Moody’s says following the US Federal Reserve raise of its short-term interest rate by 25 basis points, the first time the Fed has increased the rate since December 2015, when it was raised to 0.25% from 0%, where it had been for seven years. Although the increase is small, the Fed’s decision is credit positive for housing finance agencies (HFAs) in aggregate because higher interest rates boost their investment earnings, drive profit margins and present opportunities to grow loan portfolios and rebuild balance sheets.

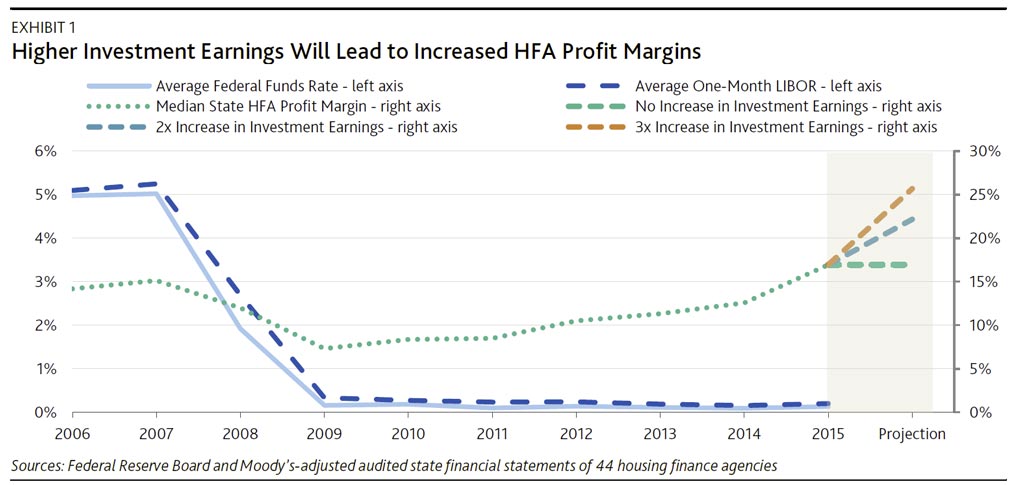

As of fiscal year-end 2015, roughly 7.2% of HFAs’ assets were held in cash and cash equivalents, which will immediately benefit from the rate increase and boost investment earnings. Historically, HFA profitability has closely tracked investment earnings. Between 2007 and 2009, the steep drop in interest rates led to a decline in HFA profitability. Since then, low interest rates have curtailed profits, although HFA earnings have recovered owing to selling mortgage-backed securities in the secondary market and savings from bond refundings. Now, profit margins should expand with the higher interest rates boosting investment earnings. We project that HFA sector-wide profit margins will increase by 5% if investment income doubles from 2015 levels and by 9% if investment income triples (see Exhibit 1). Actual results will vary among the HFAs.

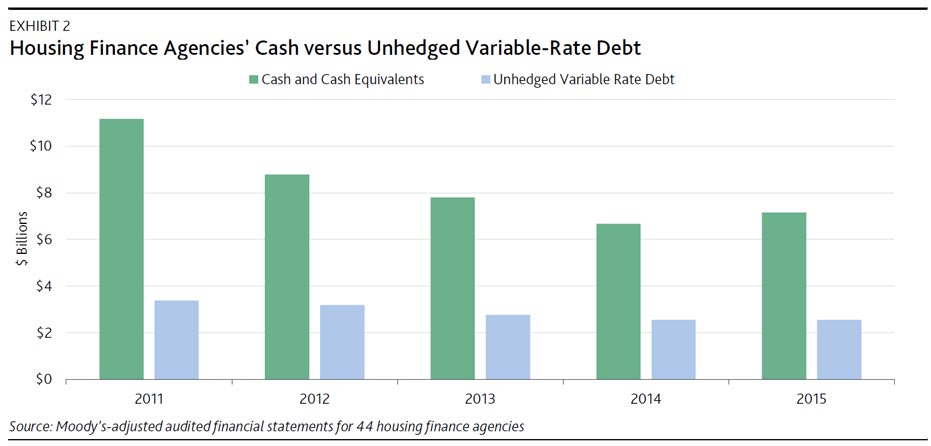

As interest rates rise, HFAs will be challenged by higher interest expense on both their hedged and unhedged variable-rate debt. However, increased investment earnings on cash held by HFAs combined with the interest rate swaps on the hedged variable rate debt will alleviate the effect of the higher interest costs. HFAs can also use cash to redeem unhedged variable-rate bonds if interest rates become too high. As Exhibit 2 shows, the cash and cash equivalents that HFAs had at fiscal year-end 2015 were equal to 2.7x the amount of unhedged variable-rate debt. Higher interest rates also mean HFAs’ swap termination costs will decline, allowing HFAs to terminate swaps more economically.

An increase in mortgage rates (close to 6% or higher) would also allow HFAs to grow their loan portfolios. Although mortgage rates are not immediately affected by short-term interest rates, changes affect long-term mortgage rates. Demand for HFA mortgages is driven by the attractiveness of rates on HFA loans relative to those on conventional mortgages. With rates on conventional mortgages so low, HFAs have found it difficult to originate loans over the past seven years. With an increase in interest rates, fewer borrowers could obtain a mortgage from a conventional lender at a lower rate than from an HFA. Higher loan originations, coupled with issuance of tax-exempt bonds, would rebuild HFA balance sheets. In the past few years, HFAs have financed loans primarily through selling mortgage-backed securities in the secondary market rather than bond financing.