Anyone who’s dug into the 2008 financial crisis knows the role that bundling and selling subprime housing loans played in bringing the world to the brink of economic collapse – out-of-control behaviors well-depicted in the movie “The Big Short.”

But one thing I hope “The Big Short” doesn’t do is further tarnish the image of subprime lending.

Despite their poor reputation, such loans remain a key tool in easing the housing affordability crisis and expanding the availability of mortgages to low-income Americans seeking to realize the dream of homeownership. They also can help policymakers cope with the growing ranks of the homeless.

I’ve been studying the world of subprime in recent years, and these are some of the lessons from my current and past research. First, we need to fix the subprime mortgage market, so that the ways in which it contributed to the financial crisis aren’t repeated.

Shocking levels of homelessness

Los Angeles, New York and other cities in America are struggling to cope with the problem of homelessness and the lack of affordable housing.

On a single night in January 2015, more than 560,000 people nationwide were homeless – meaning they slept outside, in an emergency shelter or in a transitional housing program. Almost a quarter were children. Meanwhile, homeownership is hovering at 20-year lows, while about half of renters struggle to pay their landlords.

Last fall, Los Angeles Mayor Eric Carcetti asked the City Council to declare “a state of emergency” on homelessness and committed US$100 million to solving the problem, suggesting that subsidies would play a role.

But a focus on rental subsidies to solve homelessness and other affordable housing issues has adverse consequences, as evidenced by New York’s experience.

Its cluster-site housing program, in which privately owned apartment buildings are used to house homeless families when the city’s shelters are full, relies on such subsidies. But because the city typically pays market rents (or more), many landlords responded by pushing out regular (and low-income) tenants in favor of this steady stream from the government.

Such programs reduce the overall supply of affordable units, crowding out other groups in need. As more affordable housing units are allotted to the homeless, there are fewer available for low-income residents who don’t qualify for those programs and are at risk of becoming homeless themselves.

Fortunately, Mayor Bill de Blasio aims to phase out the costly program over the next three years.

While there are many other approaches to tackling homelessness, they rely on addressing an important underlying problem: the housing affordability crisis. It may seem improbable, but subprime lending could help ease the housing affordability crisis.

The role of subprime lending

The relationship between homelessness and the strains in the housing rental market is well-known: when there are more rental vacancies available, homelessness decreases (I survey the academic findings on the topic here).

This suggests that if we reduce home affordability problems, we can effectively reduce homelessness.

A powerful tool to help ease the housing affordability crisis is subprime mortgage lending – defined as loans made to borrowers with credit scores below 640.

The idea is simple: by helping more low-income tenants qualified to take out a subprime mortgage become homeowners, there’ll be more affordable rental housing available for everyone else. More supply on the market helps reduce average rents, which in turns helps more of those pushed to the streets afford a roof over their heads with less government aid. Thus this makes the policies still based on rental subsidies more effective.

However, this idea cannot be implemented until we fix the subprime mortgage market. As you can see from the graph below, the market has not yet recovered from its collapse in 2008.

The subprime market has yet to recover from its collapse.Inside Mortgage Finance, Author provided

One of the reasons the market collapsed was that investors lost confidence in the ability of loan originators and regulators to use credit scoring models to accurately assess a borrower’s creditworthiness – remember the NINJA loans (no income, no job, no assets)?

This market won’t be back up and running at full strength – and able to help address the affordability crisis – until these credit-scoring models improve and mechanisms are put in place to ensure loan quality remains adequate.

The FHFA sets new goals

There has been some movement to get the subprime market moving again.

The Federal Housing Finance Agency (FHFA), an independent federal agency that regulates Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks, recently set goals for the next two years meant to expand the availability of mortgages to low-income buyers.

This policy will keep its focus on helping a small segment of borrowers with incomes no greater than 50 percent of their area’s median income to purchase or refinance a single-family home.

But many affordable housing advocates expressed concern that these targets do not go far enough. The Woodstock Institute – a leading research and policy nonprofit organization focused on fair lending, wealth creation and financial systems reform – for example, argued that the policy won’t do enough to promote affordable and sustainable home ownership for low-income families.

How to bring back subprime

Even with the FHFA embracing the idea of expanding the availability of subprime mortgages to low-income buyers, their perceived role in the 2008 crisis and bringing down the housing market may cause justifiable resistance from the general public as a means of tackling the affordability crisis.

And one cannot blame this reaction, as it was the average American taxpayer who bailed out the reckless financial system, brought down by greedy bankers and weak politicians and regulators.

So how we can encourage more subprime lending while avoiding a repeat of 2008? In my recent research, I suggest a few ways to do this.

