Continuing our analysis of the APRA ADI data to September 2017, we will look across the various metrics for new loans, and by lender category.

APRA reports new flows by Major Banks, Other Banks, Foreign Banks and Mutuals (Credit Unions and Building Societies).

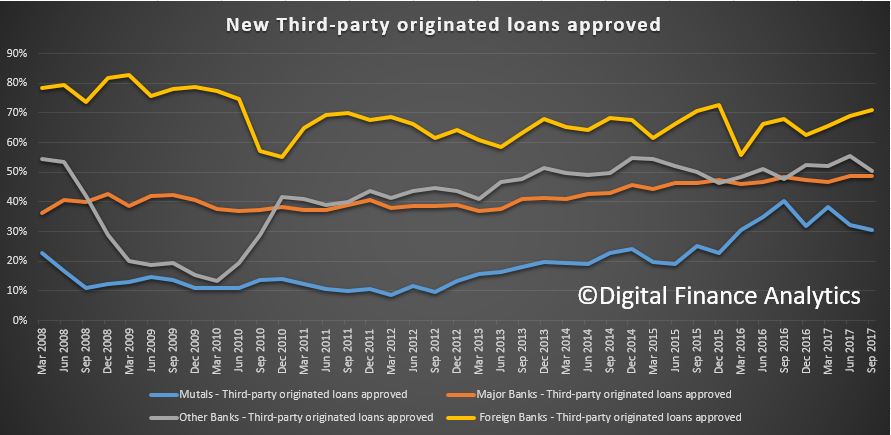

Looking first at third party origination, we see that origination from foreign banks is sitting at 70% of new loans, mutuals around 20% and other banks around the 50% mark. Overall, volume through brokers is climbing.

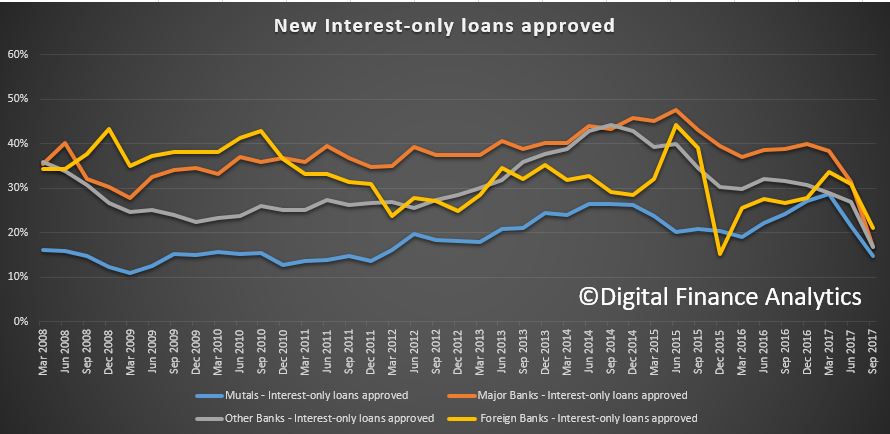

New interest only loan approvals have fallen from, in the case of the major banks, around 40% to 20%, and we see the regulatory pressure has reduced the mix across the board.

New interest only loan approvals have fallen from, in the case of the major banks, around 40% to 20%, and we see the regulatory pressure has reduced the mix across the board.

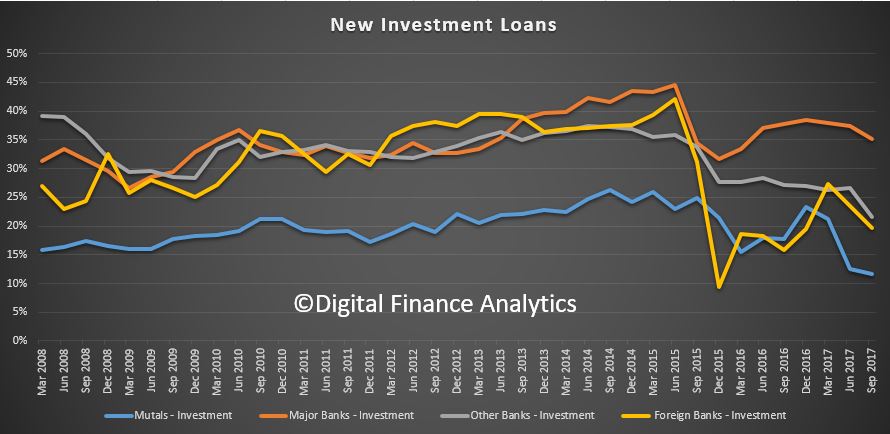

Investment loan volumes have fallen, though major banks still have the largest relative share, above 30%. Mutuals are sitting around 10%.

