The Royal Commission into Financial Services Misconduct has now uncovered evidence of poor industry practice from both the lending camp, including from mortgage brokers, and the financial advice camp. In both cases their forensic analysis revealed cases of consumers being put in the wrong products, charged for services they never received and on fee structures which were hardly transparent.

In addition, some advisers and brokers were restricted by the product portfolios available via their organisations, and ties back to the big banks and other large players were often not adequately disclosed.

But here’s the thing. There are two distinct flavours of regulation in play, despite both being within ASIC’s bailiwick. I believe it is time to move to a unified common set of regulatory standards to cover both credit and wealth domains.

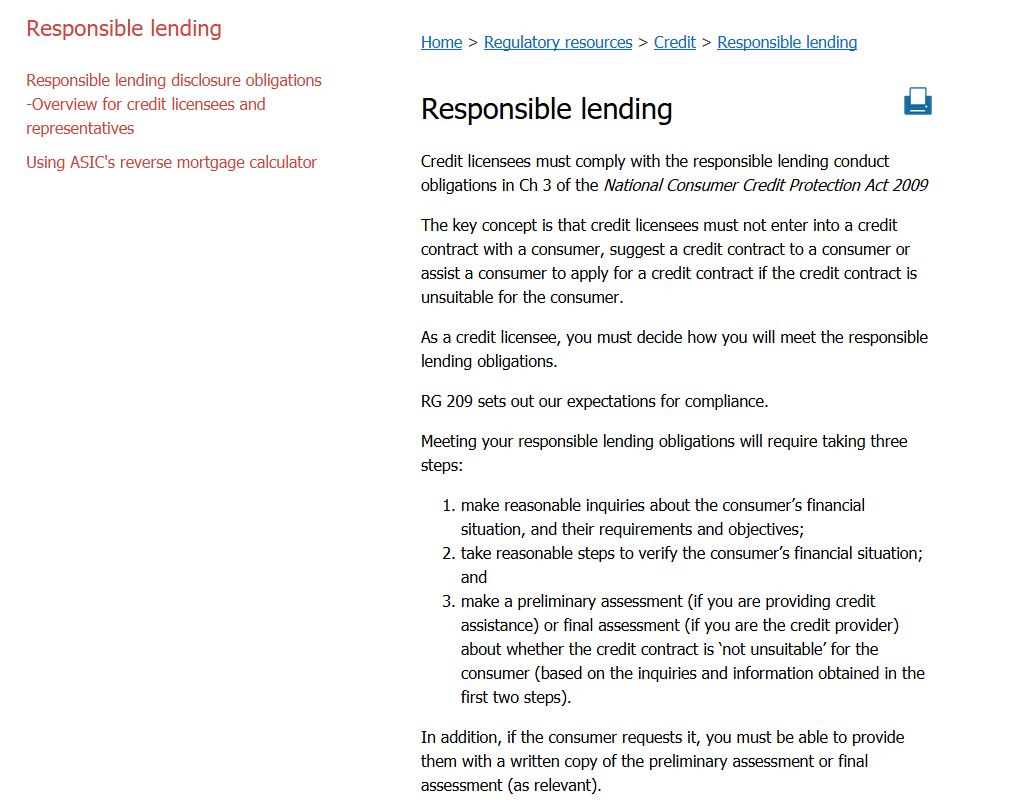

Lending and credit are based on ASIC’s regulations for responsible lending, which requires both a lender, and intermediary – like a broker – to ensure the loan is “not unsuitable”.

This looking at the purpose of the loan, making an assessment of the ability of the consumer to repay, and ensuring it is fit for purpose. What warrants as appropriate steps depends on the nature of the transaction and og the individual capabilities of the customers involved, so it is “scalable”. But that said, they are not obliged to act in the best interests of their client, and fee disclosure is at best rudimentary. Trailing commissions for example are not disclosed. The precise meaning and definition of what is suitable is still subject to case law. But overall, this is weak protection, and as we have seen from the Commission has failed to protect many borrowers. There is nothing here about the best or most appropriate product and it does not include any reference to whole of market analysis. Just, at best “Not Unsuitable”.

This looking at the purpose of the loan, making an assessment of the ability of the consumer to repay, and ensuring it is fit for purpose. What warrants as appropriate steps depends on the nature of the transaction and og the individual capabilities of the customers involved, so it is “scalable”. But that said, they are not obliged to act in the best interests of their client, and fee disclosure is at best rudimentary. Trailing commissions for example are not disclosed. The precise meaning and definition of what is suitable is still subject to case law. But overall, this is weak protection, and as we have seen from the Commission has failed to protect many borrowers. There is nothing here about the best or most appropriate product and it does not include any reference to whole of market analysis. Just, at best “Not Unsuitable”.

