1 percent at an annual rate. Percentage changes calculated as seasonally adjusted flow divided by previous quarter’s seasonally adjusted level, shown at an annual rate

Nonfinancial business debt rose at an annual rate of 2.6 percent in the fourth quarter, down from an annual rate of 6.3 percent in the previous quarter.

Federal government debt increased 2.9 percent at a seasonally adjusted annual rate in the fourth quarter of 2016, down from an annual growth rate of 8.2 percent in the previous quarter.

State and local government debt rose at an annual rate of 0.2 percent in the fourth quarter of 2016, down from an annual growth rate of 0.7 percent in the previous quarter.

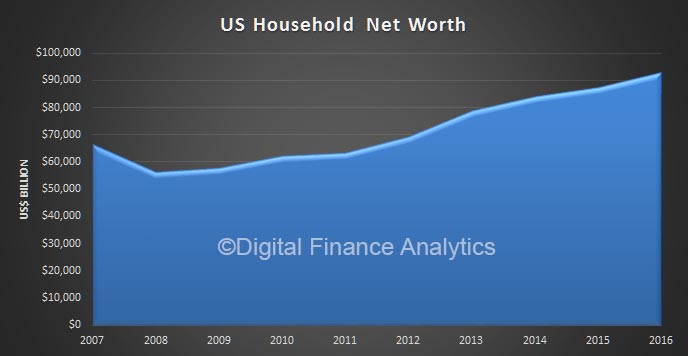

The net worth of households and nonprofits rose to $92.8 trillion during the fourth quarter of 2016. The value of directly and indirectly held corporate equities increased $728 billion and the value of real estate rose

$557 billion.

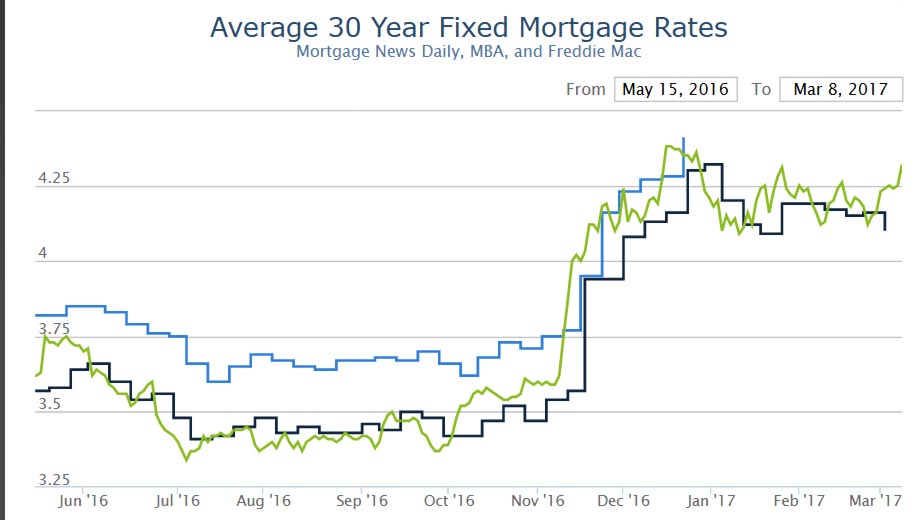

Mortgage ratesspiked, big-time, today. Underlying bond markets had already moved higher in rate overnight, but the trend was taken to a new level by an exceptionally strong employment report from ADP. Although this isn’t the big jobs report (we’ll get that on Friday), many market participants treat the ADP numbers as one of several advance indicators of Friday’s jobs report. Sometimes it doesn’t register a response, but when it beats the forecast by as much as it did today (298k vs 190k), markets can’t help but adjust their trajectory ahead of Friday.

The net effect was the sharpest move higher in rates in several months, slightly outpacing last Wednesday’s rout. Moreover, with the exception of a modest improvement on Monday, rates have moved higher every single day since February 27th. In just over a week, the average conventional 30yr fixed quote is up approximately a quarter of a percent for most lenders. Stronger lenders are offering 4.25% on top tier scenarios while many moved up to 4.375% with today’s weakness.

