Neil Slonim, theBankDoctor has published an excellent four part series on the future of non-bank small business lending in Australia. The complete series is reproduced here, with permission.

He concludes that smaller businesses need non-bank lenders especially if they have been rejected by a bank or have relatively modest but often urgent needs for funds or a limited or less than perfect trading history or they are unable or unwilling to offer property as security. However, as he points out, there are traps for the unwary!

The big four banks have long dominated small business finance but things are changing. Post Royal Commission, the banks are still on the nose, they are clamping down on small business credit and meanwhile there’s a whole bunch of non-bank lenders out there offering to help people establish and grow their business.

This paper shines a light on the challenges and opportunities facing both non-bank lenders and their customers.

It is designed to help small business owners make better decisions about how to finance their business by providing an independent insight into the differences between borrowing from a bank and a non-bank as well as the differences between the diverse range of non-bank lenders.

We explore the gap between the expressed intent and action of small business owners towards shifting to non-bank lenders and highlight impediments to the growth of a sector critical to the survival and prosperity of Australia’s small businesses.

Finally we identify what needs to be done for it to fulfill its potential.

The paper is in four parts:

- Part 1. Banks and non-banks are different.

- Part 2. Segmenting the bank & non-bank markets.

- Part 3. Non-bank lenders are a genuine alternative to banks but are SMEs buying it?

- Part 4. What needs to happen for the non-bank sector to become the force SMEs need it to be?”

PART 1. BANKS & NON-BANKS ARE DIFFERENT.

For better or for worse, small business owners know what to expect when borrowing from a bank but how well acquainted are they with non-bank lenders? Non-banks are different to banks as well as to each other. There are several important differences between banks and non-banks including:

The big four banks are huge public companies with combined market value of $400b. They have so much going for them – strong balance sheets, long track records of profitability, access to capital, independent boards, economies of scale and especially customers. They could buy out any non-bank lender whenever they wanted. And with their huge in-house technology capabilities, connections and deep pockets, they could also replicate any product offered by non-bank lenders whenever they wanted.

On the other hand, very few non-bank lenders are publicly listed, they are small, many are only a few years old and yet to turn a profit and most boards are comprised of owner executives.

The banks enjoy Government backing by virtue of the guarantee on deposits and tacit “too big to fail” status. Amongst other benefits, this gives them access to massive low cost deposits that provide a significant funding advantage.

It is inconceivable that any government would bail out a failing non-bank lender and the government guarantee on deposits is only available to banks (authorised deposit taking institutions).

The banks have millions of customers which historically have been a captive market for cross selling. Incumbency and inertia are perhaps their biggest intangible assets.

Along with access the low cost funding, a major challenge faced by non-bank lenders is winning new customers in order to grow.

The banks have a focused and well resourced lobby group in the Australian Banking Association. The ABA developed the 2019 Code of Banking Practice which has been signed twenty six banks including the big four. The Code has been approved by ASIC.

Non-bank lenders do not have their own dedicated association. Perhaps the nearest equivalent is the Australian Finance Industry Association (AFIA) which has over 100 members plus 45 associate members. The big four banks are also members. AFIA is not as well resourced or singularly focused as the ABA but it has overseen the development of a Code of Practice for online small business lenders. Seven lenders have signed up to this code although it has not been approved by ASIC.

The banks have around 5,600 branches around the country. Whilst branches are a more expensive way of engaging with customers compared to the more technology based means adopted by many non-bank lenders, a branch network does afford direct access to customers.

Non-bank lenders are more inclined to rely on lower cost technology to engage with customers.

The banks offer a wide range of products and services covering all industry sectors. Having a wide range of products and servicing many industries can also be both an advantage and a disadvantage.

Most non-banks offer a limited product range but many specialist product or industry lenders have been able to carve out niches for themselves.

Banks are regulated by APRA in accordance with the Banking Act. Post Royal Commission, engagement with regulators including ASIC, APRA and ACCC will only increase.

Non-banks are not licensed to take deposits and are much less regulated which has its benefits and disadvantages for both the lenders and their borrowers. But in time there is little doubt non-bank lenders will be subject to levels of regulation not vastly different to the banks.

From the above it would seem that the non-bank lenders are really up against it but they do have one hugely significant advantage in that customers actually like them much more than they like the banks.

