From St. Louis Fed, On The Economy Blog.

It seems natural that capital would flow into countries with higher capital productivity and economic growth. A recent Economic Synopses essay, however, explores why capital doesn’t always flow to the highest growth regions.

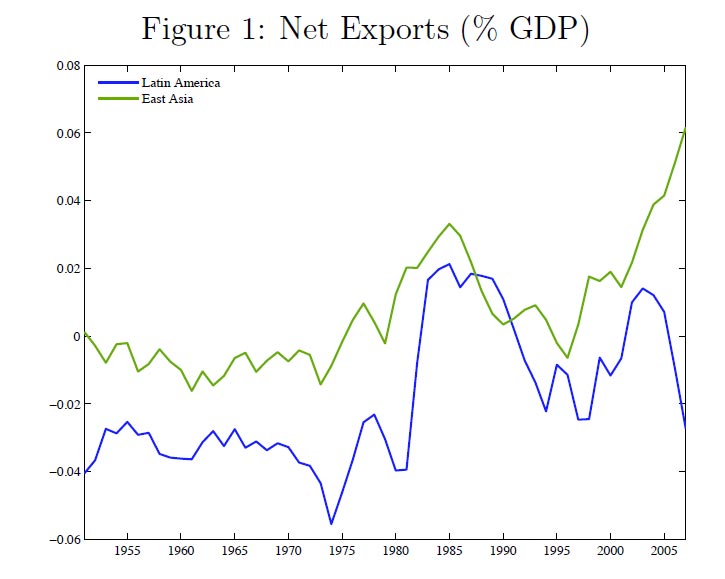

The Case of Latin America and East Asia

Economist Paulina Restrepo-Echavarria and her co-authors1 used capital flows to East Asia and Latin America following World War II as an example. Economic growth and capital productivity were quite high for East Asian countries during this period, yet little investment flowed into the region.

Conversely, Latin America received substantial capital despite neither capital productivity nor economic growth being high. The authors wrote: “In fact, Latin American economic growth substantially lagged behind the economic growth of virtually all other countries in Western and Northern Europe, the Asian Tigers and North America during this period.” (For figures showing these trends, see the essay “The Direction of Capital Flows.”)

International Capital Market Imperfections

Restrepo-Echavarria and her co-authors noted two reasons why capital doesn’t always flow to high-growth areas. The first is that international capital market imperfections, such as capital controls, and other impediments to international transactions prevented capital from flowing into high-growth regions. Put another way, local controls—such as tariffs, taxes, laws and quantity restrictions—prevented or discouraged capital from flowing into these high-growth regions.

The authors explained that, under this belief, more capital would have flowed to these regions had international capital markets been more open.

Domestic Imperfections

The other possibility given by Restrepo-Echavarria and her co-authors was that domestic imperfections, specifically domestic capital market distortions, played a role in preventing inflows of capital to high-growth regions.

The authors wrote: “So, for example, for the domestic (East Asian) capital market, credit controls, interest controls, privatization of banks, entry barriers to banking, and bank reserves and requirements, among others, kept international capital from flowing into East Asia.”

International Vs. Domestic Distortions

The authors turned to their working paper, “Bad Investments and Missed Opportunities? Postwar Capital Flows to Asia and Latin America,”2 for insight to some of the economic forces driving these flows.

They found that domestic distortions played a much larger role in accounting for international capital flows, though both international and domestic imperfections played significant roles. They also found that international capital market distortions have continued to play a role despite many countries liberalizing their international capital markets over time.

Restrepo-Echavarria and her co-authors concluded: “This ongoing distortion partly reflects the legacy of accumulated international capital market distortions over time. Thus, even if international capital market imperfections are ultimately removed, their history can continue to have very large impacts into the future.”

Notes and References

1 Restrepo-Echavarria’s co-authors were Lee Ohanian of UCLA and Mark L.J. Wright of the Federal Reserve Bank of Chicago.

2 Ohanian, Lee E.; Restrepo-Echavarria, Paulina and Wright, Mark L.J. “Bad Investments and Missed Opportunities? Postwar Capital Flows to Asia and Latin America.” NBER Working Paper No. 21744, National Bureau of Economic Research, November 2015.

Additional Resources

- Economic Synopses: The Direction of Capital Flows

- Working Paper: Bad Investments and Missed Opportunities? Postwar Capital Flows to Asia and Latin America

- On the Economy: China’s Currency and Net International Income Flow