Nonbank online lenders are becoming more mainstream alternative providers of financing to small businesses. In 2018, nearly one-third of small business owners seeking credit reported having applied at a nonbank online lender. The industry’s growing reach has the potential to expand access to credit for small firms, but also raises concerns about how product costs and features are disclosed. The report’s analysis of a sampling of online content finds significant variation in the amount of upfront information provided, especially on costs. On some sites, descriptions feature little or no information about the actual products or about rates, fees, and repayment terms. Lenders that offer term loans are likely to show costs as an annual rate, while others convey costs using terminology that may be unfamiliar to prospective borrowers. Details on interest rates, if shown, are most often found in footnotes, fine print, or frequently asked questions.

The report’s findings build on prior work,

including two rounds of focus groups with small business owners who

reported challenges with the lack of standardization in product

descriptions and with understanding product terms and costs.

In addition, the report finds that a number of websites require prospective borrowers to furnish information about themselves and their businesses in order to obtain details about product costs and terms. Lenders’ policies permit any data provided by the small business owner to be used by the lender and other third parties to contact business owners, often leading to bothersome sales calls. Moreover, online lenders make frequent use of trackers to monitor visitors on their websites. Even when visitors do not share identifying information with the lender, embedded trackers may collect data on how they navigate the website as well as other sites visited.

The Federal Reserve Board and Federal Deposit Insurance Corporation announced Tuesday that they did not find any “deficiencies,” which are weaknesses that could result in additional prudential requirements if not corrected, in the resolution plans of the largest and most complex domestic banks. However, plans from six of the eight banks had “shortcomings,” which are weaknesses that raise questions about the feasibility of a firm’s plan, but are not as severe as a deficiency. Plans to address the shortcomings are due to the agencies by March 31, 2020.

Resolution plans, commonly known as living

wills, describe a bank’s strategy for rapid and orderly resolution

under bankruptcy in the event of material financial distress or failure.

In the plans of Bank of America, Bank of

New York Mellon, Citigroup, Morgan Stanley, State Street, and Wells

Fargo, the agencies found shortcomings related to the ability of the

firms to reliably produce, in stressed conditions, data needed to

execute their resolution strategy. Examples include measures of capital

and liquidity at relevant subsidiaries. The agencies did not find

shortcomings in the plans from Goldman Sachs and J.P. Morgan Chase.

The firms will receive feedback letters, which will be publicly available on the Board’s website.

For the six firms whose plans have shortcomings, the letter details the

specific weaknesses and the actions required. Overall, the letters note

that each firm made significant progress in enhancing its resolvability

and developing resolution-related capabilities but all firms will need

to continue to make progress in certain areas.

To that end, the letters confirm the

agencies expect to focus on testing the resolution capabilities of the

firms when reviewing their next plans. Resolving a large bank would be

challenging and unprecedented, and the agencies expect the firms to

remain vigilant as markets change and as firms’ activities, structures,

and risk profiles change.

The agencies also announced on Tuesday

that Bank of America, Goldman Sachs, Morgan Stanley, and Wells Fargo had

successfully addressed prior shortcomings identified by the agencies in

their December 2017 resolution plan review.

The US Consumer Financial Protection Bureau, Federal Reserve Board, and Office of the Comptroller of the Currency today announced that the threshold for exempting loans from special appraisal requirements for higher-priced mortgage loans during 2020 will increase from $26,700 to $27,200.

The threshold amount will be effective January 1, 2020, and is based

on the annual percentage increase in the Consumer Price Index for Urban

Wage Earners and Clerical Workers (CPI-W) as of June 1, 2019.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010

amended the Truth in Lending Act to add special appraisal requirements

for higher-priced mortgage loans, including a requirement that creditors

obtain a written appraisal based on a physical visit to the home’s

interior before making a higher-priced mortgage loan. The rules

implementing these requirements contain an exemption for loans of

$25,000 or less and also provide that the exemption threshold will be

adjusted annually to reflect increases in the CPI-W. If there is no

annual percentage increase in the CPI-W, the agencies will not adjust

this exemption threshold from the prior year. However, in years

following a year in which the exemption threshold was not adjusted, the

threshold is calculated by applying the annual percentage change in

CPI-W to the dollar amount that would have resulted, after rounding, if

the decreases and any subsequent increases in the CPI-W had been taken

into account.

The Fed chair Jerome Powell said after the decision ” We don’t see a recession, we’re not expecting a recession, but are are making monetary policy more accommodative”, saying it is a mistake to hold onto your firepower until a downturn has gathered moment. This was seen by the market as “hawkish”, much to Trump’s annoyance! The US dollar was stronger after the announcement.