One of the reasons subprime loans became such a problem in the run-up to the crisis is just the sheer volume (see the boom in subprime lending from 2001 to 2005 in the above graph). This expansion was fueled by the generous homeownership subsidies given to low-income households.

One way to help prevent this is to vary the size of the homeownership subsidy countercyclically to control the amount of credit flowing into the economy and prevent overborrowing during expansionary periods. It would be higher at times when the housing market contracts, and lower when it’s booming.

Another problem was that lenders had an incentive to originate mortgages to borrowers who couldn’t afford them because all the risk was passed along to banks and other investors through collateralized mortgage obligations (CMO) and other sophisticated financial instruments.

The Federal Reserve in conjunction with other regulators could reduce this risk by carefully monitoring how many mortgages lenders keep in their own portfolios. When the share lenders hold increases, they have more incentives to better screen borrowers and thus originate better mortgages.

Lastly, the so-called adverse selection problem on the part of the mortgage originator in the secondary market should also be taken into account. This problem occurs when the mortgage originator has more information about the quality of mortgages that are securitized than the secondary market investors who snap up the CMO. That allows the originator to keep the low-risk mortgages in its own portfolio while distributing the high-risk mortgages to investors.

Improving existing credit scoring models is crucial to ameliorating this problem. Also, the Fed should more carefully monitor the quality of mortgages that are sold to investors and share its information with them. At the very least, that would reduce the investors’ information disadvantage with respect to originators.

Accompanied by the right means to regulate the housing market, we can support subprime while avoiding the disastrous outcomes highlighted in “The Big Short.“ And we can create an environment in which making low-cost mortgages available to people helps resolve the problem of unaffordable housing and homelessness.

Author: Jaime Luque, Assistant Professor, Real Estate & Urban Land Economics, University of Wisconsin-Madison

Governor Lael Brainard, spoke at the 2016 U.S. Monetary Policy Forum, New York, New York. The speech highlighted that whilst there was a phase when different economic centres were diverging, now there are more common elements, including low growth, low interest rates and low inflation. Global shocks are being transmitted via the financial system, creating volatility and spillover effects.

To the extent that we are observing limited divergence in inflation outcomes and less divergence in realized policy paths than many anticipated, this could be attributable to common shocks or trends that cause economic conditions to be synchronized across economies. The sharp repeated declines in the price of oil have been a major common factor depressing headline inflation and are also likely feeding into low core inflation, although to a lesser extent. As noted previously, these price declines have led headline inflation across the globe to behave quite similarly over this time period. Even so, most observers expect this source of convergence in inflationary outcomes to eventually fade and thereafter not affect monetary policy paths over the medium term.

In contrast, a more persistent source of convergence may be found in an apparent decline in the neutral rate of interest. The neutral rate of interest–or the rate of interest consistent with the economy remaining at its potential rate of output and inflation remaining at target level–appears to have declined over the past 30 years in the United States and is now at historically low levels. Similarly, longer-run interest rates appear also to have fallen across a broad group of advanced and emerging market economies, suggesting that neutral rates are at historically low levels in many countries around the world and near or below zero in the major advanced foreign economies. Although the reasons for the declines in neutral rates are not perfectly understood and may differ across countries, there are some common drivers, such as slower productivity and labor force growth and a heightened sensitivity to risk.

The very low levels of the shorter run neutral rate reflect in part headwinds from the crisis that are likely to dissipate over time. However, if many of the common forces holding down neutral rates prove persistent, then neutral rates may remain low through the medium term, implying a shallower path for policy trajectories.

The global economy is also experiencing a downshift in emerging market growth momentum led by China, which may prove somewhat persistent. Whereas earlier in the recovery there was a striking divergence between the relatively buoyant growth in major emerging economies and depressed growth in advanced economies, lately the extent of divergence has diminished noticeably. China is undergoing a challenging set of economic transitions. Trend growth has slowed substantially and is expected to slow further, and the composition of growth is shifting away from resource-intensive manufacturing and exports toward a greater share for consumption and services. China’s investment has slowed sharply recently after accounting for nearly one-third of global investment over the past three years and about one-half of global consumption in certain metals such as iron ore, aluminum, copper, and nickel. Commodity exporters and close trading partners in Asia will be most affected, but the changes in the composition and rate of growth in a country that has accounted for about one-third of the growth in world output and trade will likely ripple through the global economy much more generally.