Investment loan volumes have fallen, though major banks still have the largest relative share, above 30%. Mutuals are sitting around 10%.

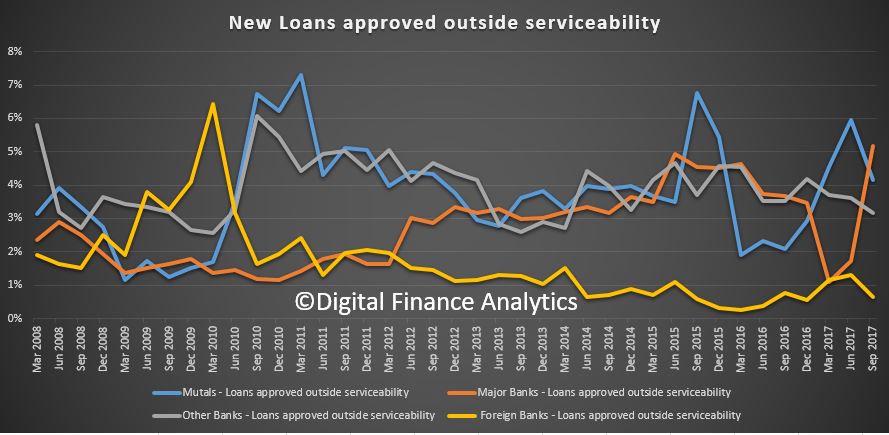

There has been a spike in loans being approved outside serviceability, with major banks reporting 5% or so in September. This may well reflect a tightening of standard serviceability criteria and the wish to continue to grow their loan books.

There has been a spike in loans being approved outside serviceability, with major banks reporting 5% or so in September. This may well reflect a tightening of standard serviceability criteria and the wish to continue to grow their loan books.

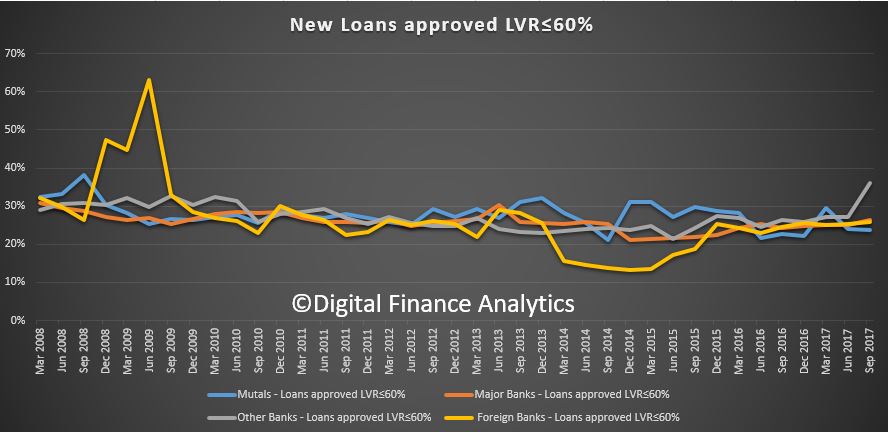

Finally, we look across the LVR bands for new loans. There has been a small rise in loans between 60% LVR, but around 30% of all new loans are in this range.

Finally, we look across the LVR bands for new loans. There has been a small rise in loans between 60% LVR, but around 30% of all new loans are in this range.

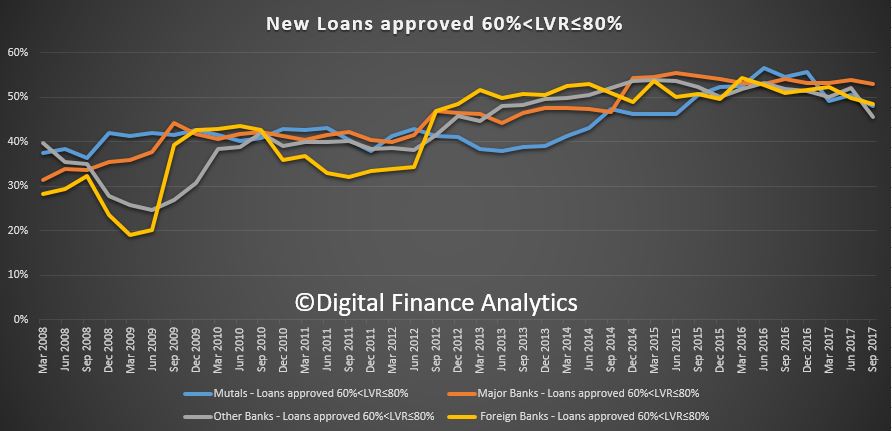

We see a small fall in the relative proportion of loans in the 60-80% range, but close to half of all loans written are still in this range.

