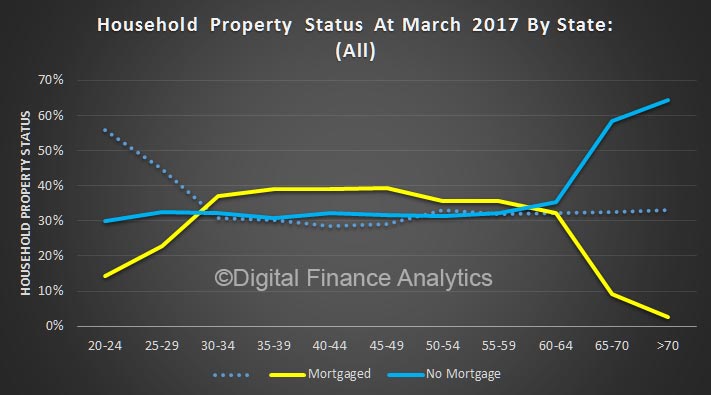

On average, according to our surveys, one third of households are living in rented accommodation, one third own their property outright, and one third have a mortgage. Actually the trend in recent years has been to take a mortgage later and hold it longer, and given the current insipid income growth trends this will continue to be the case. Essentially, more households than ever are confined to rental property, and more who do own a property will have a larger mortgage for longer.

Now, if we overlay age bands, we see that “peak mortgage” is around 40% from late 30’s onward, until it declines in later age groups. The dotted line is the rental segment, which attracts high numbers of younger households, and then remains relatively static.

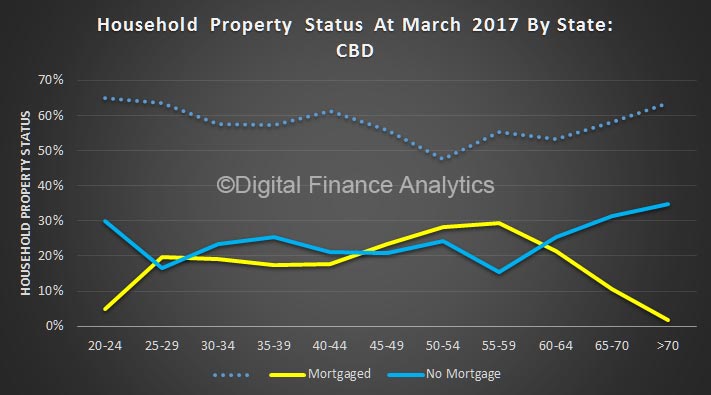

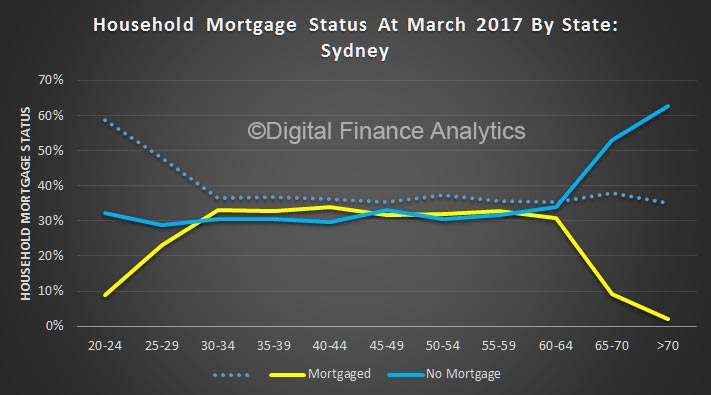

But the mix varies though the age bands, and across locations. For example, in the CBD of our major cities, most people rent. Those who do own property will have a mortgage for longer and later in life.

But the mix varies though the age bands, and across locations. For example, in the CBD of our major cities, most people rent. Those who do own property will have a mortgage for longer and later in life.

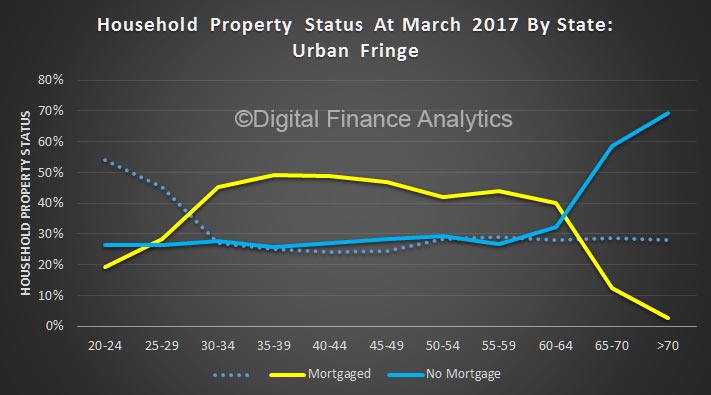

Compare this with households on the urban fringe. Here more are mortgaged, earlier, less renting, and mortgage free ownership is higher in later life.