Amplified Spillovers

Of course, policy divergence among major economies could be limited by rapid and strong transmission of foreign shocks across borders. In particular, although the U.S. real economy has traditionally been seen as more insulated from foreign trade shocks than many smaller economies, the combination of the highly global role of the dollar and U.S. financial markets and the proximity to the zero lower bound may be amplifying spillovers from foreign financial conditions. By one rough estimate, accounting for the net effect of exchange rate appreciation and changes in equity valuations and long term yields, over the past year and a half, the United States has experienced a tightening of financial conditions that is the equivalent of an additional increase of over 75 basis points in the federal funds rate.10

The transmission of divergent economic conditions across borders typically occurs though a couple of different channels. First, a decline in demand in one country reduces its demand for imports from other countries. Second, the fall in economic activity would be expected to trigger a more accommodative monetary policy, which helps offset the effect of the shock by both supporting domestic demand and weakening the exchange rate. The weaker exchange rate in turn leads domestic consumers to switch their expenditures away from more expensive foreign imports to cheaper domestic products while increasing the competitiveness of exports. The extent to which monetary policy offsets the shock by dispersing it to trade partners as opposed to strengthening domestic demand depends on the responsiveness of domestic demand relative to the exchange rate. The exchange rate channel, by raising the price of imports in domestic currency, also pushes up domestic inflation and exerts downward pressure on foreign inflation.

The strength of spillovers across countries and the extent to which that affects policy divergence across countries depend on a foreign economy’s openness to these different channels. The recent experience of Sweden suggests that for highly open economies, the effect of foreign shocks can be extremely powerful. Sweden’s economic growth has been relatively rapid recently, reaching nearly 4 percent over the most recent four quarters. Moreover, the employment gap is estimated to be nearly closed, and there are signs of financial excess in the housing market. In ordinary times, these conditions would be consistent with relatively tight monetary policy. However, inflation has run persistently well below the central bank’s 2 percent inflation target. Given the relative openness of Sweden’s economy, moving the inflation rate back up to target has been greatly complicated by the sensitivity of Sweden’s exchange rate and financial conditions to developments in the euro area, where domestic economic conditions are consistent with much more accommodative policy. As a result, the Riksbank has been pursuing extremely accommodative monetary policy, most recently lowering the interest rate on deposits to minus 0.5 percent and authorizing the Governor and Deputy Governor to intervene in foreign currency markets.

Even in the much larger United States economy, with imports accounting for a little over 15 percent of gross domestic product (GDP), spillovers can be quite strong, in part reflecting the international role of U.S. financial markets and the dollar. Since the middle of 2014, with a reassessment of demand growth in the euro area and subsequently in emerging markets and other commodity exporters, the real trade-weighted value of the dollar has increased nearly 20 percent. As a result, in 2014 and 2015, net exports subtracted a little over 1/2 percentage point from GDP growth each year, and econometric models point to a subtraction of a further 1 percentage point this year.12 In addition, the dollar’s appreciation is estimated to have put significant downward pressure on inflation: Non-oil import prices fell 3-1/2 percent in 2015, subtracting an estimated 1/2 percentage point from core PCE inflation.

Financial channels can powerfully propagate negative shocks in one market by catalyzing a broader reassessment of risks and increases in risk spreads across many financial markets. Since the beginning of the year, U.S. financial markets have reacted strongly to adverse news on emerging market growth, even though the news on the U.S. labor market has remained positive. In this regard, although China’s direct imports from the United States are modest, uncertainty about changes to its exchange rate system and financial imbalances, together with changes in the composition of its growth, have had broader global spillovers that may pose risks to the U.S. outlook.

Recent events suggest the transmission of foreign shocks can take place extremely quickly such that financial markets anticipate and indeed may thereby front-run the expected monetary policy reactions to these developments. It also appears that the exchange rate channel may have played a particularly important role recently in transmitting economic and financial developments across national borders. Indeed, recent research suggests that financial transmission is likely to be amplified in economies with near-zero interest rates, such that anticipated monetary policy adjustments in one economy may contribute more to a shifting of demand across borders than a boost to overall demand. This finding could explain why the sensitivity of exchange rate movements to economic news and to changes in foreign monetary policy appear to have been relatively elevated recently.

Financial tightening associated with cross-border spillovers may be limiting the extent to which U.S. policy diverges from major economies. As policy adjusts to the evolution of the data, the combination of heightened spillovers from weaker foreign economies, along with a lower neutral rate, could result in a lower policy path in the United States relative to what many had predicted.

Policy

In circumstances where many economies face common negative shocks or where negative shocks in one country are quickly transmitted across borders, it is natural to consider whether coordination can improve outcomes. Under certain conditions–such as flexible exchange rates, deep and well-regulated financial markets, and flexible product and labor markets–policies designed for the domestic economy can readily offset any spillovers from economic conditions abroad, and policies designed to address domestic conditions can achieve desirable outcomes both within the national economy and more broadly.