We think there is growing pressure to lift international capital market rates higher, which will create upward momentum on rates in Australia.

Uncertainty about the scale of penalties for US retail mortgage-backed securities (RMBS) practices more than 10 years ago will continue to weigh on some European banks’ capital management and dividends, Fitch Ratings says. They expect cautious capital retention to be a theme as the 2016 results season for European banks reaches its final stage.

The threat of large, unpredictable settlements hangs over a few European banks that have not settled yet, adding to the pressure on earnings and capitalisation from low interest rates and increased regulation. As a result, we expect banks will continue to prioritise cautious capital management and dividend policies, even though most have strengthened capital positions considerably since the financial crisis.

The US Department of Justice’s (DoJ) investigation into banks’ pre-crisis RMBS business has already cost USD31bn in cash settlements for eight of the global trading and universal banks. The DoJ examined the banks’ pre-crisis practices, including packaging, securitisation, marketing, sale and issuance of RMBS. European banks Deutsche Bank and Credit Suisse are the most recent to settle with the DoJ, agreeing to pay substantial fines of USD3.1bn and USD2.5bn, respectively, and to provide consumer relief.

Investigations into other European banks, notably RBS, Barclays, UBS and HSBC are ongoing. Barclays rejected a settlement in late 2016 and now faces a lawsuit. RBS, unlike other European banks, also still has a pending lawsuit with the US Federal Housing Finance Agency, which we estimate could add about USD3bn (based on an average past settlement rate of 10% of exposure) to any settlement with the DoJ.

Monetary fines have only constituted part of the settlements, and substantial amounts have been agreed in the form of so-called consumer relief, which we believe are proving far less punitive in financial terms. Consumer relief can include loan forgiveness, origination of lower cost loans and financing for affordable housing, targeted at the most vulnerable customers. Deutsche Bank has until 2022 to complete its USD4.1bn required consumer relief, and Credit Suisse until 2021, to complete USD2.8bn.

Pending regulatory and litigation settlements are factored into our analysis as a contingent liability. When a large settlement is reached, we assess the incremental cost in cash terms above provisions already booked and the affordability of the remainder through earnings. When a settlement will absorb at least two quarters’ earnings, we assess its impact on capital and the bank’s plans to remediate the capital effect.

We do not expect the outstanding investigations to lead to significant new restrictions on banks’ businesses or to damage their franchises. Banks have tightened conduct risk controls extensively in the period since the RMBS activity under investigation took place.

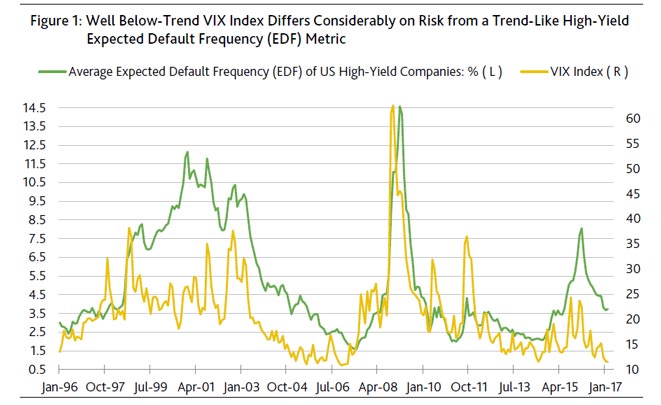

The February 1 FOMC meeting minutes noted two interrelated developments. First, the narrowing by “corporate bond spreads for both investment- and speculative-grade firms” to widths that “were near the bottom of their ranges of the past several years.” Secondly, some FOMC members were struck by how “the low level of implied volatility in equity markets appeared inconsistent with the considerable uncertainty attending the outlook for such policy initiatives.”

Thus, some high-ranking Fed officials sense that market participants are excessively confident in the timely implementation of policy changes that boost after-tax profits. And they may be right, according to Treasury Secretary Steven Mnuchin’s recent comment that corporate tax reform legislation may not be passed until August 2017 at the earliest. The ongoing delay at remedying the Affordable Care Act warns of a possibly even longer wait for corporate tax reform and other fiscal stimulus measures.

