The Bank of England just released their lending trends data for first quarter 2015. Included in the report is some relevant data on investment or buy-to-let loans. BTL mortgages accounted for 15% of the total outstanding value of UK-resident mortgages as at end-2014 Q4. The rate of possession of buy-to-let properties was almost twice as high as for owner-occupied ones.

Overall, the rate of growth in some measures of the stock of lending to UK businesses picked up in the three months to February. Net capital market issuance was positive in this period. Mortgage approvals by all UK-resident mortgage lenders for house purchase rose slightly in the three months to February compared to the previous period. The stock of secured lending to households increased, but the pace of growth has slowed since 2014 H1. The annual growth rate in the stock of consumer credit was little changed in recent months.

Pricing on lending to small and medium-sized enterprises was little changed in the three months to February. Respondents to the Bank of England’s 2015 Q1 Credit Conditions Survey reported that spreads on new lending to large businesses fell significantly. The Bank’s series of quoted interest rates on fixed-rate mortgages decreased in 2015 Q1 compared to the previous quarter. Quoted rates on some personal loans continued to fall.

Contacts of the Bank’s network of Agents noted that credit availability had eased further, including for most small and medium-sized companies. Respondents to the Bank of England’s Credit Conditions Survey expected demand for bank lending to increase significantly from small businesses, increase from medium-sized businesses and be unchanged from large businesses in 2015 Q2. Lenders in the survey reported that the availability of secured credit to households was broadly unchanged and that

demand for secured lending fell significantly in the three months to early March 2015.

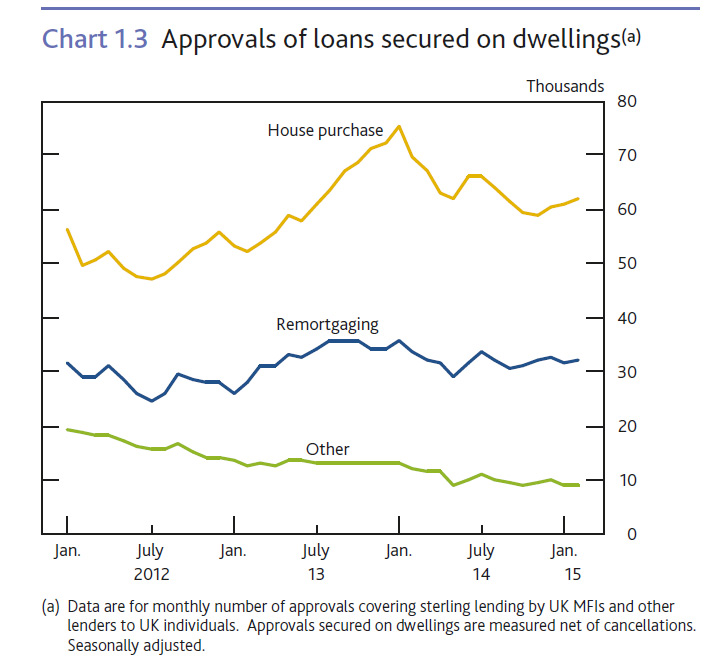

Secured lending to individuals. The number of mortgage approvals by all UK-resident mortgage lenders for house purchase increased slightly in the three months to February compared to the previous period. Approvals for remortgaging also rose slightly. The stock of secured lending to individuals increased, but the pace of growth has slowed since 2014 H1. The monthly net mortgage flow was little changed in recent months.

