My latest Friday chat with journalist Tarric Brooker @AvidCommentator on Twitter. We look at the latest economic and financial news, and consider the consequences.

Tarric’s slides are available at: https://avidcom.substack.com/p/charts-that-matter-10th-june-2022

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Welcome To The Danger Zone: With Tarric Brooker [Podcast]

The RBA Financial Stability Report includes a warning about high household debt AND home price falls. But their “new” model is proposing a less powerful relationship between prices and interest rate moves than their previous one (which was built at a time lower rates were expected…) I smell a rat…

They suggest 15% falls over a couple of years if interest rates rise by 2%, whereas the previous model was ~28% for 1% change.

Pretty convenient eh?

Go to the Walk The World Universe at https://walktheworld.com.au/

The RBA released their Financial Stability Review today, and we look over the main points and highlight some of the issues. https://www.rba.gov.au/publications/fsr/2021/oct/

There is a risk of excessive borrowing due to low interest rates and rising house prices. Most borrowers’ income has recovered, but others may struggle with loan repayments.

Go to the Walk The World Universe at https://walktheworld.com.au/

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s main financial regulatory agencies. There are four members: the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor chairs the Council and the RBA provides secretariat support. It is a non-statutory body, without regulatory or policy decision-making powers. Those powers reside with its members. The Council’s objectives are to promote stability of the Australian financial system and support effective and efficient regulation by Australia’s financial regulatory agencies. In doing so, the Council recognises the benefits of a competitive, efficient and fair financial system. The Council operates as a forum for cooperation and coordination among member agencies. It meets each quarter, or more often if required.

This is the source of the Australian financial regulatory group-think and underscores connection between the “independent” central bank and Treasury! The CFR has recently started publishing updates on its activities. This is the latest. We need an inquiry into the regulatory system, something which was missing from the Hayne Royal Commission, by design.

At its meeting on 18 September 2019, the Council of Financial Regulators (the Council) discussed risks facing the Australian financial system, regulatory issues and developments relevant to its members. The main topics discussed included the following:

Financing conditions and the housing market. Council members discussed credit conditions and recent developments in the housing market. Housing credit growth has been subdued, particularly growth in credit to investors. The major banks have seen slower growth relative to other lenders. Subdued credit growth has been primarily driven by weaker credit demand, though loan approvals have picked up recently. The potential for risks to financial stability from falling housing prices in Sydney and Melbourne has abated somewhat, with prices rising in the past few months. In contrast, prices have continued their prolonged decline in Western Australia and the Northern Territory and so the prevalence of negative equity for borrowers in those regions has continued to rise. The Council also discussed the continuing tight credit conditions for small businesses, with little growth in credit outstanding over the past year. The Council will continue to closely monitor developments.

Members discussed progress with updating the guidance

regarding responsible lending provisions in the National Consumer Credit

Protection Act 2009. The updated guidance should provide greater clarity about

what is required for a lender to comply with its obligations, taking into

consideration enhancements to lending practices, the impact of competition from

new market entrants, as well as enhanced access to and usage of consumer credit

data and technological tools.

Policy developments. APRA provided an update on a number of policy initiatives, including changes to the related entities framework for banks and other ADIs and proposals to strengthen remuneration requirements across all APRA-regulated entities. The proposed remuneration requirements seek to better align remuneration frameworks with the long-term interests of entities and their stakeholders, and incorporate a recommendation from the Royal Commission on limiting remuneration based on financial metrics. APRA briefed members on the outcomes of its capability review.

Superannuation fund liquidity. The Council considered arrangements for managing liquidity at superannuation funds during periods of market stress. They noted that arrangements had operated as intended during the financial crisis and had since been strengthened. They agreed that existing arrangements provide an appropriate incentive for superannuation funds to manage their liquidity and that circumstances where a systemic liquidity problem could arise for the superannuation system were highly unlikely. Members concluded that no additional measures, including access to liquidity from the Reserve Bank, were warranted.

Financial market infrastructure (FMI). Members discussed key elements of a package of proposed regulatory reforms for FMIs, including some changes to the supervisory framework and a resolution framework for clearing and settlement facilities. The reform package is expected to be released by the Council for consultation later in 2019. The package will seek to modernise and streamline regulators’ supervisory powers and provide new powers to resolve a distressed domestic clearing and settlement facility. Following the consultation, the Council will provide its findings to the Government to assist with policy design and the drafting of legislation.