Evidence of this includes Trustpilot and Net Promoter Scores that the banks could only dream of. The CBA is the only one of the big four with an overall positive NPS but it only rates 3.8 and is followed by NAB (-5.6), ANZ (-6.8) and Westpac (-7.3). It is not uncommon for non-banks to have NPS scores in the 70’s.

The other big advantage non-bank lenders have is that they can and do move quickly. They are not constrained by legacy systems, convoluted organisational structures and an aversion to change.

The banks still dominate SME lending, but this is a huge market and there is both the room and need for the non-bank lenders. In Part 2 we look at the relative size and composition of these markets.

PART 2. SEGMENTING THE BANK & NON-BANK SME LENDING MARKETS.

The biggest problem in analysing the Australian SME lending market is the lack of a uniform definition of what constitutes a small or a medium business. The measures used can be based on turnover, borrowings or employees. The banks themselves are divided although a cynic might describe this as a ploy.

The RBA, ABS, regulators and other government bodies don’t have a common definition. Kate Carnell is the Australian Small Business & Family Enterprise Ombudsman not the Australian SME Ombudsman. Visy Group and Hancock Prospecting are family enterprises with estimated net worths of $6.9b and $5.1b respectively. It’s a minefield and until such time as all stakeholders can agree on this, it will remain impossible to accurately measure SME lending. Acknowledging this is not an easy task, let’s have a go anyway.

Bank Lending to SMEs.

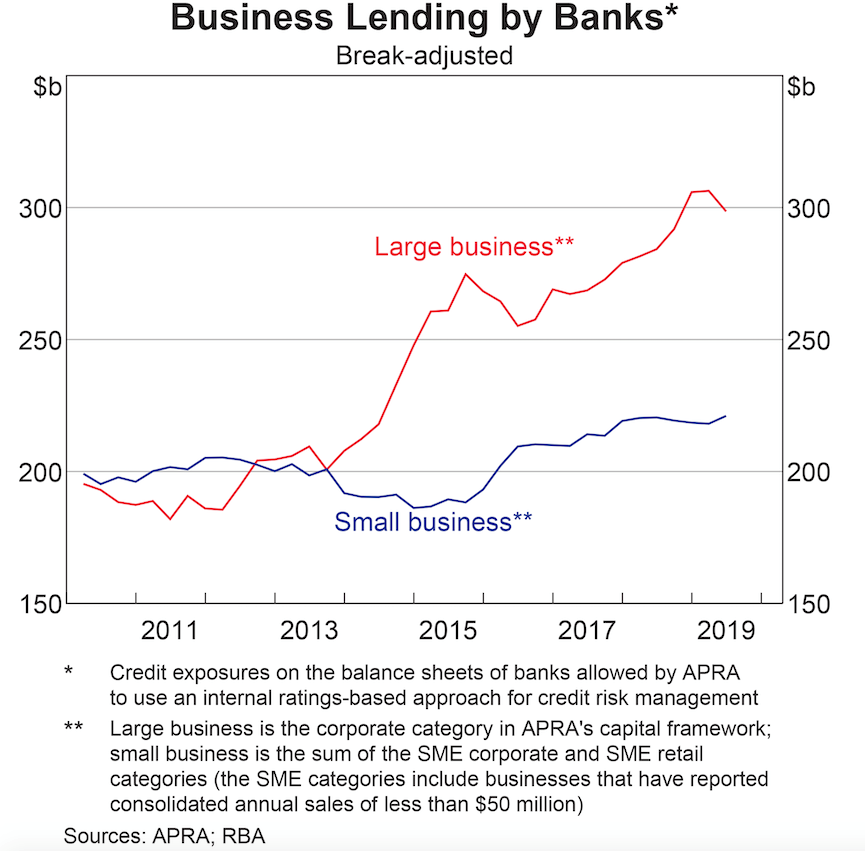

The chart below derived from APRA and RBA statistics, business lending by banks to small business (defined as annual turnover of less than $50m – that’s right, $50m turnover is a small business!) is around $230b. This chart also confirms the widely held view that since 2013 the banks have preferred to lend to larger businesses than their smaller counterparts.

There is not much point in commenting on the composition of the bank lending market as it is dominated by the big four bank oligopoly including their subsidiaries.

Non-bank lending to SMEs.

Not only do we have the inconsistency in the definition of a small or medium business but the non-bank SME lending sector itself is comprised of literally hundreds of organisations and total lending volumes so no-one can put a reliable figure on how much non-bank SME lending takes place in Australia.

