Just before Christmas APRA advised the imposition of a 1% Counter Cyclical Capital Buffer on Australian Banks. Interesting timing, seeing as the Bank For International Settlements had set 2023 as the required date. Up to this point APRA has argued a 1% buffer was not needed in Australia – so what changed?

So, we wonder, are they being forced to comply. and what does this mean for our “strong” banks as interest rates rise and lending slows?

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

The Australian Prudential Regulation Authority (APRA) today announced temporary changes to its expectations regarding bank capital ratios, to ensure banks are well positioned to continue to provide credit to the economy in the current challenging environment.

Over the past decade, the Australian banking system has built up substantial capital buffers. The highest quality form of capital, Common Equity Tier 1 (CET1) capital, reached $235 billion at the end of 2019. As a result, banks are typically maintaining capital levels well above minimum regulatory requirements.

In 2017, APRA set benchmark capital targets for banks to enable them to be regarded internationally as unquestionably strong (which was a recommendation of the 2014 Financial System Inquiry). These benchmarks are well above current minimum regulatory requirements. For the four major banks, for example, this benchmark equated to having a CET1 ratio of at least 10.5 per cent of risk-weighted assets. A lower benchmark applies for smaller banks. In comparison, the actual CET1 ratio of the banking system by the end of 2019 had reached 11.3 per cent.

APRA is advising all banks today that, given the prevailing circumstances, it envisages they may need to utilise some of their current large buffers to facilitate ongoing lending to the economy. This is especially the case for banks wishing to take advantage of new facilities announced today by the Reserve Bank of Australia to promote the continued flow of credit. Provided banks are able to demonstrate they can continue to meet their various minimum capital requirements, APRA would not be concerned if they were not meeting the additional benchmarks announced in 2016 during the period of disruption caused by COVID-19.

APRA Chair Wayne Byres said: “APRA has been pursuing a program to build up the financial strength of the system for many years, when banks had the capacity to do so. As a result, the Australian banking system is well-capitalised by both historical and international standards.

“APRA’s objective in building up this capital strength has been to ensure it is available to be drawn upon if needed in times such as this. Today’s announcement reflects the underlying strength of the system: even if the banking system utilises some of its current large buffers, it will still be operating comfortably above minimum regulatory requirements,” Mr Byres said.

On 4 March, the Federal Reserve Board (Fed) finalized changes to its capital rules for US banks with assets greater than $100 billion. Via Moody’s.

The final changes increase the flexibility banks have to payout capital more aggressively and will likely give bank management greater leeway to reduce the size of their management buffers and operate with capital ratios closer to the minimum levels required.

The final version establishes a stress capital buffer (SCB) that incorporates the Fed’s stress test results into its regulatory Pillar 1 capital requirements for these banks. Originally proposed in April 2018, the final rule includes a number of changes that weaken the original, making it credit negative for all US banks covered by the rule.

The Fed’s impact analysis of the final rule suggests that in aggregate the Common Equity Tier 1 (CET1) capital requirements at the affected US banks could decline up to $59 billion: $6 billion at the eight US global systemically important banks (G-SIBs) and $35 billion at the rest. Since most banks currently hold a management buffer above existing requirements, the affected banks could actually cut their CET1 capital by twice this amount and still comply with the final rule. The CET1 capital reduction could be $40 billion (a 5% decline) at the G-SIBs, $50 billion (a 21% decline) at other banks with $250 billion or more in assets, and $35 billion (a 16% decline) at banks with assets between $100 and $250 billion.

Consistent with the proposal, the final rule integrates stress testing into the Fed’s regulatory capital requirements by replacing the capital conservation buffer, which is currently 2.5%, with the SCB. The SCB will be the higher of either 2.5%, or the difference between the starting and minimum projected CET1 capital ratio under the severely adverse scenario of the Fed’s Dodd-Frank Act Stress Test (DFAST) plus four quarters of planned common stock dividends.

Starting in October 2020, if a bank’s risk-based capital ratios fall below the aggregate of the minimum capital requirement plus the SCB, the relevant G-SIB surcharge, and the countercyclical capital buffer (if any), restrictions would apply to capital payouts and certain discretionary bonus payments. As in the proposal, the final rule changes the current annual Comprehensive Capital Analysis and Review (CCAR) and DFAST process.