Treasury bond yields declined in quick response to the increased likelihood of a longer wait for fiscal stimulus. Lower benchmark yields will lessen the equity market’s negative response to any downwardly revised outlook for after-tax profits. Provided that profits avoid a replay of their year-to-year contraction of the five quarters ended Q2-2016 and that interest rates do not jump, a deeper than -5% drop by the market value of US common stock should be avoided.

The importance of interest rates to a richly priced and supremely confident equity market cannot be overstated. In fact, the rationale for an unduly low VIX index found in the FOMC’s latest minutes contained a glaring error of omission. Inexplicably, no mention was made of how expectations of a mild and thus manageable rise by interest rates have helped to reduce the equity market’s perception of downside risk. An unexpectedly severe firming of Fed policy would doubtless send the VIX index higher in a hurry.

Moreover, the FOMC’s latest minutes failed to comment on the close linkage between the now below-trend spreads of corporate bonds and an exceptionally low VIX index. As inferred from long-term statistical relationships, the VIX index now supports the possibility of corporate bond yield spreads that are much narrower than what is suggested by the default outlook. For the purpose of quantifying the latter, an aggregate version of expected default frequencies will be employed.

VIX Index and high-yield EDF metric differ on risk

Though the calculations of both the VIX index and EDF (expected default frequency) metrics are sensitive to asset price volatility, the messages delivered by each measure of risk can differ significantly. The 0.72 correlation between month-long averages of the VIX index and the aggregate EDF metric of US/Canadian high-yield issuers is statistically significant, but it is also far from perfect. For example, despite their relatively strong positive correlation, the VIX index and the high-yield EDF occasionally move in different directions.

Since the January 1996 inception of the average high-yield EDF metric, the medians during business cycle upturns were 3.7% for the high-yield EDF and 17.9 for the VIX index. Recently, the high-yield EDF nearly matched its median of all recovery months since December 1995, while a VIX index of less than 13 was well under its comparably measured median. In other words, the high-yield EDF metric senses a good deal more financial market risk than the VIX index does.

By way of simple regression analysis, the high-yield EDF metric now predicts an 18.3 midpoint for the VIX index, which is far above a recent reading of 12.2. Conversely, the VIX index predicts a 2.7% midpoint for the high-yield EDF metric that is less than the actual EDF of 3.7%.

The two broad measures of risk also now predict two vastly different midpoints for the US high-yield bond spread. Compared to the high-yield spread’s recent 384 bp, the VIX index predicts a midpoint of 365 bp which is much thinner than the 462 bp predicted by the recent high-yield EDF and the EDF’s three-month trend.

Both cannot be right. Nevertheless, the modest outlook for 2017’s profits from current production suggests that the EDF’s predictions for the VIX index and the high-yield spread may prove to be more accurate than the VIX index’s projections for the high-yield EDF metric and spread. However as noted earlier, the realization of modest profits growth may be sufficient for the purpose of warding off a deep slide by share prices provided that the effective fed funds rate finishes 2017 no higher than 1.13%, while the 10-year Treasury yield’s annual average for 2017 is no greater than 2.6%.

