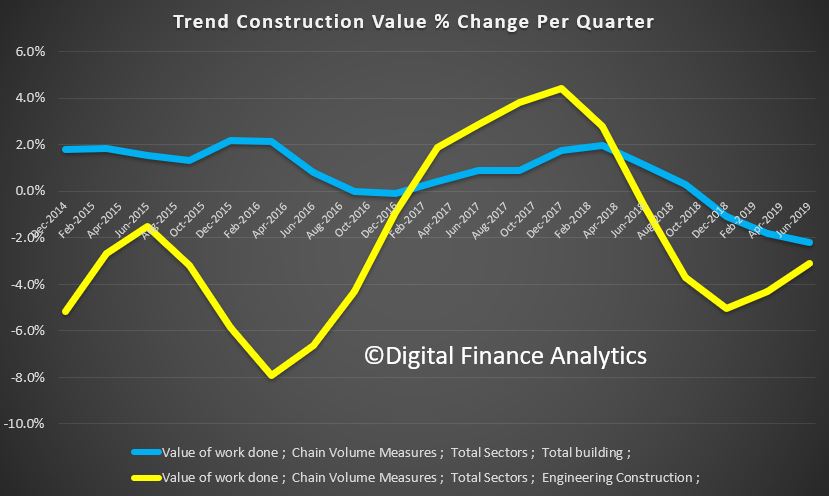

The ABS released their June 2019 “Construction Work Done, Australia, Preliminary” today. It paints a picture of slowing momentum once again. This will flow into a weaker GDP number ahead.

The trend estimate for total construction work done fell 2.7% in the June quarter 2019.

The seasonally adjusted estimate for total construction work done fell 3.8% to $48,778.0m in the June quarter.

The trend estimate for total building work done fell 2.2% in the June quarter 2019.

The trend estimate for non-residential building work done fell 0.8% and residential building work fell 3.0%.

The seasonally adjusted estimate of total building work done fell 5.7% to $28,506.2m in the June quarter.

The trend estimate for engineering work done fell 3.1% in the June quarter.

The seasonally adjusted estimate for engineering work done fell 1.1% to $20,271.8m in the June quarter.

The construction sector is in a downtrend, with activity having peaked in mid-2018. This reflects: (1) the turning down of the home building cycle; (2) a pull-back in public works; and (3) a further winding down of private infrastructure activity led by the mining sector (although this dynamic has largely run its course).

With the construction sector representing around 13% of the economy this result will dent Q2 GDP, potentially in the order of 0.4ppts – depending upon how these quarterly partials flow through to the national accounts estimates.

The housing downturn still has further to go and will weigh on conditions throughout 2019 and into 2020.

On public works, there is a sizeable work pipeline and governments are adding projects to the investment pipeline – suggesting that the segment will be more supportive of conditions over the forecast period. On private infrastructure, commencements have picked-up somewhat (eg some iron ore projects have proceeded in response to the recent elevated prices) and the work pipeline has increased – pointing to an emerging lift in activity during the year ahead.