To try to give a sense of how fragmented the non-bank SME lending market is, let’s look at three of the more widely recognised players outside the big four banks:

Prospa, the acknowledged leader in online business loans, had a loan book of $379m at June 2019. It originated over $500m in loans in FY2019 and has a customer base of 20,000. In its 2019 annual report it claims to have a 50 per cent share of the online business loans market implying that online business lenders are currently originating about $1b of loans per annum.

Scottish Pacific, Australia’s leading non-bank debtor finance lender had loan receivables of over $1b in 2018 with around 1,600 customers. Interestingly, its biggest competitors are Westpac and NAB which also happen to provide wholesale funding to Scottish Pacific.

Judo Bank can no longer be regarded as a non-bank as it gained its license earlier this year. It plans to be lending more than $1b to SMEs by the end of this year and $10b within 3 years which they say represents only 2 per cent of the SME lending market, implying a market size of $500b. Judo claims there is a $90b “finance gap” for SMEs that want finance but cannot get it from banks.

These three lenders have combined total loans of less than $3b, representing about 1.25 per cent of the size of the combined SME loan books of the banks. Between them they could have around 25,000 customers in a potential market in excess of one million small businesses.

Segmenting this market is only marginally less difficult than measuring its size. One way this might be done is by distinguishing between “Old” and “New” lenders.

The former have been around for some time, often decades. The products they offer tend to be traditional and the credit process while taking advantage of new technology still remains much the same.

Perhaps the biggest “Old” segment is finance for assets such as equipment, vehicles, machinery and computer hardware. The products they offer include operating lease, finance lease, commercial hire purchase, chattel mortgage and novated lease. Some asset financiers specialise in servicing one industry such as hospitality or health care whilst others finance a full range of industries.

Other “Old” type lenders might also include debtor finance, import and export finance and supply chain finance.

Premium funding of insurance and other professional fees is another type of business lending that has been around for some time.

Some “Old” lenders are well known ASX companies whilst others are one person businesses which can fly under the radar.

”New” lenders are those that have entered the market in the last few years and the way they gather and analyse data and then make and communicate decisions is centred around technology. These are also commonly referred to as “online”, “fintech” or “alternative” lenders.

The most common products offered by online lenders are principal and interest (amortising) loans, lines of credit and merchant cash advances. Some also provide debtor and other forms of working capital finance.

“New” lenders also include global giants like PayPal and Amazon that offer their customers access to finance based on the volume of business conducted. A new Australian bank Tyro is another rapidly growing player in what is generally termed the Merchant Cash Advance segment.

To varying degrees the “Old” lenders are now adopting “New” ways of doing business through the use of technology.

Wholesale v Retail.

For several reasons, such as cumbersome legacy systems, banks are unable to make acceptable returns from lending to the bottom end of the SME market where loan sizes are small, property security is not available and where the borrower has either a limited or less than perfect trading history. But this doesn’t mean they don’t have exposure to this end of the market because very often they do. How? Simply, instead of lending directly to these SMEs, they lend to the non-banks that do. The big banks provide “wholesale” funding to “retail” non-bank lenders that finance SMEs the banks themselves probably wouldn’t lend to.

Whilst they are happy not to lend directly to the low end of the SME market, the banks wont cede that segment of the market which is low risk, well secured by property and offers good returns from the range of bank products supplied.

Whether it is through wholesale or retail lending, their sheer size still enables the banks to dominate small business lending but through their actions and inactions, they have opened the door for the non-bank lenders.

PART 3. NON-BANK LENDERS ARE A GENUINE ALTERNATIVE TO BANKS BUT ARE SMES BUYING IT?

According to most recent SME Growth Index conducted by East & Partners for Scottish Pacific, less than 18 per cent of SMEs see their bank as the preferred lender for future growth, down from around 40 per cent in 2014. The same report indicates that now more SMEs are likely to fund growth by using a non-bank than their main bank. Howe much of this trend is due to disenchantment with the banks or, on the other had, attraction to non-banks?

Let’s first look at why SMEs are dis-engaging with the banks. Below are five reasons or “pain points”:

1. It has become harder to get a loan from a bank.

The AltFi 2019 SME Research Report, commissioned by online lender OnDeck Australia, revealed almost one in four small

business owners who have applied for bank finance have been rejected.

This is even higher amongst those with lower turnover or shorter trading

history. The 2019 SME Banking Insights Report commissioned by Judo Bank revealed an identical

rejection rate. And once they’ve been rejected by a bank, SMEs are less

inclined to go back.