The final rule eliminates the assumption that a bank’s balance sheet and risk-weighted assets will grow under the stress scenarios, eliminates the Fed ability to object on quantitative grounds to a bank’s capital plan, and removes the 30% dividend payout ratio as a threshold for heightened scrutiny of a bank’s capital plan. Both the flat balance sheet assumption and the requirement that banks hold capital for only four quarters of dividends rather than for the full amount of planned payouts over the stress test horizon lower capital requirements versus the current stress testing regime.

The decrease is only partially offset for G-SIBs by the first-time inclusion of the G-SIB surcharge within the Fed’s stress test.

The final rule is weaker than the original proposal for several reasons. Under the proposal, banks would not have been allowed to pay out capital in excess of their approved capital plans without Fed prior approval. In the final rule, banks can in most cases make payouts in excess of amounts in their capital plan, provided the payout is otherwise consistent with the payout limitations in the final rule.

Additionally, the final rule modifies payout limitations to allow firms with an SCB in excess of 2.5% to pay a greater portion of their dividends and management bonuses and to repurchase shares for a period of time after capital ratios fall below the requirement. And in the final rule, the SCB, unlike the DFAST capital requirements, will not incorporate material business plan changes, such as those resulting from a merger or acquisition. As a result, such actions will only affect a bank’s capital ratio once the action has occurred.

The final rule also excludes the originally proposed stress leverage buffer requirement, which would not have been a binding constraint for most banks. Its elimination from the final rule removes this requirement as a potential backstop. And without the stress leverage buffer, the still pending proposal to modify the supplementary leverage ratio for the eight G-SIBs by tying it more closely to the G-SIB surcharge could further weaken the ability of the leverage ratio to serve as a backstop requirement and would also be credit negative.

The US Federal Reserve Board on Wednesday approved a rule to simplify its capital rules for large banks, preserving the strong capital requirements already in place.

The “stress capital buffer,” or SCB,

integrates the Board’s stress test results with its non-stress capital

requirements. As a result, required capital levels for each firm would

more closely match its risk profile and likely losses as measured via

the Board’s stress tests. The rule is broadly similar to the proposal

from April 2018, with a few changes in response to comments.

“The stress capital buffer materially

simplifies the post-crisis capital framework for banks, while

maintaining the strong capital requirements that are the hallmark of the

framework,” Vice Chair for Supervision Randal K. Quarles said.

The SCB uses the results from the Board’s

supervisory stress tests, which are one component of the annual

Comprehensive Capital Analysis and Review (CCAR), to help determine each

firm’s capital requirements for the coming year. By combining the

Board’s stress tests—which project the capital needs of each firm under

adverse economic conditions—with the Board’s non-stress capital

requirements, large banks will now be subject to a single,

forward-looking, and risk-sensitive capital framework. The

simplification would result in banks needing to meet eight capital

requirements, instead of the current 13.

The SCB framework preserves the strong

capital requirements established after the financial crisis. In

particular, the changes would increase capital requirements for the

largest and most complex banks and decrease requirements for less

complex banks. Based on stress test data from 2013 to 2019, common

equity tier 1 capital requirements would increase by $11 billion in

aggregate, a 1 percent increase from current capital requirements. A

firm’s SCB will vary in size throughout the economic cycle depending on

several factors, including the firm’s risks.

To reduce the incentive for firms to take

on risk and further simplify the framework, the final rule does not

include a stress leverage buffer as proposed. All banks would continue

to be subject to ongoing, non-stress leverage requirements.

Large banks have substantially increased

their capital since the first round of stress tests in 2009. The common

equity capital ratio of the banks in the 2019 CCAR has more than doubled

from 4.9 percent in the first quarter of 2009 to 12.2 percent in the

fourth quarter of 2019, with total capital doubling to more than $1

trillion.