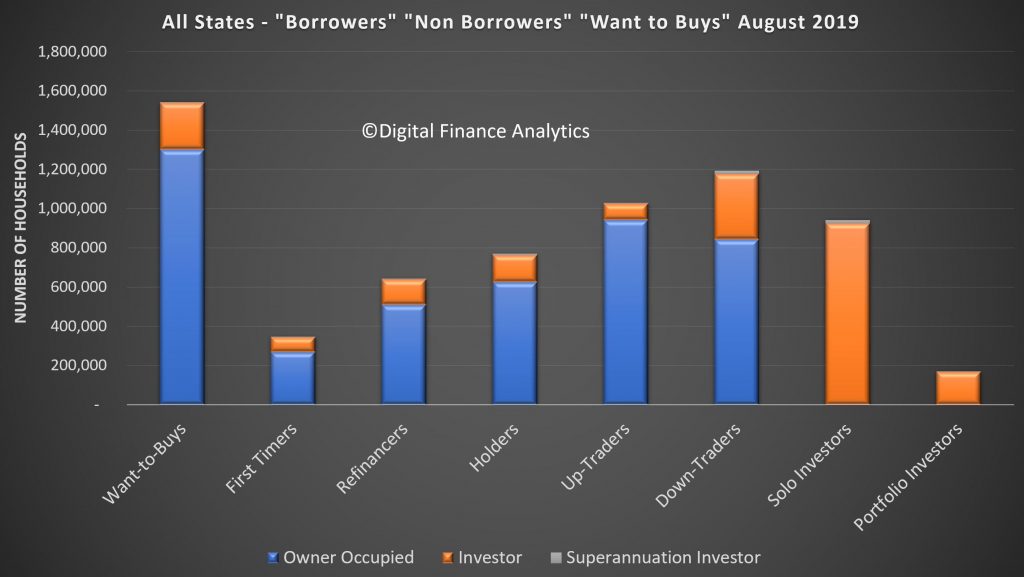

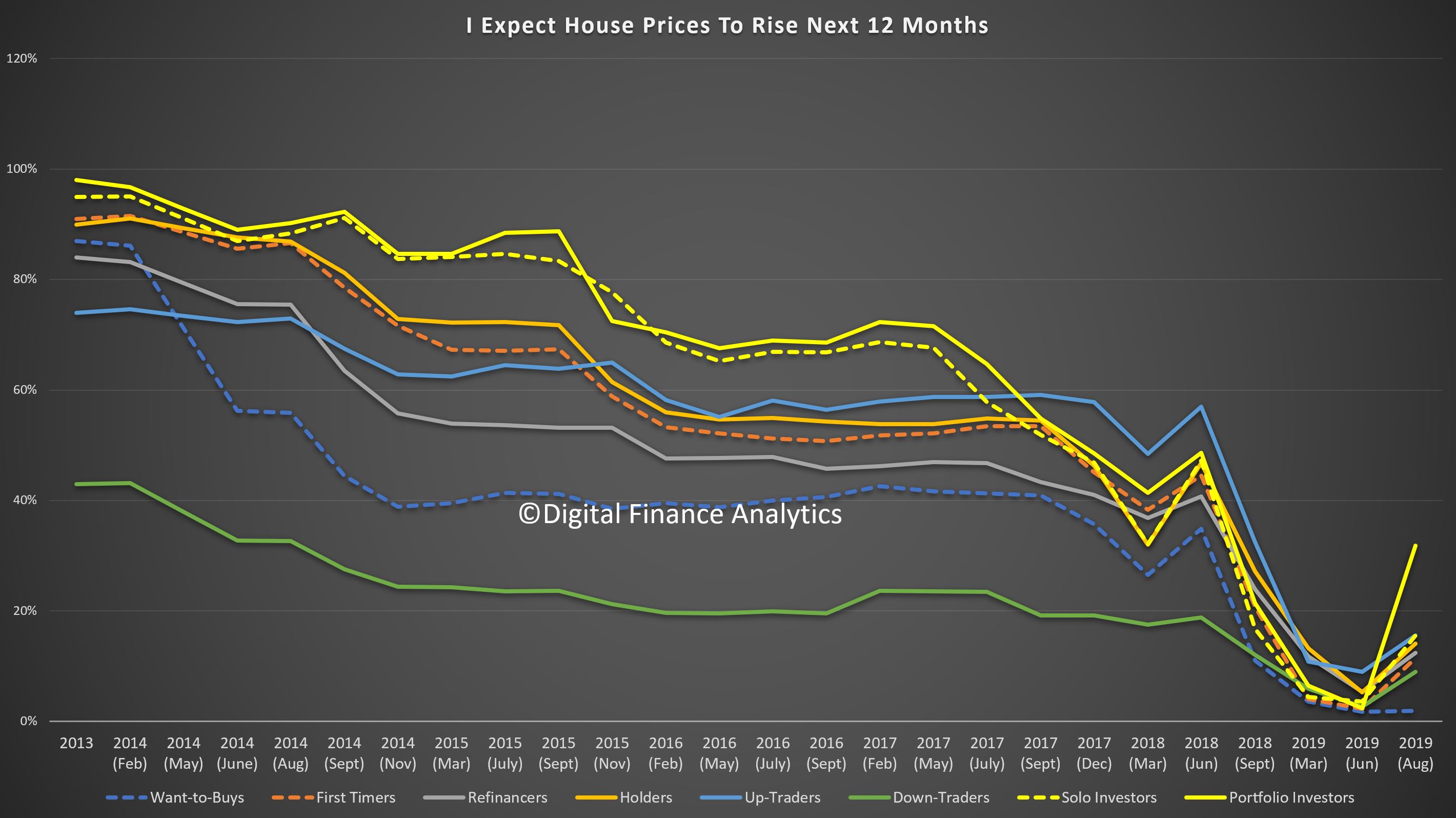

Digital Finance Analytics will be releasing the results from our rolling household surveys over the next few days. This is the first in the series.

These are the results from our 52,000 households looking at property buying propensity, price expectations and a range of other factors.

We use a segmented approach to the market for this analysis, and in our surveys place households in one of a number of potential segments.

Want To Buys: households who would like to buy, but have no immediate path to to purchase. There are more than 1.5 million households currently in this group.

First Timers: first time buyers with active plans to purchase. There are around 350,000 households in this segment.

Up-Traders: households with plans to buy a larger property (and sell their current one to facilitate the up-sizing. There are around 1 million households in this group.

Down Traders: households wishing to sell and down size, sometimes buying a smaller property at the same time. There are around 1.2 million households in this group.

Some of these households will hold investment property as well. We categorise investors into one of two groups.

Solo Investors: households with one or two investment properties. There are about 940,000 of these.

Portfolio Investors: households with more than two investment properties. There are around 170,000 of these.

Finally we also identify those who are planning in refinance existing loans, but are not intending to buy or sell property – flagged as Refinancers, and those with no plans to buy, sell or refinance – flagged as Holders.

It is the interplay of all these segments which drives the property market and demand for mortgages.