In some circumstances, however, cooperation can be quite helpful. If, for example, economies face a common challenge, coordination can communicate to markets that policymakers recognize the challenge and will work to address it. Reducing uncertainty about the direction of policy and addressing concerns about policies working at cross-purposes can boost the confidence of businesses and households. With intensified transmission effects in the vicinity of the zero lower bound, there is a risk that uncoordinated policy on its own could have the effect of shifting demand across borders rather than addressing the underlying weakness in global demand. The difficult start to the year should be a prompt for greater policy coherence and clarity. This might be a good time for policymakers to reaffirm their commitment to work toward the common goal of strengthening global demand.

Similarly, with anemic global demand and interest rates near zero, in some economies there is scope for monetary policy to be more effective with fiscal policy working in the same direction. With potential growth and nominal borrowing rates both low, public investment that increases potential in the longer run and demand in the shorter run could make an important contribution. A joint determination by policymakers across major economies to better deploy policy tools to provide support for global demand could be beneficial.

Research from the USA highlights the fact that when house prices fall, and household debt is high, the rise in defaults is more correlated to the number of households falling behind in their mortgage payments that the debts of those already in default.

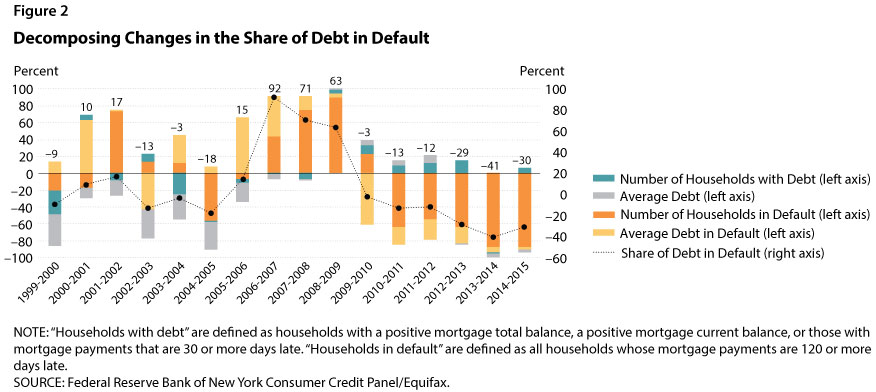

The large decrease in US house prices between 2006 and 2011 led to a dramatic increase in mortgage debt defaults. Since then, the share of mortgage debt in default has decreased significantly and is now close to the pre-2006 level. In this essay, we argue that these fluctuations are predominantly the consequence of changes in the number of households falling behind in their mortgage payments (the extensive margin) and not changes in the amount of debt of those in default (the intensive margin). On average, the extensive margin accounts for 78 percent of the increase in the 2006-09 period and 93 percent of the decrease in the 2011-15 period. This information may be useful in designing prudential policies to mitigate mortgage default.

The analysis is performed using data from the Federal Reserve Bank of New York Consumer Credit Panel/Equifax. In our measure of default, we consider all households with mortgage payments 120 or more days late. Figure 1 shows the share of mortgage debt in default, which fluctuated between 0.7 percent and 1 percent in the 1999-2006 period and then jumped to 7.5 percent in 2009. The figure also shows the evolution of house prices, whose collapse coincided with increasing mortgage defaults. In a recent article, Hatchondo, Martinez, and Sánchez (2015) show how these two series are related: A rapid decrease in house prices causes a sharp increase in mortgage defaults because more households find themselves with negative home equity (“under water”), and some of these households find it beneficial to default after a negative shock to income (i.e., unemployment).

We decompose the changes in the share of debt in default into changes in four different components: average debt in default, number of households in default, average debt, and number of households with debt. Basically, since

we can compute the percentage change (%∆) in the share of debt in default as follows:

Figure 2 shows the results of the decomposition by year; the four colors in each column represent the changes in the four components. The percentage value (shown on the left vertical axis) illustrates the change in the share of debt in default generated by the changes in a particular component. According to the previous equations, the summation of changes in the four components equals the changes in the share of debt in default (represented by the values for the black dots as shown on the right axis). For example, the black dot for 2006-07 has a value of 92, which indicates that the share of debt in default increased by 92 percent in that time period.

There are three interesting findings. First, and most importantly, we find that fluctuations in the number of households in default accounted for most of the fluctuations in the share of debt in default (shown by the size of the orange part of the bars in Figure 2). The share of households in default was very large not only for the years when defaults were increasing (2006 to 2009), but also for the subsequent years when the share of debt in default decreased slowly but steadily. The changes in the number of households in default confirm our earlier claim that the drastic decline in house prices between 2006 and 2009 caused negative home equity for more households. For some of these households a negative income shock triggered default, thus leading to the sharp increase in mortgage debt default. Another reason for this pattern is the delay in foreclosure proceedings that started during the Great Recession. Chan et al. (2015) show that borrowers’ knowledge of a possible long delay between the formal notice of foreclosure and the actual foreclosure sale date affects the likelihood of default: Borrowers who anticipate a longer period of “free rent” have a greater incentive to default on their mortgages.