Also on Wednesday, the Board released the

instructions for the 2020 CCAR cycle. The instructions confirm that 34

banks will participate in this year’s test. CCAR consists of both the

stress tests that assess firms’ capital needs under stress and, for the

largest and most complex banks, a qualitative evaluation of the

practices these firms use to determine their capital needs in normal

times and under stress. Results will be released by June 30.

APRA remains in a low risk bubble, according to their paper today, which keeps the counter-cyclical buffer at 0. However they flag that may change ahead. I have to say this seems perverse, given the high debt levels and low economic performance and increased risks. Plain weird, and a million miles off the Reserve Bank NZ’s approach.

The Australian Prudential Regulation Authority (APRA) has decided to keep the countercyclical capital buffer (CCyB) for authorised deposit-taking institutions (ADIs) on hold at zero per cent, but has flagged the likelihood of a non-zero default level in the future.

The CCyB is an additional amount of capital that APRA can require ADIs to hold at certain points in the economic cycle to bolster the resilience of the banking sector during periods of heightened systemic risk. It has been set at zero per cent of risk-weighted assets since it was introduced in 2016.

In its annual information paper on the CCyB, APRA today confirmed it considers that a zero per cent CCyB remains appropriate at this point in time based on an assessment of the systemic risk environment for ADIs.

Among the factors APRA considered in making its decision were:

low credit growth;

minimal change in the risk profile of new housing lending;

movements in residential property prices, particularly recent growth; and

increased entity costs due to operational risk events and misconduct.

After carefully examining

these dynamics, APRA concluded that the current policy setting remains

appropriate.

In conjunction with the other agencies on the Council of Financial Regulators,

APRA will continue to closely monitor financial and economic conditions. APRA

reviews the buffer quarterly, and may adjust it if future circumstances warrant

this.

However, the information paper notes that APRA is also giving consideration to

introducing a non-zero default level for the CCyB as part of its broader

reforms to the ADI capital framework.

APRA Chair Wayne Byres said: “Given current conditions, and the financial strength

built up within the banking sector, a zero counter-cyclical buffer remains

appropriate.

“However, setting the countercyclical capital buffer’s default position at a

non-zero level as part of the ‘unquestionably strong’ framework would not only

preserve the resilience of the banking sector, but also provide more

flexibility to adjust the buffer in response to material changes in financial

stability risks. This is something APRA will consult on as part of the next

stage of the capital reforms currently underway.

“Importantly, this would be considered within the capital targets previously

announced – it does not reflect any intention to further raise minimum capital

requirements.”

APRA expects to commence the next stage of its ADI capital consultation in the

first half of next year. APRA’s revised capital framework is currently

scheduled to come into effect from 1 January 2022.

According to Moody’s, on 5 December, the Reserve Bank of New Zealand (RBNZ) announced the finalisation of its capital requirements for New Zealand banks. The RBNZ’s decision to raise capital requirements – although slightly watered down from its earlier proposal – is broadly credit positive, because it will make the banking system more resilient to shocks. At the same time, the higher capital requirements will weigh on the banks’ return on equity. We expect the new measures will prompt higher lending rates in efforts to boost profitability and constrain growth in more capital-intensive lending.

