The Federal Reserve Board has released the scenarios banks and supervisors will use for the 2019 Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Act stress test exercises. The extreme scenario assumes a short sharp fall, in 2020.

Whilst its a theoretical exercise, kudos to the FED for making public the inputs, and of course they will publish results, to an individual firm level later (unlike or opaque APRA tests, where disclosure remains appalling).

Stress tests, by ensuring that banks have adequate capital to absorb losses, help make sure that they will be able to lend to households and businesses even in a severe recession. CCAR evaluates the capital planning processes and capital adequacy of the largest U.S. bank holding companies, and large U.S. operations of foreign firms, using their planned capital distributions, such as dividend payments and share buybacks and issuances. The Dodd-Frank Act stress tests also help ensure that banks can continue to lend during times of stress, but use standard capital distribution assumptions for all firms. Both assessments only apply to domestic bank holding companies and foreign bank intermediate holding companies with more than $100 billion in total consolidated assets.

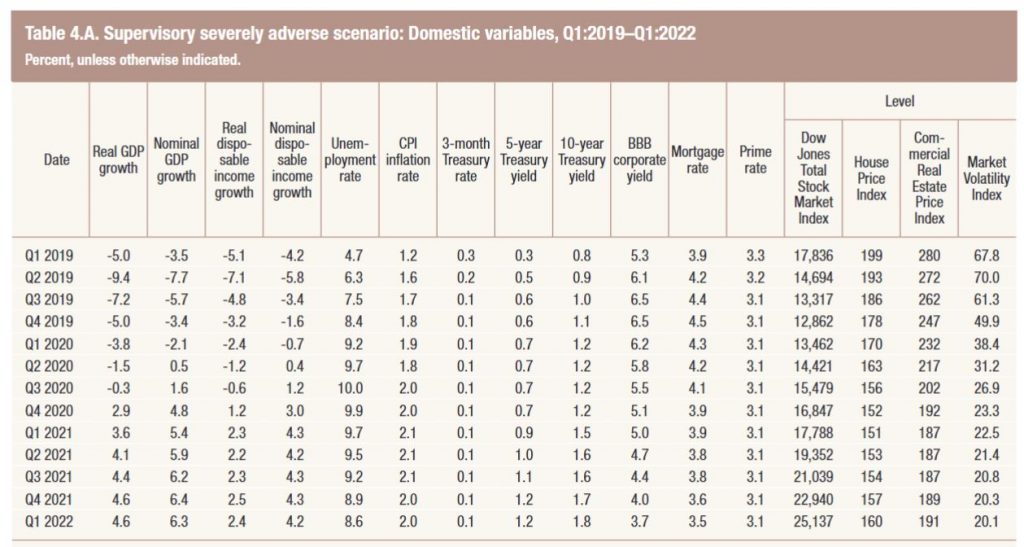

The stress tests run by the firms and the Board apply three hypothetical scenarios: baseline, adverse, and severely adverse. For the 2019 cycle, the severely adverse scenario features a severe global recession in which the U.S. unemployment rate rises by more than 6 percentage points to 10 percent. In keeping with the Board’s public framework for scenario design, a stronger economy with a lower starting point for the unemployment rate results in a tougher scenario. The severely adverse scenario also includes elevated stress in corporate loan and commercial real estate markets.

“The hypothetical scenario features the largest unemployment rate change to date,” Vice Chairman for Supervision Randal K. Quarles said. “We are confident this scenario will effectively test the resiliency of the nation’s largest banks.”

The adverse scenario features a moderate recession in the United States, as well as weakening economic activity across all countries included in the scenario.

The adverse and severely adverse scenarios describe hypothetical sets of events designed to assess the strength of banking organizations and their resilience. They are not forecasts. The baseline scenario is in line with average projections from surveys of economic forecasters. It does not represent the forecast of the Federal Reserve.

Each scenario includes 28 variables–such as gross domestic product, the unemployment rate, stock market prices, and interest rates–covering domestic and international economic activity. Along with the variables, the Board is publishing a narrative description of the scenarios that also highlights changes from last year.

Firms with large trading operations will be required to factor in a global market shock component as part of their scenarios. Additionally, firms with substantial trading or processing operations will be required to incorporate a counterparty default scenario component.

Banks are required to submit their capital plans and the results of their own stress tests to the Federal Reserve by April 5, 2019. The Federal Reserve will announce the results of its supervisory stress tests by June 30, 2019. The instructions for this year’s CCAR will be released at a later date.

Also on Tuesday, the Board announced that it will be providing relief to less-complex firms from stress testing requirements and CCAR by effectively moving the firms to an extended stress test cycle for this year. The relief applies to firms generally with total consolidated assets between $100 billion and $250 billion.

As a result, these less-complex firms will not be subject to a supervisory stress test during the 2019 cycle and their capital distributions for this year will be largely based on the results from the 2018 supervisory stress test. At a later date, the Board will propose for notice and comment a final capital distribution method for firms on an extended stress test cycle in future years.