Second, our results indicate that from 2003 to 2007 the average amount of debt (the gray part of the bars in Figure 2) exerted downward pressure on the share of debt in default. That is, since the average amount of debt was increasing, if the other three components had not increased, the share of debt in default would have decreased.

Finally, we find that the average amount of debt in default (the yellow part of the bars in Figure 2) was important in the 2006-08 period. This finding indicates that part of the increase in the share of debt in default during that period was actually due to an increase in the amount of the debt of households in default. This increase is in line with the fact that the decline in house prices affected households with larger debt (not necessarily subprime loans) that were not falling into default before 2006. When house prices plummeted in 2006, more households from this group defaulted. Later in the recession, the importance of the average amount of debt was overtaken by the number of households in default as more and more households with similar characteristics chose to default.

To summarize, the rapid increases in mortgage debt in default between 2006 and 2011 captured the attention of the public, policymakers, and researchers. It is important to understand the main forces driving the default increase, especially in designing prudential policies that minimize mortgage default such as those analyzed by Hatchondo, Martinez, and Sánchez (2015). The decomposition exercise in this essay suggests that the evolution of the share of mortgage debt in default can be accounted for mostly by changes in the number of households in default rather than changes in the overall amount of mortgage debt and the number of households with mortgages. Changes in the amount of debt in default also played a nonnegligible role, especially during the pre-crisis to early crisis periods.

The Federal Reserve Board on Friday announced a $131 million penalty against HSBC North America Holdings, Inc. and HSBC Finance Corporation for deficiencies in residential mortgage loan servicing and foreclosure processing. The penalty is being assessed in conjunction with an agreement involving similar deficiencies that HSBC announced Friday with the U.S. Department of Justice, other federal agencies, and the state attorneys general.

The penalty assessed by the Board is the maximum amount allowed under the law, taking into account the circumstances of HSBC’s unsafe and unsound practices and foreclosure activities. The penalty may be satisfied by providing borrower assistance or remediation in conjunction with the Department of Justice settlement, or by providing funding for nonprofit housing counseling organizations. If HSBC does not satisfy the full penalty amount within two years, the remaining amount must be paid to the U.S. Department of Treasury. The Board will closely monitor compliance by HSBC with the requirements of the order.

The terms of the monetary assessment against HSBC are similar to those that were part of the penalties issued by the Board in February 2012 and July 2014 against six other mortgage servicing organizations that reached similar agreements with the U.S. Department of Justice and the state attorneys general.

The Board previously issued an enforcement action in April 2011 requiring HSBC to correct its servicing and foreclosure-related deficiencies. That action was among 14 corrective actions issued against Board-supervised mortgage servicers or their parent holding companies for unsafe and unsound practices in residential mortgage loan servicing and foreclosure processing.

Information received since the Federal Open Market Committee met in December suggests that labor market conditions improved further even as economic growth slowed late last year. Household spending and business fixed investment have been increasing at moderate rates in recent months, and the housing sector has improved further; however, net exports have been soft and inventory investment slowed. A range of recent labor market indicators, including strong job gains, points to some additional decline in underutilization of labor resources. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation declined further; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen. Inflation is expected to remain low in the near term, in part because of the further declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.

Given the economic outlook, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The minutes of the December 2015 Federal Open Market Committee have been published, and outlines the discussions which underpinned the decision to lift the US federal funds rate. Here is an extract:

Regarding the medium-term outlook, inflation was projected to increase gradually as energy prices and prices of non-energy imports stabilized and the labor market strengthened. Overall, taking into account economic developments and the outlook for economic activity and the labor market, the Committee was now reasonably confident in its expectation that inflation would rise, over the medium term, to its 2 percent objective. However, for some members, the risks attending their inflation forecasts remained considerable. Among those risks was the possibility that additional downward shocks to prices of oil and other commodities or a sustained rise in the exchange value of the dollar could delay or diminish the expected upturn in inflation. A couple also worried that a further strengthening of the labor market might not prove sufficient to offset the downward pressures from global disinflationary forces. And several expressed unease with indications that inflation expectations may have moved down slightly. In view of these risks and the shortfall of inflation from 2 percent, members expressed their intention to carefully monitor actual and expected progress toward the Committee’s inflation goal.