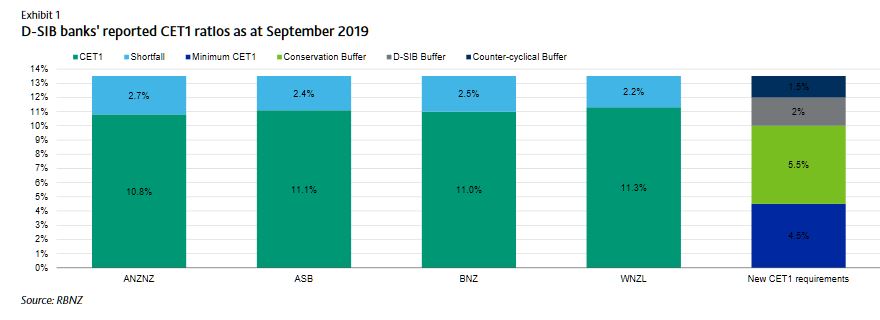

For domestic systemically important banks (D-SIBs), which are New Zealand’s four largest banks, ANZ Bank New Zealand Limited, ASB Bank Limited, Bank of New Zealand, and Westpac New Zealand Limited, the Common Equity Tier 1 (CET1), Tier 1 and Total Capital requirements have risen to 13.5%, 16% and 18% of risk weighted assets (RWA), respectively. While the new rules are a slight relaxation from the RBNZ’s initial proposal of 14.5%, 16% and 18% announced in December 2018, they represent a significant increase from the current requirements of 7%, 8.5% and 10.5%. For all other banks, the CET1, Tier 1 and total capital ratio requirements will be 11.5%, 14% and 16%, respectively.

The RBNZ also announced that existing Additional Tier 1 and Tier 2 securities will no longer count towards regulatory capital. Replacing them will be redeemable, perpetual, preference shares and subordinated debt, provided these securities do not have any contractual contingent features such as conversion or write-off at the point of non-viability.

The higher requirements will be implemented by maintaining a regulatory minimum Tier 1 ratio of 7%, of which 4.5 percentage points must be CET1 capital, and introducing a number of prudential capital buffers, which total 9 percentage points (see Exhibit 1). Under the new framework, banks can temporarily operate below 13.5%, but above 4.5%, without triggering a breach of regulatory requirements. However, they will be subject to more intensive supervision and other consequences such as dividend restrictions. On average, the D-SIB CET1 ratios are around 2.5 percentage points lower than the new requirement of 13.5% (Exhibit 1).

The RBNZ is also limiting the difference between the calculation of RWAs by D-SIBs, which use the internal ratings based approach (IRB), and other banks that use the Standardised approach. This will be done by recalibrating the calculation IRB banks’ RWAs to around 90% of the outcome under the Standardised approach. The combination of higher capital ratio targets and higher RWAs imposed on D-SIBs could spur more competition by reducing some of the capital advantage previously enjoyed by banks using the IRB approach.

The new capital regime will take effect from 1 July 2020 and the banks will have up to seven years to meet the new rules, an increase from the five years initially proposed. The RBNZ’s decision to extend the transition period will ensure banks are well placed to meet the new targets, especially given the Australian Prudential Regulation Authority’s (APRA) recent changes to Australian Prudential Standards (APS) 222 to further restrict how much equity support Australia’s largest banks can provide to their New Zealand subsidiaries, and proposed changes to APS 111, which will increase the capital requirements of providing such support.

The Australian parents of the New Zealand D-SIBs Australia and New Zealand Banking Group Limited, Commonwealth Bank of Australia, National Australia Bank Limited, and Westpac Banking Corporation have all disclosed the estimated impact of the new rules (Exhibit 2).

The additional capital requirements imposed on the big four by the Reserve Bank of New Zealand has seen analysts downgrade their forecasted return on equity across the major institutions. Via InvestorDaily.

The Reserve Bank of New Zealand (RBNZ)

has demanded the local arms of the big four raise their total capital

ratio from a minimum of around 10.5 per cent to 18 per cent over the

next seven years. The central bank had previously estimated that this

would see a collective raise of around $19.1 billion.

Currently, banks in New Zealand hold an average of around 14.3 per cent.

According

to an analysis from Morningstar, the big four’s raise will be a

combined $12.4 billion (NZ$13 billion) to meet the new tier 1 capital

requirements amounting to 16 per cent of risk weighted assets, versus

the current 8.5 per cent.

S&P Global has placed the figure at around $15.7 billion (NZ$16.4 billion).

The

changes, which come into effect from next year, have been made to

protect consumers against loan losses and to prevent the banks from

reaching a point of failure.

But the

time frame is key, as the central bank extended it from its original

proposed five years for the raise to soften any economic shocks.

Morningstar said the longer period will see banks organically retaining

additional capital from earnings, instead of triggering equity raisings

or dividend cuts.

Analysts at the

investment bank expect the Australian majors to respond to the new

measures by repricing loans and deposits and by reducing exposure to

higher-risk sectors and borrowers.

Further,

S&P Global noted the implementation of the measures should not

materially reduce the availability of credit in New Zealand, but the

banks could cut lending to customer segments that would require

increased regulatory capital.