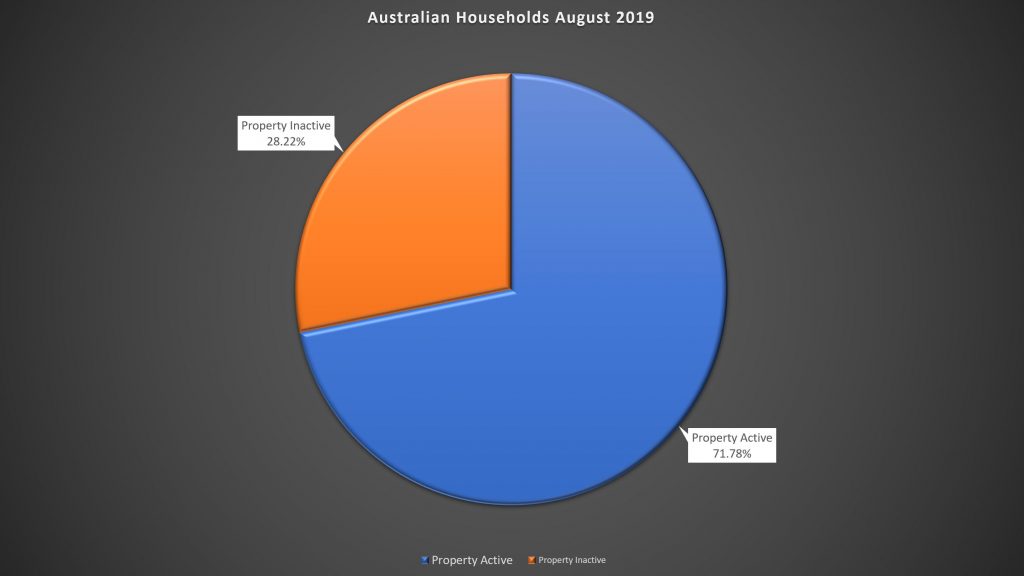

Around 72% of households are property active – meaning they want to buy, sell, or own property. More than 28% are property inactive, meaning they rent, live with parents or in other arrangements. Our surveys track all household cohorts. A greater proportion are falling into the inactive category.

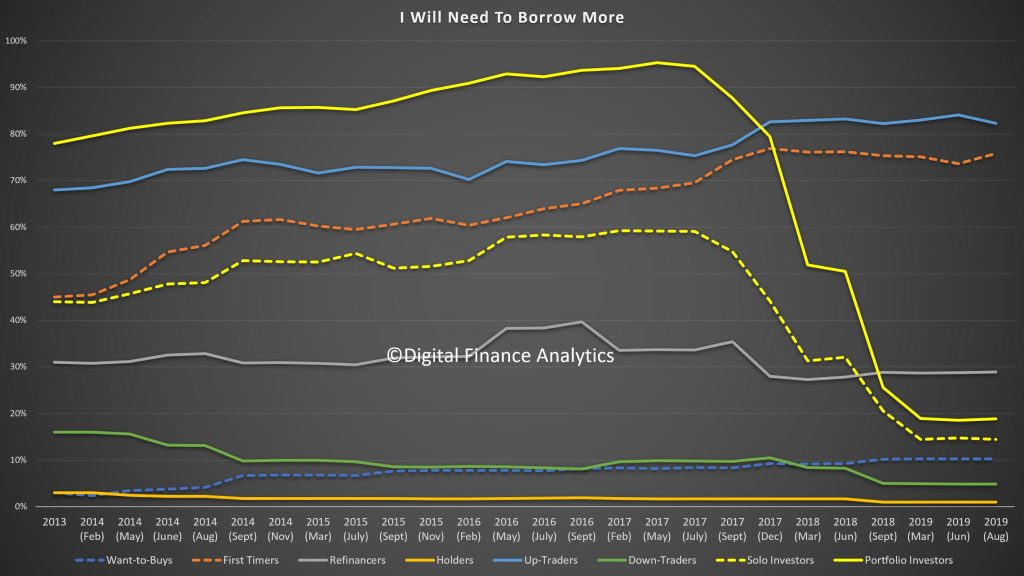

Intention To Transact Is Rising (From A Low Base)

We ask about households intentions to transact in the next 12 months, and whether they will be buy-led (seeking to purchase a property first) or sell-led (seeking to sell a property first). (Click on Image To See Full Size).

Property investors are still coy (hardly surprising given the fall in capital values, the switch to P&I loans and receding rentals. But Down Traders, First Time Buyers and Refinancers are showing more intent.

We will look at the drivers by segment in a later post.

But the Buy Side and Sell Side Analysis is telling

Those seeking to buy are being led by First Time Buyers and Down Traders.

Those looking to sell are being led by the Down Traders, and Property Investors. In fact this suggests we will see a spike in listings as we move into spring.

Our equilibrium model suggests that currently supply is not meeting demand (adjusted for property types and locations) in a number of prime Sydney and Melbourne locations, within 30 minutes of the CBD. But beyond that demand is below current supply, and more is coming.

On this basis, we expect to see some local price uplifts, but not a return to the rises a couple of years back. What is clear, is that the property investment sector continues to slumber, and Down Traders are getting more desperate to sell.

Finally, today demand for more credit is coming from Up-Traders, First Time Buyers and Refinancers. Not Investors.

And price expectations seem to be on the improve, driven by investors. But it is still lower than a couple of years ago.

Next time we will dive into the segment specific drivers.

“What we need to do is rebuild confidence in Australia’s building and construction sector,” said federal minister Karen Andrews after the July 2019 meeting of the Building Ministers’ Forum). Via The Conversation.

This has been a recurring theme since the federal, state and

territory ministers commissioned Peter Shergold and Bronwyn Weir in

mid-2017 to assess the effectiveness of building and construction

industry regulation across Australia. They presented their Building Confidence report to the ministers in February 2018.

In the 18 months since then, the combined might of nine governments

has made scant progress towards implementing the report’s 24 simple

recommendations. Confidence in building regulation and quality has

clearly continued to deteriorate among the public and construction

industry.

