The focus on power prices and the behaviour of the power companies where households end up on higher rates, draws attention to the oldest trick in the book – offer attractive rates for new business, but rely on consumer apathy/confusion or create hurdles to continue to get the best prices. Companies seeking to maximise their returns from hapless consumers.

The same is true in financial services, where both on the mortgage and deposit side of the ledger, it is easy for households to drift to rates which are not the best available. The banks rely on this to protect their margins and profits, just like the power companies.

Now of course the power companies, under duress, are going to write to some consumers to help them find better deals. So why not the banks too?

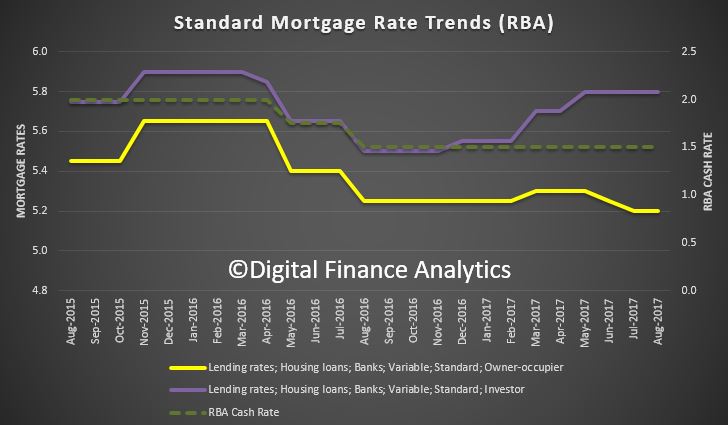

In the past year lenders repriced their mortgage books aggressively, to increase margins, and imposed out of cycle rate hikes on all borrowers. The trajectory of those varied between investor and owner occupied loans.

This chart, using data from the RBA tracks the rates on offer and we overlay the cash rate on the second axis. They have built quite a war chest!

But in fact, the best new attractor rates are more than 100 basis points lower for some low risk customers, but only for new ones. It is harder for existing customers to get better rates, (but it is still worth being proactive and asking). There are costs involved in switching, and work to be done to find the deals out there.

But in fact, the best new attractor rates are more than 100 basis points lower for some low risk customers, but only for new ones. It is harder for existing customers to get better rates, (but it is still worth being proactive and asking). There are costs involved in switching, and work to be done to find the deals out there.

Philip Lowe commented recently on how competitive dynamics drove lenders to take more risk:

One might ask why lenders themselves did not do more to constrain their activities in these areas, given the earlier trends were adding to risk in the overall system. When everything is going well, it appears that any single institution has difficulty pulling back. Each worries about their competitive position and about the market reaction. Individual institutions are also more likely to focus on their own risks, rather than the risks to the system as a whole.

We suspect the same argument would be mounted internally – replace risk, with profit – against the idea of helping customers to optimise the returns from their deposits and reduce their mortgage rates. But we think this is precisely where differentiation can and should emerge.

If a bank was really interested in customer outcomes, they would be proactive in suggesting products with better rates, rather than relying on inertia. Actually this could become a significant point of differentiation, and would be a touchstone for brand improvement and cultural change.

Imagine using the information systems inside the bank to analyse existing product footprints and proactively suggest better alternatives. No better way to build customer trust a loyalty, something which is sadly missing in the current profit at all cost drive approach. The truth is that long term shareholder value is actually aligned to building true customer loyalty. Yet this is largely ignored at the moment.

What about a proactive financial health check, where the bank and customer could jointly discuss options and alternatives? This is even something a robo-banker might do.

Time for someone to step out from the pack.