After assessing the outlook for economic activity, the labor market, and inflation and weighing the uncertainties associated with the outlook, members agreed to raise the target range for the federal funds rate to ¼ to ½ percent at this meeting. A number of members commented that it was appropriate to begin policy normalization in response to the substantial progress in the labor market toward achieving the Committee’s objective of maximum employment and their reasonable confidence that inflation would move to 2 percent over the medium term. Members agreed that the post meeting statement should report that the Committee’s decision reflected both the economic outlook and the time it takes for policy actions to affect future economic outcomes. If the Committee waited to begin removing accommodation until it was closer to achieving its dual-mandate objectives, it might need to tighten policy abruptly, which could risk disrupting economic activity. Members observed that after this initial increase in the federal funds rate, the stance of monetary policy would remain accommodative.

However, some members said that their decision to raise the target range was a close call, particularly given the uncertainty about inflation dynamics, and emphasized the need to monitor the progress of inflation closely.

Members also discussed their expectations for the size and timing of adjustments in the target range for the federal funds rate going forward. Based on their current forecasts for economic activity, the labor market, and inflation, as well as their expectation that the neutral shortterm real interest rate will rise slowly over the next few years, members expected economic conditions would evolve in a manner that would warrant only gradual increases in the federal funds rate. However, they also recognized that the appropriate path for the federal funds rate would depend on the economic outlook as informed by incoming data. Members stressed the potential need to accelerate or slow the pace of normalization as the economic outlook evolved. In the current situation, because of their significant concern about still-low readings on actual inflation and the uncertainty and risks present in the inflation outlook, they agreed to indicate that the Committee would carefully monitor actual and expected progress toward its inflation goal. In determining the size and timing of further adjustments to monetary policy, some members emphasized the importance of confirming that inflation would rise as projected and of maintaining the credibility of the Committee’s inflation objective. Based on their current economic outlook, they continued to anticipate that the federal funds rate was likely to remain, for some time, below levels that the

Committee expected to prevail in the longer run.

The Committee also maintained its policy of reinvesting principal payments from agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. In view of members’ outlook for moderate growth in economic activity, inflation moving toward its target only gradually, and the asymmetric risks posed by the continued proximity of short-term interest rates to their effective lower bound, the Committee anticipated retaining this policy until normalization of the level of the federal funds rate was well under way. This policy, by keeping the Committee’s holdings of longer term securities at sizable levels, should help maintain accommodative

financial conditions.

Fed Vice Chairman Stanley Fischer spoke about three related issues associated with the zero lower bound (ZLB) on nominal interest rates and the nexus between monetary policy and financial stability: first, whether we are moving toward a permanently lower long-run equilibrium real interest rate; second, what steps can be taken to mitigate the constraints imposed by the ZLB on the short-term interest rate; and, third, whether and how central banks should incorporate financial stability considerations in the conduct of monetary policy. The experience of the past several years in the United States and many other countries has taught us that conducting monetary policy effectively at the ZLB is challenging, to say the least. And while unconventional policy tools such as forward guidance and asset purchases have been extremely helpful, there are many uncertainties associated with the use of such tools.

Are We Moving Toward a World With a Permanently Lower Long-Run Equilibrium Real Interest Rate?

We start with a key question of the day: Are we moving toward a world with a permanently lower long-run equilibrium real interest rate? The equilibrium real interest rate–more conveniently known as r*–is the level of the short-term real rate that is consistent with full utilization of resources. It is often measured as the hypothetical real rate that would prevail in the long-run once all of the shocks affecting the economy die down. In terms of the Federal Reserve’s approach to monetary policy, it is the real interest rate at which the economy would settle at full employment and with inflation at 2 percent–provided the economy is not at the ZLB.

Recent interest in estimates of r* has been strengthened by the secular stagnation hypothesis, forcefully put forward by Larry Summers in a number of papers, in which the value of r* plays a central role. Research that was motivated in part by attempts that began some time ago to specify the constant term in standard versions of the Taylor rule has shown a declining trend in estimates of r*. That finding has become more firmly established since the start of the Great Recession and the global financial crisis.

A variety of models and statistical approaches suggest that the current level of short-run r* may be close to zero. Moreover, the level of short-run r* seems likely to rise only gradually to a longer-run level that is still quite low by historical standards. For example, the median long-run real federal funds rate reported in the Federal Reserve’s Summary of Economic Projections prepared in connection with the December 2015 meeting of the Federal Open Market Committee has been revised down about 1/2 percentage point over the past three years to a level of 1-1/2 percent. As shown in the figure below, a decline in the value of r* seems consistent with the decline in the level of longer-term real rates observed in the United States and other countries.