“RBNZ’s

initiatives strengthen bank-capital levels, which provides a greater

buffer to manage a potential increase in loan losses,” the Morningstar

analysis read.

It has made no changes

to its earnings forecasts or valuations of the banks, however, despite

expecting the summation of flat or slightly higher loan books and higher

net interest margins will lead to moderately lower cash NPATs across

the New Zealand divisions.

“The effect on group earnings is immaterial though,” Morningstar said.

“The drag on the banks’ returns on equity is larger.”

The

assessment has predicted a reduction in return on equity for CBA by 46

basis points to 14.8 per cent, Westpac by 22 basis points to 11.4 per

cent, ANZ by 16 basis points to 11.5 per cent and NAB by 36 basis points

to 11.3 per cent.

S&P Global has said likewise, expecting ROE to “considerably decline”.

The

Morningstar analysts also believe the major banks can maintain current

dividend levels, but retaining a greater portion of New Zealand profits

leaves less headroom to offset unexpected hits on earnings or capital.

Westpac

and NAB have slashed their dividend payouts, and ANZ cut its dividend

franking level recently, reflecting impacts on profit from unexpected

remediation.

ANZ in particular is

raising capital at the group level to meet the RBNZ rules, holding a

larger investment in its New Zealand division than the other banks.

None of the other banks have indicated any intention to raise capital, but the possibility remains in the future.

“Seven

years is a long time, and this view will need to be reviewed as the

banks’ strategic response takes shape,” the Morningstar analysts stated.

“The

New Zealand operations of the banks will remain highly profitable

despite the additional capital, hence we do not expect a divestment to

be on the cards.”

The Reserve Bank of New Zealand today released its final decisions following its comprehensive review of its capital framework for banks, known as the Capital Review. The trajectory will be over a longer period, with more flexibility, but the banks will still need to hold more capital.

Governor Adrian Orr said the

decisions to increase capital requirements are about making the banking system

safer for all New Zealanders, and will ensure bank owners have a meaningful

stake in their businesses. The changes will be implemented over seven years,

giving plenty of time for banks to manage a smooth transition and minimise any

adjustment costs.

“Our decisions are not just

about dollars and cents. More capital in the banking system better enables

banks to weather economic volatility and maintain good, long-term, customer

outcomes,” Mr Orr says.

“More capital also reduces

the likelihood of a bank failure. Banking crises cause not only harmful

economic costs but also distressful social issues, such as the general decline

in mental and physical health brought about by higher rates of unemployment.

These effects are felt for generations,” Mr Orr says.

The key decisions, which start to take effect from 1 July 2020, include banks’ total capital increasing from a minimum of 10.5% now, to 18% for the four large banks and 16% for the remaining smaller banks. The average level of capital currently held by banks is 14.1%.

Relative to the Reserve

Bank’s initial proposals, the final decisions also include:

More flexibility for banks on the use of specific capital instruments;

A more cost-effective mix of funding options for banks;

A lesser increase in capital for the smaller banks consistent with their more limited impact on society should they fail;

A more level capital regime for all banks – with the four large banks having to measure the risks of their exposures (lending) more conservatively, more in line with the smaller banks; and

More transparency in capital reporting.

The adjustments to the original proposals reflect our analysis and industry feedback over the past two years. All of these changes will be phased in over a seven-year period, rather than over five years as originally proposed, in order to reduce the economic impacts of these changes.

Deputy Governor and General

Manager of Financial Stability Geoff Bascand says the decisions were shaped by

valuable public input and insight received through an unprecedented number of

submissions as well as public focus groups. Three international experts also

provided supportive perspectives on the proposals.

“We’ve listened to feedback

and reviewed all the data, and are confident the decisions are the right ones

for New Zealand,” Mr Bascand says.

“We have amended our

original proposals in a number of ways so we achieve a high level of resilience

at lower potential cost, with a smoother transition path for all participants.

Our analysis shows that the benefits of these changes will greatly outweigh any

potential costs.”