Stored-value payment facilities. The Council finalised a report to the Government proposing a revised regulatory framework for payment providers that hold stored value. The proposed framework seeks to reduce the complexity of existing regulation, while providing adequate protection for consumers and the flexibility to accommodate innovation. Both the Financial System Inquiry and the Productivity Commission’s inquiry into Competition in the Australian Financial System called for a review of the regulatory framework. The report will be provided to the Government in the near future.

Banks’ offshore funding. The IMF’s recent Financial Sector Assessment Program (FSAP) review of the Australian financial system recommended that Australian regulators encourage a reduction of banks’ use of offshore funding and an extension of the maturity of their borrowings. Members noted that banks manage their risks from offshore borrowing through currency hedging and holding foreign currency liquid assets, and that there are various other factors mitigating the risks. They welcomed the progress that the banks had made in lengthening the maturity of their offshore term debt over recent years. A further lengthening of the maturity of their offshore borrowing would reduce the rollover risk for banks and the broader financial system.

Stablecoins. The Council considered some potential policy implications of so-called ‘stablecoins’ and associated payment services, particularly those linked to large, established networks. A stablecoin is a crypto-asset designed to maintain a stable value relative to another asset, typically a unit of currency or a commodity. Members concluded that elements of the existing regulatory framework, along with the framework proposed for stored-value facilities, were likely to apply to products of this type, but that Australian regulators would need to consider any international regulatory frameworks that might ultimately be established. Council agencies and a number of other Australian regulators are collaborating on their analysis of stablecoins. They are also drawing on their membership of several international groups focused on similar issues. Council members stressed the benefits of having a flexible, technology-neutral regulatory regime in dealing with these and other innovations.

Cyber security and crisis management. The Council reviewed work under way and planned by working groups focused on cyber security and crisis management. One focus of cyber security work in the period ahead will be aligning financial sector efforts with broader initiatives, including those of the Australian Cyber Security Centre and the Government’s 2020 Cyber Security Strategy. Recent work on crisis management in the banking sector has included a joint crisis simulation with New Zealand regulators, focussed on the testing of communications, under the auspices of the Trans-Tasman Council on Banking Supervision.

The RBA released their Financial Stability report today, and even with the rose tinted RBA glasses there are a number of worrying issues touched on. Though none new. But their analysis of negative equity is over optimistic. So we will look at what they say, and highlight some additional considerations.

The RBA said:

Domestic economic conditions remain broadly supportive of financial stability. The unemployment rate has remained around 5 per cent since the previous Review and corporate profit growth has also been strong.

However, GDP growth in Australia also slowed in the second half of 2018. In particular, consumption growth eased and the outlook for consumption is uncertain.

Conditions in the housing market remain weak. Nationally, housing prices are 7 per cent below their late 2017 peak, although they are still almost 30 per cent higher since the start of 2013.

Growth in housing credit was slightly lower over the six months to February than the preceding half year, with investor credit hardly growing at all.

Nationally, falling housing prices have been driven by weaker demand and increased housing supply. The tightening in the supply of housing credit from improved lending standards has played a smaller part. Importantly, these more rigorous lending standards have seen the quality of new loans improve in recent years.

Measures of financial stress among households are generally low and households remain well placed to service their debt given low unemployment, low interest rates and improvements to lending standards. However, there has been an increase in housing loan arrears rates. The increase in arrears has been largest in Western Australia, where the decline in mining related activity has seen housing prices fall for nearly five years and unemployment increase.

They did in “deep dive” on negative equity using their securitised loan data.

Large housing price falls in parts of Australia mean some borrowers are facing negative equity – where the outstanding balance on the loan exceeds the value of the property it is secured against. Negative equity creates vulnerabilities both for borrowers and lenders. A borrower having difficulty making loan repayments who has negative equity cannot fully repay their debt by selling the property. Negative equity also implies that banks are likely to bear losses in the event that a borrower defaults. Evidence from Australia and abroad suggests that borrowers who experience an unexpected fall in income are more likely to default if their loan is in negative equity.

