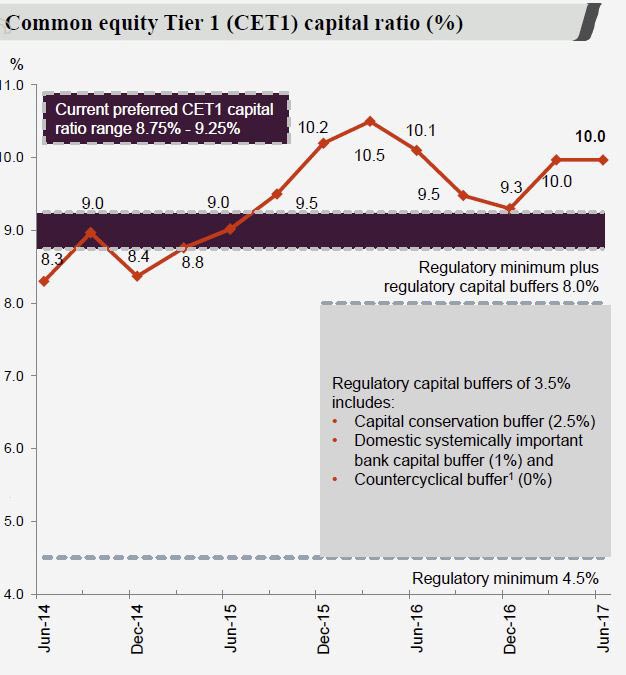

Westpac released their Q3 Capital update today. The CET1 ratio was 10% at 30 June 2017, and equivalent to 15.3% on a comparable international basis. This is higher than expected helped by strong dividend reinvestment. They said they would provide further guidance on their preferred CET1 range (8.75%-9.25%) once APRA finalises its capital adequacy framework review.

The Net table funding ratio was 108% and the liquidity coverage ratio was 128%. The bank is well placed on these key ratios.

The Net table funding ratio was 108% and the liquidity coverage ratio was 128%. The bank is well placed on these key ratios.

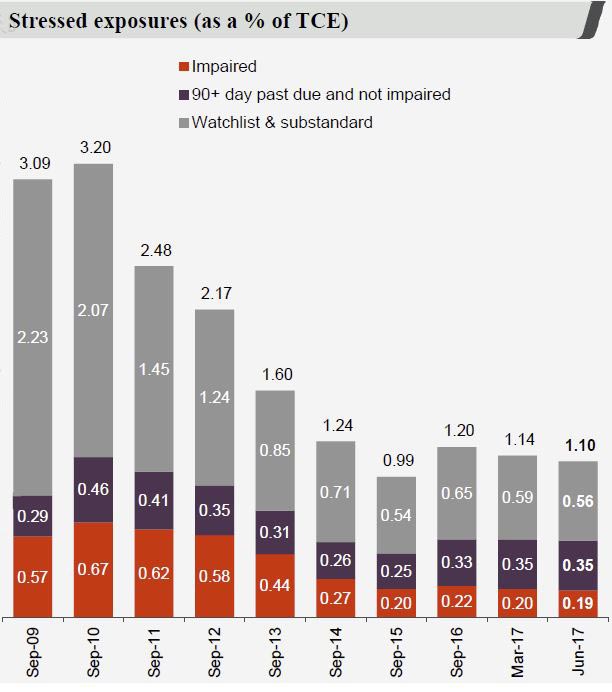

Stressed exposures TCE decreased by 4 basis points to 1.10%. Most sectors, including commercial property, mining and New Zealand dairy improved.