Compare this with households on the urban fringe. Here more are mortgaged, earlier, less renting, and mortgage free ownership is higher in later life.

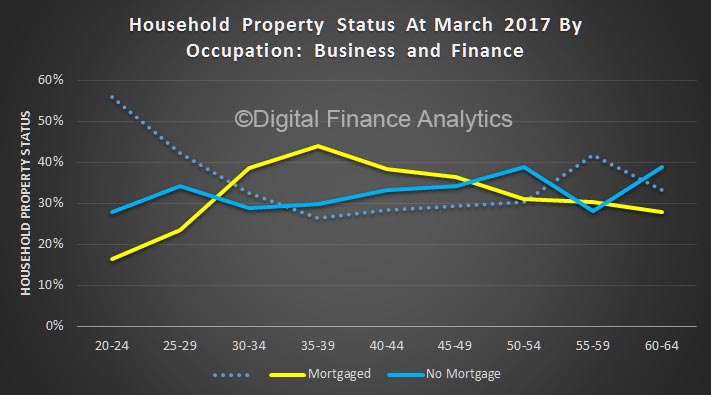

Different occupations have rather different profile. For example those employed in business and finance reach a peak mortgage 35-39 years, and then it falls away (thanks to relatively large incomes).

Different occupations have rather different profile. For example those employed in business and finance reach a peak mortgage 35-39 years, and then it falls away (thanks to relatively large incomes).

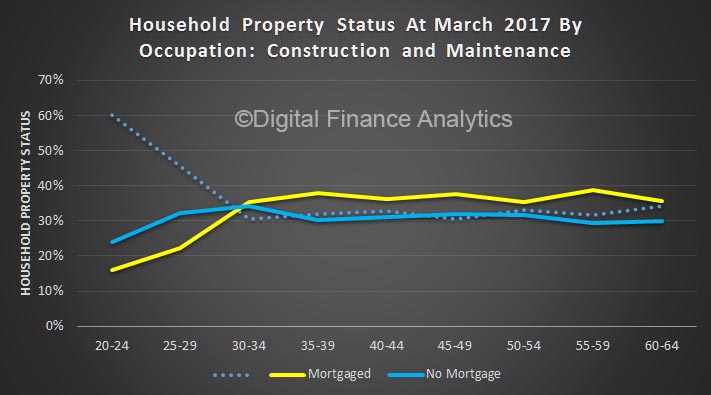

Compare this with those working in construction and maintenance.

Compare this with those working in construction and maintenance.

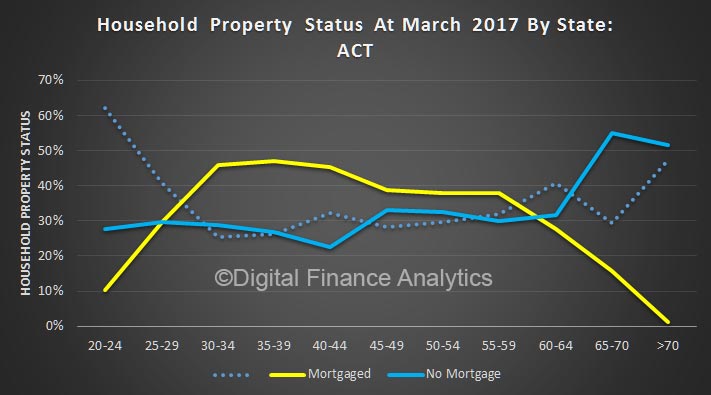

Finally, across the states, the profiles vary. In the ACT more households get a mortgage between 30-34, thanks to predictable public sector wages.

Finally, across the states, the profiles vary. In the ACT more households get a mortgage between 30-34, thanks to predictable public sector wages.