In last week’s Four Corners program, Cracking Up,

Weir was asked whether she would buy an apartment. She responded: “I

wouldn’t buy a newly built apartment, no […] I’d buy an older one.” She

went on to say:

We have hundreds of thousands of apartments that have been built

across the country over the last two, three decades. Probably the

prevalence of noncompliance has been particularly bad, I would say in

the last say 15 to 20 years […] And that means there’s a lot of existing

building stock that has defects in it […] There’ll be legacy issues for

some time and I suspect there’ll be legacy issues that we’re not even

fully aware of yet.

These comments may not have delighted those developers trying to sell

new apartments, or owners selling existing apartments, but they are

fair and correct. Confidence will not be restored until all the

governments act together to improve regulatory oversight and deal with

existing defective buildings.

Residents of the Lacrosse, Neo200, Opal and Mascot towers and other buildings with serious defects are already living with the impact of “legacy” problems. Over the weekend, another apartment building was evacuated

– this time in Mordialloc in southeast Melbourne. The building was

deemed unsafe because it was clad with combustible material and had

defects in its fire detection and warning system.

A costly but essential fix

Fixing such defects is a costly business. A Victorian Civil and Administrative Tribunal decision

established that replacing the combustible cladding on the Lacrosse

building in Melbourne would cost an average of A$36,000 per unit. At

Mascot Towers, consultant engineers estimated the cost of structural repairs at up to A$150,000 per unit on average.

According to UNSW and Deakin

research, between 70% and 97% of units in strata apartments have

significant defects. Let’s assume 85% have such defects and the average

cost of fixing these is only $25,000 per unit. That would mean total

repair costs for the 500,000 or so tall apartments (four-storey and

above) across Australia could exceed A$10 billion.

The Victorian government has taken the lead on combustible cladding, setting up and funding a A$600 million scheme

to replace it. It’s also replacing combustible cladding on low-rise

school buildings even though these may comply with the letter of the

National Construction Code.

No other state has yet followed this lead. This is concerning given the risk to life. No one viewing images of the Neo200 fire in the Melbourne CBD could doubt how dangerous combustible cladding can be.

The other states and territories should immediately copy the

Victorian scheme. While not perfect, and probably underfunded, it is a

positive step to improve public safety. The Andrews government should be

congratulated for doing something practical while its counterparts in

New South Wales and Queensland, which have many buildings with

combustible cladding, fiddle about.

All governments share responsibility

The federal government’s response has been inadequate. When asked

about contributing to the Victorian scheme, Karen Andrews said:

The Commonwealth is not an ATM for the states […] this problem is of

the states’ making and they need to step up and fix the problem and dig

into their own pockets.

This flies in the face of reality. All nine governments are responsible for building regulation and enforcement. All signed the intergovernmental agreement on building regulation.

The federal government, which chairs the Building Ministers’ Forum, leads building regulation in Australia. The Australian Building Codes Board, which produces the National Construction Code,

is effectively a federal government agency. The precursor to the

national code, the Building Code of Australia, was a federal initiative.

The crop of building defects we see today are a direct result of

negligent regulation by all nine governments over the past two decades.

Clearly, they all have a legal and moral duty to coordinate and

contribute to a program to manage the risks and economic damage this has

created.

The governments must stop playing a blame game. Effective programs

are urgently needed to fix defects, including combustible cladding,

incorrectly installed fire protection measures, structural

noncompliance, structural failure and leaks.

The Australian Building Codes Board, which is directly responsible

for the mess, should be reformed to ensure it becomes an effective

regulator. The National Construction Code should be changed to make consumer protection an objective in the delivery of housing for sale.

All parties involved will have to take some pain: regulators,

developers, builders, subcontractors, consultants, certifiers, insurers,

aluminium panel manufacturers, suppliers and owners. Only governments

can broker a solution as it will require legislation and an allocation

of responsibility for fault.

The alternative will probably be a huge number of individual legal cases and a rash of owner bankruptcies, which may well leave the guilty parties untouched.