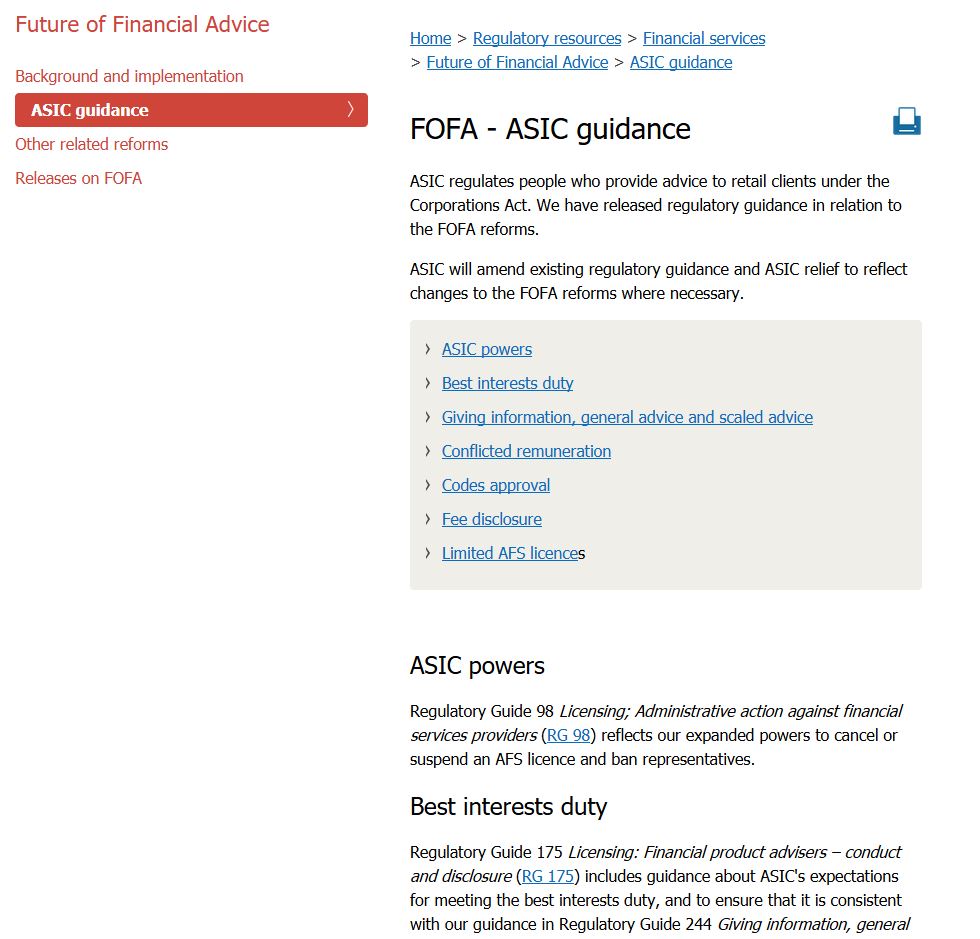

On the financial advice side of the house, as is being explored by the Commission currently, under the FOFA rules, advisers must work in the best interests of their clients, disclose remuneration, and their relationship with product manufacturers if appropriate.

This is a whole different set of rules, again regulated by ASIC. Note again, this does not include finding the best product, or providing whole of market advice. So the rules are slightly stronger, but still incomplete.

This is a whole different set of rules, again regulated by ASIC. Note again, this does not include finding the best product, or providing whole of market advice. So the rules are slightly stronger, but still incomplete.

Now consider this scenario. I am a property investor who is seeking a mortgage as part of a strategy to build wealth. I will need a life insurance policy also. Who do I talk to? A mortgage broker can assist me with finding a mortgage, but cannot help with life insurance. But if I go and talk to a financial adviser unless they are also a mortgage broker, they cannot assist with the mortgage. And if I find an adviser qualified in both regimes, which rules do they work under?

And that’s the point. The regulations, which by the way are an accident of history in that the responsible lending laws evolved from earlier state legislation, get in the way of providing holistic unified advice. A consumer has both credit AND other wealth management requirements as part of a single issue. Indeed, there are trade-offs, for example between holding more or less investment properties, versus investing in other market related investment products. Indeed, it is feasible to wrap property investments into an overall wealth strategy.

So I suggest that now is the time to create a new unified set of rules to apply to all financial advisers, whether they are advising on credit or wealth products. They should be crafted around best interests of their clients, and should mean offering whole of market advice. That means creating an advice plan which spans both investments and lending. The plan should be based on a fee for service, and the advisers’ remuneration should not be in any way linked to a commission or revenue flow from the products they suggest.

Indeed, we should break apart the advice element from the product sale, and application. I suggest that individual product application could be completed by the adviser as part of a fee for service, but they should not receive any additional remuneration related to successful product sales.

This also has implications for ASIC, as it would reshape the advice landscape, but potentially could both simplify the regulatory regime, and strengthen the protection for customers, and help facilitate better customer outcomes. Down the track, advisers would require one set of qualifications, and would be become more recognised professionals.

I believe the current chaotic regulatory environments, which were crafted to appease the finance industry, are in appropriate and the time has come to create a single unified set of regulations. This would assist customers, but would also help the industry on its journey towards professionalism.

You’re really on the right track, but the regulations need to go much further than just financial planners and mortgage brokers. Updated regulations should also include property advisors – particularly those who charge for ‘education’ as well as taking commissions from developers and then take the commission trail for the mortgage and the insurance. In my opinion, the regulatory environment is so bent out of shape we need to start from scratch. Trouble is . .there will always be those who will skate around the regulations and leave consumers vulnerable. For this reason, the industry needs to also focus on educating consumers so they can identify bad advice before they sign up to pay for it over and over – and in some cases even after they pass away (how bad is that??).

Thanks- yes I agree the whole approach to regulation needs to change, from the ground up.

Closing down the vertical integration (as banks sell off financial planning) will lead to less biased product recommendations as will fee for service and that applies to both financial planning and mortgage broking.

Perhaps then the right product for the right purpose for the client will be an easier choice.

Without commissions, getting paid a fee for service is another kettle of fish!