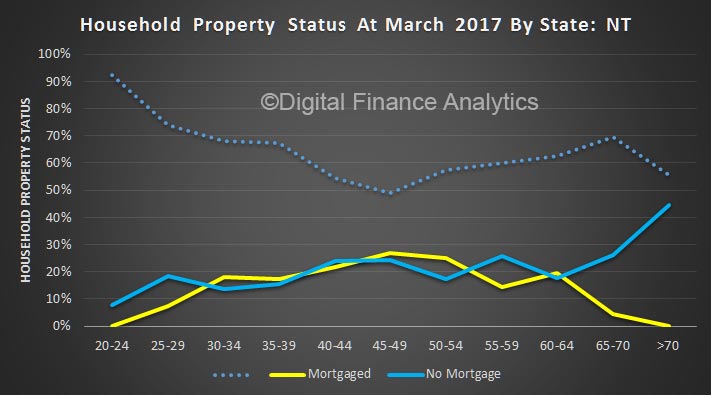

Renting is much more likely for households in NT.

Renting is much more likely for households in NT.

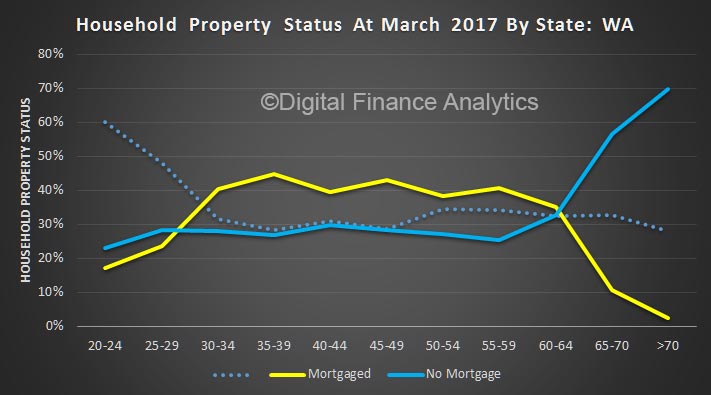

WA has a high penetration of mortgages among younger households (reflecting the demography there).

WA has a high penetration of mortgages among younger households (reflecting the demography there).

Most of the other states follow the trend in NSW, with the rule of thirds clearly visible.

Most of the other states follow the trend in NSW, with the rule of thirds clearly visible.

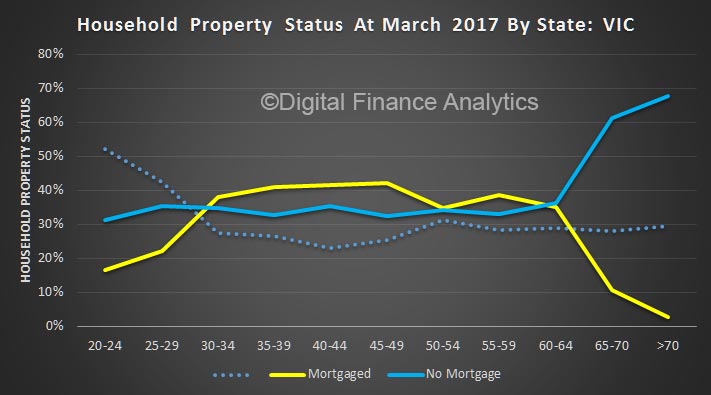

Victoria, for example, has a higher penetration of mortgages, and smaller proportions of those renting.

Victoria, for example, has a higher penetration of mortgages, and smaller proportions of those renting.

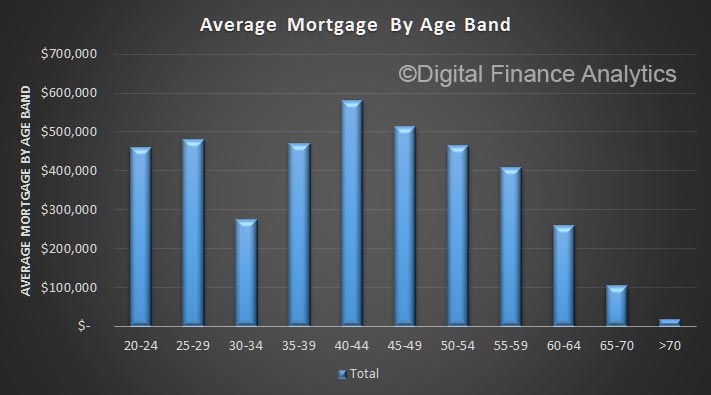

We find these trends important, because it highlights local variations, as well as the tendency for mortgages to persist further in the journey to retirement. This explains why, as we highlighted yesterday, some older households still have a high loan to income ratio as they approach retirement. To underscore this, here is average mortgage outstanding by age bands.

We find these trends important, because it highlights local variations, as well as the tendency for mortgages to persist further in the journey to retirement. This explains why, as we highlighted yesterday, some older households still have a high loan to income ratio as they approach retirement. To underscore this, here is average mortgage outstanding by age bands.