A working paper from the BIS – “Effectiveness of unconventional monetary policies in a low interest rate environment” examines the connection between low interest rates and unconventional monetary policy, and their findings suggest the “neutral” rate is likely to rise much faster than many are currently expecting, with significant potential economic impact. Indeed, Central Banks are “behind the curve” and that the assumed lower “neutral interest rate may in fact be wrong.

A reliance on balance sheet tools can, for example, result in resource misallocations, disruptive risk-taking behaviour and political economy challenges. These costs, among others, would have to be weighed against the benefits when considering the appropriate role for central bank balance sheets in the new normal era as well as in future crisis periods.

They suggest that unconventional monetary policies (UMPs) became less effective in the post-GFC period, but not for the reasons typically given. The explanation is nuanced and emerges from careful assessment of the various links in the monetary transmission mechanism.

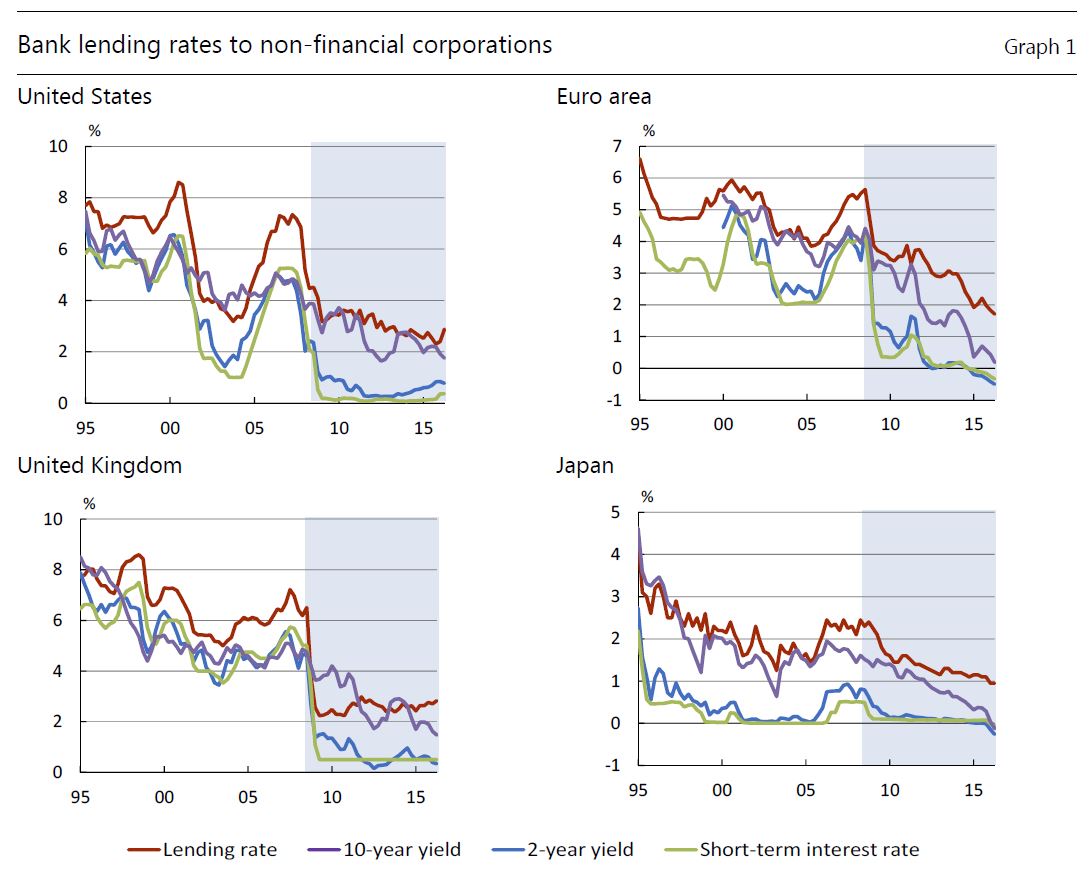

Post the GFC, major central banks in advanced economies cut policy rates sharply and, then when the room for manoeuvre closed, resorting to a range of unconventional monetary policies (UMPs) that exploited the financial firepower of central bank balance sheets. The lacklustre recovery that followed has naturally raised questions about the effectiveness of these new tools. This paper uses extensive modelling to investigate the links, and the results are troubling. Not least, they find evidence supporting the hypothesis that the economy did not become less interest-sensitive in the aftermath of the GFC, once changes in the “natural” rate of interest are taken into account. They conclude that UMPs had a declining impact on economies over time. Looking forward, the results suggest that the normalisation of balance sheet policies could be accompanied by an increase in the conventionally estimated “natural” rate, which if not taken into account would increase the risk that central banks will find themselves falling behind the curve.

They conclude:

We find that unconventional monetary policies were effective in providing some stimulus to economies at the perceived lower bound for policy rates. The responsiveness of the economy to private sector interest rates remained remarkably stable in our sample. However, it must also be noted that the overall effectiveness fell for two key reasons. First, the “bang for the buck” of central bank balance sheet stimulus declined over time. Larger and larger programmes were necessary to achieve a given change in sovereign yields. Second, the “natural” rate tended to decline with (unexpected) expansionary unconventional monetary policies. This suggests that monetary policy decisions have influenced the perceived “natural” rate, contrary to what is implied by the conventional wisdom. This correlation may also help to explain why monetary policy appears to have had been less stimulative than expected in the past decade, and may indicate that monetary policy could prove to be more stimulative than expected during the normalisation with no change in the conventional wisdom.

Note: BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS.