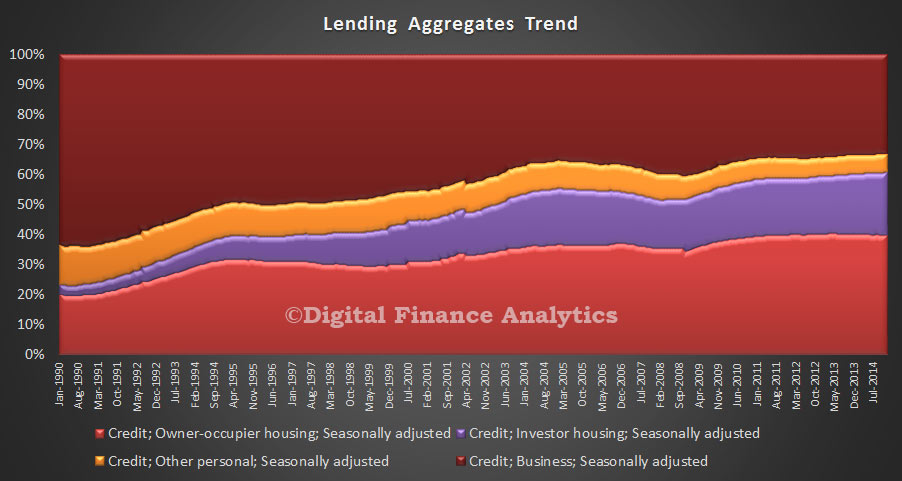

Today the data from RBA and APRA showed the strength of lending in the housing sector, and only 33% of lending is business related. This over-emphasis on property investment in particular is a systemic problem, and must be addressed if we are to drive growth in the right direction. Business needs more focus.

To illustrate the point, the mix between business lending and housing (both owner occupied and investment) is worth examining from 1990 onwards. Back then, business lending accounted for about 65% of all lending. Today it is 33%. As a result we know from our SME surveys that many businesses are finding it difficult to get funding on reasonable terms. On the other hand, we see lending for housing, and especially investment lending inflating the banks balance sheets and house prices, but this is not truly productive.

To illustrate the point, the mix between business lending and housing (both owner occupied and investment) is worth examining from 1990 onwards. Back then, business lending accounted for about 65% of all lending. Today it is 33%. As a result we know from our SME surveys that many businesses are finding it difficult to get funding on reasonable terms. On the other hand, we see lending for housing, and especially investment lending inflating the banks balance sheets and house prices, but this is not truly productive.

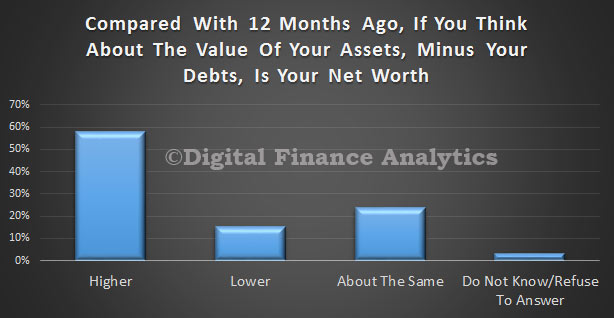

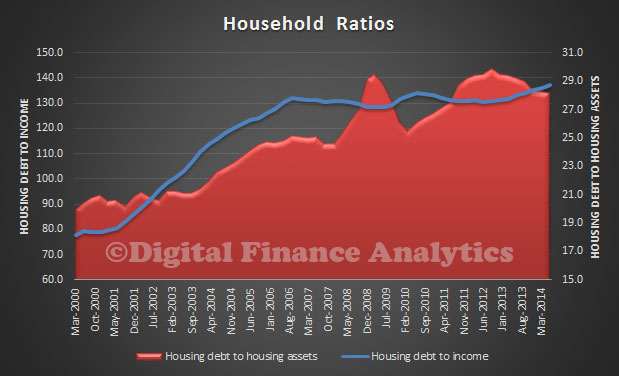

Its time to impose additional controls on investment lending, and to re-balance lending towards businesses who will be able to generate real economic growth for the country. The current situation, where household net worth grows…

… thanks to over-high house prices is not sustainable when it is powered by ever more household debt.

… thanks to over-high house prices is not sustainable when it is powered by ever more household debt.

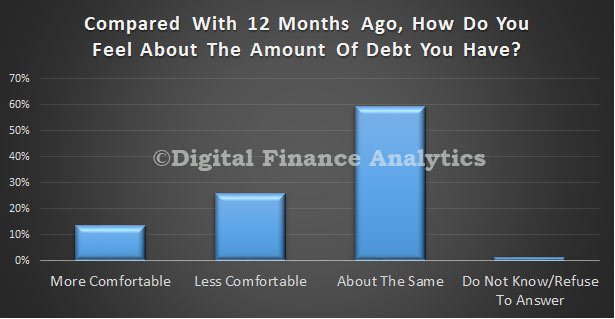

From our surveys, a quarter of households are less comfortable with the amount of debt they have compared with 12 months ago.

Any further interest rate cuts without these measures would be irresponsible.

Any further interest rate cuts without these measures would be irresponsible.