Fresh on the heels of the FSI report, the core thesis of which is that the Australian Banks are too big to fail, so capital buffers must be increased to protect Australia from potential risks in a down turn (a “mild” crash could lead to the loss of 900,000 jobs and a $1-2 trillion or more cost to the economy), it was interesting to see the publication yesterday by APRA of the guidelines for mortgage lending, and ASIC’s targetting interest only loans. This action is coordinated via the Council of Financial Regulators (CFR). This body is the conductor of the regulatory orchestra, and has only had an independant website since 2013. It is the coordinating body for Australia’s main financial regulatory agencies. It is a non-statutory body whose role is to contribute to the efficiency and effectiveness of financial regulation and to promote stability of the Australian financial system. The Reserve Bank of Australia (RBA) chairs the Council and members include the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), and The Treasury. The CFR meets in person quarterly or more often if circumstances require it. The meetings are chaired by the RBA Governor, with secretariat support provided by the RBA. In the CFR, members share information, discuss regulatory issues and, if the need arises, coordinate responses to potential threats to financial stability. The CFR also advises Government on the adequacy of Australia’s financial regulatory arrangements.

Whilst FSI recommended beefing up ASIC, and introducing a formal regulatory review body, it did not fundamentally disrupt the current arrangements. Interestingly, CFR is a direct interface between the “independent” RBA and Government.

So, lets consider the announcements yesterday. None of the measures are pure macroprudential, but APRA is reinforcing lending standards by introducing potential supervisory triggers (which if breached may lead to more capital requirements, or other steps) using an affordability floor of 7% or more (meaning if product interest rates fell further, banks could not assume a fall in serviceability requirements) and at least an assumed rise in rates of 2% from current loan product rates. In addition, any lender growing their investment lending book by more than 10% p.a. will be subject to additional focus (though APRA makes the point this is not a hard limit). These guidelines relate to new business, and does not directly impact loans already on book (though refinancing is an interesting question, will existing borrowers who refinance be subject to new lending assessment criteria?) ASIC is focussing on interest-only loans, which are growing fast, and are often related to investment lending.

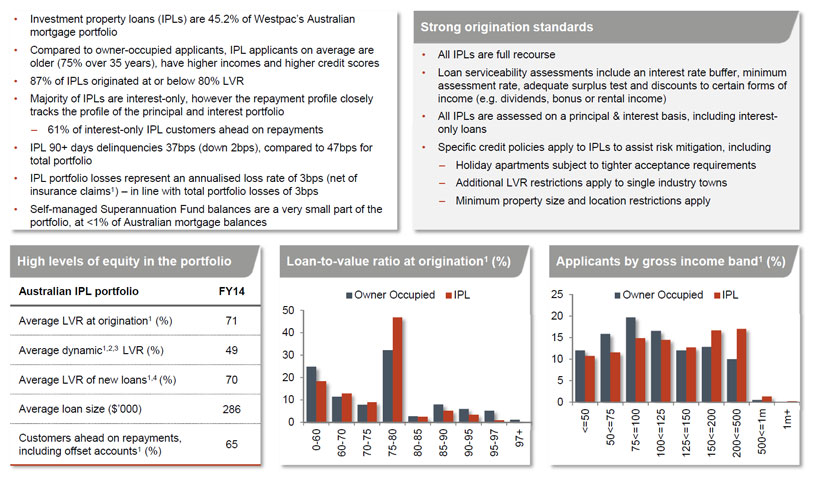

The banks currently have different policies with regards to serviceability buffers. Analysts are looking at Westpac in the light of these announcements, because it grew its investment housing lending book fast, uses 180 basis points serviceability buffer and an interest rate floor of 6.8%. Investment property loans make up ~45% of WBC’s housing loan portfolio (compared with the majors average of ~36%), and has grown at ~12% year on year this financial year (compared with the average across the majors of ~10%). WBC made some interesting comments in their recent investor presentation relating to investment loans, highlighting that investors tended to have higher incomes than owner occupied loans.

Other banks have different underwriting formulations with buffers of between 1.5% and 2.25% buffers. ASIC has of course also stressed that lenders must consider borrowers ability to repay and take account other expenditure. There is evidence of the “quiet word from the regulator” working as recently we have noted some slowing investment lending at WBC (currently they would be below the 10% threshold) and amongst some other lenders too. However, some of the smaller lenders may be impacted by APRA guidance, given stronger recent growth.

Other banks have different underwriting formulations with buffers of between 1.5% and 2.25% buffers. ASIC has of course also stressed that lenders must consider borrowers ability to repay and take account other expenditure. There is evidence of the “quiet word from the regulator” working as recently we have noted some slowing investment lending at WBC (currently they would be below the 10% threshold) and amongst some other lenders too. However, some of the smaller lenders may be impacted by APRA guidance, given stronger recent growth.

What does this all mean. First, we see now what APRA meant in their earlier remarks “collecting additional information, counselling the more aggressive lenders, and seeking assurances from Boards of our lenders that they are actively monitoring lending standards. We’re about to finalise guidance on what we see as sound mortgage lending practice”. Second, we do not think this will materially slow down housing investment lending, and this is probably what the RBA wants, given its belief consumer spending should replace mining investment as a source of growth. The regulators are trying to manage potential risks in the system, by targetting higher risk lending whilst letting housing lending continue to run. Third, it leaves open the door to macroprudential later if needed. Lastly, existing borrowers may be loathe to churn if they are now required to meet additional buffers. This may slow refinancing, and increase longevity of loans in portfolio (and loans held longer are more profitable for the banks).

2 thoughts on “Housing Finance Regulation – Tweaked, Not Reformed”