At present, the incidence of negative equity remains low. Given the large increases in housing prices that preceded recent falls and the decline in the share of mortgages issued with high loan to- valuation ratios (LVRs), housing prices would need to fall significantly further for negative equity to become widespread. However, even if this did occur, increased defaults would be unlikely if the unemployment rate remains low, particularly given the improvements in loan serviceability standards over recent years.

Estimating the share of borrowers with negative equity requires data on current loan balances and property values. The RBA’s Securitisation Dataset contains the most extensive and timely data on loan balances and purchase prices.

The Securitisation Dataset includes about one-quarter of the value of

all residential mortgages, or around 1.7 million mortgages.

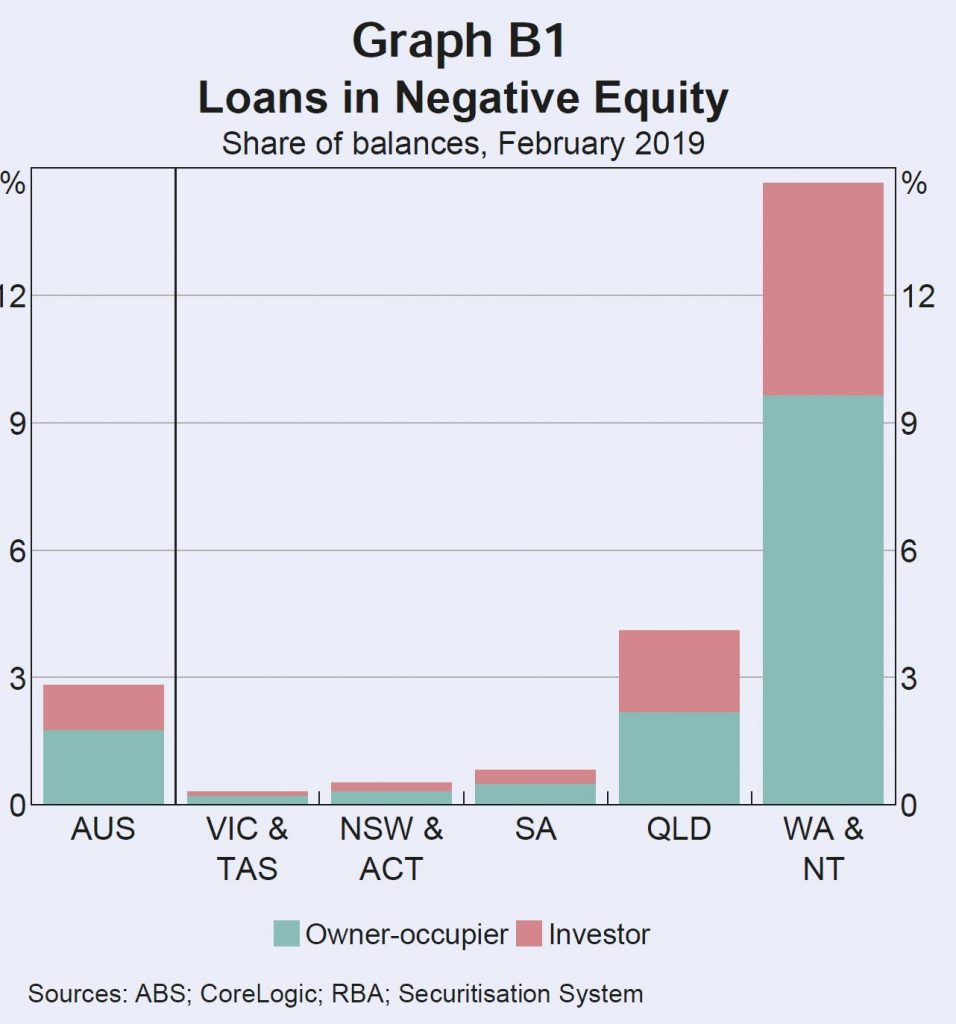

This data can be combined with regional data on housing price movements to estimate the share of loans that are currently in negative equity. This suggests that nationally, around 2¾ per cent of securitised loans by value are in negative equity (just over 2 per cent of borrowers). The highest rates of negative equity are in Western Australia, the Northern Territory and Queensland, where there have been large price falls in areas with high exposure to mining activity. Almost 60 per cent of loans in with negative equity are in Western Australia or the Northern Territory. Rates of negative equity in other states remain very low.

