The biggest Australian banks are fairing well in a year of increased pressure to reform from politicians, international events like the Britain’s exit from the European Union and more regulation from the Australian Prudential Regulation Authority (APRA).

A number of interrelated factors have contributed to the relatively strong performance of the Australian banks. For instance, the banks have limited exposure to the types of securities which led to massive losses for their counterparts in other countries. The banks also heavily rely on domestic loans, particularly the low risk household sector, so better lending standards and a proactive approach to prudential supervision by APRA may have contributed.

The Basel III regulatory requirements, brought in after the 2008 financial crisis, emphasise holding an increased amount of subordinated debt, as a measure of market discipline. However all the big four banks are holding less and less subordinated borrowings. More specifically, it declined by more than 50% from 2007 to 2014, according to our calculations.

APRA limits banks’ holdings of higher risk securitised assets, these are loans packaged into securities, to a maximum of 25% of the banks’ loan portfolio. These are high risk if not properly understood or defined, as happened with United States home loans, blamed for the start of the global financial crisis.

When Australian banks calculate bank capital requirements, they need to fully account for securitised assets. This is a rule from APRA that goes beyond international standards, to reflect the risk inherent in these products.

Inter-bank liquidity tightened significantly with all banks increasing their holdings of Exchange Settlements Accounts at the Reserve Bank, this a form of low risk liquidity. Australian banks have lower interbank deposits compared to their Europe and USA counterparts and are also heavily involved in long term wholesale funding and are required to hold more liquid assets including government debt to deal with liquidity. All of this makes Australian banks less risky in times of crisis because spillover effects from other banks are less likely.

There has been a significant increase in concentration in the Australian banking industry since the global financial crisis. For example with Westpac and the Commonwealth Bank of Australia taking over St. George Bank and Bank West, respectively.

Following mergers, the big four account for 88% of the Australian banking system assets. This reinforces the idea that the banks are “too big to fail”.

The banks have also moved to more fee generating activities, which increases risk, but to a lesser extent in Australian banks. Data shows between 1998 and 2014, on average, 1.2% greater interest income was generated relative to non-interest income for Australian banks, according to our analysis. However, there is also similar evidence for the top eight publicly-listed Canadian banks. They exhibit on an average, a 2.5% increase in net interest revenue relative to non-interest income over the same time period.

This reinforces that Australian and Canadian banks demonstrated extra ordinary resilience during the credit turmoil in the global financial crisis. The World Economic Forum in 2008 reported that Australia and Canada were among the top four safest banking systems in the world.

Large banks in Australia are active in international markets through direct ownership of foreign based banks and having offshore operations as a source of capital. Deregulation of banking in countries such as the USA, Canada, Australia and many developing countries has opened up new markets for foreign banks. Australian banks’ largest international exposure is to New Zealand, where all big four banks retain sizeable operations.

Although the growing interdependence among international economies and financial markets is certain to continue, the impact of Brexit on Australian banks remains minimal. It remains to be seen in the long-run how Australian banks will weather the international banking/economic developments.

As a last measure of the bank health, we can measure the domestic systemic risk with a methodology based on one used by the official Basel Committee on Banking Supervision. Based on July 2016 monthly data, the big four banks account for 80.38% of the systemic risk in the financial system and the riskiest, from highest to lowest, are the National Australia Bank, the Commonwealth Bank of Australia, Westpac and ANZ.

ASIC says Australia and New Zealand Banking Group Limited (ANZ) is refunding $28.8 million to 376,570 retail accounts, and 17,230 business accounts, after it failed to clearly disclose when certain periodical payment fees would apply.

Periodical payments are automatic ‘set and forget’ fixed-amount payments put in place by the customer. They are an alternative to direct debit arrangements, and allow customers to establish a regular payment to another account (for example, to make fortnightly rental payments). Banks may charge a fee for this service, depending on the terms and conditions for the account.

In ANZ’s case, the account terms and conditions stated that a periodical payment was a transaction to ‘another person or business.’ This meant that transactions made by the customer to another account in the customer’s own name, whether with ANZ or another financial institution, were not covered by ANZ’s own definition of a periodical payment and could not be charged the fees that could otherwise apply to periodical payments.

ANZ discovered that it was charging fees on payments made between accounts held in the customer’s own name, contrary to its definition of a ‘periodical payment’. ANZ subsequently reported the matter to ASIC as a significant breach of its financial services obligations. ASIC acknowledges the cooperative approach taken by ANZ in its handling of this matter, and its appropriate reporting of the matter to ASIC.