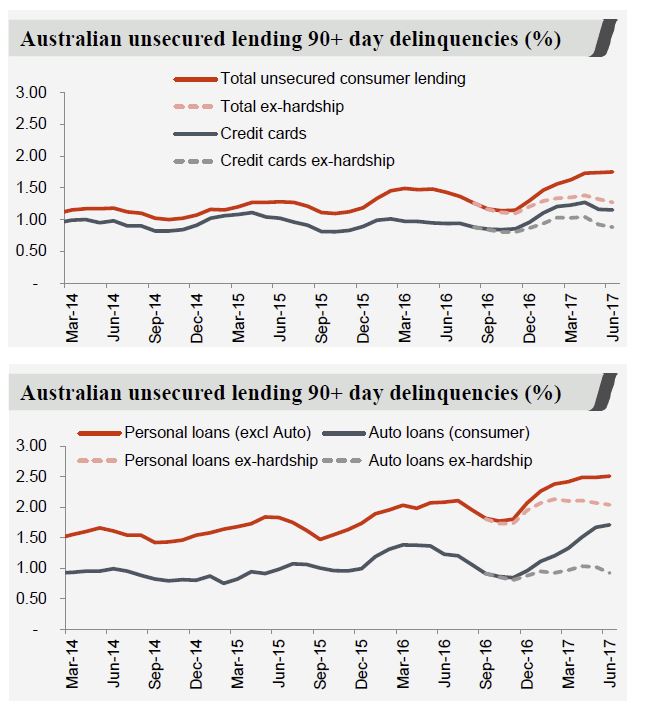

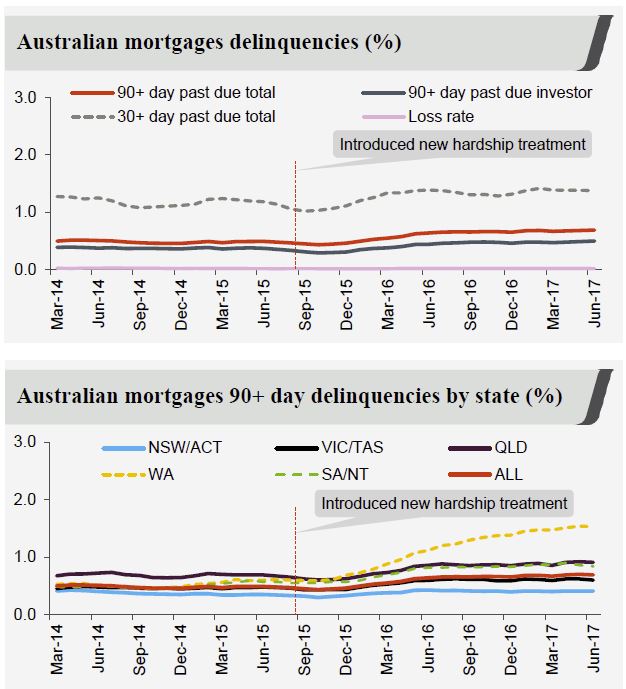

Unsecured delinquencies rose in the quarter, up 12 basis points to 1.75% mostly due to APRA hardship reporting changes. Changes in the reporting of hardship have had an impact on the level of reported delinquencies, with mortgage 90+ day up 16 basis points and unsecured consumer lending the change lifted 90+ day by 49 basis points. Cyclone Debbie caused a further rise.

Unsecured delinquencies rose in the quarter, up 12 basis points to 1.75% mostly due to APRA hardship reporting changes. Changes in the reporting of hardship have had an impact on the level of reported delinquencies, with mortgage 90+ day up 16 basis points and unsecured consumer lending the change lifted 90+ day by 49 basis points. Cyclone Debbie caused a further rise.

30+ day delinquencies were at 138 basis points, compared with 139 in March, and 130 in Sept 16. 90+ delinquencies were 69 basis points, compared with 67 in March.

30+ day delinquencies were at 138 basis points, compared with 139 in March, and 130 in Sept 16. 90+ delinquencies were 69 basis points, compared with 67 in March.  The number of properties in possession rose from 382 to 422, mainly due to a rise in WA and QLD. The WA trend is visible, thanks to weaker economic conditions. Actual losses for the 9 months was a low $57 million.

The number of properties in possession rose from 382 to 422, mainly due to a rise in WA and QLD. The WA trend is visible, thanks to weaker economic conditions. Actual losses for the 9 months was a low $57 million.