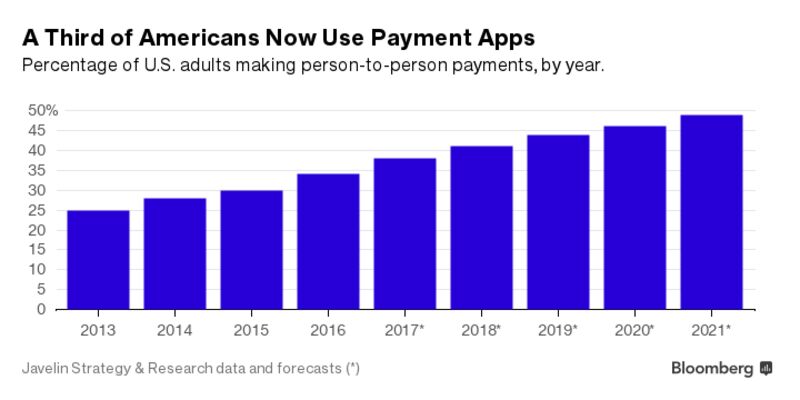

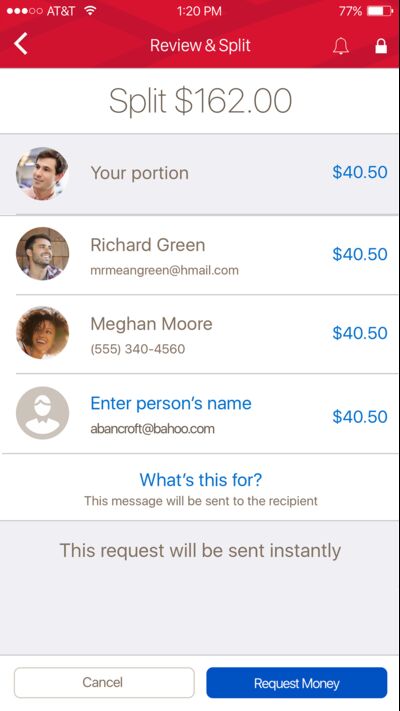

For years, US banks have watched as their youngest customers split restaurant checks, shared utility bills, and pitched in for parties using third-party payment apps such as Venmo.

Now they’re trying to take back the person-to-person payments business by launching an app of their own.

Nineteen banks, including Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo, are teaming up to start Zelle, a website and app that will let users send and request money much as Venmo does. Bank of America says it is the first to incorporate all of Zelle’s capabilities—including the ability to split bills between users—into its own mobile app, starting today. A standalone Zelle payment app should be available to anyone with a debit card, regardless of where he or she banks, by the middle of the year.

Bank of America's upgraded payment app. Source: Bank of America

Zelle has some stiff competition from Venmo and its parent company, PayPal Holdings Inc. Venmo, which started in 2009, processed $17.6 billion in transactions last year, a 135 percent increase from the previous year. In the common vernacular, “to Venmo” means to move money to and from friends and family. That’s a huge advantage, said Michael Moeser, director of payments at Javelin Strategy & Research. When presented with another option, “An avid Venmo user is going to ask, ‘Why do I need something else?'” he said.

Zelle’s not-so-secret weapon is its connection to the big banks where millions of Americans keep their money. Request $40 from a roommate over the Zelle network using BofA’s app, and the money shows up in your account within minutes of when he agrees to send it. On Venmo, that $40 would show up in your Venmo wallet right away, but then it stays there. To get the cash into your hands, you need to log into your Venmo account, cash out your balance, and wait—sometimes days—for the money to show up in your bank account.

Venmo is trying to accelerate that process. PayPal made deals with Mastercard Inc. and Visa Inc. to move money over their debit card networks. By the middle of 2017, it should be possible to cash out a PayPal or Venmo account instantly, according to PayPal Holdings spokesman Josh Criscoe.

Zelle was built by Early Warning, a bank-owned company that also runs the clearXchange payment system. It’s no easy task to build an app that syncs with 19 large banks, four payment processors, and two card networks. Each has its own legacy technology, and many already have person-to-person payment tools, such as Chase’s QuickPay, that are popular with some customers.

To launch the new app without disrupting the old systems, Zelle is being rolled out in phases. In the first, under way now, bank payment apps will incorporate Zelle’s options and basic design without any Zelle branding. Banks can add these features whenever they’re ready. Later, bank apps will tout Zelle branding, and, sometime in the first half of the year, a standalone app will be launched.

BofA’s person-to-person payments will be free. Although members of the Zelle network will have the option to charge, it’s not clear if any banks will even try to do so when Venmo and other payment apps cost nothing.

The lack of an obvious revenue opportunity may be one reason why it has taken so long for banks to launch a serious competitor to Venmo. Moeser summarized the attitude of banks until recently: “Do I really care about two 18-year-olds sending $20 to each other? Maybe not.”

But the people designing Zelle imply their goal is much bigger than just helping college students split a pizza bill.