As a result, ANZ will refund fees that were charged to customers for payments into another account in the customer’s own name. These fees include:

non-payment fees charged on personal and commercial accounts when the payment did not proceed because of insufficient funds held in the ANZ deposit account; and

payment fees charged on commercial accoumts when a payment is processed from the ANZ deposit account.

The total amount being refunded includes approximately $25.8 million of fees, with an additional $3 million in interest.

ANZ has subsequently changed its terms and conditions to clarify instances where fees for periodical payments apply to an ANZ deposit account.

ASIC Deputy Chairman Peter Kell said, ‘Good fee disclosure is integral to ensuring that consumers are in an informed position about how best to manage the cost of their banking.’

ANZ has commenced contacting affected customers to explain the impact and the reimbursement and expects to complete the remediation process by the end of September 2016.

In a separate release, ANZ confirmed it has begun refunding around 390,000 accounts in relation to unclear fee disclosures for certain periodical payments. For the majority of impacted accounts, the fee refunds are below $50.

The issue relates to fees being charged for periodical payments to a customer’s own accounts.

ANZ Group Executive Australia Fred Ohlsson said: “When we identify an issue where we haven’t got things right, we will make sure our customers are not left out of pocket.”

“We proactively reported this matter to ASIC and have been working hard to ensure customers are repaid as soon as possible. We’ve already begun making payments to our customers and expect all customers will be refunded by the end of September.

“I’d like to apologise to all our impacted customers for the concern that we know issues like this can cause,” Mr Ohlsson said.

A total of $28 million is being paid that includes fee refunds and around $3 million in additional compensation. ANZ has already refunded around $11 million to 192,000 accounts.

ANZ says after falling in July, job advertisements bounced a solid 1.8% m/m in August and are up 8% over the past year. In trend terms, job ads were up 0.5% m/m, suggesting a moderate pace of labour market improvement.

“The bounce in ANZ job ads in August is an encouraging sign that the improvement in labour market conditions is continuing. The rise in job ads is consistent with the ongoing strength in business conditions and increasing capacity utilisation reported in the business surveys.

The pace of improvement in job ads suggests that labour market conditions are improving moderately. While it does not suggest a rapid turnaround in the unemployment rate, it points to ongoing growth in employment. At current levels, the rate of job ads growth is consistent with employment growing at an annual pace of close to 2% y/y.

Overall, this is consistent with our view that the unemployment rate will slowly improve over the next year, supported by low interest rates and solid business conditions.”

ANZ today announced its Mastercard customers can now use their smartphone to make tap and go payments with Android Pay or Apple Pay.

From today, more than 500,000 ANZ customers with a Mastercard credit card can use contactless payments.

Mastercard was the first in the world to offer contactless payments, and Australians are fast adopters with more than seven out of ten Mastercard transactions now made using contactless technology at over 750,000 terminals across Australia. Consumers are now able to enjoy safe and convenient payments from their devices in store, within apps and soon on the web.

ANZ uses tokenisation security to protect card numbers by never sharing them with the merchant or saving them on the device.

The announcement comes after ANZ became the first major Australian bank to offer Android Pay to customers in July this year and after ANZ this year became the first major Australian bank to offer Apple Pay to customers. ANZ remains the only major Australian bank to offer these services.

ANZ today confirmed Moody’s decision to revise Australia’s macro profile has resulted in a change in the outlook for the major Australian banks, including ANZ, from stable to negative.

Moody’s reaffirmed ANZ’s Aa2 rating moving from Aa2 (Outlook Stable) to Aa2 (Outlook Negative) saying it expected a more challenging operating environment for the banks for the remainder of 2016 and beyond.

The ratings outlook change has not impacted Moody’s rating of ANZ’s baseline credit or counterparty risk assessment.

Moody said that bank profits are likely to be squeezed thanks to low interest and strong competition between lenders, as well as moderately rising credit costs. That said they comment on the strong profitability in the sector, and higher capital ratios.

“While Moody’s expects further capital improvements over time, the timing of such improvements will depend on the global and domestic regulatory agenda.”

ANZ released a trading update for the nine months to 30 June 2016. The results are unaudited. Essentially, in a slower-growth environment, overall revenue is flat, costs are controlled, and bad debts are managable, though consumer delinquencies are rising slightly. No real surprises.

