There is a rising chorus demanding that APRA loosen their rules for mortgage lending in the face of slipping home prices. This despite the RBA’s recent comments about the risks in the system, especially relating to investor and interest only loans. But this is unlikely, and in fact more tightening, either by a rate rise, or macroprudential will be needed to contain the risks in the system. The latter is more likely.

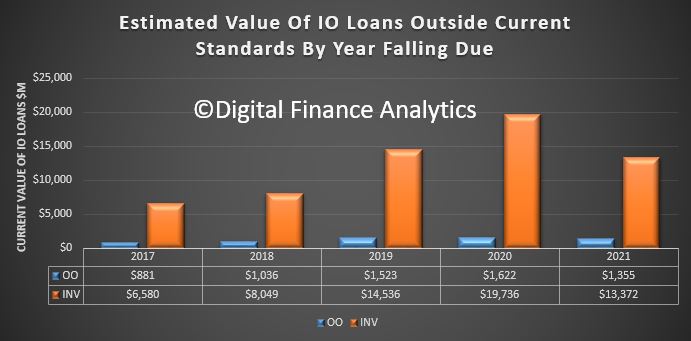

Some of this will come from the lenders directly. For example, last week ANZ said it will be regarding all interest-only loan renewals as credit critical event requiring full income verification from 5 March. If loans failed this assessment these loans would revert to P&I loans (with of course higher repayment terms). We are already seeing a number of forced switches, or forced sales thanks to the tighter IO rules more generally. This is just the start. More than $60 billion of IO loans are outside current underwriting standards on our estimates.

Some of this will come from the lenders directly. For example, last week ANZ said it will be regarding all interest-only loan renewals as credit critical event requiring full income verification from 5 March. If loans failed this assessment these loans would revert to P&I loans (with of course higher repayment terms). We are already seeing a number of forced switches, or forced sales thanks to the tighter IO rules more generally. This is just the start. More than $60 billion of IO loans are outside current underwriting standards on our estimates.

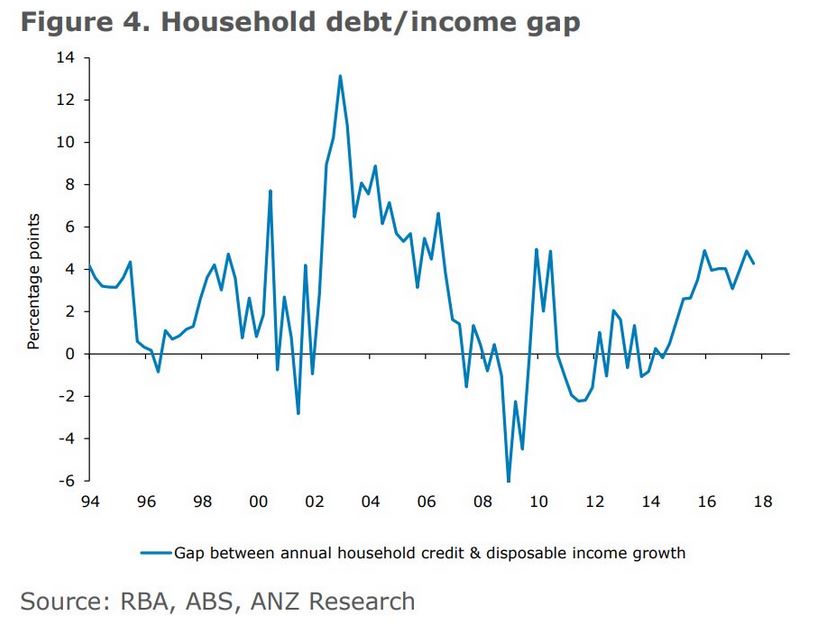

But, as ANZ has pointed out in a separate note from David Plank, Head of Australian Economics at ANZ; household leverage is still increasing, this despite a moderation in housing credit growth over the past year. Household debt continues to grow faster than disposable income.

With household debt being close to double disposable income it will actually require the growth in household debt to slow well below that of income in order for the ratio of household debt to income to stabilise, let alone fall.

In fact, he questions whether financial stability has really being improved so far, when interest rates are so very low.

A key concern we have with the RBA’s comfort with recent household debt trends is whether the slowdown in household debt growth is likely to be sustained with interest rates so low.

Our analysis on the debt/income gap suggests that the RBA’s comfort with how things are evolving on the debt front may be misplaced.

The first sign of this will be clear evidence of recovery in house prices, possibly already underway, which will likely be followed by a reacceleration in debt growth.

If things develop in this fashion it will be interesting to see whether the RBA maintains its focus on clear progress toward the mid-point of the inflation target range as the key to the setting of interest rates.

We suspect that the first port of call to any signs of a reacceleration in household debt will be additional macro-prudential policy…

In other words expect more tightening before the cash rate goes up.