Estimates of negative equity from the Securitisation Dataset may, however, be under or overstated. They could be understated because securitised loans are skewed towards those with lower LVRs at origination. In contrast, the higher prevalence of newer loans in the dataset compared to the broader population of loans, and not being able to take into account capital improvements on values, will work in the other direction. Some private surveys estimate closer to 10 per cent of mortgage holders are in negative equity. However, these surveys are likely to be an overestimate for a number of reasons; for instance, by not accounting for offset account balances.

DFA Says: Of course DFA estimates 10% of households in negative equity, after taking offset balances into account, and also adding in the current forced sale value of the property and transaction costs.

Information from bank liaison and estimates based on 2017 data from the Household Incomes and Labour Dynamics of Australia (HILDA) survey suggest rates of negative equity are broadly in line with those from the Securitisation Dataset.

DFA Says: The HILDA data is at least 2 years old, so before the recent price falls – so this set will understate the current position.

The continuing low rates of negative equity outside the mining exposed regions reflect three main factors: the previous substantial increases in housing prices; the low share of housing loans written at high LVRs; and the fact that many households are ahead on their loans, having accumulated extra principal payments.

Housing prices in some areas of Sydney and Melbourne have fallen by upwards of 20 per cent from their peak in mid to late 2017. But only a small share of owners purchased at peak prices, and many others experienced price rises before property prices began to fall. Properties purchased in Sydney and Melbourne since prices peaked account for around 2 per cent of the national dwelling stock. Looking further back, properties purchased in these two cities since prices were last at current levels still only account for around 4½ per cent of the dwelling stock.