The statutory net profit is $4.3 billion whilst the Cash Profit (“Adjusted Proforma”) was $5.2 billion, down 3%.

The profit before provisions was up 5%, with income increasing at a faster

rate than expenses. Increased technology, D&A and project costs were offset by productivity savings including lower employee (FTE) numbers. FTE reduction continued at a steady rate through the period.

The group Net Interest Margin (NIM) was stable at 2.01% assisted by portfolio rebalancing in Institutional offset by increased funding costs and asset pricing competition.

The total provision charge was $1.4 billion comprised of individual provisions of $1.34 billion and collective provisions of $60 million. The third quarter individual provision charge was in line with the average of the First Half. The 3rd Quarter loan loss charge was circa A$480m and a little higher than expected.

Excluding the payment of the 2016 interim dividend (net of the dividend reinvestment plan), CET1 increased 44 bps in the third quarter, primarily driven by cash earnings generation and capital benefits from the continued reduction of lower return assets in Institutional.

Here is an interview with the CEO Shayne Elliott.

The Retail businesses in both Australia and New Zealand performed well. Retail experienced modest asset growth and margin pressure in a competitive market for mortgages and deposits. Small Business Banking remains an area of good growth in both markets, while conditions in Corporate and Business Banking remained highly competitive.

The re-balancing of the Institutional business continued with further

reductions in lower yielding assets supported by business restructuring.

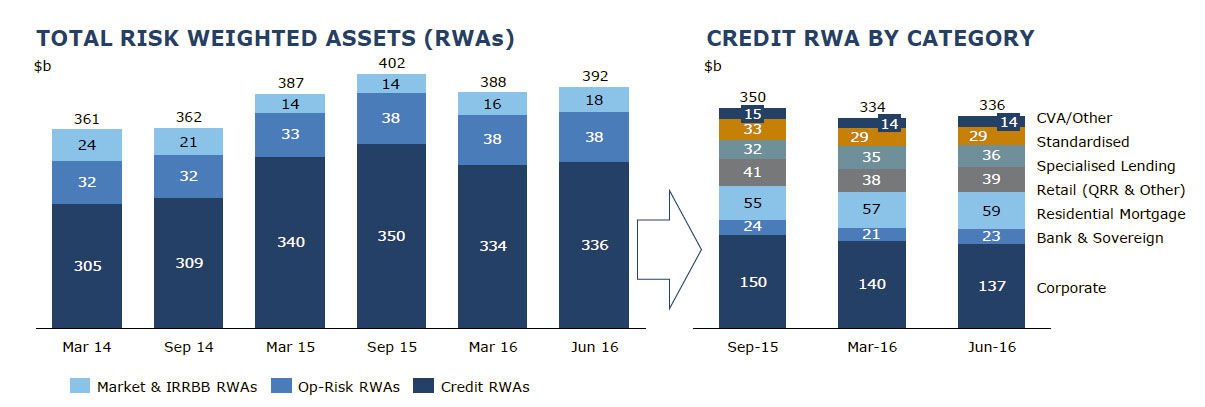

The ongoing focus on reducing and improving the quality of Risk Weighted Assets (RWA) has delivered a $15 billion decrease in Credit Risk Weighted Assets (CRWA) on a constant currency basis. Momentum has been consistent throughout the year to date with approximately a third of that total reduction in CRWA occurring in the third quarter.

Divisional revenue decreased by a lower percentage than the reduction in RWAs. At period end cost growth was in the low single digits benefitting from prior period productivity initiatives. The re-balancing of the business had a positive impact on the Division’s margins of approximately 5 bps (excl Global Markets). Including Global Markets margins declined 5 bps. Global Markets income was $1.5 billion, 90% of which came from Customer Sales flows.

Following the announcement on Friday 5 August 2016 by the Australian Prudential Regulation Authority (APRA) reaffirming its revised average mortgage risk weight targets, ANZ advises that the average credit risk weighting of the Group’s Australian residential mortgage lending book will increase.

The announcement by APRA provided an update on discussions and reviews it is conducting with the authorised deposit taking institutions (ADIs) accredited to use an internal ratings based (IRB) approach to credit risk, regarding refinements to risk models as part of its routine supervisory process. APRA announced that it is recalibrating the impact of refinements to risk models on the required risk weighting for residential mortgages.