We see a small fall in the relative proportion of loans in the 60-80% range, but close to half of all loans written are still in this range.

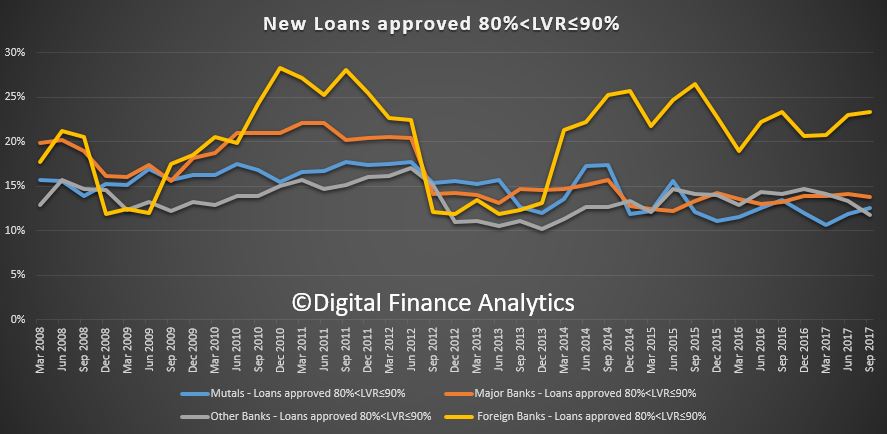

Turning to the 80-90% LVR range, we see a rise in lending by foreign banks, with more than 20% of their loans falling in this range. Other lenders are averaging 10-15 %.

Turning to the 80-90% LVR range, we see a rise in lending by foreign banks, with more than 20% of their loans falling in this range. Other lenders are averaging 10-15 %.

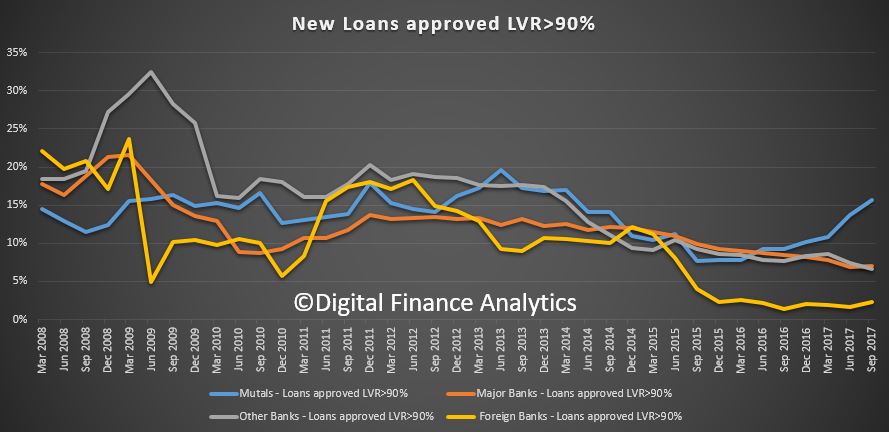

Finally, there is a rise in loans above 90% being written by mutuals, (as they they to grow share), while the banks are around 7% and foreign banks lower still.

Finally, there is a rise in loans above 90% being written by mutuals, (as they they to grow share), while the banks are around 7% and foreign banks lower still.

So overall, we see the impact of regulatory intervention. The net impact is to slow lending momentum. As lenders tighten their lending standards, new borrowers will find their ability to access larger loans will diminish. But the loose standards we have had for several years will take up to a decade to work through, and with low income growth, high living costs and the risk of an interest rate rise, the risks in the system remain.

So overall, we see the impact of regulatory intervention. The net impact is to slow lending momentum. As lenders tighten their lending standards, new borrowers will find their ability to access larger loans will diminish. But the loose standards we have had for several years will take up to a decade to work through, and with low income growth, high living costs and the risk of an interest rate rise, the risks in the system remain.