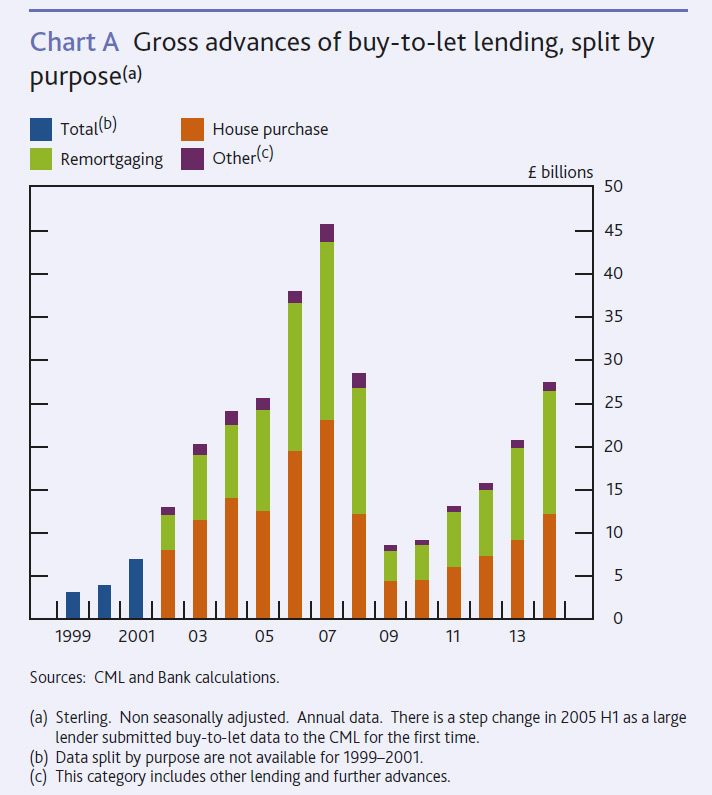

Overall, gross secured lending was higher in 2014 than in recent years. Within this, the share of gross lending for buy-to-let purposes increased. BTL lending represented 13% of total gross mortgage lending in 2014, with gross advances having recovered from its post-crisis trough though still below its 2007 peak. BTL mortgages accounted for 15% of the total outstanding value of UK-resident mortgages as at end-2014 Q4. A buy-to-let mortgage is a mortgage secured against a residential property that will not be occupied by the owner of that property or a relative, but will instead be occupied on the basis of a rental agreement. In 1996 the Association of Residential Letting Agents, the trade body of estate agents dealing with rental properties, along with four lenders set up its first BTL initiative to encourage private individuals to invest in rental property. This market grew steadily and the share of BTL lending in total gross mortgage lending increased until mid-2008, according to data from the Council of Mortgage Lenders (CML).

Overall, gross secured lending was higher in 2014 than in recent years. Within this, the share of gross lending for buy-to-let purposes increased. BTL lending represented 13% of total gross mortgage lending in 2014, with gross advances having recovered from its post-crisis trough though still below its 2007 peak. BTL mortgages accounted for 15% of the total outstanding value of UK-resident mortgages as at end-2014 Q4. A buy-to-let mortgage is a mortgage secured against a residential property that will not be occupied by the owner of that property or a relative, but will instead be occupied on the basis of a rental agreement. In 1996 the Association of Residential Letting Agents, the trade body of estate agents dealing with rental properties, along with four lenders set up its first BTL initiative to encourage private individuals to invest in rental property. This market grew steadily and the share of BTL lending in total gross mortgage lending increased until mid-2008, according to data from the Council of Mortgage Lenders (CML).

After the onset of the financial crisis, gross buy-to-let lending fell more sharply than total mortgage lending. Reflecting discussions with the major UK lenders, the July 2011 Trends in Lending publication noted one reason for this decline in 2008–09 was that the availability of this lending was said to have tightened as some specialist lenders exited this market. Another reason was that wholesale funding markets — often used to fund BTL lending — became impaired.

After the onset of the financial crisis, gross buy-to-let lending fell more sharply than total mortgage lending. Reflecting discussions with the major UK lenders, the July 2011 Trends in Lending publication noted one reason for this decline in 2008–09 was that the availability of this lending was said to have tightened as some specialist lenders exited this market. Another reason was that wholesale funding markets — often used to fund BTL lending — became impaired.

