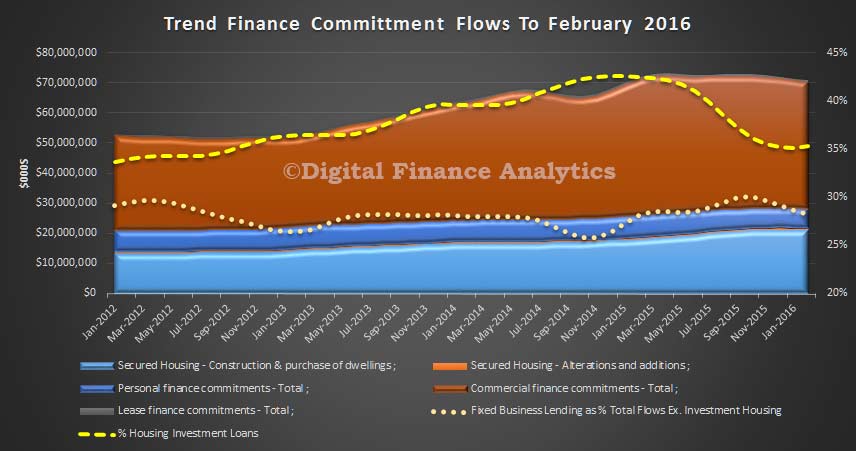

The ABS data on lending finance was issued on Wednesday, and the seasonally adjusted numbers caught the headlines. Housing finance was up 1.7% month on month, and commercial finance was up 5.6%. However, the seasonally adjusted numbers have lots of noise in the data, we we think they obscure what is really going on. So, first we look at the trend data. Overall credit flows fell by 0.9% in the month. Within that secured housing fell 0.6%, whilst secured lending for alternations and additions rose 0.5%. Revolving credit (mainly credit cards) fell 1.7% as households continues to pay off the Christmas binge, but fixed loans rose 0.5%. Commercial fixed loans (which include housing investment loans), fell 1.6%. However, the value of housing investment loans were line ball from last month, so the fall was from other commercial sectors, which is not good.

As a result, we see from the summary chart that the proportion of fix commercial lending NET of housing investment fell, from 28.7% to 28.2%, so in trend terms, lending for commercial purposes continued to fall. Assuming that lending is correlated to prospective economic growth, this is bad news.

On the other hand, lending for investment housing was still very present, and lifted to 35.3% of all secured housing loans. Investment lending still has momentum. Also, now we are seeing more households deciding to stay put and renovate. We expect lending demand for renovations to be strong in coming months.

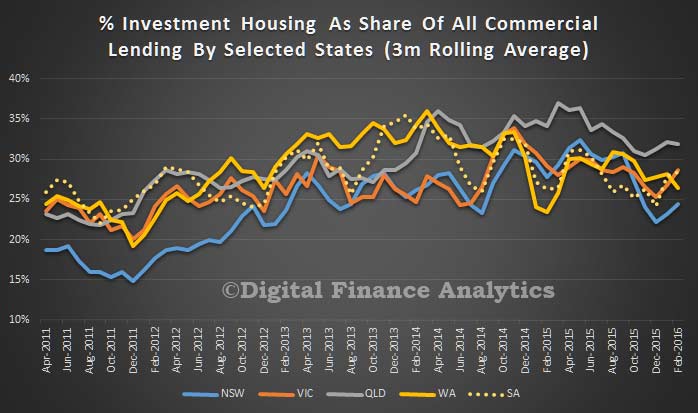

The other piece of data which is important is the state lending footprint. Some made much of the apparent fall in investment lending in NSW, but taking the original data (there are no trend or seasonally adjusted series), and using a rolling average over 3 months, we see a different story. The best way to look at this is to compare lending for investment housing (sum of new construction and purchase of existing dwellings for rental), compared with all commercial lending. When we look at the series, we do see a small fall in NSW, though with an upward inflection in the latest data. But we see that NSW has a lower relative share of housing investment loans compared with QLD and WA. In fact relatively there has been a greater proportion of investment loans written in these states for since 2011. VIC is also lower, though above NSW. So, the story about the great fall in housing investment momentum in NSW is over done. On the other hand, we should be more concerned about the ongoing investment momentum in QLD and WA, where house prices are set to ease, and mining re-balancing is most at work. We think the risks are higher here.

We are still not seeing sustained commercial investments which are required to drive true economic growth. Housing is still doing too much of the heavy lifting, with household debt as high as it has ever been.

We are still not seeing sustained commercial investments which are required to drive true economic growth. Housing is still doing too much of the heavy lifting, with household debt as high as it has ever been.