The exact increase for ANZ will not be confirmed until ANZ has submitted and had approved its new mortgage capital model, and APRA has completed its recalibration, but is expected to be within the 25% – 30% range recommended by the Financial Services Inquiry. This is expected to be effective in the First Quarter of FY2017.

This follows APRA’s announcement of 20 July 2015 which advised changes to capital requirements for Australian residential mortgage exposures for IRB ADIs in response to a recommendation from the Financial Services Inquiry. The outcome of those changes was, from 1 July 2016 an increase in the average credit risk weighting applied to ANZ’s Australian residential mortgage lending from approximately 15% to approximately 25%.

APRA has, since 2008, sought to strengthen major bank capital ratios through a number of adjustments to Risk Weighted Assets (RWA) across a variety of asset classes and risk types.

This has the effect of the reported capital ratio remaining broadly unchanged despite ADIs increasing the absolute amount of capital held.

While the exact increase for ANZ remains uncertain, the table below sets out the impact of APRA’s previously announced changes and the possible impact of additional risk model changes, on ANZ’s Common Equity Tier-1 position (CET1), based on a credit risk weighting at the mid-point of the 25%-30% range recommended by the Financial Services Inquiry.

On a proforma basis as at 30 June 2016, based on a credit risk weighting at the mid-point of the 25%-30% range, ANZ’s CET1 ratio would be approximately 9.0% and the aggregate capital impact would be offset by the equity raising undertaken by ANZ in August and September 2015.

Any 1% increase or decrease from the mid-point would have an impact on the proforma CET1 ratio of approximately 0.06% and on Common Equity of approximately $250 million. ANZ believes that while the size of any increase in the RWA charge on Australian residential mortgages remains uncertain, it has the ability to meet its current stated capital objectives, including an internationally comparable capital position within the top quartile of international peers and an APRA CET1 ratio of approximately 9%.

ANZ’s previously announced capital plan includes:

Rebalancing the Group’s capital allocation by continuing to reduce the amount of capital allocated to its Institutional Banking business and reviewing certain assets in the portfolio. In 9 months to 30 June 2016, Institutional Banking’ s Credit Risk Weighted Assets have declined by $15 billion (on an FX adjusted basis) and ANZ has completed the sale of its Esanda dealer finance business.

Gradually reverting to the historical Dividend Payout Ratio range of 60-65% of annual Cash Profit as announced at the 1H16 Financial Results. Over time, ANZ expects that these and other initiatives will allow the Group to target a stronger balance sheet and capital structure. However alternatives such as providing a discount to the Dividend Reinvestment Plan (DRP) and/or DRP underwriting could provide additional flexibility if required.

ANZ says job advertisements fell by 0.8% in July. This was the first decline since April and may reflect heightened uncertainty temporarily delaying the hiring plans of some employers. Annual growth in job ads has slowed to 6.9% from 8.0% in the previous month.

The fall in July was driven by both internet and newspaper job ads. Internet job advertisements, which are the main driver of total job ads, declined by 0.7% in July. Annual growth in internet jobs ads slowed from 8.8% in June to 7.9% in July.

The more volatile newspaper ads remain on a structural downward trend and fell further in July, down 12.6% in the month to be 41.7% lower than a year ago.

The labour market has lost some momentum so far in 2016, with slower average growth in both employment and job ads seeing the unemployment rate stabilise around 5¾% after declining in the second half of last year from a peak of 6.3%.

More recently, job ads rebounded strongly in May, followed by a modest rise in June, but these increases have been partly unwound by the decline in July. Given that ads fell sharply in early July, we think this decline may partly reflect the impact of increased uncertainty following the close federal election on 2 July and the shock decision by the UK to leave the European Union on 24 June.

This impact appears to have been short-lived, with job ads picking up over the course of July, and little sustained effect from the increase in uncertainty on business and consumer confidence. For example, the ANZ-Roy Morgan index of consumer sentiment fell about 3% in

the weeks after Brexit and the federal election, but recouped almost all of that fall by the end of July.

With surveyed business conditions remaining upbeat and the RBA cutting rates in August, we look for a gradual improvement in hiring intentions over the remainder of the year

ANZ today announced the Standard Variable Rate Indices for Residential Home Loan products will decrease by 0.12%pa, while increasing the rate on its one and two-year term deposits by up to 0.75%pa.

