Data from the Digital Finance Analytics Core Market Model tells an interesting story when we look at households dependence on wealth from property.

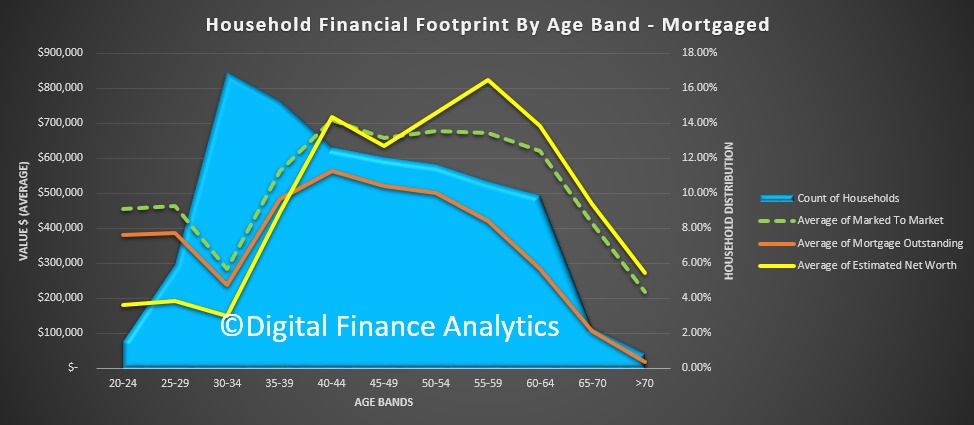

To illustrate the point, here are three charts, looking at different household groups. The first is the owner occupied mortgage group.

The blue area represents the distribution of households by age bands. The yellow line shows the relative value of total net worth (assets less debt, including superannuation). The green dotted line shows the value of property, in today’s terms, and the red line the current mortgage. It is very clear that older Australians have greater net assets and smaller mortgages. It is also clear that much of that worth is from paper profits relating to property. They would take a bath if prices were to fall.

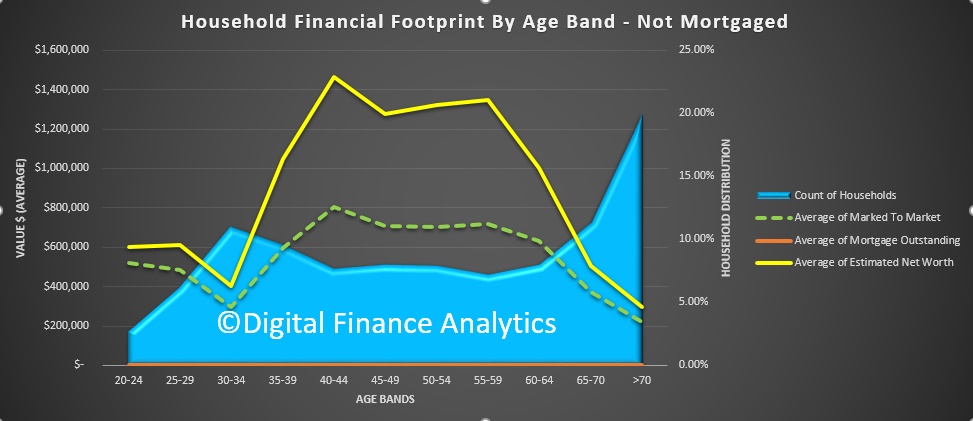

Households without a mortgage have greater worth in other savings vehicles, including shares, deposits and property. They are more insulated from property value falls, and of course would not be hit by rising mortgage rates directly.

Households without a mortgage have greater worth in other savings vehicles, including shares, deposits and property. They are more insulated from property value falls, and of course would not be hit by rising mortgage rates directly.

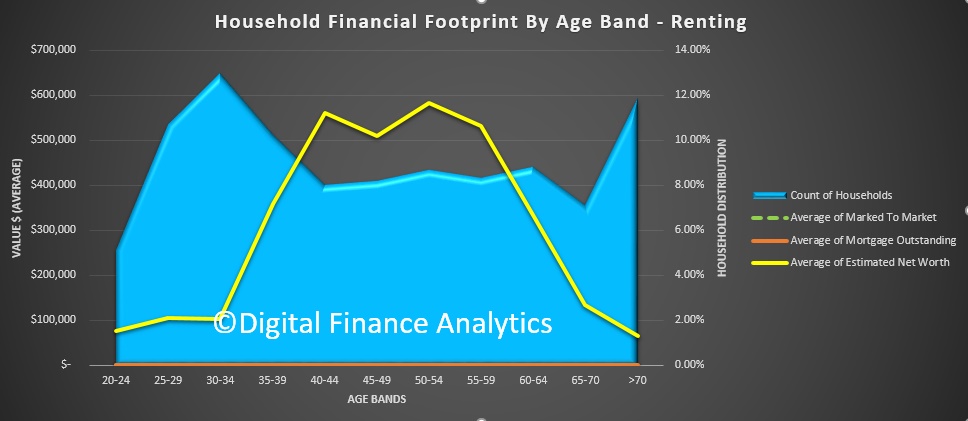

Finally, those who rent have a lower average net worth. Younger renters have little in the way of assets, whereas older renters on average hold higher balances, partly thanks to superannuation.

Finally, those who rent have a lower average net worth. Younger renters have little in the way of assets, whereas older renters on average hold higher balances, partly thanks to superannuation.

The analysis reconfirms how critical property values are to overall net worth. As a nation, we are highly exposed to future price movements. Any correction, whilst it might make property accessible for first time buyers, will seriously erode the net worth of households, especially those in the older age bands. The on-flow to economic outcomes suggests the risks are real, as Phillip Lowe said last night.

The analysis reconfirms how critical property values are to overall net worth. As a nation, we are highly exposed to future price movements. Any correction, whilst it might make property accessible for first time buyers, will seriously erode the net worth of households, especially those in the older age bands. The on-flow to economic outcomes suggests the risks are real, as Phillip Lowe said last night.

One thought on “Property And Household Financial Footprints”