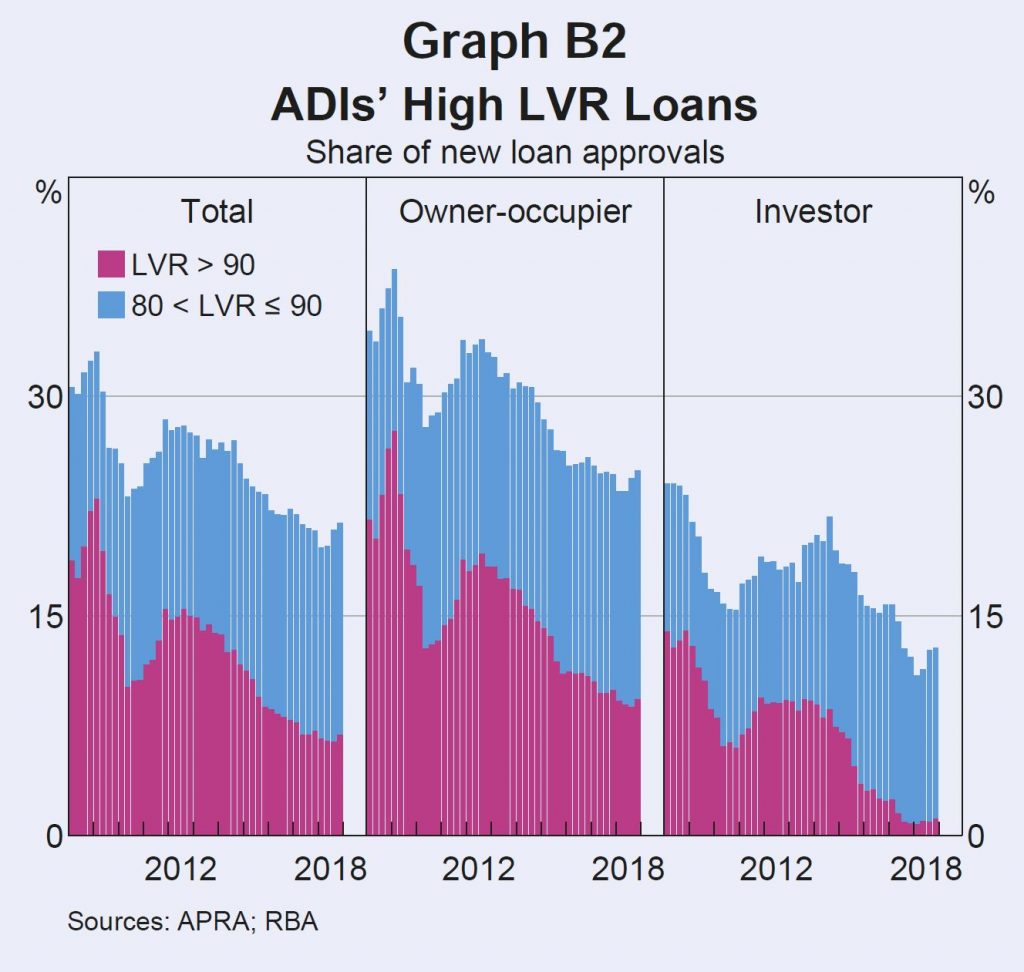

Few recent borrowers had high starting LVRs. Over the past five years, the share of loans issued by ADIs with LVRs above 90 has roughly halved. Since 2017, it has averaged less than 7 per cent (Graph B2). Around 80 per cent of ADI loans are issued with an LVR of 80 or less. Around 15 per cent of owner-occupier borrowers and 20 per cent of investors take out a loan with a starting LVR of exactly 80.

Given most borrowers do not have high starting LVRs, housing price falls need to be large for widespread negative equity. Only 15 per cent of regions have experienced price declines of 20 per cent or more from their peaks. Around 90 per cent of these regions are in Western Australia, Queensland and the Northern Territory.

If a borrower has paid off some of their debt, then price declines will need to be larger still for them to be in negative equity. Most borrowers have principal and interest loans that require them to pay down their debt and many borrowers are ahead of their repayment schedule. Around 70 per cent of loans are estimated to be at least one month ahead of their repayment schedule, with around 30 per cent ahead by two years or more.

When a borrower is behind on repayments and their loan is in negative equity, banks classify the loan as ‘impaired’. Banks are required to raise provisions against potential losses from impaired loans through ‘bad and doubtful debt’ charges. Currently the proportion of impaired housing loans is very low, at 0.2 per cent of all residential mortgages, despite having increased of late (Graph B3).

Queensland, Western Australia and the Northern Territory together account for around 90 per cent of all mortgage debt in negative equity. These states have regions that experienced large and persistent housing price falls over several years.

This has often been coupled with low income growth and increases in unemployment, which have reduced the ability of borrowers to pay down their loans. Loans currently in negative equity were, on average, taken out around five years ago and had higher average LVRs at origination, of around 85 per cent. This made them particularly susceptible to subsequent falls in property values. Investment loans are also disproportionately represented, despite typically having lower starting LVRs than owner-occupier loans. Investors are more likely to take out interest-only loans in order to keep their loan balance high for tax purposes. Around 10 per cent of loans in negative equity have interest only terms expiring in 2019, which is double the share for loans in positive equity. For these borrowers, the increase in repayments from moving to principal and interest may be difficult to manage, especially as loans in negative equity are already more likely to be in arrears. Having more borrowers in this scenario is distressing for the borrowers themselves and for the communities they live in. However, it is unlikely to represent a risk to broader financial stability given it remains largely restricted to mining-exposed regions, which represent a very small share of total mortgage debt.

