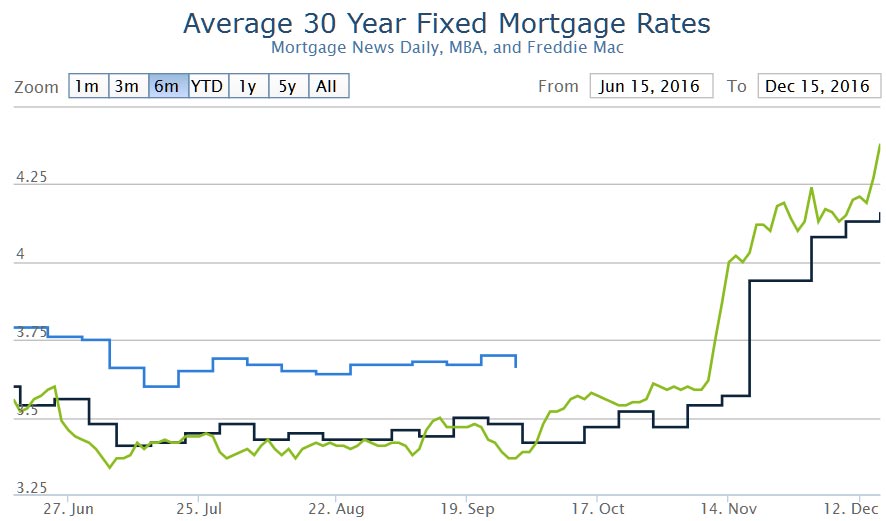

Don’t believe anything you read about mortgage rates today… well, except this. In fact, you’re welcome to believe anything you read as long as it acknowledges the fact that rates have risen nearly a quarter of a point from last week, pushing them well into the highest levels in more than 2 years. The average top tier conventional 30yr fixed rate is quickly approaching 4.5%. Nearly every lender that was at 4.125% last week is now at 4.375%. Lenders who were at 4.25% last week are mostly up to 4.5%.

The overall spike in rates since the election is now on par with the 2013 taper tantrum. You’ll hear time and again “don’t worry… rates are historically low…” and my personal favorite “for every .125% in rate, the payment only rises $7 per $100k borrowed.” All of that is true, except perhaps for the “don’t worry” part. Some borrowers may need to worry about no longer qualifying due to debt-to-income guidelines.

Rates haven’t risen a mere .125%, after all. That’s just today’s increase. Added to recent losses, the damage is between .75 and 1.0% now. Let’s take a more average loan amount of $250k and see what happens when the rate goes up 0.75. The increase is over a hundred dollars a month.

Many of the people interviewed by financial journalists have a hard time relating to most of the people that will end up being exposed to their opinions. $100/month may not sound like the end of the world to the CEO of some financial firm, but it is more than enough to tip the scales for prospective homebuyers. They’ll have to adjust their price range at least $20k to get back to the same payment. If that’s not an option for the area, then they’re no longer a prospective homebuyer, or they’ll be forced to move out of the area. This dynamic is not congruent with “not worrying.”

Oh, and you’ll also need to worry if rates will continue to move higher. That’s possible, although for technical reasons, the higher rates go, the more challenging it will be to continue higher. It’s also possible that markets are riding on a cloud of optimistic euphoria and that the cloud will dissipate as the new year begins. It’s possible this rise in rates is a necessary ingredient in longer term trends. In other words, rates have to rise so they can fall again. Last but not least, it’s possible I don’t know everything and rates will go much higher than they are currently, but if that happens, it will increasingly have consequences for the economy.