Wealth management company Yellow Brick Road Holdings Ltd has announced a full year loss for FY16 of $9.5m compared with a loss of $2.5m in the prior year. This despite an increase in revenue for the year 31.4% to $217.9m. No dividends were recommended or paid in the financial year. They did not meet their revenue targets and as a result, a period of consolidation and cost cutting is now the order of the day.

Underlying earnings before interest expense, tax, depreciation and amortisation (‘EBITDA’) and excluding impairment charges and other non-operating expenses for the consolidated entity was a loss of $3,901,000 (2015: profit of $1,276,000).

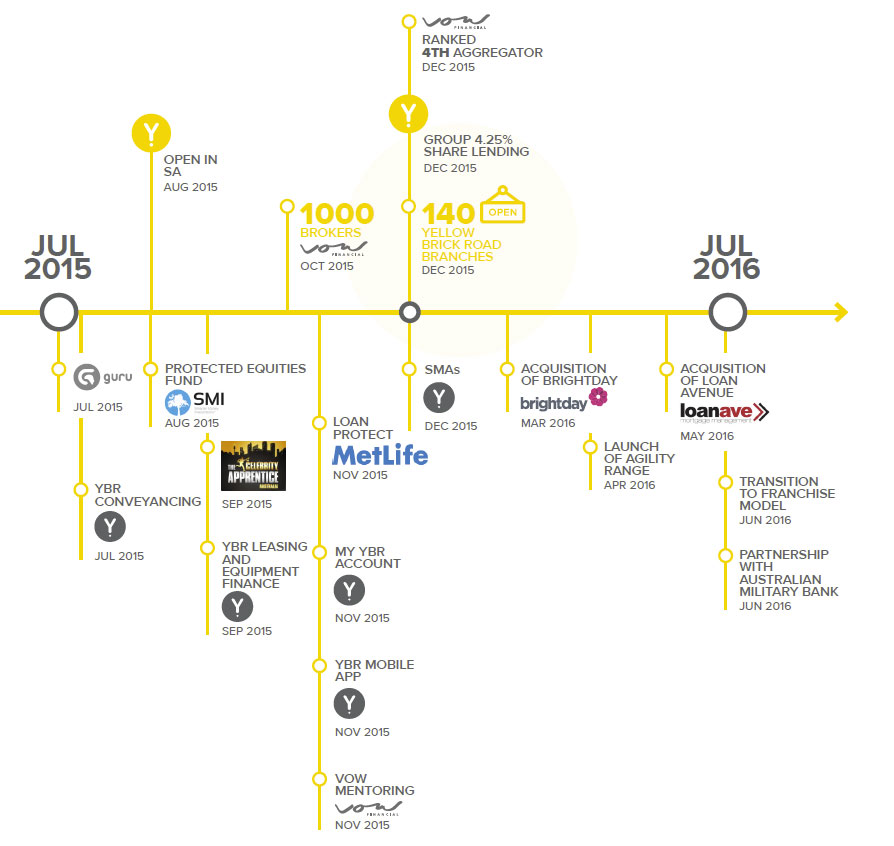

During the year they made a number of acquisitions, and recently announced a significant restructure.

They aspire to become Australia’s leading non-bank financial services company by 2020 through four core activities.

They aspire to become Australia’s leading non-bank financial services company by 2020 through four core activities.

- Central is lending activity that provides scale. Group settlements grew by $3.5 billion in FY16, up 28 per cent and with over $37 billion in loans

under management to date. They are pursuing a $100 billion loan book under management which equates to an approximate market share of 5 per cent. With residential lending softening, the group has invested further in commercial lending achieving 32 per cent growth vs PCP. Additionally in November they entered the small business lending market via a partnership with new SME lending platform Valiant Finance. - This lending business provides a foundation and opportunity for warm introductions for wealth management services which provide margin. Wealth management revenue is up 11 per cent against FY15, with insurance premiums under management up 25 per cent and Yellow Brick Road Super funds under management up 19 per cent on the prior comparable period. Their suite of wealth offerings was rounded out in FY16 by the launch of critical gateway and adjacent products including My YBR Account (OneVue) and eight separately managed accounts, Loan Protect (Metlife), and Protected Equities Fund (Smarter Money Investment and NWQ). They are targeting wealth penetration of 30 per cent of their client base.

- Using geographic modelling, they are increasing their distribution network of local business owners in all communities across Australia. Ongoing recruitment initiatives have netted 354 additional qualified representatives in the Vow Financial and Yellow Brick Road networks in FY16. New quality benchmarks and onboarding procedures are helping ensure higher productivity of these new members with a particular focus on the first two years of operation. The group now has 1500 qualified members operating in all markets across Australia. The FY17 focus is on maintaining momentum in broker recruitment whilst creating multiple avenues for access to financial planners. The target is 300 branded branches and 1000 broker groups.

- Strategic partnerships that leverage scale are an important source of product income. By 2020, they intend to see 10 per cent of income through partnerships, which can be achieve without the complexity or cost of vertical integration.

They say they have faced a number of headwinds in the year.

- Lower rates have increased competition and the addition of more players in the marketplace has seen an increase in refinancing behaviour. Customers are more aware of their ability to get a better rate and the landscape is more competitive than ever. This is of benefit to the younger Yellow Brick Road book but does place some challenges on our more established Vow brokers.

- An increase in the cost of funding has put pressure on margins across the

industry. As lenders respond to regulatory pressure, borrowers face the hurdle of greater scrutiny on household expenditure measurement (HEM) and income verification, which plays into lower approval rates and impacts market size. - The outcome of the current broker remuneration review will likely further shape the mortgage industry in FY17. For planners, new legislation that mandates a biennial obligation to seek client permission to continue servicing and charging will require significant changes to the servicing model of most.

- Australia’s investment lending landscape changed with tougher rules for offshore purchasers and restrictions to lenders’ investor ratios. This has resulted in a restricted environment.

“The completion of a period of heavy investment in brand and distribution build has been met with tough lending conditions and as a result our revenue targets have not been reached. As is appropriate, when macro factors shift in this way, we adapt by shifting to a period of consolidation. This means some tough cost cutting and maintaining strict spending

discipline, while bedding down the recent acquisitions. It also means delivering our technology innovations and leveraging our brand equity”.