Given the current debate about “Unquestionably strong” banks, it is worth reading the Bank of England’s approach to minimum loss-absorbing capacity these institutions must hold, and how it can comprise both ‘going concern’ and ‘gone concern’ resources.

The Bank of England published a Statement of Policy on our approach to setting MREL (a minimum requirement for own funds and eligible liabilities) for UK banks, building societies and the large investment firms on 8 November 2016.

These rules represent one of the last pillars of post-crisis reforms designed to make banks safer and more resilient, and to avoid taxpayer bailouts in future. Banks are now required to hold several times more loss-absorbing resources than they did before the crisis, while annual stress tests check firms’ resilience to severe but plausible shocks. Banks are now also structured in a way that supports resolution. The Bank of England now has the legal powers necessary to manage the failure of a bank, and significant progress has been made to ensure there is coordination between national authorities should a large international bank fail.

The new rules will be introduced in two phases. Banks will be obliged to comply with interim requirements by 2020. From 1 January 2022, the largest UK banks will hold sufficient resources to allow the Bank of England to resolve them in an orderly way.

What is MREL?

MREL is a critical part of a resolution strategy. It determines the minimum loss-absorbing capacity these institutions must hold, and it can comprise both ‘going concern’ and ‘gone concern’ resources.

Going-concern resources, typically in the form of common equity, absorb losses in times of stress and ensure that a bank can keep operating and that it can maintain the supply of credit to the economy.

Gone-concern resources, typically in the form of debt, absorb losses when a bank undergoes resolution or is placed into insolvency.

Smaller institutions that provide banking activities of a scale that means that they can be allowed to go into insolvency if they fail, will satisfy MREL by simply meeting their minimum regulatory capital requirements as a going concern. There is no gone-concern requirement for these firms. More detail on the capital framework for bank capital is set out in the Supplement to the December 2015 Financial Stability Report.

But larger banks and building societies with a size or functions that mean they have a resolution plan involving the use of the Bank’s resolution tools will be required to hold additional MREL beyond their going-concern requirements.

In addition, firms are expected to hold going-concern capital buffers on top of these requirements. The buffers are calibrated to recognise systemic importance or idiosyncratic exposures, and are intended to be used so that banks can absorb losses without breaching minimum requirements. As these capital buffers are not permitted to count towards meeting MREL, they add to the total loss-absorbing capacity of each bank.

How much MREL must larger firms hold?

The MREL for large firms is needed in a resolution both to absorb losses and to recapitalise their continuing business. Our policy is that from 1 January 2022 they should be required to hold both their going-concern requirements together with additional MREL of an amount equal to those going concern requirements. In other words, their MREL will be two times their going-concern requirements.

These UK firms will become subject to interim requirements on 1 January 2020, prior to the final requirements coming into force in 2022. We will review our approach to calibration of the 2022 MREL for all firms before the end of 2020, before we set final MRELs. In doing so, we will have particular regard to any intervening changes in the UK regulatory framework, as well as institutions’ experience in issuing liabilities to meet their interim MRELs.

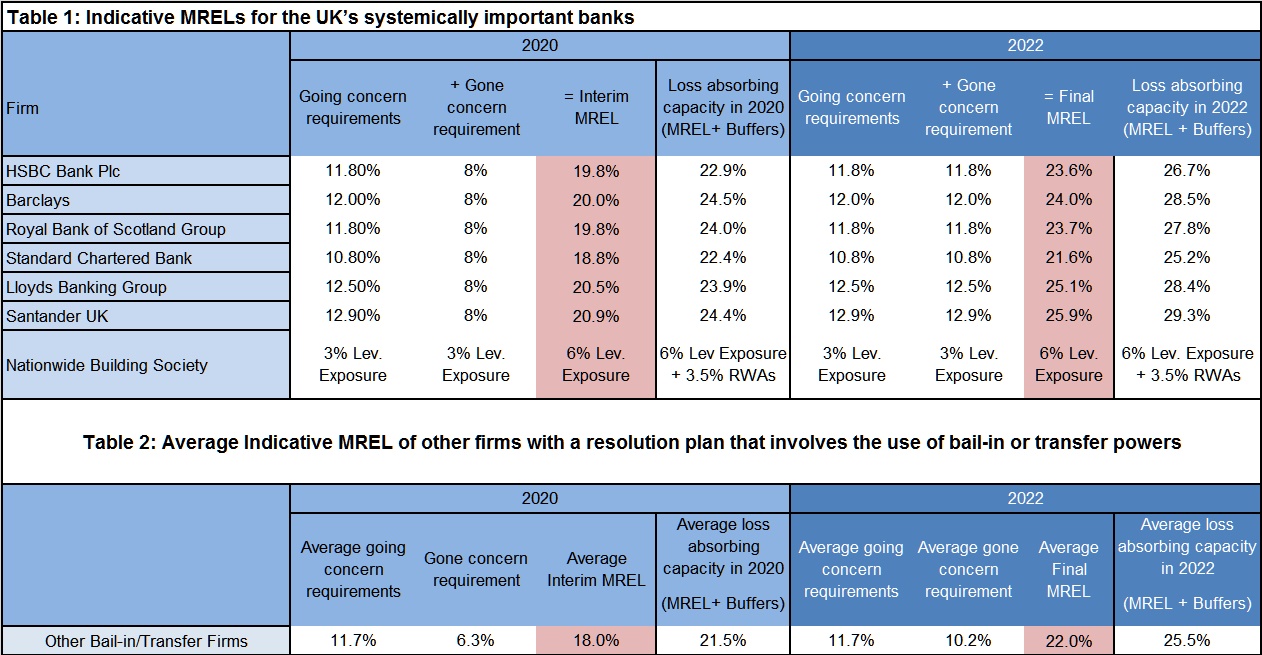

Table 1 below provides the estimates of the interim and final consolidated MREL requirements that we have sent to each of the UK’s global and domestic systemically important banks. As a firm’s MREL will depend upon its going concern requirements in a particular year, these 2020 and 2022 MRELs are simply indicative and are based on the calibration methodology set out in our Statement of Policy, with reference to the firms’ minimum capital requirements and balance sheets as at December 2016.

In addition to the global and domestic systemically important UK banks, there are eight other UK banks and building societies that currently have a resolution plan that involves the use of resolution tools by the Bank (rather than reliance on the insolvency regime). These are:

- Clydesdale Bank

- The Co-operative Bank

- Coventry Building Society

- Metro Bank

- Skipton Building Society

- Tesco Bank

- Virgin Money

- Yorkshire Building Society.

Table 2 provides the average of the indicative 2020 and 2022 MRELs and total requirements for these other firms.

We have provided an average for these firms as publishing MRELs for each of them would also reveal the firm-specific element of their capital assessments, many of which have not previously been disclosed. Accordingly, the Prudential Regulation Authority will consider its disclosure policy and undertake the appropriate consultations before a final decision on publishing individual MRELs for these firms is taken.

The Co-operative Bank has been excluded from the calculation of the average because the firm is currently seeking a sale, which has the potential to significantly affect The Co-operative Bank’s balance sheet. Therefore an indicative MREL based on The Co-op’s balance sheet today may not be a useful guide to the eventual requirement.

One thought on “UK Minimum requirements for eligible liabilities and own funds (MREL)”