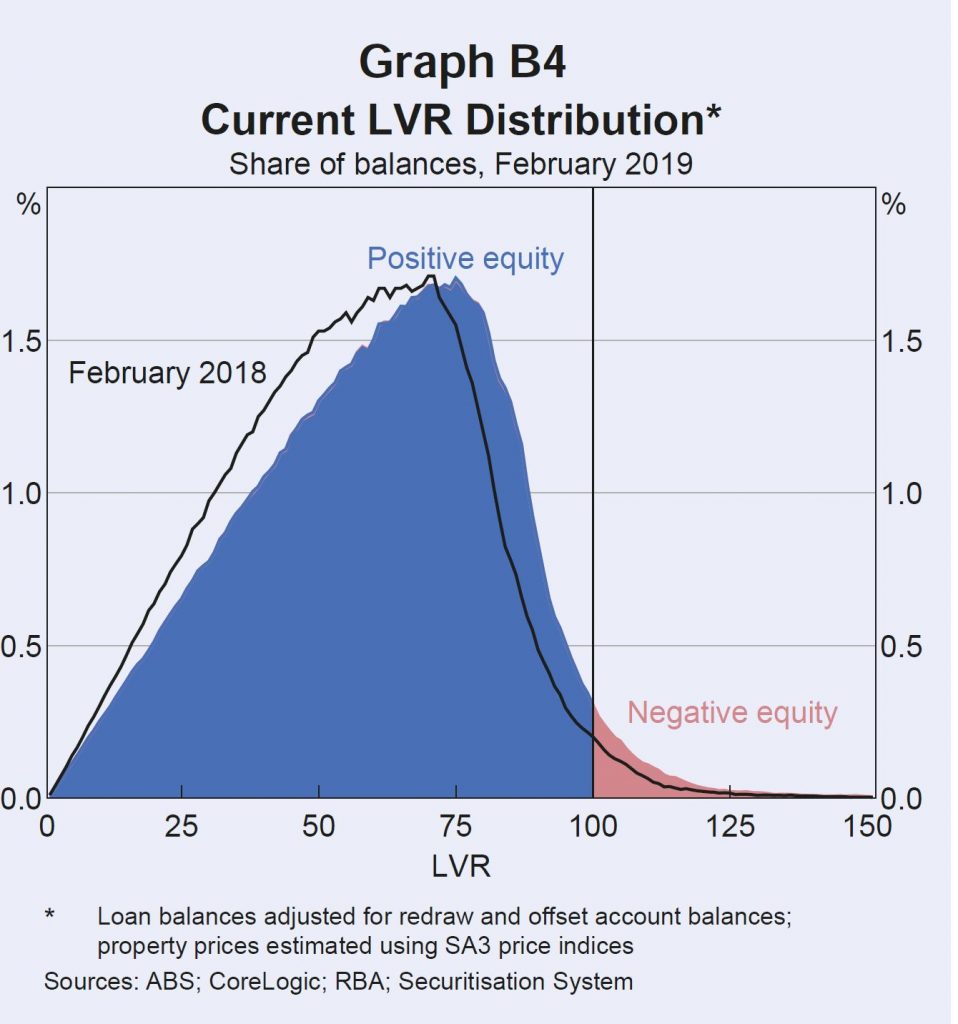

Continued housing price falls would be expected to increase the incidence of negative equity, particularly if they affect borrowers with already high LVRs. Around 11/4 per cent of loans by number (and 13/4 per cent of loans by value) have a current LVR between 95 and 100, making them likely to move into negative equity if there are further housing price falls (Graph B4).

However, compared to the international experience with negative equity during large property downturns, the incidence of negative equity in Australia is likely to remain low. Negative equity peaked in the United States at over 25 per cent of mortgaged properties in 2012 and in Ireland it exceeded 35 per cent, as peak to trough price falls exceeded 30 and 50 per cent respectively.

However, high origination LVRs were far more common in these countries than they have been in Australia.

DFA Says: Except we know there were high levels of mortgage fraud and incorrect data supporting loan applications. Higher than in Ireland.

Even if negative equity was to become more common in the larger housing markets of Sydney and Melbourne, impairment rates for banks are unlikely to increase significantly while unemployment and interest rates remain low.

DFA Says: you need to get post code granular to see what is going on. As our earlier heat map showed.

I will talk about how climate change affects the objectives of monetary policy and some of the challenges that arise in thinking about climate change.

Finally, I will also briefly discuss how climate change affects financial stability.

Let me start by highlighting a few of the dimensions that we need to consider:

We need to think in terms of trend rather than cycles in the weather. Droughts have

generally been regarded (at least economically) as cyclical events that recur every so

often. In contrast, climate change is a trend change. The impact of a trend is

ongoing, whereas a cycle is temporary.

We need to reassess the frequency of climate events. In addition, we need to reassess our

assumptions about the severity and longevity of the climatic events. For example, the

insurance industry has recognised that the frequency and severity of tropical cyclones (and

hurricanes in the Northern Hemisphere) has changed. This has caused the insurance sector to

reprice how they insure (and re-insure) against such events.