Author: Geoff Hanmer, Adjunct Lecturer in Architecture, UNSW

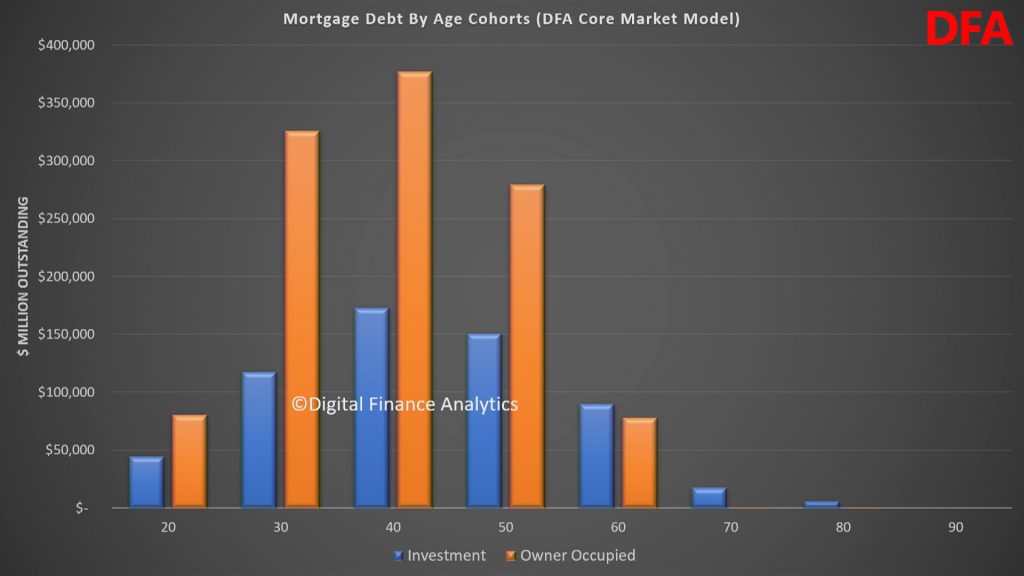

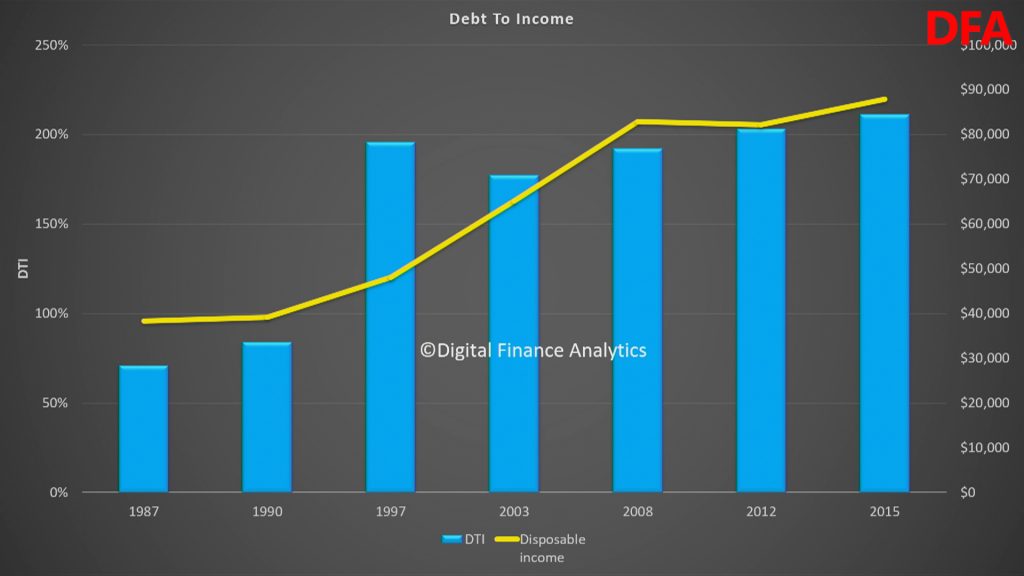

The new AHURI report highlight the fact that more Australians are taking mortgage debt into retirement, will have to us superannuation to repay the debt, and so put more pressure on Government in terms of future support.

High debt into retirement is also leading to more stress.

Our surveys show the relative debt by age cohorts. The trends are “moving to the right” as people buy later, get larger loans, and hold them into retirement. Overall debt has never been higher.

As a result the debt to income ratio of those over 55 years has deteriorated significantly.

The final point to make is households as they enter retirement will be more reliant on fixed incomes, at a time when savings rates on deposits are at a record low. So servicing this debt into retirement will be a major issue.

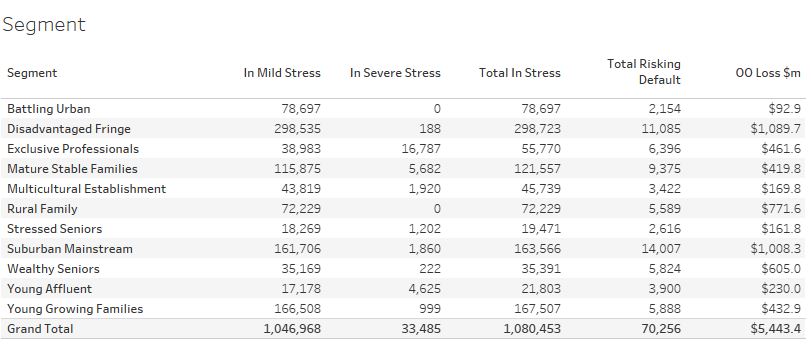

Combined this explains why mortgage stress is lurking among older households, as our July stress data revealed. This includes more than 35,000 “Wealthy Seniors” across the country.

ASIC says that Allianz Australia Insurance Limited (Allianz) will refund over $8 million in consumer credit insurance (CCI) premiums and fees including interest to more than 15,000 consumers.

This follows ASIC’s review of the sale of CCI by lenders in Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622), and forms part of ASIC’s broader priority to address harms and unfair practices impacting consumers in insurance.

Allianz’s refund relates to the sale of cover to

consumers who were ineligible to make a claim for unemployment or

disability, the sale of death cover to customers under 21 years of age

who were unlikely to need that cover, and the charging of fees to

customers who paid premiums by the month without adequate disclosure.

The remediation program covers certain CCI products

issued by Allianz including mortgage and loan protection policies sold

through financial institutions. These CCI products provided cover

against the risk of consumers being unable to meet loan commitments

because of death, injury, illness or involuntary unemployment.

