The ANZ Net Interest Margin (NIM), reported last week was 1.99%, and typically banks in Australia are achieving a NIM slightly above this. So, it was interesting to see this note from Moody’s, discussing the NIM of US banks, which has risen to 3.21%, and continues a positive trend over the past year.

Last week, US banks’ reported third-quarter earnings and higher net interest margins (NIM), a credit positive because NIM is a key driver for net interest income, which accounts for more than half of most banks’ net revenue.

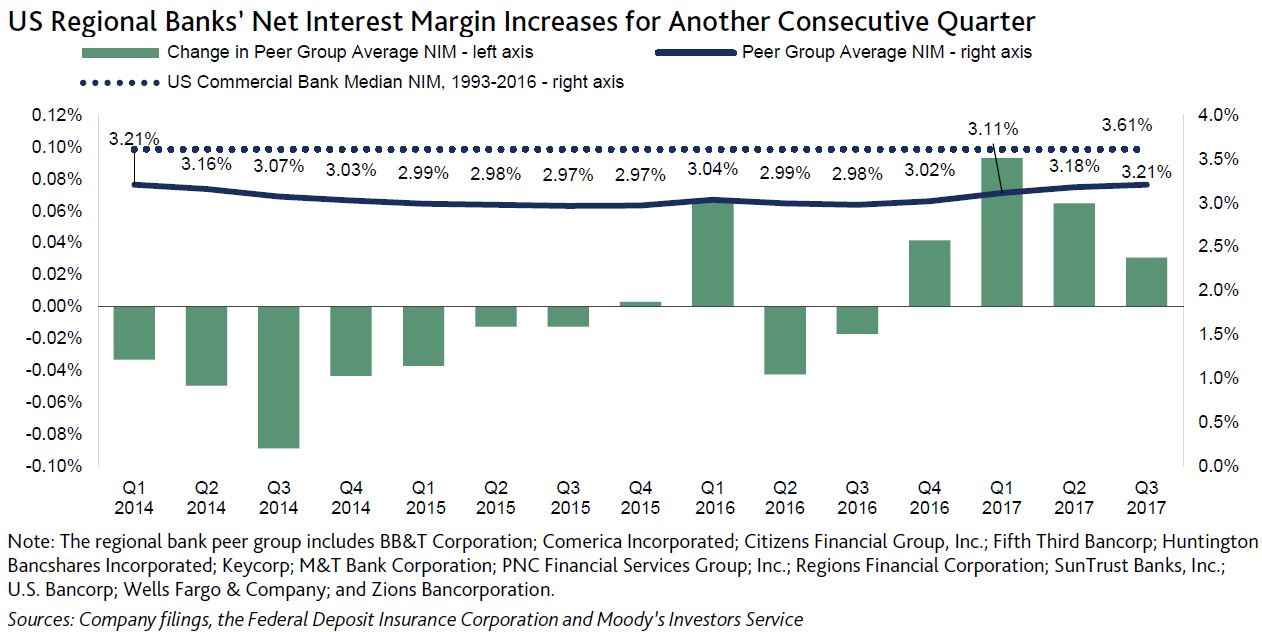

Quarter over quarter, the average NIM for the largest US regional banks increased three basis points (Exhibit 1) to 3.21% from 3.18%, continuing a four-quarter positive trend. However, the rate of improvement is slowing. The Federal Funds rate increased 25 basis point (bp) in each of the past three quarters. However, as the bars show, the rate of improvement for listed regional banks’ average NIM has declined each quarter.

Accelerating deposit costs explain why the NIM is not increasing at a consistent rate with each 25 bp increase in the Federal Funds rate. Exhibit 2 shows deposit betas for total deposits (interest-bearing and noninterest-bearing) for each of the past three quarters. Deposit beta is the increase in cost of deposits relative to the increase in the Federal Funds rate. There was a significant step up in beta in the second quarter, which continued in the third quarter. In their earnings calls, most bank managements indicated that retail deposits are not repricing upward, despite the rise in market interest rates. This is not the case with deposits from the banks’ wealth management clients, and especially from their commercial clients, which are both more price sensitive.