“This is a great time for us to move [person-to-person payments] from millennials to mainstream,” said Lou Anne Alexander, Early Warning’s group president for payments. The use of mobile banking apps is expanding exponentially, creating many more opportunities for people of all ages to send and request money. “Any place we see checks and cash, that’s our target,” she said.

Because Zelle is sponsored by and connected to their banks, Alexander said users should feel more comfortable using it for larger transactions and for a broader array of uses, from paying a contractor to collecting money for a school dance team. Zelle may also be used for business-to-consumer payments, such as insurance companies paying out claims.

Anything that promotes the use of digital payments is ultimately good for Venmo, said PayPal’s Criscoe. “The common enemy is cash.”

Zelle and Venmo have a lot in common with one major exception. Venmo is also a social app, where users can and do choose to make their transactions, along with any associated emoji-filled messages, public. Criscoe said the average user checks Venmo two to three times a week just to see what his or her friends are up to.

Zelle users won’t have the option to spy on their friends’ payment activity. The idea was tested on consumers but fell flat with Zelle’s intended audience, Alexander said. “While appealing to some ages, it’s not really appealing to all.”

According to the US Bureau of Labor Statistics, real (adjusted for inflation) average hourly earnings were unchanged from January 2016 to January 2017. Before adjusting for inflation, average hourly earnings increased 2.5 percent over the 12 months ending in January 2017. Over the same period, the Consumer Price Index for all Urban Consumers (CPI-U), which is used to adjust average hourly earnings for inflation, also increased 2.5 percent.

Since 2009, the 12-month change in average hourly earnings ranged from 1.5 percent (in October 2012) to 3.6 percent (in December 2008 and January 2009). Over the same period, the 12-month change in the CPI-U ranged from −2.0 percent (in July 2009) to 5.5 percent (in July 2008). The 12-month change in real hourly earnings ranged from −2.4 (in July 2008) percent to 4.8 percent (in July 2009).

The 12-month changes in average hourly earnings and the CPI-U were equal in April, May, and June 2014. From that time until December 2016, the change in hourly earnings was greater than the change in the CPI-U, resulting in positive changes in real average hourly earnings.

These data are from the Current Employment Statistics program and are seasonally adjusted. Data for the most recent 2 months are preliminary.

One of the outcomes of the 2008 financial crisis was recognizing the cascading effects that the severe financial stress or failure of a large institution can have on financial markets and the economy at large. A primary goal, therefore, of post-crisis financial reform was heightened supervision and regulation of those institutions whose sheer size or risk-taking posed the greatest threat to financial stability.

These reforms were primarily codified in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. Under the Dodd-Frank Act, US financial institutions with $50 billion or more in assets are subject to enhanced prudential regulatory standards. These standards are designed to accomplish two primary objectives:

Improve an institution’s resiliency to both decrease its probability of failure and increase its ability to carry out the core functions of banking

Reduce the effects of a bank’s failure or material weakness on the financial system and the economy at large

To meet these objectives, the Federal Reserve employs a number of tools to monitor institutions and reduce the risks they pose to the U.S. financial system.

Capital Stress Testing

The Fed annually assesses all bank holding companies with more than $50 billion in assets to ensure they have sufficient capital to weather economic and financial stress. This exercise, called the Comprehensive Capital Analysis and Review (CCAR), also allows the Fed to look at the impact of various financial scenarios across firms.

If the Fed determines that an institution cannot maintain minimum regulatory capital ratios under two sets of adverse economic scenarios, the institution may not make any capital distributions such as dividend payments and stock repurchases without permission.

A complementary exercise to CCAR is Dodd-Frank Act stress testing (DFAST). The DFAST exercise is conducted by the financial firm and reviewed by the Fed. It aids the Fed in assessing whether institutions have sufficient capital to absorb losses and support operations during adverse economic scenarios. This forecasting exercise applies to banks and bank holding companies with more than $10 billion in consolidated assets.