What determines r*? Fundamentally, the balance of saving and investment demands does so. A very clear systematic exposition of the theory of r* is presented in a 2015 paper from the Council of Economic Advisers. Several trends have been cited as possible factors contributing to a decline in the long-run equilibrium real rate. One a priori likely factor is persistent weakness in aggregate demand. Among the many reasons for that, as Larry Summers has noted, is that the amount of physical capital that the revolutionary IT firms with high stock market valuations have needed is remarkably small. The slowdown of productivity growth, which has been a prominent and deeply concerning feature of the past four years, is another factor reducing r*. Others have pointed to demographic trends resulting in there being a larger share of the population in age cohorts with high saving rates.7 Some have also pointed to high saving rates in many emerging market countries, coupled with a lack of suitable domestic investment opportunities in those countries, as putting downward pressure on rates in advanced economies–the global savings glut hypothesis advanced by Ben Bernanke and others at the Fed about a decade ago.

Whatever the cause, other things being equal, a lower level of the long-run equilibrium real rate suggests that the frequency and duration of future episodes in which monetary policy is constrained by the ZLB will be higher than in the past. Prior to the crisis, some research suggested that such episodes were likely to be relatively infrequent and generally short lived. The past several years certainly require us to reconsider that basic assumption.

Moreover, the experience of the past several years in the United States and many other countries has taught us that conducting monetary policy effectively at the ZLB is challenging, to say the least. And while unconventional policy tools such as forward guidance and asset purchases have been extremely helpful, there are many uncertainties associated with the use of such tools.

I would note in passing that one possible concern about our unconventional policies has eased recently, as the Federal Reserve’s normalization tools proved effective in raising the federal funds rate following our December meeting. Of course, issues may yet arise during normalization that could call for adjustments to our tools, and we stand ready to do that.

The answer to the question “Will r* remain at today’s low levels permanently?” is that we do not know. Many of the factors that determine r*, particularly productivity growth, are extremely difficult to forecast. At present, it looks likely that r* will remain low for the policy-relevant future, but there have in the past been both long swings and short-term changes in what can be thought of as equilibrium real rates Eventually, history will give the answer.

But it is critical to emphasize that history’s answer will depend also on future policies, monetary and other, notably including fiscal policy.

What is the relationship between high consume debt levels, and consumption? This is an important question for Australia, given the current record levels of personal debt, and sluggish consumer activity. Also, what will happen should house prices slip back, and households shift to a deleveraging mentality? The short answer is it will have a significant depressive economic impact – if insights from a newly published paper are true.

In a Bank of Canada Staff Working Paper, “Debt Overhang and Deleveraging in the US Household Sector: Gauging the Impact on Consumption” they use a dataset for the US states to examine whether household debt and the protracted debt deleveraging helps to explain the dismal performance of US consumption since 2007, in the aftermath of the housing bubble. By separating the concepts of

deleveraging and debt overhang—a flow and stock effect—they conclude that excessive indebtedness exerted a meaningful drag on consumption over and beyond income and wealth effects.

The leveraging and subsequent deleveraging cycle in the US household sector had a signifi cant impact on the performance of economic activity in the years around the Great Recession of 2007-09. A growing body of theoretical and empirical studies has therefore focused on explaining to what extent and through which channels the excessive buildup of debt and the deleveraging phase might have contributed to depressing economic activity and consumption growth.

They use panel regression techniques applied to a novel data set with prototype estimates of personal consumption expenditures at the state-level for the 51 US states (including the District of Columbia) over the period from 1999Q1 to 2012Q4. They include the main determinants as used in traditional consumption functions, but add in debt and its misalignment from equilibrium. They conclude that excessive indebtedness of US households and the balance-sheet adjustment that followed have had a meaningful negative impact on consumption growth over and beyond the traditional effects from wealth and income around the time of the Great Recession and the early years of the recovery. The e ffect is mostly driven by the states with particularly large imbalances in their household

sector. This might be indicative of non-linearities, whereby indebtedness begins to bite only when there is a sizable misalignment from the debt level dictated by economic fundamentals. They show that some states experienced significant deleveraging and a fall in household wealth.

They argue that the nature of the indebtedness determines the ultimate impact of debt on consumption. The drag on US consumption growth from the adjustments in household debt appears to be driven by a group of states where debt imbalances in the household sector were the greatest. This suggests that the adverse e ffects of debt on consumption might be felt in a non-linear fashion and only

when misalignments of household debt leverage away from sustainable levels – as justfi ed by economic fundamentals – become excessive. Against the background of the ongoing recovery in the United States, where the deleveraging process appears to be already over at the national level, one might expect house-hold debt to support consumption growth going forward as long as the increase in debt does not lead to a widening of the debt gap.