In contrast, an Australian Banking Associationsurvey of its members revealed 94 per cent of small business loan applications are approved. This number appears so high that it stretches credibility and so does not assist the perception of banks.

The banks say they remain open for business but demand for business credit has fallen citing a drop in loan applications of 33 per cent since 2014. The counter view is that many SMEs have just given up applying for bank loans.

2. Not only is it harder to get a bank loan, it takes longer and the process can be onerous and time consuming. Banks are now being especially cautious by probing into the personal spending habits of their small business clients. A delayed “no” decision can really impact on cash flow. The AltFi report revealed that more than 29 per cent of SME’s claim to have been negatively affected as a result of the time taken to get finance – with this increasing to 65 per cent if they had been turned down by a bank.

3. Service levels

have fallen as a result of regular restructuring and downsizing in banks. The

relationship banking model is no longer available to small businesses and the

personal connections which many once had no longer exist. This is the core

premise of Judo Bank’s offering.

4. Banks generally don’t want small business borrowers unless they can offer

property as security. But declining home ownership rates, especially amongst

younger small business owners, means that for many a loan from a bank is

simply out of the question. ABS statistics show that a

third of Australians don’t own a home and another 30 per cent have a home

that is already mortgaged. The SME Growth Indexrevealed that 21 per cent of SMEs cited their desire to avoid

offering property as security as the key reason for looking to switch to a

non-bank lender. And 92 per cent were prepared to consider paying more in order

to avoid having to offer property as security.

5. Many SMEs have lost faith in banks and believe the banks are all much the same. Almost 10 per cent of respondents in the SME Growth Indexsaid the Royal Commission disclosures were the reason for switching to non-bank lenders to fund their growth.

Bank leaders openly acknowledge they have put shareholders ahead of customers and longstanding customers believe that loyalty doesn’t count any more. Following the most recent RBA Cash Rate cut, Macquarie Bank claimed banks are offering new retail mortgage customers on average a 50 basis point (0.05 per cent) discount compared to existing customers. It would not be unreasonable to conclude that banks are doing the same with loyal small business customers where fees and charges are even more opaque.

Clearly many SMEs are not

enamoured with the banks so it is not surprising they seem to be favourably

disposed to switching to non-bank lenders. Interest in non-banks is

growing with the AltFi report indicating 22

per cent of SME’s are open to considering this option compared to 11 per cent

who had considered online lenders previously. And only 2.6 per cent respondents

said they would not consider using a non-bank lender.

The Australian SME Banking Council report of 2019 produced by global financial services

research organisation RFi Groupfound,

perhaps unsurprisingly, that openness to using alternative lenders is much

stronger amongst people under the age of 44. And in terms of operating tenure,

the sweet spot for alternative lenders is newer businesses that have been in

operation for less than 2 years. RFi defines

“alternative” as those using different lending models from banks, for instance

peer-to-peer lenders (which match investors with borrowers), or companies that

use non-traditional information, like sales data or customer reviews, to verify

loan applications. This is really the fintech segment.

The AltFi report revealed that 33 per cent of SMEs rejected by

a bank ended up borrowing from family and friends. Another third used a credit

card and 13 per cent actually gave up! Only 6 per cent of SMEs knocked back by the

bank went to a non-bank lender.

So if the banks are on the nose and SMEs have favourable intentions

towards non-banks, why are they still much more inclined to revert to

traditional sources of funds like credit cards and what is really holding them back from

borrowing from non-bank lenders? ? Here’s four possible

explanations:

1. Awareness of non-bank lending options has improved considerably although there is still room for improvement. But once the awareness challenge is overcome, the next hurdle is understanding and this is not easy. Many, perhaps the majority, don’t have a level of understanding to confidently dip their toe in the water and borrow from a non-bank. Plus they are time poor so when push comes to shove they often just try to muddle through via more familiar means.

2. Borrowing from a non-bank

lender can be expensive but the way some lenders disclose, or not disclose,

fees and charges can make it difficult to work out exactly how expensive. In

addition, this inhibits the capacity to be able to make apples with apples

comparisons between alternative providers. General chat about some non-bank

lenders acting more like “payday lenders” is a turn-off for SMEs and impacts on

all non-bank lenders.

3. SMEs struggle to know where to get independent and affordable advice on

what is the best way to finance their business. And most advisors don’t have a

good working knowledge of the non-bank lending sector anyway.