Liquidity Stress Testing

The financial crisis made it clear that a firm’s liquidity, or ability to convert assets to cash, is important during periods of financial stress. In response, the Fed launched the Comprehensive Liquidity Assessment and Review (CLAR) in 2012 for the country’s largest financial firms.

CLAR allows the Fed to assess the adequacy of the liquidity positions of the firms relative to their unique risks and to test the reliability of these firms’ approaches to managing liquidity risk.

Resolution and Recovery Plans

Banking organizations with total consolidated assets of $50 billion or more are also required to submit resolution plans to the Fed and the Federal Deposit Insurance Corp. Each plan must describe the organization’s strategy for rapid and orderly resolution in the event of material financial distress or failure.

Have these tools made a difference? The answer is clearly “yes,” as shown in the figure below.

The capital ratios of the country’s largest firms (those with more than $250 billion in assets) have shown solid positive progress. In fact, one important measure of capital strength for this group of institutions, the average Tier 1 risk-based capital ratio, has increased 48.1 percent since 2007.

Some in the industry and in Washington, D.C., are calling for a re-evaluation of the Dodd-Frank Act provisions. While modifications for smaller, non-systemic firms would be welcomed by many, the damage from the financial crisis makes it sensible to continue strong expectations for the largest firms.

In a move that generated widespread concern last week, President Donald Trump signed an executive order that aims to repeal the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act. Even Dodd-Frank’s strongest supporters acknowledge that parts of the law could be tweaked to remove excessive financial regulation and made simpler. But they worry that in the process of such reforms, much of what is good in Dodd-Frank will be undone.

The Trump administration’s vehicle to repeal Dodd-Frank is the Financial Choice Act, a failed 2016 bill being reintroduced by Republican Congressman Jeb Hensarling, who is chairman of the House Financial Services Committee. The bill gets its new traction from Trump’s presidential order, signed on February 3, which lists seven so-called “Core Principles” to regulate the U.S. financial system. The order directs the treasury secretary to consult with the heads of the member agencies of the Financial Stability Oversight Council and report within 120 days if existing laws and regulations support those principles.

According to Michael Barr, University of Michigan Law School professor and a key architect of the Dodd-Frank Act, the Choice Act would imperil the interests of the middle class, retirees and investors. “It just seems like a recipe for a huge disaster,” he said. “[Dodd-Frank] put in place real guardrails against re-creating the kind of financial crisis we saw in 2008. It is inexcusable that the administration has targeted the most vulnerable people in our society to be the ones that bear the brunt of their ideological push.”

Wharton professor of legal studies and business ethics Peter Conti-Brown does not expect an easy passage for the Choice Act. He said he is intrigued by the game plan of the administration in its pushback against Dodd-Frank. Describing the Republicans in Congress as “a coalition that includes rightwing Rust Belt populism that is hostile to international trade, for example,” he noted that they “should similarly be profoundly skeptical” of most provisions of the Choice Act. “It would be very hard to sell to those who voted for radical change … and call for an end to protections for average workers, consumers and investors.”