To address these issues, Allianz will,

for ineligible sales of unemployment and disability cover,

refund premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018;

reassess all withdrawn and declined claims where the consumer was ineligible for the policy at the time of sale;

invite consumers to submit a claim if they have not already done so and pay valid claims plus interest; and

continue to honour active policies and not rely on employment eligibility criteria as a basis to decline an unemployment or disability claim;

for sales of death cover to customers under 21 years of age,

refund all premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018; and

preserve existing death cover for active policyholders on current terms without charging for it;

for monthly policy payment customers,

refund all administration fees and loading charged plus interest; and

correct any future direct debit amounts.

ASIC Commissioner Sean Hughes said, ‘Disappointingly,

our work on the sale of CCI has highlighted widespread mis-selling and

poor product design. This remediation outcome is only one of many

examples where CCI has failed consumers. We expect insurers to cease to

sell insurance products that provide little or no value.’

‘We need a financial system that is fair. Insurers and

other financial institutions need to rise to the challenge and embed the

principle of fairness into their businesses to ensure we do not see any

further instances of this kind of poor value product being pushed on to

consumers’ added Mr Hughes.

Allianz will stop issuing new CCI policies from 30

September 2019. It will continue to fulfil its obligations to existing

CCI policyholders.

Allianz is expected to write to all affected consumers

about their refund offer from October 2019. Consumers with questions

about their cover should contact Allianz by email at here_to_help@allianz.com.au.

Background

ASIC’s recent review of the sale of CCI has resulted in

refunds of over $100 million due to more than 300,000 affected

consumers. On 11 July 2019, we released Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622) detailing our findings and setting minimum standards for lenders and insurers who issue or sell CCI (19-180MR).

ASIC is currently consulting on a proposal to ban the

sale of CCI and direct life insurance through unsolicited telephone

calls (19-188MR).

The proposed ban aims to address unfair sales conduct and protect

consumers from being sold products that they do not need, want or

understand.

ASIC has also commenced investigations into a number of entities that have been involved in mis-selling CCI to consumers.

Separately, in 2018, Allianz refunded $45.6 million to

68,000 consumers for add-on insurance sold through car dealerships that

were of little or no value (18-008MR).

Interesting speech from Wayne Byers “Reflections on a changing landscape“. He discussed the ” extraordinary intervention” to save our banks a decade ago (in a footnote), significant in my view, for what it said, and for what it missed out. There is no mention that both NAB and Westpac required bailing out by the FED’s TAF after the GFC. An important little fact?

APRA’s activities have expanded significantly over the past five years. This has not been a smooth transition: the regulatory pendulum has swung between periods of significant regulatory change, and times when there have been demands to pare back. But overall there is no doubt that expectations of APRA have grown, and they have pushed us into new fields of endeavour. There is no sign that tide is going to turn soon.

I’m not sure what the issues de jour will be in five years’ time but there’s a very good chance they will not be the issues we think are most important today. The past five years has shown that what might seem unusual or out of scope today, can quickly become a core task tomorrow. Some of the topics that I have talked about tonight were not seen, five years ago, to be at the heart of APRA’s role.

In contrast, later this week we will publish our 4 year Corporate Plan and a number of them will be called out as our core outcomes, ranking alongside maintaining financial safety and resilience.

If there is one lesson from the past five years, it is that – be it regulators or risk managers – being ready and able to respond to the demands of a rapidly changing landscape is probably the most important attribute we all need to possess.

But the footnote was the most interesting in my view. For what it said, and for what it missed out.

It is sometimes said the Australian banking system ‘sailed through’ the financial crisis. While the system did prove relatively resilient, there was extraordinary intervention necessary to keep the system stable and the wheels of the economy turning.

That included (i) an unprecedented fiscal response – one of the largest stimulus packages in the world;

(ii) an unprecedented monetary response – the official cash rate was cut by 425 basis points in a little over six months;

(iii) the RBA substantially expanded its market operations and balance sheet;

(iv) ASIC imposed an 8-month ban on the short selling of financial stocks; and

(v) the Federal Government initiated a guarantee of retail deposits of up to $1 million, and a facility for authorised deposit-taking institutions (ADIs) to purchase guarantees for larger deposits and wholesale funding out to 5 years (indeed, at one point more than one-third of the banking system’s entire liabilities were subject to a Commonwealth Government guarantee).

As I have said previously, if all of the above was needed to keep the system stable and operational, then it is difficult to argue that the system sailed through or that some further strengthening of regulation was not justified.

He failed to mention the massive bail-out of our banking system from the FED and the fact that it was China’s response which supported our economy. The evidence suggests we were much closer to the abyss than was acknowledged at the time. Westpac and NAB both required support from the FED, as revealed in papers from the FED.

The US Dodd-Frank Act requires the US Federal Reserve to reveal which institutions it loaned money to under the various bail out programmes.

“Under the program, the Federal Reserve auctioned 28-day loans, and, beginning in August 2008, 84-day loans, to depository institutions in generally sound financial condition… Of those institutions, primary credit, and thus also the TAF, is available only to institutions that are financially sound.

Now of course the question is what does “financially sound” institutions mean. Well, look at the entire list – its long, but some of the names will be familiar. The FED data shows more than 4,200 separate transactions across more than 400 institutions globally between 2008 and 2010.

UK based Lloyds TSB plc received USD$10.5 billion – and was later partially nationalised by the UK government.

And another UK Bank, the Royal Bank of Scotland (RBS) got US$53.5 billion plus and additionally US$1.5 billion for its exposures via ABN Amro after RBS bought it. That was nationalised too.

