Expected inflation rose steadily throughout 2016 and had a relatively large gain during the week of the U.S. elections. What does this mean and why is it important?

The Rise of Expected Inflation

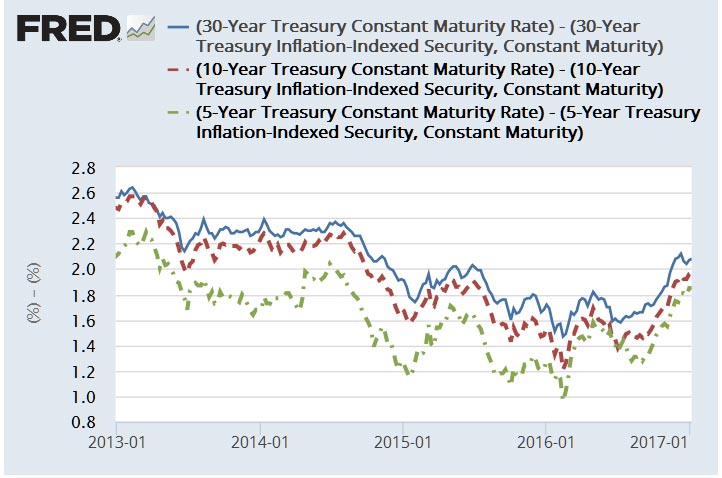

The breakeven rate is the difference between the benchmark Treasury rate and its corresponding inflation-protected security rate. It is used as a market measure of expected inflation. For example, the difference between the 10-year constant maturity Treasury note and the 10-year inflation-protected Treasury note on Nov. 4 was 1.7 percent. This means that investors expect inflation to be around 1.7 percent over the next 10 years.

Over the period Nov. 4-11, the 30-year breakeven rate rose by 10 basis points, while both the 10-year and five-year breakeven rates rose by 8 basis points. By the last week of 2016, breakeven rates were inching closer to the Fed’s longer-run target of 2 percent inflation:1

- The 30-year breakeven rate was 2.07 percent.

- The 10-year rate was 1.97 percent.

- The five-year rate was 1.85 percent.

The Election’s Effect on Expected Inflation

Though unexpected by most, the election results in early November delivered a positive shock to U.S. financial markets overall. Market expectations shifted with the anticipation of aggressive fiscal policy changes, including higher infrastructure spending, financial deregulation and major tax reforms. If these policy changes materialize, they could lead to higher productivity, higher growth rates and a quicker pace of inflation.

However, they could also lead to higher than anticipated levels of U.S. government debt and a growing deficit. Along with recent announcements of major oil-producing countries curbing production to reduce excess supply of oil and help push oil prices higher, speculation around these policies has reinforced expectations of higher inflation.

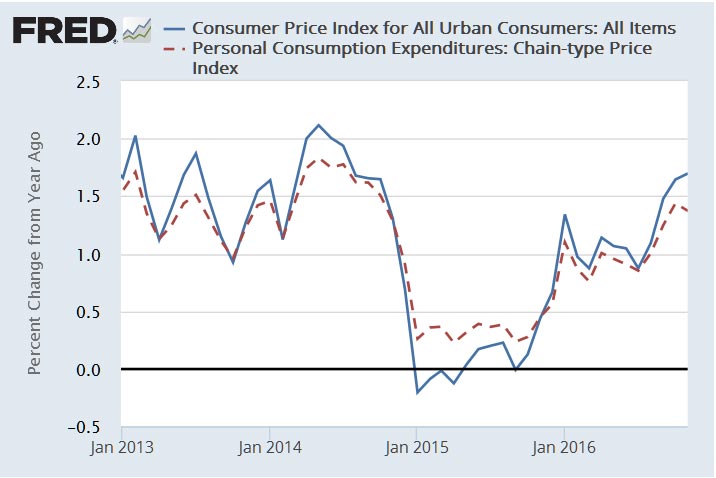

Despite historically low interest rates, and particularly after the steep decline in energy prices at the end of 2014, headline inflation in the U.S. has remained below the Fed’s target rate of 2 percent, as seen in the figure below.

Inflation expectations also declined below 2 percent toward the end of 2014. However, their rise during the last six months of 2016 is a sign suggesting future inflation is expected to be around the Fed’s target rate. At this point, which policies will come to fruition and their impact on the economy remains to be seen.

Notes and References

1 It’s important to note that the Fed’s inflation target is based on the personal consumption expenditures price index, while inflation-protected Treasuries rely on the consumer price index.