We need to think about how the economy is currently adapting and how it will adapt both to

the trend change in climate and the transition required to contain climate change. The

time-frame for both the impact of climate change and the adaptation of the economy to it is

very pertinent here. The transition path to a less carbon-intensive world is clearly quite

different depending on whether it is managed as a gradual process or is abrupt. The trend

changes aren’t likely to be smooth. There is likely to be volatility around the trend,

with the potential for damaging outcomes from spikes above the trend.

Both the physical impact of climate change and the transition are likely to have first-order

economic effects.

Climate Change, Economic Models and Monetary Policy

The economics profession has examined the effects of climate change at least since Nobel Prize

winner William Nordhaus in 1977. Since then, it has become an area of considerably more active

research in the profession.[4]

There has been a large body of research around the appropriate design of policies to address

climate change (such as the design of carbon pricing mechanisms), but not that much in terms of

what it might imply for macroeconomic policies, with one notable exception being the work of

Warwick McKibbin and co-authors.[5]

How does climate affect monetary policy? Monetary policy’s objectives in Australia are full

employment/output and inflation. Hence the effect of climate on these variables is an

appropriate way to consider the effect of climate change on the economy and the implications for

monetary policy. The economy is changing all the time in response to a large number of forces.

Monetary policy is always having to analyse and assess these forces and their impact on the

economy. But few of these forces have the scale, persistence and systemic risk of climate

change.

A longstanding way of thinking about monetary policy and economic management is in terms of

demand and supply shocks.[6]

A positive demand shock increases output and increases prices. The monetary policy response to a

positive demand shock is straightforward: tighten policy. Climate events have been good examples

of supply shocks. Indeed, droughts are often the textbook example used to illustrate a supply

shock. A negative supply shock reduces output but increases prices. That is a more complicated

monetary policy challenge because the two parts of the RBA’s dual mandate, output and

inflation, are moving in opposite directions. Historically, the monetary policy response has

been to look through the impact on prices, on the presumption that the impact is temporary. The

banana price episode in 2011 after Cyclone Yasi is a good example of this. The spike in banana

prices and inflation was temporary, although quite substantial. It boosted inflation by 0.7

percentage points. The Reserve Bank looked through the effect of the banana price rise on

inflation. After the banana crop returned to normal, prices settled down and inflation returned

to its previous rate.

The response to such a shock is relatively straightforward if the climate events are temporary

and discrete: droughts are assumed to end; the destruction of the banana crop or the closure of

the iron ore port because of a cyclone is temporary; things return to where they were before the

climate event. That said, the output that is lost is generally lost forever. It is not made up

again later, but rather output returns to its former level.

The recent IPCC report documents that climate change is a trend rather than cyclical, which makes the assessment much more complicated. What if droughts are more frequent, or cyclones happen more often? The supply shock is no longer temporary but close to permanent. That situation is more challenging to assess and respond to.

Climate Change and Financial Stability

Having talked about the macroeconomic impact of climate change and how that might affect monetary

policy, I will briefly discuss climate through the lens of financial stability implications.[10] Financial

stability is also a core part of the Reserve Bank’s mandate. Challenges for financial

stability may arise from both physical and transition risks of climate change. For example,

insurers may face large, unanticipated payouts because of climate change-related property damage

and business losses. In some cases businesses and households could lose access to insurance.

Companies that generate significant pollution might face reputational damage or legal liability

from their activities, and changes to regulation could cause previously valuable assets to

become uneconomic. All of these consequences could precipitate sharp adjustments in asset

prices, which would have consequences for financial stability.

The reason that I will only cover the implications of climate change for financial stability only

briefly today is that it has been very eloquently discussed by Geoff Summerhayes (APRA) and John

Price (ASIC) including at this forum over the past two years.[11] I would very much

endorse the points that Geoff and John have made. Geoff stresses the need for businesses,

including those in the financial sector to implement the recommendations of the Task Force for

Climate-related Financial Disclosures (TCFD).[12]

I strongly endorse this point. We have seen progress on this front in recent years, but there is

more to be done. Financial stability will be better served by an orderly transition rather than

an abrupt disorderly one.