In Ireland, Allied Irish Bank needed US$34.7 billion of loans from the Fed between February 2009 and February 2010 . This is the bank bailed out via the Irish taxpayer.

And Deutsche Bank needed a massive US$76.8 billion in loans in total (and that bank continues to struggle today).

The list goes on. Bayerische Landesbank required a US$13.4 billion bailout from the state of Bavaria, but also borrowed US$108.19 billion between December 2007 and October 2009.

Where these banks sound?

And our own “financially sound” institutions National Australia Bank and Westpac needed help from the Fed. NAB needed around $7 billion in total (allowing for the exchange rate).

In fact NAB raised $3 billion from shareholders in 2008 to add capital to its business in parallel.

And in January 2008 Westpac said everything was fine with its US exposures, just one month after they got their first bail-out from the FED, worth US$90 million.

In fact, there was a long queue then, as the Fed spreadsheet shows that alongside Westpac, was Citibank, Lloyds TSB Bank, Bayerische Landesbank and Societe Generale, all of whom where bailed out by Governments in their respective countries.

Now, the RBA wrote at the time:

“The Australian financial system has coped better with the recent turmoil than many other financial systems. The banking system is soundly capitalised, it has only limited exposure to sub-prime related assets, and it continues to record strong profitability and has low levels or problem loans. The large Australian banks all have high credit ratings and they have been able to continue to tap both domestic and offshore capital markets on a regular basis.”

So the question is did APRA and the RBA know what was going on?

And my question more generally is how prepared are we for a similar crisis now – given the changed economic and geopolitical forces in play?

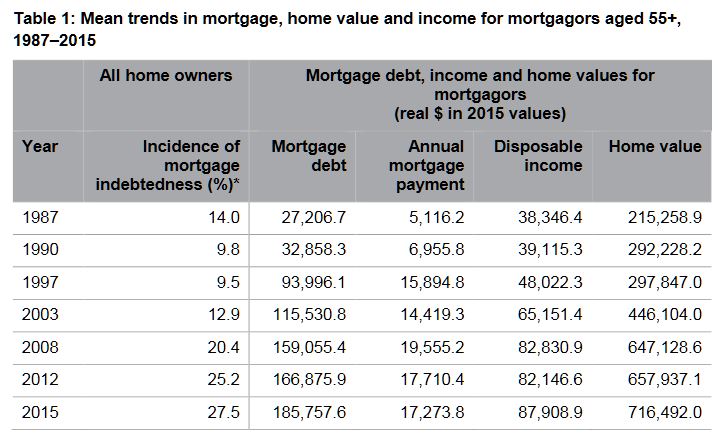

Between 1987 and 2015, average real mortgage debt among older Australians (aged 55+ years) blew out by 600 per cent (from $27,000 to over $185,000 in $2015), while their average mortgage debt to income ratios tripled from 71 to 211 per cent over the same period, according to new AHURI research.

The research, Mortgage stress and precarious home ownership: implications for older Australians, undertaken for AHURI by researchers from Curtin University and RMIT University, investigates the growing numbers of older Australians who are carrying high levels of mortgage debt into retirement, and considers the significant consequences for their wellbeing and for the retirement incomes system.

‘Our research finds that back in 1987 only 14

per cent of older Australian home owners were still paying off the mortgage on

their home; that share doubled to 28 per cent in 2015’, says the report’s lead

author, Professor Rachel

ViforJ of Curtin University.

‘We’re also seeing these older Australians’ mortgage debt burden increase from

13 per cent of the value of the average home in the late 1980s to around 30 per

cent in the late 1990’s when the property boom took off, and it has remained at

that level ever since. Over that time period, average annual mortgage

repayments have more than tripled from $5,000 to $17,000 in real terms.’

When older mortgagors experience difficulty in meeting mortgage payments,

wellbeing declines and stress levels increase, according to the report.

Psychological surveys measuring mental health on a scale of 0 to 100 reveal

that mortgage difficulties reduce mental health scores for older men by around

2 points and an even greater 3.7 points for older women. Older female

mortgagors’ mental health is more sensitive to personal circumstances than

older male mortgagors. Marital breakdown, ill health and poor labour market

engagement all adversely affect older female mortgagors’ mental health scores

more than men’s.

‘These mental health effects are comparable to those resulting from long-term

health conditions,’ says Professor ViforJ. ‘As growing numbers of older

Australians carry mortgages into retirement the rising trend in mortgage

indebtedness will have negative impacts on the wellbeing of an increasing

percentage of the Australian population.’

High mortgage debts later in life also present significant challenges for housing

assistance programs. The combination of tenure change and demographic change is

expected to increase the number of seniors aged 55 years and over eligible for

Commonwealth Rent Assistance from 414,000 in 2016 to 664,000 in 2031, a 60 per

cent increase. As a consequence the real cost (at $2016) of CRA payments to the

Federal budget is expected to soar from $972 million in 2016, to $1.55 billion

in 2031. The unmet demand for public housing from private renters aged 55+

years is also expected to climb from roughly 200,000 households in 2016, to

440,000 households in 2031, a 78 per cent increase.

There are also challenges for Government retirement incomes policy. The burden

of indebtedness in later life is growing; longer working lives and the use of

superannuation benefits to pay down mortgages are increasingly likely outcomes.

The Australian Financial Complaints

Authority will begin naming financial firms in its published determinations to

increase transparency in the financial sector and enhance consumer confidence.