Gross lending for BTL purposes has grown since 2010, reflecting both supply and demand factors, and was £27.4 billion in 2014. Over the past five years the share of total BTL lending in overall mortgage lending has picked up to 15% in 2014 Q4, higher than in the pre-crisis period, according to data from the CML. Data based on the Bank of England and Financial Conduct Authority’s Mortgage Lenders and Administrators Return (MLAR), derived from a different reporting population and definitions of residency, also show that gross BTL lending grew faster than overall gross mortgage lending in recent years. Contacts of the Bank’s network of Agents noted that the rental market had continued to grow strongly in recent months, supporting continued steady growth in buy-to-let activity.

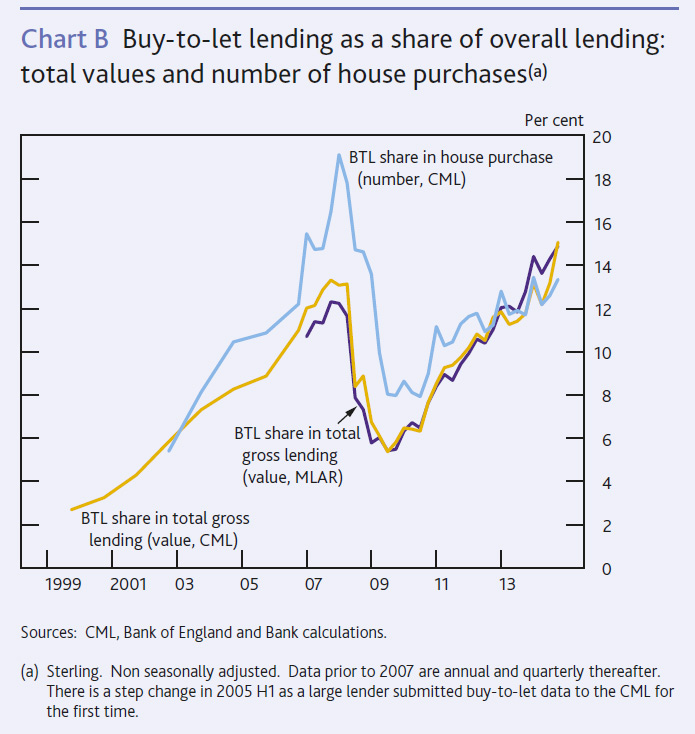

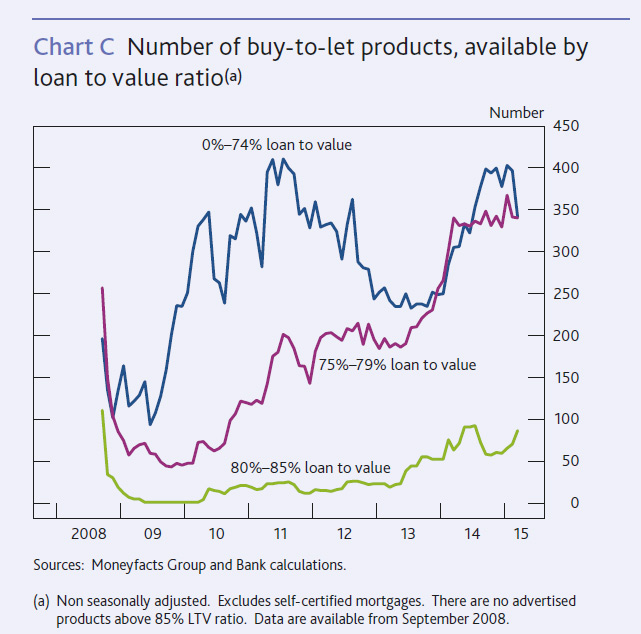

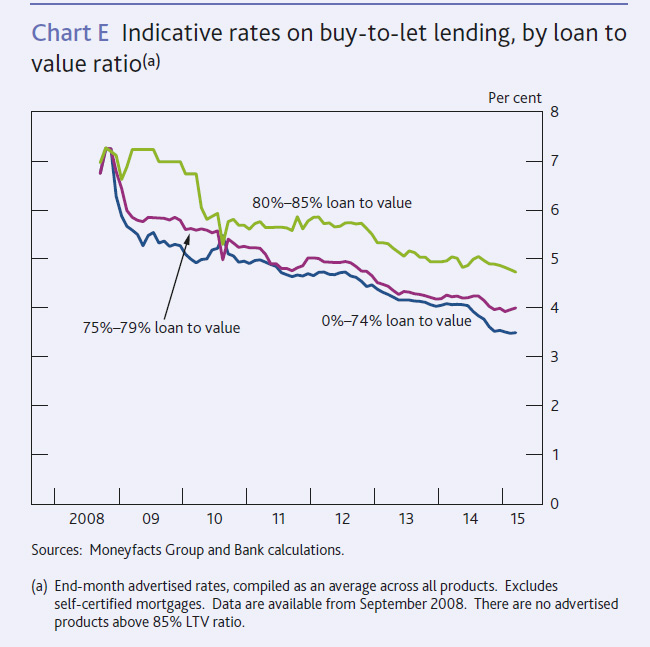

Gross buy-to-let advances for remortgaging have also increased in recent years. Its share of the total grew from 32% in 2002 to 52% in 2014, with the share of gross advances for house purchase at 45%.  The share of the number of BTL mortgages for house purchase in the total number of house purchases has increased from its trough in 2010 to 13% in 2014 though remains below its 2008 peak, according to data from the CML. A significant proportion of advertised BTL mortgage products in the four years after the financial crisis were at loan to value (LTV) ratios below 75%. The number of advertised BTL mortgage products at LTV ratios of 75% and above has increased since mid-2013, but most are below 80% LTV ratio.

The share of the number of BTL mortgages for house purchase in the total number of house purchases has increased from its trough in 2010 to 13% in 2014 though remains below its 2008 peak, according to data from the CML. A significant proportion of advertised BTL mortgage products in the four years after the financial crisis were at loan to value (LTV) ratios below 75%. The number of advertised BTL mortgage products at LTV ratios of 75% and above has increased since mid-2013, but most are below 80% LTV ratio.