“Following the Global

Financial Crisis, many regulators around the world have been taking steps to

improve the safety of their banking systems. We’re confident we have the

calibrations right for New Zealand conditions. These changes will be subject to

monitoring, with the Reserve Bank reporting publicly on implementation during

the transition period,” Mr Bascand says.

On 19 November, the US Federal Reserve, the Comptroller of the Currency, and the Federal Deposit Insurance Corporation approved a final capital rule for the largest US banks that requires them to adopt the standardized approach for counterparty credit risk (SACCR).

The rule must be adopted by those US banks which are mandated to use the Basel III advanced approaches (i.e., advanced internal ratings-based); other US banks may voluntarily adopt it. The advanced approaches banks include the eight US global systemically important banks: Bank of America, The Bank Of New York Mellon, Citigroup, Goldman Sachs, JPMorgan Chase & Co, Morgan Stanley State Street Corporation, and Wells Fargo & Company, as well as Capital One, Northern Trust Corporation, PNC Financial Services Group, and U.S. Bancorp. Many of these entities are also benefitting from the Fed’s Repo operations, which are designed to provide additional liquidity.

Moody’s says as originally proposed, SACCR would have resulted in a modest increase in risk-based capital requirements for the largest US banks but a modest decline in their leverage ratio requirements. However, in the final rule US regulators made several revisions to the original proposal which we expect will reduce both capital requirements, a credit negative.

The final rule is effective on 1 April 2020, with a mandatory compliance date of 1 January 2022. In 2014 the Basel Committee on Banking Supervision adopted SACCR as an amendment to the Basel III framework and in October 2018 US regulators proposed requiring the largest US banks to use SACCR for calculating their derivatives exposure amounts. SACCR is a more risk-sensitive approach to risk-weighting counterparty exposures than the current method and also revises certain calculations related to cleared derivatives exposures, including the measurement of off-balance-sheet exposures related to derivatives included in the denominator of the supplementary (i.e., Basel III) leverage ratio (SLR).

In the final rule, US regulators have made certain revisions to the original proposal, including reducing capital requirements for derivative contracts with commercial end-user counterparties and allowing for the exclusion of client initial margin on centrally cleared derivatives held by a bank on behalf of its clients from the SLR denominator.

Regulators explained that the reduction in capital requirements for exposures to commercial end-users is consistent with congressional and other regulatory actions intended to mitigate the effect of post-crisis derivatives reforms on the ability of such counterparties to manage risks. Additionally, the exclusion of client initial margin on centrally cleared derivatives is consistent with the G20 mandate to establish policies that encourage the use of central clearing. The revisions may also prevent cross jurisdictional regulatory arbitrage because they would align the US with regulations in the UK and Europe on this matter, which are key jurisdictions where many of the largest US banks operate.

Nevertheless, a reduction in capital requirements would allow firms to increase their capital payouts or add incremental risk in other businesses without needing to hold more capital. Regulators estimate that the final rule would result, on average, in an approximately 9% decrease in large US banks’ calculated exposure amount for derivatives contracts and a 4% decrease in their standardized riskweighted assets associated with derivative exposures. The final rule would also lead to an increase of approximately 37 basis points (on average) in banks’ reported SLRs. If all 12 US banks subject to this rule were to maintain their SLRs at current levels instead of letting them rise as they would under the final rule, it would lead to the removal of approximately $55 billion in Tier 1 capital from the US banking system.

Regulators also estimated that the final rule would lead to changes in individual banks’ SLRs, ranging from a decrease of five basis points to an increase of 85 basis points. Regulators did not identify which bank would receive the largest benefit. Moody’s estimate that if one of the six largest US banks is the beneficiary of an 85-basis-point increase in its SLR and the SLR was previously its binding capital constraint, allowing it to return to its shareholders an amount of capital equal to the entire benefit, it would lead to a reduction of between $9 billion and $25 billion in capital at just one bank.

In addition, on 19 November, US banking regulators published a final rule that amends the supplementary leverage ratio calculation to exclude custody bank holdings of central bank deposits. The change will only apply to The Bank of New York Mellon, State Street Corporation and Northern Trust Corporation.

