All eyes are on the US Federal Reserve which is expected to raise interest rates for the first time in nearly a decade. Since the financial crisis in 2008, the US, along with the eurozone, UK and Japan have held their interest rates close to zero and used quantitative easing to flood financial institutions with capital.

This two-pronged approach to reviving economic growth has led to a colossal amount of money being injected into the global financial system, offered at next to nothing. While the aim has been to revitalise the consumer spending needed to boost the economies of advanced economies, developing countries are poised to be the victims of these policies.

More than US$12 trillion has been injected into the global financial system since 2008 all in the name of stabilising the global economy. The injection of hot money at this pace and quantity is nothing more than a false economy, and could sooner rather than later trigger massive economic challenges in emerging economies.

Investors have been able to borrow significant sums for very little and direct the proceeds into high-yielding assets in developing countries. A fire hose of cash has poured into investments, financing infrastructure and other projects. But the massive surge in the supply of cheap credit has created unstable bubbles.

As the following graph shows, key emerging economies such as Ghana, Nigeria, Argentina, Brazil, Thailand and Vietnam have seen dramatic increases in their debt stock. And they are not alone. World Bank data shows they are among 80 emerging markets whose debt has increased significantly since the financial crisis.

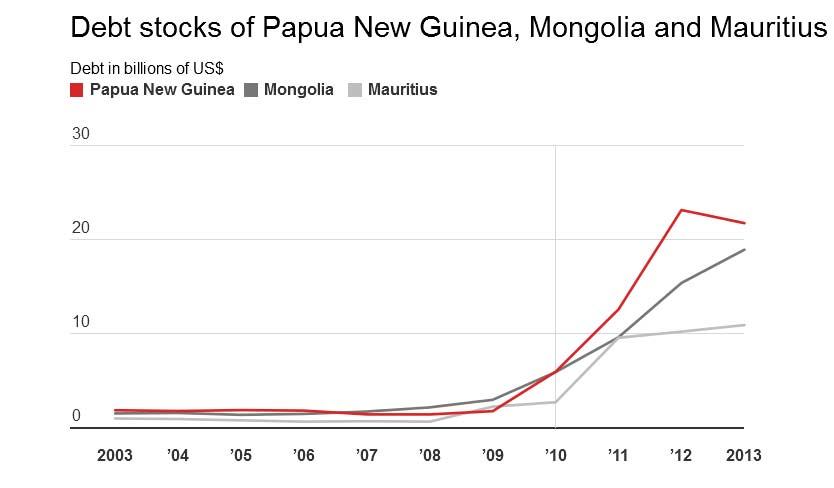

A number of others such as Mongolia, Mauritius and Papua New Guinea saw their debt stock increase by close to 1,000% in the five years following the 2008 financial crisis. These are all low income economies and so their ability to absorb economic shocks is minimal. If (and when) foreign investment is pulled out, they will suffer.

Bubble bursting

If investment is withdrawn – as is likely when interest rates rise – this will leave a gaping hole in the financial system of the recipient countries. Investment in everything from infrastructure to health, education and manufacturing in these countries would be left chronically underfunded, as a colossal amount of money would need to be channelled towards debt-servicing for many years to come.

Not only this, an increase in interest rates could trigger a massive capital outflow from developing countries to where the return on investments has suddenly increased. This is likely to cause a massive shortfall in market capitalisation and burble-busting in the developing countries affected.

To fill the sudden shortfall in capital, the developing countries affected could turn to public or private lenders for urgent financial assistance. But this will increase their debt burden even further.

Most of the debt stocks owed by these developing countries are denominated in foreign currencies, with approximately 80% in US dollars. As the US raises interest rates, the US dollar will strengthen, which will significantly heighten the debt-servicing cost for countries paying back their debts in that currency. Given the nature of their fragile economies, developing countries including Nigeria, Vietnam, Ethiopia and Ghana are most likely to be vulnerable and may have to resort to further borrowing and a fire sale of valuable assets in order to meet their debt obligations.

Exchange rate uncertainty could also trigger a series of credit events, which are capable of hurting the countries’ credit rating. This could lead to margin calls and a review of the existing terms and conditions of lending. And this will only exacerbate the debt burden of the countries concerned even further.

Even a small percentage increase in interest rates is likely to cause shock waves across developing countries. It is a challenging time for emerging markets right now, with commodities in a prolonged slump, and with both China and the eurozone (other key investors) facing economic slowdown.

With an interest rate hike marking the end of cheap credit, this will cause a gaping hole in developing economies’ capital markets. The outflow of capital from their markets will in turn cause their currencies to depreciate further, while the US dollar will strengthen as money flows in. This could lead to even more serious and prolonged debt-servicing problems.

Author: , Senior Lecturer, Quantitative and Financial Economics, University of Westminster