Note that Bank of Canada staff working papers provide a forum for staff to publish work-in-progress research independently from the Bank’s Governing Council. This research may support or challenge prevailing policy orthodoxy. Therefore, the views expressed in this paper are solely those of the authors and may differ from official Bank of Canada views. No responsibility for them should be attributed to the Bank of Canada, the European Central Bank or the Eurosystem.

US Banks are increasing their exposure to commercial real estate and increased competitive pressures are contributing significantly to historically low capitalization rates and rising property values. Influenced in part by the continuing strong demand for such credit and the reassuring trends in asset-quality metrics many institutions’ CRE concentration levels have been rising.

A CRE loan refers to a loan where the use of funds is to acquire, develop, construct, improve, or refinance real property and where the primary source of repayment is the sale of the real property or the revenues from third-party rent or lease payments. CRE loans do not include ordinary business loans and lines of credit in which real estate is taken as collateral. Financial institutions with concentrations in owner-occupied CRE loans also should implement appropriate risk management processes.

Between 2011 and 2015, multi-family loans at insured depository institutions increased 45 percent and comprised 17 percent of all CRE loans held by financial institutions, and prices for multi-family properties rose to record levels while capitalization rates fell to record lows. At the same time, other indicators of CRE market conditions (such as vacancy and absorption rates) and portfolio asset quality indicators (such as non-performing loan and charge-off rates) do not currently indicate weaknesses in the quality of CRE portfolios.

During 2016, supervisors from the banking agencies will continue to pay special attention to potential risks associated with CRE lending.

The regualtors have jointly issued a statement to remind financial institutions of existing regulatory guidance on prudent risk management practices for commercial real estate (CRE) lending activity through economic cycles. They say that historical evidence demonstrates that financial institutions with weak risk management and high CRE credit concentrations are exposed to a greater risk of loss and failure. In general, financial institutions that succeeded during difficult economic cycles took the following actions, which are consistent with supervisory expectations:

established adequate and appropriate loan policies, underwriting standards, credit risk management practices, and concentration limits that were approved by the board or a designated committee; lending strategies, such as plans to increase lending in a particular market or property type, limits for credit and other asset concentrations, and processes for assessing whether lending strategies and policies continued to be appropriate in light of changing market conditions; and strategies to ensure capital adequacy and allowance for loan losses that supported an institution’s lending strategy and were consistent with the level and nature of inherent risk in the CRE portfolio.

conducted global cash flow analyses based on reasonable (not speculative) rental rates, sales projections, and operating expenses to ensure the borrower had sufficient repayment capacity to service all loan obligations.

performed market and scenario analyses of their CRE loan portfolio to quantify the potential impact of changing economic conditions on asset quality, earnings, and capital.

provided their boards and management with information to assess whether the lending strategy and policies continued to be appropriate in light of changes in market conditions.

assessed the ongoing ability of the borrower and the project to service all debt as loans converted from interest-only to amortizing payments or during periods of rising interest rates.

implemented procedures to monitor the potential volatility in the supply and demand for lots, retail and office space, and multi-family units during business cycles.

maintained management information systems that provided the board and management with sufficient information to identify, measure, monitor, and manage concentration risk.

implemented processes for reviewing appraisal reports for sufficient information to support an appropriate market value conclusion based on reasonable market rental rates, absorption periods, and expenses.

The Federal Reserve raised the Fed funds rate by 25 basis points to 0.25 percent – 0.5 percent, during its FOMC meeting held on December 16th. While the Fed said is “reasonably confident that inflation will rise, over the medium term, to its 2 percent objective” , Fed Governors were also carefully to point that “economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate”. It was the first hike since June 2006 when Ben Bernanke increased the benchmark rate from 5 to 5.25 percent. From 1971 until 2015, Interest Rate in the United States averaged 5.93 percent, reaching an all time high of 20 percent in March of 1980 and a record low of 0.25 percent in December of 2008.

Information received since the Federal Open Market Committee met in October suggests that economic activity has been expanding at a moderate pace. Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. A range of recent labor market indicators, including ongoing job gains and declining unemployment, shows further improvement and confirms that underutilization of labor resources has diminished appreciably since early this year. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; some survey-based measures of longer-term inflation expectations have edged down.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will continue to expand at a moderate pace and labor market indicators will continue to strengthen. Overall, taking into account domestic and international developments, the Committee sees the risks to the outlook for both economic activity and the labor market as balanced. Inflation is expected to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee continues to monitor inflation developments closely.

The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2 percent objective. Given the economic outlook, and recognizing the time it takes for policy actions to affect future economic outcomes, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent. The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.