One area that Geoff highlighted in a recent speech is that there is a data gap which needs to be

addressed:[13] ‘The

challenge governments, regulators and financial institutions face in responding to the

wide-ranging impacts of climate change is to make sound decisions in the face of uncertainty

about how these risks will play out.’ In that regard, Geoff mentions one challenge that I

spoke about earlier in the context of monetary policy. Namely, taking the climate modelling and

mapping that into our macroeconomic models. For businesses and financial markets, that challenge

is understanding the climate modelling and conducting the scenario analysis to determine the

potential impact on their business and investments.

He gave APRA a good wrap for is progress on the Basel based supervisory framework. His comments on their mortgage sector interventions were, well, interesting (I would say, too little too late!).

In 2014, we initiated a quite intensive supervisory effort to lift and reinforce lending standards. Our concern was that due to strong competitive pressures, policies were not suitably calibrated to the Australian environment at the time – one of high and rising house prices, high household debt, subdued household income growth and historically low interest rates. We issued additional supervisory guidance, and allocated significant resources to ensure lending policies were suitably aligned with it. Unfortunately, this provided evidence that strong incentives to grow profit and market share often saw lenders weaken and/or override policies in order to generate sales. Moreover, the dangers did not seem to be strongly called out by compliance and audit functions.

To me, the perspective he paints is still far too narrow in terms of really tacking financial stability, Basel is but one element, not the universe!

Here is his introduction…

Translating prudential policy into prudent practice

I’ve been asked to speak this morning about the challenge of translating prudential policy into prudent practice. From a global perspective, that’s an important issue to focus on because policy reform will mean little if it does not translate into improved practices and behaviours.

Translating global reform proposals to improved banking practice is a four-step process:

global reforms have to be agreed as international standards;

agreed international standards then need to be translated into domestic regulation;

bank policies, systems and frameworks then have to be modified to comply with new regulations; and

actual banking behaviours and practices need to adjust to a new set of constraints on the way business is done.

The first of these steps is pretty much complete. A decade on

from the financial crisis, the marathon international policy-making

efforts to restore and protect the resilience of the global banking

system have, by and large, reached the finish line. Greatly strengthened

risk-based capital requirements, a supplementary leverage ratio, with

additional buffers for systemically important banks, liquidity and

funding requirements in the form of the Liquidity Coverage Ratio (LCR)

and the Net Stable Funding Ratio (NSFR), tighter large exposure limits

and new margining requirements for OTC derivatives, and an enhanced

disclosure regime provide a comprehensive package of prudential policy

reforms. The Basel Committee has worked long and hard, and should be

commended for the final product.

The Basel Committee’s output –

besides lots of paper! – are agreements on the design and calibration of

minimum standards. Those agreements are critical to global financial

stability. Unfortunately, they are not worth the paper they are written

on if they are not translated into domestic regulation by member

jurisdictions – the second step in the process I referred to earlier. To

repeat the frequent exhortations of the G20 leaders, to achieve the

desired objective of a resilient global financial system the reforms

need to be implemented in a “full, timely and consistent manner”.

A quick look at the Basel Committee’s latest implementation monitoring report shows something of a mixed scorecard. While the core Basel III risk-based capital requirements and the LCR are largely in force around the world, there has been less progress in some other areas: many requirements are subject to lengthy transitional periods, implementation of the NSFR has been disappointingly slow in a number of jurisdictions, and margining and disclosure requirements can be described as a little patchy.

In short, not all commitments to act have been met by

action. That is disappointing. While some delays and trade-offs are

valid, on occasion it appears to reflect a regulatory version of the

“first mover disadvantage” that supervisors often criticise the industry

for – jurisdictions not wanting to do the right thing and move promptly

because of a concern that other jurisdictions may not follow suit. This

reveals a disappointing penchant to put the interests of banks and

their shareholders above that of their depositors and the broader

community – something that prudential supervisors must constantly guard

against.

For our part, we’ve made good progress on the financial

reform agenda in Australia. While the banking sector here escaped the

worst of the crisis a decade ago, that didn’t mean APRA was complacent

about the importance of building resilience. The core capital, liquidity

and funding reforms of Basel III are all in place, with a conservative

overlay in many areas. Moreover, we have done this without the extensive

transitional periods that have been necessary in other parts of the

world. I acknowledge, though, that we don’t have a perfect record and

still have a few gaps to close, such as the enhanced Pillar III

disclosure requirements. We are committed to addressing these as soon as

we can.

Blog")