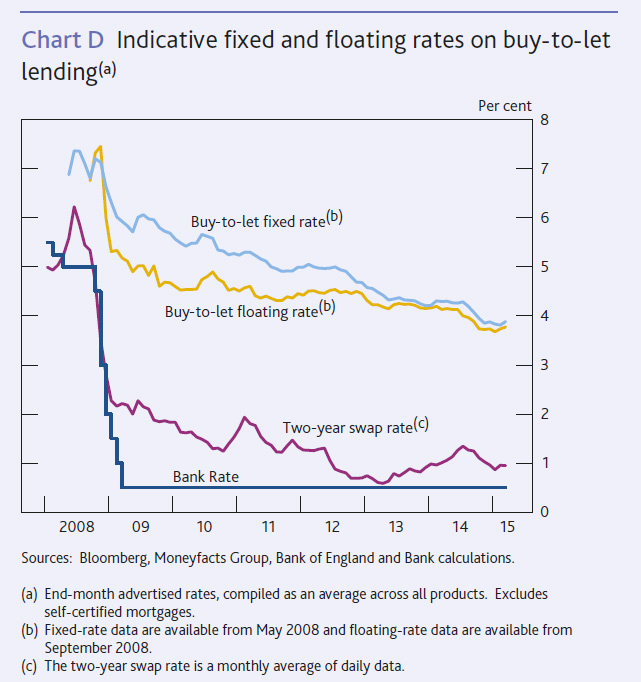

Data on quoted rates for fixed-rate BTL mortgages from Moneyfacts Group indicate that they have fallen since the onset of the financial crisis. This follows the same broad pattern as the aggregate measures of quoted rates on fixed-rate mortgages published by the Bank of England. Spreads over reference rates initially widened on fixed-rate BTL products, as mortgage rates fell by less than swap rates. Since 2013, spreads on these products narrowed as relevant reference rates increased. In recent months, spreads ticked up as fixed BTL rates fell by less than these swap rates. Floating BTL mortgage rates have also decreased since the onset of the financial crisis. The decrease was similar to that for rates on fixed BTL products since 2013. With Bank Rate unchanged, spreads over Bank Rate for floating-rate BTL mortgages have narrowed in recent years. Looking ahead, lenders in the Bank of England’s Credit Conditions Survey expected a reduction in spreads on BTL lending in 2015 Q2. Indicative BTL rates by LTV ratio ranges have also decreased over the years. Rates for LTV ratios below 75% have fallen sharply over the past twelve months.

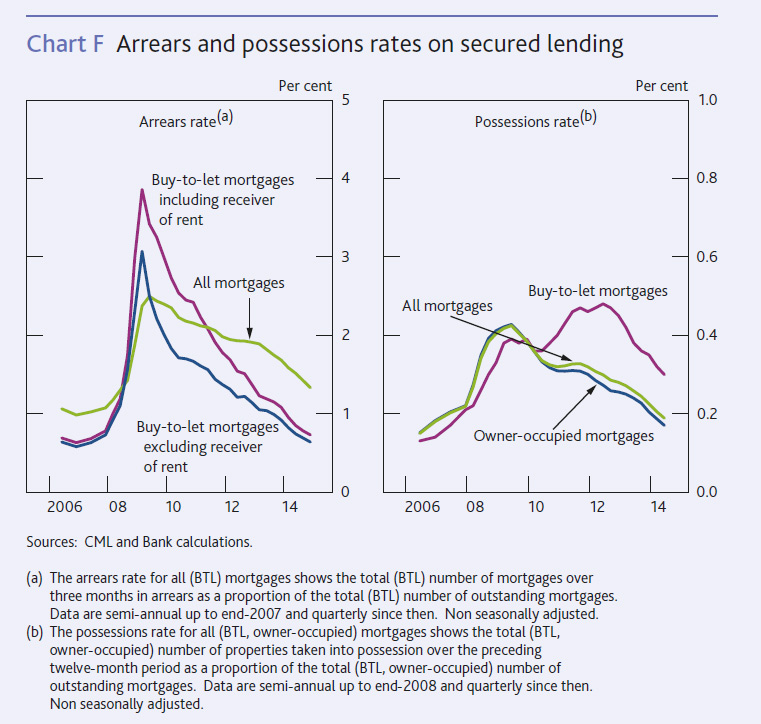

BTL mortgages as a proportion of the total number of outstanding mortgages more than three months in arrears rose sharply at the start of 2009, around the same time as the overall mortgage arrears rate. The BTL arrears rate fell back and has been lower than that for all mortgages in recent years. In some contrast, the possessions rate on BTL mortgages peaked much later than that for owner-occupied mortgages and while it has fallen recently, still remains higher than that for owner-occupiers. But the CML noted that some of the differences in the path of arrears and possession rates seen when comparing the BTL sector with the wider market reflects the use of receivers of rent in the BTL sector. Other things being equal, the use of receivership may have mitigated some increase in reported BTL arrears and possession rates and delayed the increase in reported BTL possessions.

The rate of possession of buy-to-let properties was almost twice as high as for owner-occupied ones, even though the rate of underlying arrears on buy-to-let lending remained lower in 2014, according to data from the CML. They commented that this was because lenders offer extended forbearance to owner-occupiers to help them get through periods of financial difficulty without losing their home.

The rate of possession of buy-to-let properties was almost twice as high as for owner-occupied ones, even though the rate of underlying arrears on buy-to-let lending remained lower in 2014, according to data from the CML. They commented that this was because lenders offer extended forbearance to owner-occupiers to help them get through periods of financial difficulty without losing their home.