The change comes following the

Royal Commission into Misconduct in the Banking, Superannuation and Financial

Services Industry.

AFCA undertook a public

consultation and submitted an application to the Australian Securities and

Investments Commission (ASIC) to change the AFCA Rules.

AFCA Chief Ombudsman and CEO David

Locke said AFCA is committed to being open, transparent and accountable to the

public.

“AFCA plays an important public

role and we recognise that transparency in our data and decisions is essential

to rebuilding trust in the financial sector,” Mr Locke said.

“We already publish decisions on

our website, but we have been unable to name the financial firms

involved.

“We welcome ASIC’s approval to

change our Rules, which will allow us to now name financial firms in decisions

we publish on our website.

“This is an important change, and

the public will now be able to access increased information about the actions

of financial firms.”

AFCA is working with ASIC to determine the start date for the naming of financial firms. Further updates will be provided when available.

ASIC has approved changes to the Australian Financial Complaints

Authority (AFCA) Rules to allow the scheme to name financial firms in

published determinations.

In its first six months, AFCA received 35,263 complaints. About 4,500

to 5,000 complaints are currently expected to be finalised each year by

way of determination. While the publication of determinations has been a

longstanding feature of the external dispute resolution schemes in

Australia, the names of firms involved in financial services,

superannuation and credit complaints have not been published to date.

AFCA applied for approval to change their Rules to enable

identification of firms following public consultation. Consumers who are

party to a complaint will continue to be anonymised in all

determinations.

In approving this change ASIC took into account stakeholder feedback

to AFCA’s public consultation and the statutory approval criteria.

ASIC’s view is that naming firms in determinations can help identify

conduct or market problems within firms or affecting specific products

or services, as well as highlighting where firms have done the right

thing. It will also enhance transparency and accountability of firms’

performance in complaints handling and of AFCA’s own decision-making.

To support the new Rules, AFCA will shortly be issuing updated

operational guidelines which set out examples of the circumstances in

which a determination naming a financial firm would not be published.

This includes where naming may expose confidential information about a

firm’s systems or policies.

Naming firms in AFCA determinations is part of a broader set of

reforms aimed at increasing transparency in financial services. This

includes Parliament giving ASIC power to collect and to publish internal

dispute resolution (IDR) data at firm level. The UK Financial

Ombudsman Service has been naming firms in published determinations

since 2013

The National Consumer Credit Protection Amendment (Mortgage Brokers) Bill 2019 — containing a new bests interest duty obligation on mortgage brokers, as recommended by Commissioner Kenneth Hayne in the final report of the banking royal commission. Via The Adviser.

The bill states that brokers “must act

in the best interests of consumers when giving credit assistance in

relation to credit contracts”, meaning:

where there is a

conflict of interest, mortgage brokers must give priority to consumers

in providing credit assistance in relation to credit contracts,

mortgage

brokers and mortgage intermediaries must not accept conflicted

remuneration — any benefit, whether monetary or non-monetary that could

reasonably be expected to influence the credit assistance provided or

could be reasonably expected to influence whether or how the licensee or

representative acts as an intermediary.

employers, credit

providers and mortgage intermediaries must not give conflicted

remuneration to mortgage brokers or mortgage intermediaries.

The

draft bill, which is open for consultation until 4 October, notes that

the duty to act in the best interests of the consumer in relation to

credit assistance is a “principle-based standard of conduct” and “does

not prescribe conduct that will be taken to satisfy the duty in specific

circumstances”.

“It is the responsibility of mortgage brokers to

ensure that their conduct meets the standard of ‘acting in the best

interests of consumers’ in the relevant circumstances,” the bill states.

According to the bill, the content of the duty “ultimately depends on the circumstances in which credit assistance is provided”.

Examples of such content cited in the draft bill include:

prior

to the recommendation of a credit product, it could be expected that

the mortgage broker consider a range of such products (including the

features of those products) and inform the consumer of that range and

the options it contain,

any recommendations made could be

expected to be based on consumer benefits, rather than benefits that may

be realised by the broker (such as commissions);

in cases

where critical information is not obtained when inquiring about a

consumer’s circumstances, the broker could be expected to refrain from

making a recommendation about a loan where there is a consequent risk

that the loan will not be in the consumer’s best interests;

a

broker would not suggest a white-label home loan that has the same

features as a branded product from the same lender, but with a higher

interest rate, because it would not be in the best interests of the

consumer to pay more for an otherwise similar product; and

during

an annual review, a broker would not suggest that the consumer remain

in a credit contract without considering whether this would be in the

consumer’s best interests.

In addition to the new best

interests obligation, the draft bill requires a mortgage broker to

“resolve conflicts of interests in the consumer’s favour”.

The

bill states that “if the mortgage broker knows, or reasonably ought to

know”, that there is a conflict between the interests of the consumer

and the interests of the broker or a related party, the mortgage broker

“must give priority to the consumer’s interests”.

As an extension

to the best interests duty, the bill builds on remuneration reforms

proposed by the Combined Industry Forum, which includes:

requiring the value of upfront commissions to be linked to the amount drawn down by borrowers instead of the loan amount;

banning campaign and volume-based commissions and payments; and capping soft dollar benefits.

The

proposed regulations also limit the period over which commissions can

be clawed back from aggregators and mortgage brokers to two years and

prohibit the cost of clawbacks being passed on to consumers.

The new provisions are scheduled for implementation by 1 July 2020.