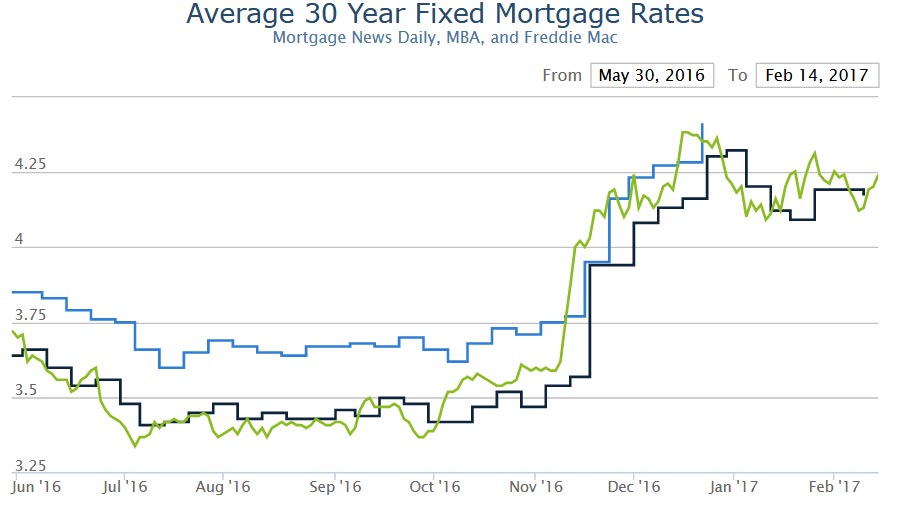

US Mortgage rates moved higher for the 4th straight day today, following Fed Chair Janet Yellen’s congressional testimony. It wasn’t that Yellen’s speech or Q&A contained any major surprises. Rather, bond markets (which dictate rates) were simply looking for some indication of “sooner vs later” with respect to the Fed’s next rate hike. Her comments were generally more in line with “sooner.” Bond markets responded by quickly trading rates to higher levels, resulting in multiple “negative reprices” for mortgage lenders this morning.

Bonds calmed down in the afternoon, and ended up clawing back roughly half of the morning’s losses by the end of the day. Many lenders were consequently able to offer “positive reprices”–bringing rate sheets part of the way back to yesterday’s levels.

Despite the afternoon improvements, essentially every lender is in worse shape today vs yesterday. The average top tier conventional 30yr fixed quote is back up to 4.25%–a move that was already in-progress yesterday. Today’s rates are the highest since February 3rd.

Deregulation is likely to be a significant theme for US financial institutions (FIs), with the Trump administration and Republican leaders in Congress indicating broad support to limit and simplify the regulatory regime, says Fitch Ratings. Fitch does not believe that the Dodd-Frank Act will be repealed in full; however, select provisions are potentially subject to substantial revision.

Determining the aggregate ratings or credit impact of a major deregulation initiative without specific policy proposals would be premature. It remains unclear which, if any, deregulation policies will be the focus of the administration and ultimately be passed.

However, Fitch believes that the Financial Choice Act (FCA), proposed by House Financial Service Committee Chairman Representative Jeb Hensarling, R-TX, in 2016, may serve as a blueprint for some of the changes ahead. The FCA is broad in scope and includes proposals to change FI activities, modify and potentially reduce financial regulators’ authority, limit regulatory burdens for certain FIs, add greater congressional oversight of regulators and propose reform to market infrastructure.

In determining the potential impact of such regulatory changes, both the direct impact of the change and the responses from individual banks will be key in determining the ultimate issuer credit effect. The extent to which the reforms could lead to a reduction or changes to the quality of capital and/or liquidity, or weaken governance, will be particularly important for ratings over time.

Several parts of the FCA target regulatory relief for strongly capitalized and well-managed banks, such as a proposal to exempt banks from many regulations should they exceed a 10% or higher financial leverage ratio. Smaller banks meeting the requirements would most likely benefit. For large global systemically important banks, Fitch estimates that the $400 billion in incremental Tier I capital necessary to achieve the minimum leverage ratio – the calculation would likely be similar to the Basel III supplementary leverage ratio – would outweigh any potential cost benefits of regulatory relief.

Limiting regulatory authority is another key plank of the FCA. The most significant change for the markets would be the proposed restructuring of the Federal Reserve, including how it sets interest rates, as well as its authority as a central bank. The proposed rule also calls for restructuring the Consumer Financial Protection Bureau (CFPB), adding congressional review of financial agency rulemaking and subjecting agencies’ rulemaking to judicial review, among others.

Overall, Fitch believes that such reviews could hamper agencies’ effectiveness and significantly impede their ability to issue new rules, which could have an overall negative effect on the system. Fitch believes that restructuring the CFPB with a Consumer Financial Opportunity Commission, as stipulated in the FCA, would lower compliance costs and reduce potential fines for consumer finance, but lead to weakening control frameworks.

Nonfinancial business debt rose at an annual rate of 2.6 percent in the fourth quarter, down from an annual rate of 6.3 percent in the previous quarter.

Nonfinancial business debt rose at an annual rate of 2.6 percent in the fourth quarter, down from an annual rate of 6.3 percent in the previous quarter.