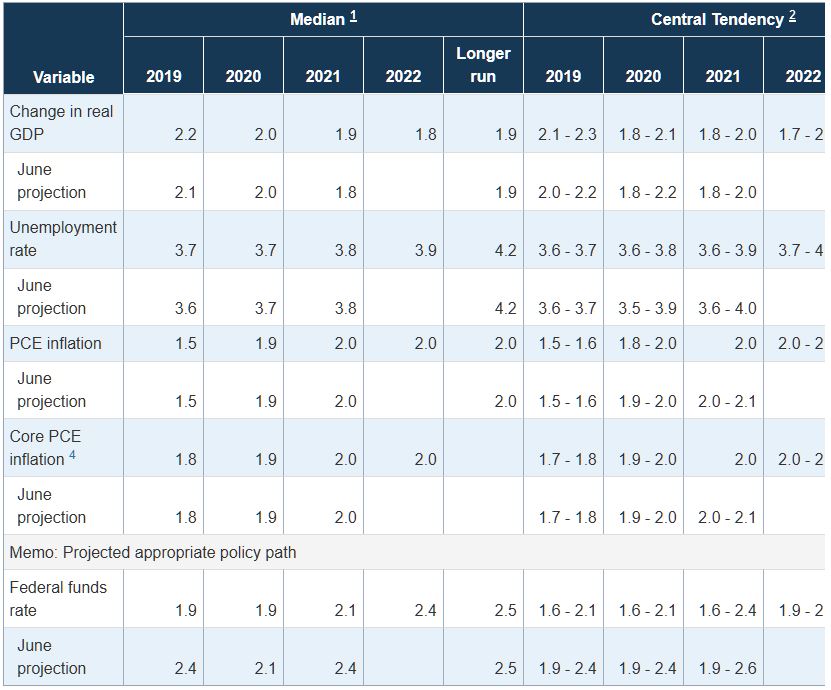

Information received since the Federal Open Market Committee met in July indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports have weakened. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-3/4 to 2 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the

target range for the federal funds rate, the Committee will assess

realized and expected economic conditions relative to its maximum

employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information,

including measures of labor market conditions, indicators of inflation

pressures and inflation expectations, and readings on financial and

international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair, John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were James Bullard, who preferred at this meeting to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent; and Esther L. George and Eric S. Rosengren, who preferred to maintain the target range at 2 percent to 2-1/4 percent.

The approval by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) of the newly updated Volcker rule will ease compliance with the requirements that prevent banks from engaging in proprietary trading, and, in doing so, would enhance their role as market makers and aid market liquidity, according to Fitch Ratings.

The revamped Volcker rule — or Volcker 2.0 — reduces the onus on banks to prove that their trading activities are not proprietary in nature. In addition, and consistent with the aim to tailor regulatory rules, banks with between $1.0 billion and $20.0 billion in trading assets would be subject to a simplified compliance program, while community banks, defined as banks under $10.0 billion in assets with minimal trading assets and liabilities (under 5% of total assets) were already exempted from the Volker rule as part of the Economic Growth, Regulatory Relief, and Consumer Protection Act.

While

most recent regulatory easing initiatives have been aimed at the

smaller banks, Fitch views this change as more impactful for the larger

banks. Relaxing the Volcker rule does not help smaller banks as they

generally do not engage in the type of trading activities the

regulations restrict.

The final rule changed in one important

aspect from the original proposal. Under the initial proposal, the rule

would have encompassed all of a bank’s fair-valued trading assets and

liabilities — the so-called “accounting prong”. However, the final rule

did not retain this test, which would have been more restrictive for

banks and would have scoped-into over $400 billion of available-for-sale

assets. Instead, the rule continues to define a trading account based

on a modified version of the existing rule — as to whether there is a

short-term trading intent — which is more subjective than the

accounting-based test. The new rule also eliminates the presumption that

trading positions held for 60 days or less constitutes prop trading,

thereby freeing up some of the compliance burden associated with

short-tenor trades.

Volcker 2.0 also provides more leeway for

banks to effectively self-police their compliance with the rule as they

will not be required to automatically notify supervisors when internal

risk limits are exceeded. Previously, the rule required banks to

promptly report limit breaches or increases to the regulators.

“Under

the prior rule, banks were presumed guilty unless proven innocent. With

Volcker 2.0, banks are more generally presumed to be innocent unless

proven guilty” said Christopher Wolfe, Managing Director at Fitch

Ratings.

The new rule also modifies the liquidity management

exclusion from the proprietary trading restrictions, permitting banks to

use a broader range of financial instruments to manage liquidity. It

adds new exclusions for error trades, offsetting swap transactions,

certain customer-driven swaps, hedges of mortgage servicing rights, and

purchases or sales of instruments that do not meet the definition of

trading assets/liabilities. It also eliminates the extra-territoriality

reach of the rule for foreign banking entities covered fund activities,

where the risk occurs and remains outside of the U.S.