Westpac provided further details of the changes in their mortgage book, thanks to the regulatory intervention on IO loans. IO loans are at least 50 basis points higher than the equivalent P&I loan. Investment loans are at least 47 basis points higher than the equivalent OO loan.

They have imposed a maximum LVR of 80% for all new IO loans (including limit increases, term extensions and switches. They are no longer accepting external refinances from other financial institutions for OO IO. There are no fees to switch from IO to P&I.

They have imposed a maximum LVR of 80% for all new IO loans (including limit increases, term extensions and switches. They are no longer accepting external refinances from other financial institutions for OO IO. There are no fees to switch from IO to P&I.

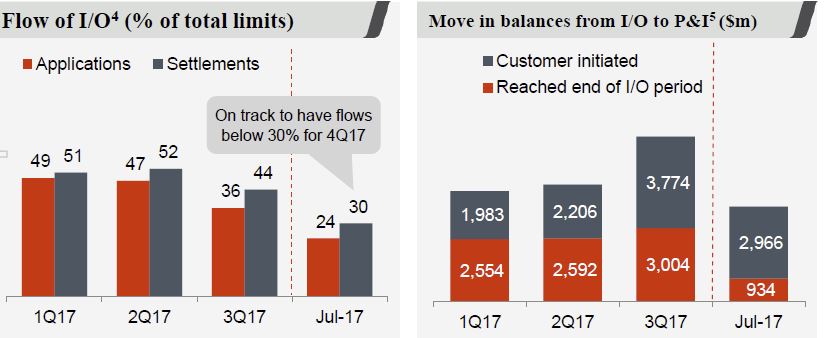

The say the flow of IO lending was 44% in 3Q17, with applications 36% of flows (down from 52% and 47% in 2Q17). Despite seeing settlements above 30% IO, currently, they say they should be below 30% by 4Q17 – September 17.

The 30% IO cap incorporates all new IO loans, including bridging finance, construction loans, lines of credit as well as limit increases on existing loans. The IO cap excludes flows from switching between repayment types, such as IO to P&I or from P&I to IO and also excludes term extensions of IO terms within product maximums (5 years for IO OO and 10 years for investor loans).

The 30% IO cap incorporates all new IO loans, including bridging finance, construction loans, lines of credit as well as limit increases on existing loans. The IO cap excludes flows from switching between repayment types, such as IO to P&I or from P&I to IO and also excludes term extensions of IO terms within product maximums (5 years for IO OO and 10 years for investor loans).

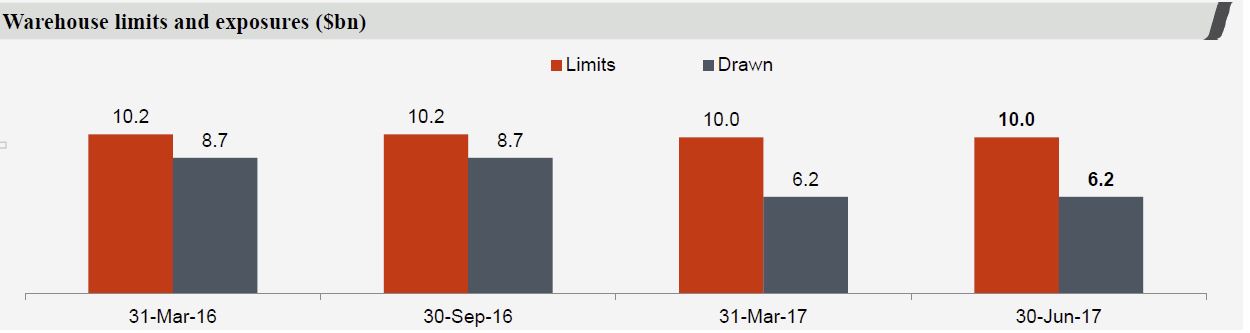

They also described their mortgage warehouse, with Westpac providing funding for over 20 Australian mortgage originators (both ADI and non-ADI). The bank’s warehouse limits have been stable at around $10bn, but asset balances have been more variable.