All Standard Variable Rate Indices for Residential Home Loan products to decrease by 0.12%pa. For Owner Occupiers this reduces the Index Rate to 5.25%pa; Residential Investor Index Rate reduces to 5.52%pa. All business lending variable rate indices will decrease by 0.10%pa. Deposit rate special for popular one-year Advanced Notice Term Deposit to increase by 0.60%pa to 3.00%pa; two-year term deposit to increase 0.75%pa to 3.20%pa with both effective 5 August.

ANZ Group Executive Australia Fred Ohlsson said: “This was a considered decision that balances the expectations of our home loan customers to keep lending rates as low as possible, while also supporting our savings customers who help fund our lending.

“Regulatory and funding costs have continued to rise and we need to remain attractive to depositors. We are pleased however that home loan customers can still benefit from these historically low interest rates and that we have maintained a competitive rate for both owner occupiers and investors.

“Customers concerned about the long-term direction of rates are able to take advantage of our highly competitive fixed rates that are now at historical lows, including our rate of 3.75%pa* fixed for two years,” Mr Ohlsson said.

ANZ today announced it is exploring strategic options for ANZ Share Investing that may include a sale of its share trading platform.

As part of this process, ANZ has issued an Information Memorandum to a number of international and domestic specialist providers.

ANZ Managing Director Pensions & Investments Peter Mullin said: “ANZ is committed to providing customers with access to a market leading share trading platform at a competitive price.

“As we have seen with ANZ’s recent introduction of Apple Pay and Android Pay, the days of a bank needing to own every piece of technology are gone.

“We believe we can achieve better outcomes for our customers by partnering with a specialist provider committed to the technology investment and product innovation needed to provide a world-class offering.

“The process is expected to take a number of months to finalise and in the meantime it’s business as usual for both our customers and staff,” Mr Mullin said.

“The bounce in ANZ job ads in August is an encouraging sign that the improvement in labour market conditions is continuing. The rise in job ads is consistent with the ongoing strength in business conditions and increasing capacity utilisation reported in the business surveys.

From today, more than 500,000 ANZ customers with a Mastercard credit card can use contactless payments.

From today, more than 500,000 ANZ customers with a Mastercard credit card can use contactless payments. Moody’s reaffirmed ANZ’s Aa2 rating moving from Aa2 (Outlook Stable) to Aa2 (Outlook Negative) saying it expected a more challenging operating environment for the banks for the remainder of 2016 and beyond.

Moody’s reaffirmed ANZ’s Aa2 rating moving from Aa2 (Outlook Stable) to Aa2 (Outlook Negative) saying it expected a more challenging operating environment for the banks for the remainder of 2016 and beyond.

APRA Level 2 Common Equity Tier 1 (CET1) ratio was a strong 9.7% at 30 June. However, it would fall under the higher IRB mortgage risk weighting.

APRA Level 2 Common Equity Tier 1 (CET1) ratio was a strong 9.7% at 30 June. However, it would fall under the higher IRB mortgage risk weighting.

On a proforma basis as at 30 June 2016, based on a credit risk weighting at the mid-point of the 25%-30% range, ANZ’s CET1 ratio would be approximately 9.0% and the aggregate capital impact would be offset by the equity raising undertaken by ANZ in August and September 2015.

The labour market has lost some momentum so far in 2016, with slower average growth in both employment and job ads seeing the unemployment rate stabilise around 5¾% after declining in the second half of last year from a peak of 6.3%.

All Standard Variable Rate Indices for Residential Home Loan products to decrease by 0.12%pa. For Owner Occupiers this reduces the Index Rate to 5.25%pa; Residential Investor Index Rate reduces to 5.52%pa. All business lending variable rate indices will decrease by 0.10%pa. Deposit rate special for popular one-year Advanced Notice Term Deposit to increase by 0.60%pa to 3.00%pa; two-year term deposit to increase 0.75%pa to 3.20%pa with both effective 5 August.

All Standard Variable Rate Indices for Residential Home Loan products to decrease by 0.12%pa. For Owner Occupiers this reduces the Index Rate to 5.25%pa; Residential Investor Index Rate reduces to 5.52%pa. All business lending variable rate indices will decrease by 0.10%pa. Deposit rate special for popular one-year Advanced Notice Term Deposit to increase by 0.60%pa to 3.00%pa; two-year term deposit to increase 0.75%pa to 3.20%pa with both effective 5 August. As part of this process, ANZ has issued an Information Memorandum to a number of international and domestic specialist providers.

As part of this process, ANZ has issued an Information Memorandum to a number of international and domestic specialist providers.