Comparatively thin high-yield bond spreads complement an increased willingness by banks to supply credit to businesses. The increased willingness to make business loans owes much to a benign outlook for defaults.

According to the Fed’s latest survey of senior bank loan officers, the net percent of banks tightening business — or commercial & industrial (C&I) — loan standards dipped from the +2.2 percentage point average of the four-quarters-ending with Q2- 2017 to the -3.9 points of Q3-2017. Moreover, the net percent of banks widening interest-rate spreads on new business loans plunged from the -7.9 percentage point average of the year-ended Q2-2017 to Q3-2017’s -21.1 points.

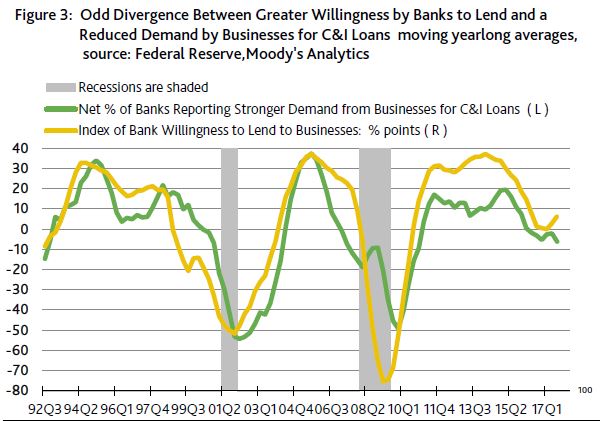

Though banks are more willing to lend to businesses, the business sector’s demand for C&I loans has receded. The same Fed survey of senior bank loan officers also found that the net percent of banks reporting a stronger demand for C&I loans from business customers sank from the -2.1 percentage-point average of the year-ended June 2017 to Q3-2017’s -11.8 points, which was the lowest quarter-long score since Q4-2011’s -15.7 points. However, Q4-2011’s reading followed a string of strong results as shown by the +14.9-point average of yearlong 2011.

By contrast, as of Q3-2017, the yearlong average of the net percent of banks reporting a stronger demand for C&I loans from business customers dropped to -6.2 points for its lowest such average since the -9.5 points of yearlong 2010. (Figure 3.)

Business borrowing says cycle upturn is past its prime

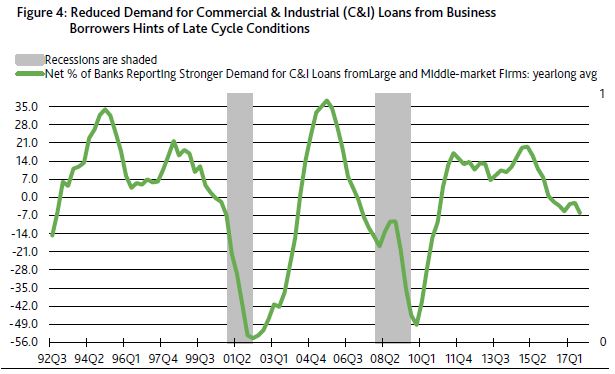

It is worth noting how the latest slide by the business-sector’s demand for C&I loans has occurred more than four years following a recession. In the context of a mature business cycle upturn, the yearlong average of the net percent of banks reporting a stronger demand for C&I loans previously sank to the -6.2 points of the span-ended Q3-2017 in Q2-2007 and Q4-2000.

Recessions materialized within 12 months of the previous two comparable drops by the business sector’s demand for bank credit. Granted the US may stay clear of a recession well into 2018, but the reality is that the current business cycle upturn is showing signs of age. Thus, the upside for interest rates is limited, especially if the annual, or year-to-year, rate of core PCE price index inflation stays under 2%. (Figure 4.)

A pronounced slowing by the annual growth rate of outstanding bank C&I loans from Q2-2016’s 10.2% surge to Q2-2017’s 2.2% rise is in keeping with a softer demand for C&I loans by business borrowers. However, the pace of newly rated bank loan programs from high-yield issuers tells a much different story.

After surging by 140.2% in Q1-2017 from Q1-2016’s depressed pace, the annual increase of new high-yield bank loan programs slowed to 2.1% in Q2-2017. Nonetheless, recent activity suggests the year-over-year growth rate for new high-yield bank loan programs will accelerate to roughly 16% during 2017’s third quarter. Support for this view comes from July 2017’s $52.4 billion of new bank loan programs from high-yield issuers that more than doubled the $24.1 billion of July 2016.

Lately, the growth of high-yield bank loan programs has been powered by refinancings of outstanding debt and the funding of acquisitions. Today’s relative ease of refinancing outstanding debt at easier terms highlights ample systemic liquidity, which will help suppress the incidence of default. Abundant liquidity also facilitates the take-over of weaker, default prone businesses by financially stronger entities. (Figure 5.)