4. According to the RFi report,

even though trust levels are down, SMEs still have a higher “comfort” level

with banks than non-banks. It showed SMEs had a 45 per cent comfort level

when dealing with a bank as compared to between 20 per cent and 30 per cent for

alternative lenders, other financial institutions and digital only banks. This

is the “better the devil you know” factor.

The RFi survey asked SMEs that were aware of alternative

lenders “why has the business not used an alternative lender?” and the main

reasons given were they are less convenient, less trustworthy and charge higher

fees/charges. This pertains to the “New” non-bank lenders like

fintechs rather than “Old” non-bank lenders.

Are non-bank lenders competitors, collaborators or no threat to the banks?

It should be noted that whilst some SMEs are able to access bank

finance (which is nearly always going to be cheaper

than non-banks) many are unable to tick all the bank’s boxes and

for them it is not a question of choosing between a bank and a

non-bank, their only option might be a non-bank lender. So non-bank

lenders will sometimes be competitors of banks and at other times be no

threat at all. And they are collaborators when the banks

providing wholesale funding. They can also collaborate through formal and

informal referral partnerships and sharing of knowledge perhaps with a

view to a bank buy out down the track. It’s complicated.

SMEs are turning off banks and at the same time they are expressing a willingness to use non-bank lenders, but many are just not buying it – yet.

In the final of this series we discuss what needs to happen for the non-bank sector to become the force SMEs need it to be.

PART 4. WHAT NEEDS TO HAPPEN FOR THE NON-BANK SECTOR TO BECOME THE FORCE SMEs NEED IT TO BE?

Small business owners need the non-bank market to be sustainable, reputable and competitive. Politicians and bureaucrats want this too. Whilst considerable progress has been achieved to date, here are some areas in which more can and needs to be done.

1. Better data on SME lending.

We live in a world where data is paramount. We have to be able to gather and report reliable data on both bank and non-bank SME lending. The starting point is to agree on a definition of what is a “small” and a ‘medium” business. Government bodies like the RBA, ABS, ASBFEO and industry associations like the ABA, AFIA, COSBOA and Fintech Australia need to agree on a definition. Here is my suggestion:

“Small” business has total borrowing limits from bank and non-bank lenders of < $1m.

“Medium” business has total borrowing limits from bank & non-bank lenders between $1m – $5m.

There will always be differing views about the appropriateness of whatever threshold is adopted and but a start has to be made somewhere.

2. Awareness & Understanding

SMEs should be able to readily understand how different products are right for different business situations. The popular phrase for this is “fit for purpose”.

There is also a lack of understanding around the issue of pricing for risk. And business owners aren’t comparing like with like if they are just comparing interest rates rather than other factors like terms and conditions and fees and charges.

Another area of confusion is security. Non-bank loans that are promoted as being “unsecured” might still require directors to provide personal guarantees and/or agree to the lender registering a General Security Agreement under the Personal Property Securities Act. Such loans should not be described or priced as “unsecured”.

Equally there is a need for a better understanding of the different roles played by debt and equity in financing the establishment and growth of a small business. Debt isn’t always the right solution.

There are tools and materials available to help SMEs and their advisors although many of these put the lender(s) first rather than the customer. A classic example is the “Financing your small business” website backed by the ABA. This is a useful resource if you are only considering applying for bank finance but it totally overlooks the existence of non-bank lenders that have offerings which might be more suitable.

The Government’s Business Finance website provides independent and free information and the Australian Small Business & Family Enterprise Ombudsman’s Business Funding Guide should be compulsory reading for any small business owner looking to raise finance.

3. Legislative protection for small business borrowers.

There is a strong argument that small business owners, many who operate as sole traders or in partnerships, should be afforded the same or at least similar level of protection as consumers. The National Consumer Credit Protection Act requires standardised disclosure of loan prices, but when those same consumers apply for a business loan they are left in the dark. For instance, consumer credit providers are required to include the Annualised Percentage Rate in any advertisement that states the amount of any repayment but this law does not apply to business credit providers.

It is perplexing why Kenneth Hayne and others continue to imply that because someone operates a small business they must have a higher level of financial literacy than a consumer. Lack of transparency in non-bank business lending remains a significant unresolved issue and this will continue to hamper its reputation and therefore growth until such time as it is properly addressed.