Although the amended calculation is credit negative because it will allow custody banks to reduce capital and still meet one of their regulatory requirements, the practical effect is limited because other regulatory capital measures, specifically post-stress capital requirements, constrain the banks.

The final rule reflects the implementation of Section 402 of the 2018 Economic Growth, Regulatory Relief and Consumer Protection Act (EGRRCPA). Although EGRRCPA primarily aims to reduce regional and community banks’ regulatory burden, it also identifies central bank deposits held by custody banks as unique. In particular, custody banks maintain significant cash deposits with central banks to manage client cash fluctuations linked to custody and fiduciary accounts. Typically, these client cash positions are funds awaiting distribution or investment, but they can spike significantly in times of stress when custodial clients liquidate securities.

Under the final rule, only the Federal Reserve, the European Central Bank or central banks of Organization for Economic Cooperation and Development member countries that have been assigned a zero risk weight under regulatory capital rules are considered qualifying central banks. The rule also defines a custody bank as any US depository institution holding company with assets under custody to total assets of greater than 30:1. This ratio precludes other large custody providers also subject to the supplementary leverage ratio, such as JPMorgan Chase & Co., from excluding central back deposits in their capital calculation, because unlike the three qualifying firms they are not predominantly engaged in custody and asset servicing.

Looked at in isolation, the final rule would allow BNY Mellon, State Street and Northern Trust to reduce their Tier 1 capital by roughly $8 billion in aggregate – a significant 17% reduction – and still maintain the same supplementary leverage ratios. However, that ratio is just one of many capital requirements.

Indeed, regulators’ own analysis of the supplementary leverage ratio revisions, based on 2018 data, indicates that the final rule is unlikely to reduce Tier 1 capital for any of the three affected holding companies because other capital requirements are more binding.

Specifically, performance of the banks’ capital requirements under the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) process has constrained them.

The future course of the custody banks’ capital positions is not yet clear because other aspects of the US regulatory capital framework remain in flux. In particular, regulators are developing a stress capital buffer, which we expect will be incorporated into the CCAR process. On balance, we anticipate that the custody banks are likely to face a capital regime that is less restrictive, though the extent of capital relief is still uncertain.

However, the banks’ reduced supplementary leverage ratio requirement is an early indication of the likely trajectory.

The New Zealand Reserve Bank has increased its supervisory monitoring of the Bank of New Zealand (BNZ) and applied precautionary adjustments to its capital requirements following the identification of weaknesses in BNZ’s capital calculation processes.

BNZ identified a number of

errors while undertaking a programme of remediation, which began in early 2018

and is expected to continue into 2020. These included three capital calculation

errors, which resulted in misreported risk weighted assets over a number of

years.

It is now required to

increase the risk weight floor of its operational risk capital model from $350

million to $600 million capital. The $250m increase is a supervisory capital

overlay.

The Reserve Bank requires

banks to maintain a minimum amount of capital, which is determined relative to

the risk of each bank’s business. BNZ has not been in breach of minimum capital

requirements at any point.

“However given the

likelihood that further compliance issues will be discovered during the review

and remediation, the Reserve Bank regards a precautionary capital adjustment as

prudent,” Deputy Governor Geoff Bascand says.

In 2017, the Reserve Bank

conducted a review of bank director attestation processes and noted that many

banks were attesting to compliance on the basis of negative assurance, ie they

did not have evidence to suggest that they were not in compliance.

Breaches are now being

identified as banks review their governance, control and assurance processes

and move from a negative assurance to a positive evidence-based assurance

framework. Over the past year, a number of banks have disclosed breaches of

their conditions of registration, Mr Bascand says. Many of these have related

to errors in the calculation of their regulatory capital or liquidity which, in

some cases, have gone undetected for a number of years.

“We are reassured by BNZ’s response to the issues along with the independent oversight from PWC,” Mr Bascand says. “BNZ has committed to providing the Reserve Bank with regular and timely updates of the details of issues as they are discovered and the remedial activity as this work progresses. “The additional capital overlay will be removed when remediation is complete. It is the Reserve Bank’s expectation that the current review will identify all outstanding compliance issues and potential breaches.”