The

relaxation of the compliance burden potentially opens up some avenues

for banks to engage in what can be viewed as proprietary trading, under

the guise of legitimate market making or liquidity management. The

original rule barred the execution of bank algorithmic trading

strategies that only trade when market factors are favorable to the

strategy’s objectives, or otherwise not qualify for the market-making

exception. In Fitch’s view, the new rule could allow banks to re-engage

in some algorithmic trading that previously did not comply and to some

degree, more effectively compete in market-making activities against

high frequency trading firms (HFTs).

Fitch views the general

prohibition against proprietary trading as a positive from a ratings

perspective. Thus, while there are no immediate rating impacts from

these changes to the Volcker rule, we would negatively view any bank

that increases directional trading activities that can be construed as

proprietary trading or fails to self-police their trading activities

appropriately. Moreover, given still heightened capital and liquidity

standards, potentially including the finalised Basel Market Risk (FRTB)

standard and compressed margins in trading businesses, any increase in

perceived proprietary trading may not generate adequate returns on

capital nor be reflected in better stock valuation.

“The

regulators have opened the door for the larger U.S. banks to engage in

selective risk taking, potentially with an eye toward enhancing market

liquidity and levelling the playing field against HFTs” said Monsur

Hussain, Senior Director at Fitch Ratings.

The Federal Reserve appears to be bailing out the president. From The US Conversation.The central bank is essentially signaling it’s now the administration’s insurer of last resort.

The cut sends a message to financial markets and households that the

Fed stands ready to give the economy a boost should it slow further.

Given that it’s forced to do so by Trump’s own policies, the central

bank is essentially signaling it’s now the administration’s insurer of

last resort.

As an expert on monetary policy

and a former Fed economist, I believe the bank’s embrace of this role

is bad for the economy. It could embolden Trump and other politicians to

pursue policies that are even more reckless – the kind intended more to

benefit narrow constituencies and help win their re-election than

support the broader national interest.

The message matters

Judging the merits of a rate cut usually can only be done in

hindsight. But the case for one seems to be more about what it signals

than directly boosting growth.

By itself, a single quarter-point reduction in the overnight

borrowing rate – the rate most directly affected by the Fed – will

likely do little to alter directly the economic decisions made by

consumers and companies. Virtually no households, and very few businesses, borrow money for such a short term.

Most mortgages, for example, are of the 30-year, fixed-rate type. And

while the Fed’s short-term “target” does eventually affect other

interest rates in the economy, long-term borrowing costs typically react

less to modest changes in monetary policy, especially if these changes

are “one-off.”

Rather, it’s the message that matters. Stoking expectations that the

Fed stands ready to provide additional monetary easing if necessary is a

powerful tool. And although rates are historically low,

the central bank still has another 2 percentage points it can cut to

stimulate the economy, as well as similar tools like so-called quantitative easing.

The Fed’s ‘insurance’ policy

Furthermore, although the economy has slowed slightly, it’s still growing. Some argue that the “insurance” of a rate cut – and the signal it provides that the Fed stands ready to do more – will help maintain that positive growth.

But the very reason the Fed feels the need to do this is because of the government’s own policies. Most economists agree that the current round of tariffs and the resulting disruptions to supply chains have been harmful.

Normally, economic conditions play

a big role in presidential elections. And as the political and economic

costs of a bad policy mount, a president would be forced to switch

course to avoid doing more harm – not to mention damaging his

re-election chances.

Therein lies the problem of the Fed’s rate cut. Its commitment to

reducing rates to stimulate the economy regardless of the source of the

slowdown insulates the administration from the consequences of its

actions, potentially leading to even more misadventures.

Not only that, cutting rates drives up the prices of risky assets – which could metastasize into something harmful, as we saw ahead of the 2008 financial collapse

– and masks other structural problems in the economy. Furthermore, rate

cuts tend to primarily benefit the upper middle class and the wealthy –

the group that owns most of the financial assets in the economy.

Americans experienced something similar in the 1970s.

AP Photo

Cuts have costs

History shows that this kind of central bank insurance is not free.

In the 1970s, President Richard Nixon pressured Fed Chair Arthur Burns

to keep interest rates low in order to help him win re-election in

1972. Ultimately, Burns acquiesced, Nixon won re-election, the Vietnam

War continued for three more years, and the U.S. economy suffered high

and disruptive inflation throughout most of the decade.

Something similar could happen if the Trump administration provides even more fiscal stimulus to bolster its 2020 election chances. Fed rate cuts in conjunction with additional fiscal stimulus could result in higher inflation – which could spook markets and lead to a nasty unwinding.

Author: Rodney Ramcharan, Associate Professor of Finance and Business Economics, University of Southern California

Blog")