4. Industry regulation including self-regulation.

The banks are more heavily regulated and monitored than non-banks. This may well be deserved but anyone who believes that misconduct in the non-bank sector is not an issue is delusional. There are 25 bank signatories to the Code of Banking Practice including the big four and post Royal Commission we can expect ASIC will be much more diligent in holding these banks to account.

Earlier this year seven online small business lenders established the Online Small Business Code of Lending Practice (not approved by ASIC) but outside of this code there are no others which bind non-bank SME lenders. This is something individual lenders and their roof bodies must address. Failure to do so in a timely and meaningful manner will invite intervention by regulators.

The Banking Royal Commission recommended a law be introduced requiring mortgage brokers to act in the best interests of their clients. It would give SMEs more confidence in dealing with brokers and introducers if there were a similar law requiring them to act in the best interest of clients they refer to lenders.

5. Government assistance for new players.

It seems that finally politicians and bureaucrats get that the best way to improve competition in the banking sector is not by trying to persuade the banks to change but to make it less onerous for new players to open for business and then compete at least on a near level playing field.

One example of this is the Australian Business Securitisation Fund which will make $2b available over time to help small banks and non-bank lend to small businesses. The goal is to “kick-start” the establishment of a securitisation market for SME loans. It is to be hoped that these funds will find their way to lenders that will help plug the “lending gap” referred to earlier.

In 2016, the UK government introduced the Bank Referral Scheme which requires banks that reject an SME loan application to refer that SME to a non-bank lender. Since that time 1,700 of the 30,000 rejected SMEs have been successfully funded under the scheme. And tellingly, the conversion rate is steadily rising as all parties become more familiar with the process.

Other kinds of government assistance which have worked successfully overseas and should be considered here include the UK’s British Business Bankand the USA’s Small Business Administration which both provide guarantee support to approved lenders that provide funding to small businesses.

6. Lower cost of capital for non-bank lenders.

This is a “chicken and egg” problem. Lenders need to demonstrate a strong record before they can access lower cost funds but when your cost of capital is high, this has to be reflected in the rates charged to customers. This will take time but if lenders can demonstrate strong performance this will be reflected in lower funding costs. Prospa’s cost of funding has fallen from 14.6 per cent in 2016 to 8.5 per cent in 2018.

Ironically, the “chicken and egg” problem is exactly the same for the small businesses that are told they need a better track record to attract more funds at lower rates.

One way, albeit expensive and onerous, for non-bank lenders to reduce their cost of capital is to obtain a banking license. Judo Bank won their license in April this year and now funds 70 per cent of its loan book from lower cost government guaranteed deposits.

7. Roles played by accountants, brokers and other trusted advisors.

Non-bank lenders are heavily dependent on “partners” for business introductions. For instance, Prospa sources 70 per cent of its business from partners including accountants and brokers. The Judo Bank model is also heavily reliant on partners.

But interestingly, the SME Growth Index revealed that less than one in ten SMEs regard their accountant or broker as their trusted finance advisor. What is perhaps more concerning is that the number of SMEs nominating their accountant as their most trusted advisor has halved since 2017 to 5.7 per cent and the Bank Manager, comes in at a lowly 2.6 per cent probably because they don’t exist to rely on!

RFi asked SMEs who had used an alternative lender “Why did you not choose to use a broker when you took out the loan?” The most common explanations were “I thought it would be simpler/quicker/cheaper to go direct” and also “I don’t trust brokers”.

This is an opportunity for brokers, accountants and their roof bodies. By keeping abreast of developments in small business funding, they will be able to better guide their clients in ways that genuinely add value to the relationship.

CONCLUSION.

It is evident from researching this topic that some statistics and surveys published by different parties can be difficult to reconcile. But what is undeniable is that smaller businesses need non-bank lenders especially if they have been rejected by a bank or have relatively modest but often urgent needs for funds or a limited or less than perfect trading history or they are unable or unwilling to offer property as security.

If non-banks and their partners, industry bodies and regulators are able to work collaboratively to ensure the sector is sustainable, reputable and competitive, the lending gap SME lending gap can be closed. Opportunity abounds for both non-bank lenders and SMEs.

As for the banks, incumbency and inertia have assisted them in maintaining their dominant positions but several pain points are steadily eroding these advantages and initiatives like Open Banking could eliminate them all together. The future of the banks lies in their own hands.

Ultimately however, it is the responsibility of borrowers to inform themselves about how non-bank lenders might help them achieve their own goals.

Neil Slonim theBankDoctor October 2019